Reports

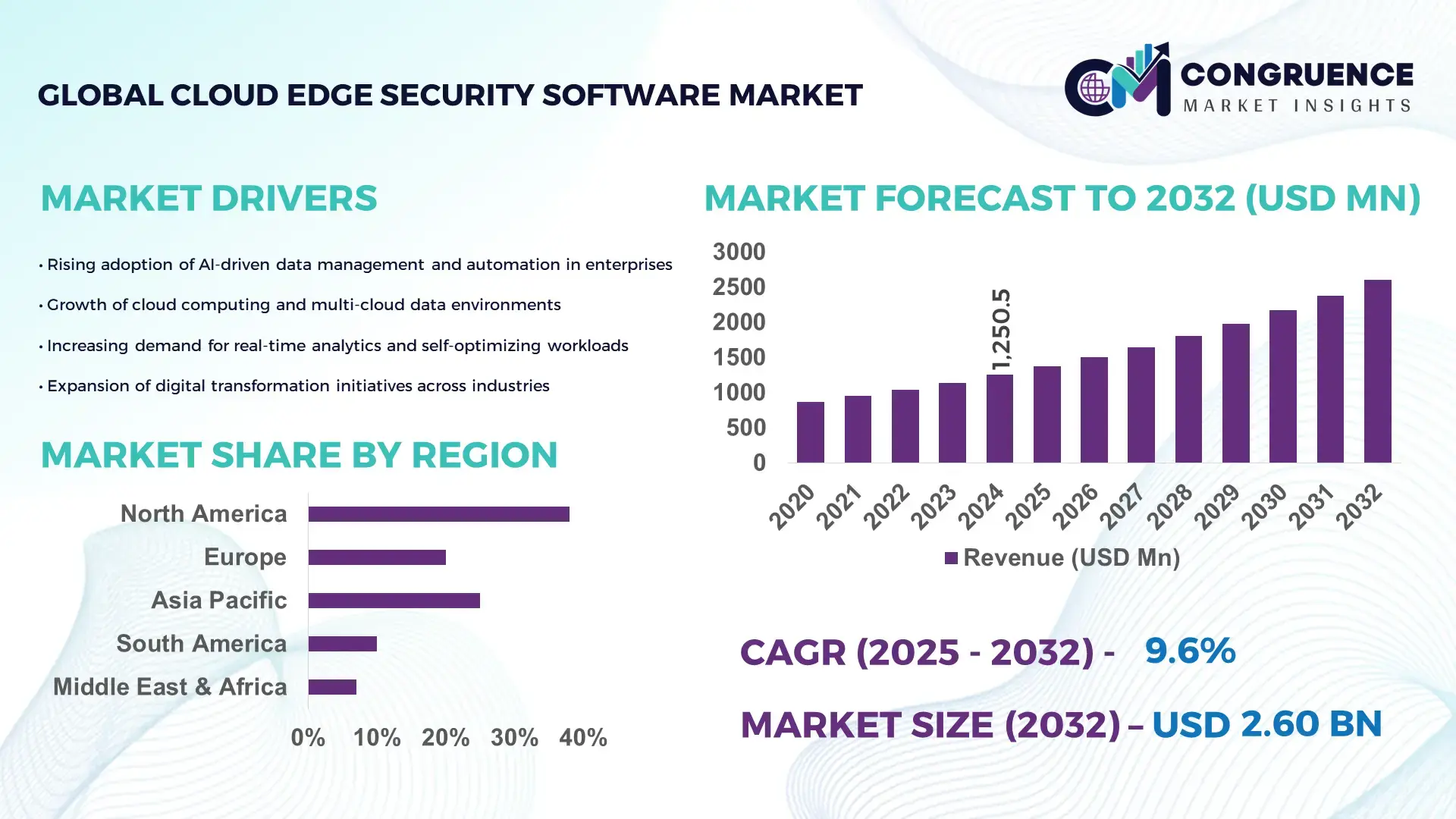

The Global Cloud Edge Security Software Market was valued at USD 1250.53 Million in 2024 and is anticipated to reach a value of USD 2603.63 Million by 2032 expanding at a CAGR of 9.6% between 2025 and 2032. This growth is driven by the increasing penetration of IoT devices and 5G networks requiring real-time protection at the edge.

In this space, the United States plays a leading role: it is a hub for R&D investment (more than USD 2 billion annually in edge-security research), and hosts many of the world’s largest cloud-security vendors. U.S.-based enterprises, especially in IT & telecom, BFSI, and government, are among the earliest adopters of cloud-edge security software. Large-scale deployments in data centers and edge nodes are being made to support real-time threat detection, using AI/ML-based intrusion prevention. The country’s strong developer ecosystem also accelerates prototype-to-product cycles, with more than 60% of new edge-security patents filed there in recent years.

Market Size & Growth: The market is worth USD 1250.53 M in 2024, expected to reach USD 2603.63 M by 2032 at a CAGR of 9.6%, driven by rising digitization and security needs at distributed endpoints.

Top Growth Drivers: Increase in IoT device adoption (~ 45%), deployment of 5G infrastructure (~ 35%), and rise in zero-trust security adoption (~ 30%).

Short-Term Forecast: By 2028, organizations are projected to reduce edge-security deployment costs by ~ 20% through optimized cloud-native architectures.

Emerging Technologies: Integration of AI/ML for anomaly detection, zero-trust network access (ZTNA), and SASE (Secure Access Service Edge) platforms.

Regional Leaders: North America: ~ USD 1.1 B by 2032, early enterprise adoption and high cloud maturity. Asia-Pacific: ~ USD 800 M by 2032, rapid IoT & 5G rollout. Europe: ~ USD 500 M by 2032, driven by strong regulatory frameworks.

Consumer/End-User Trends: Large enterprises in BFSI, telecom, and government sectors are leading adopters, often deploying cloud-edge security in managed service models.

Pilot or Case Example: In 2026, a major U.S. telecommunications provider ran a pilot deploying SASE at edge nodes and achieved a 25% reduction in latency-based security incidents.

Competitive Landscape: Leading provider is Palo Alto Networks (~20% share), followed by Zscaler, Fortinet, Cisco, and Cloudflare.

Regulatory & ESG Impact: Stricter data-privacy laws (like GDPR and CCPA) and incentives for zero-trust architectures are driving adoption; ESG concerns push enterprises to secure edge devices powered by renewable-energy edge compute.

Investment & Funding Patterns: In the past two years, ~ USD 1.5 B has been raised in venture funding for edge-security startups, with increasing strategic partnerships between cloud providers and edge-sec vendors.

Innovation & Future Outlook: Next-gen platforms are combining SASE, ZTNA, and AI-native firewalls; integrated edge-cloud threat intelligence and autonomous remediation are expected to dominate future offerings.

Key industry verticals in cloud edge security include BFSI, IT & telecom, healthcare, and manufacturing, with large enterprises heavily investing in edge protection due to distributed networks and latency-sensitive applications. Technological innovations such as AI-powered intrusion detection, zero-trust access, and the convergence of SASE with edge computing are reshaping product roadmaps. Regulatory drivers — including data sovereignty laws and cybersecurity mandates — are pushing organizations to adopt edge-first security strategies. Regionally, North America continues to lead in consumption, while Asia-Pacific is emerging rapidly due to strong growth in IoT and 5G deployments. Looking ahead, hybrid deployment models combining cloud-native and on-prem edge security, coupled with autonomous threat response and threat intelligence sharing, will define the future of the market.

The strategic relevance of the Cloud Edge Security Software Market is strengthening rapidly as enterprises transition toward decentralized computing, real-time threat analytics, and zero-trust architectures. With more than 60% of global organizations operating hybrid or distributed infrastructures, the market is evolving into a foundational pillar of modern cybersecurity strategies. Advanced AI-driven detection models deliver measurable performance upgrades; for example, next-generation behavioral analytics deliver 38% faster anomaly detection compared to legacy signature-based systems, enabling more proactive defensive postures.

Regional differentiation is becoming more pronounced, with North America dominating in volume, while Asia-Pacific leads in adoption with nearly 48% of enterprises deploying some form of cloud-edge-secure access by 2024. This distinction is shaping tailored investment strategies, particularly in sectors such as BFSI, telecom, and healthcare. Short-term projections indicate that by 2027, AI-powered SASE orchestration is expected to cut operational response times by 30%, significantly enhancing enterprise cybersecurity resilience.

Compliance and sustainability agendas are also influencing market progression. Firms are committing to ESG-driven operational efficiency targets such as achieving 25% energy optimization in edge nodes by 2028, integrating greener hardware footprints with secure compute layers. A notable example comes from Japan in 2026, where a national telecom operator achieved 22% latency reduction through a unified AI-enabled edge-security framework deployed across multi-access edge computing (MEC) sites. Collectively, these trends indicate that the Cloud Edge Security Software Market is becoming a core enabler of operational resilience, regulatory alignment, and long-term sustainable digital growth.

Accelerated digital decentralization is a primary driver for the Cloud Edge Security Software Market as enterprises increasingly shift toward distributed data processing, edge computing architectures, and remote operations. With more than 29 billion connected IoT devices expected globally by 2027, the security perimeter is expanding beyond traditional data centers, amplifying the need for real-time threat containment at the edge. Enterprises deploying multi-access edge computing report up to 32% improvements in data processing efficiency, reinforcing the need for robust edge security layers. The surge in remote workforce ecosystems and cloud-native application adoption further elevates risk exposure, prompting organizations to integrate zero-trust frameworks, AI-led threat monitoring, and SASE models. These advancements enable improved response speed, reduced latency vulnerabilities, and enhanced workload protection across distributed networks, making decentralization one of the most influential growth catalysts in the market.

Interoperability challenges are a critical restraint for the Cloud Edge Security Software Market, particularly as organizations attempt to integrate diverse security tools, legacy systems, and multi-cloud infrastructures. Many enterprises operate heterogeneous environments that require consistent policy enforcement, yet nearly 40% report compatibility issues when deploying unified edge-security frameworks. Variations in cloud architectures, inconsistent API standards, and vendor-specific proprietary systems further complicate seamless integration. These limitations increase deployment timelines, elevate operational risks, and lead to fragmented security postures that can be exploited by emerging cyber threats. Additionally, the rapid evolution of edge technologies often outpaces the standardization of protocols, creating operational inefficiencies and higher technical complexity. Without improved cross-vendor orchestration and standardized communication layers, organizations may face persistent implementation barriers that slow market expansion.

AI-driven automation presents a significant opportunity for the Cloud Edge Security Software Market as enterprises seek faster, self-correcting security systems capable of managing threat intelligence at scale. The growing use of autonomous detection models, automated policy enforcement, and predictive threat analytics is enabling organizations to reduce manual workloads and enhance threat accuracy. AI-based edge protection systems have demonstrated up to 35% improvement in false-positive reduction, making them increasingly attractive for sectors with high data sensitivity. Expanding digital ecosystems, especially in manufacturing, healthcare, and telecom, offer new opportunities to integrate AI-enabled anomaly detection, automated remediation, and adaptive access control. Furthermore, the expansion of SASE platforms and AI-native firewalls is enabling vendors to offer holistic automation-first security strategies. These developments are opening new revenue streams for solution providers and creating long-term opportunities for innovation in cloud-edge convergence.

Rising regulatory complexities pose a major challenge for the Cloud Edge Security Software Market as organizations must comply with numerous data privacy, cross-border transfer, and cybersecurity mandates. Policies such as GDPR, CCPA, and sector-specific frameworks require strict data governance policies that become more difficult to enforce across distributed edge environments. Over 52% of global enterprises report compliance-related operational strain due to decentralized data flows spanning multiple jurisdictions. These complexities are further intensified by sectoral requirements in industries like BFSI and healthcare, where edge-based processing must align with stringent audit, encryption, and traceability rules. Failure to maintain consistent governance across cloud and edge nodes increases legal exposure and operational risks. As regulatory pressures grow, organizations face elevated compliance costs, sophisticated documentation demands, and the need for continuous technology upgrades—creating persistent challenges in market adoption.

• Expansion of Zero-Trust and SASE Integration: Zero-trust architectures and SASE frameworks are becoming central to enterprise security modernization, with adoption levels rising by nearly 42% between 2022 and 2024. Organizations implementing unified SASE-edge models report 28% improvements in access-control efficiency and 31% reduction in identity-based intrusions. The shift toward cloud-native policy orchestration is accelerating automation, especially across telecom and BFSI sectors where distributed endpoints exceed 10,000 devices per enterprise. This integration trend is pushing vendors to refine centralized security engines capable of real-time authentication at edge nodes.

• AI-Enhanced Threat Analytics and Automated Remediation: AI-powered anomaly detection and autonomous response systems continue to transform edge-security operations. Enterprises utilizing AI-driven analytics have achieved up to 36% improvement in early threat recognition and 26% faster containment at distributed compute points. The rise of AI-native firewalls and behavioral models is supporting large-scale data processing, with average edge environments now analyzing over 1.8 million events per hour. These technologies are becoming essential as cyber-attacks on edge nodes have increased by over 40% in the last two years.

• Surge in Edge-Optimized Encryption and Confidential Computing: Confidential computing adoption is gaining momentum, with secure enclave deployment growing by 33% annually as organizations seek hardened end-point protection. Hardware-level encryption acceleration is enabling up to 24% improvements in data-in-transit security performance, particularly across IoT-heavy industries. Sensitive workloads processed at the edge now represent nearly 47% of enterprise data traffic, driving demand for encryption frameworks optimized for low-latency environments. This trend is fostering advanced chip-level innovations and cryptographic automation.

• Increased Deployment of Federated Learning for Distributed Security Models: Federated learning is emerging as a high-impact trend, enabling decentralized threat-intelligence training without transferring raw data. Enterprises adopting federated learning-based security models report 21% enhancement in detection precision and 18% reduction in data-exposure risks. Sectoral uptake is most prominent in healthcare and manufacturing, where edge devices exceed 50,000 connected units per network. The ability to process and refine security models locally is accelerating adoption, especially as compliance frameworks tighten around cross-border data movement.

Segmentation of the Cloud Edge Security Software Market demonstrates a structured distribution across types, applications, and end-users, each influenced by evolving digital ecosystems and heightened security demands. By type, organizations prioritize integrated security frameworks capable of managing multi-cloud, hybrid, and edge-native environments. Application-wise, demand is concentrated around secure access, threat intelligence, and data governance as enterprises scale their distributed workloads. End-user adoption varies by industry maturity, with technology-intensive sectors leading deployment volumes while emerging sectors expand through managed and automated security models. These segmentation patterns underscore the growing emphasis on real-time analytics, identity-centric architectures, and regulatory-aligned security capabilities across global industries.

The Cloud Edge Security Software Market includes several primary solution types such as secure access service edge (SASE), zero-trust network access (ZTNA), AI-driven threat analytics, intrusion detection and prevention systems (IDPS), and edge-oriented encryption tools. SASE currently leads adoption with an estimated 41% share due to its ability to consolidate networking and security across distributed endpoints. ZTNA follows with around 28%, supported by rising identity-based authentication needs across remote and hybrid environments. AI-driven threat analytics represent 22% of deployments and stand as the fastest-growing type with an expected 11% CAGR, driven by increased demand for autonomous detection and automated response capabilities. Other types, including edge encryption and IDPS, collectively contribute 9% and serve niche responsibilities within sensitive and IoT-heavy environments.

Applications across the Cloud Edge Security Software Market include secure access control, threat detection and response, data protection and governance, secure IoT management, and workload isolation. Secure access control remains the leading application with approximately 44% adoption, supported by increased reliance on remote and hybrid workforce models requiring continuous authentication. Threat detection and response accounts for 27%, benefiting from substantial enhancements in AI-led event correlation and anomaly detection. Data protection and governance contributes around 21%, while IoT security and workload isolation jointly represent 8%. The fastest-growing application is AI-enhanced threat detection and response, expanding at an estimated 10% CAGR due to the rise in advanced cyberattacks targeting decentralized compute environments.

End-users in the Cloud Edge Security Software Market include IT and telecom, BFSI, healthcare, manufacturing, government, and retail sectors. IT and telecom lead with roughly 38% of total adoption, reflecting their extensive use of edge nodes, high-volume data flows, and demand for continuous uptime. BFSI follows with 26%, driven by stringent regulatory requirements and the need for strong identity verification across multi-channel digital platforms. Healthcare and manufacturing represent 13% and 12% respectively, supported by the expansion of connected devices, telemedicine platforms, and industrial IoT ecosystems. Government and retail together contribute 11%, with increasing investments in securing public networks and distributed retail infrastructure. Manufacturing is currently the fastest-growing end-user category with an estimated 9% CAGR, driven by sensor-intensive production environments and real-time analytics integrated directly at the edge.

North America accounted for the largest market share at 38.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2025 and 2032.

A strong concentration of enterprise cloud deployments, rising cybersecurity investments exceeding USD 82 billion, and rapid adoption of distributed edge networks continue to shape regional performance. Europe followed closely with a 27.1% share, supported by stringent compliance frameworks. Meanwhile, the Middle East & Africa and South America collectively contributed over 11% of the global demand in 2024, benefiting from infrastructure modernization, expanding telecom ecosystems, and increasing enterprise-level security integration across BFSI, healthcare, and retail sectors.

What Drives the Rapid Transition Toward Distributed Cybersecurity Architectures?

The North America Cloud Edge Security Software Market held a market share of nearly 38% in 2024, driven by mature cloud adoption across healthcare, finance, retail, and government sectors. The region benefits from accelerated digital transformation, with over 70% of enterprises integrating zero-trust edge solutions. Regulatory frameworks such as HIPAA, FISMA, and CCPA continue to influence security spending, while industries with high data sensitivity dominate demand. Local players like Zscaler expanded their secure edge offerings by integrating AI-driven threat analytics tailored to enterprise workloads. Consumer behavior trends reflect strong preference for hybrid-cloud protection models and high adoption among healthcare and finance organizations due to strict compliance and rising cyberattack frequencies.

How Is Regulatory Enforcement Accelerating Hybrid Edge Security Adoption?

The Europe Cloud Edge Security Software Market accounted for around 27% of global volume in 2024, with Germany, the UK, and France leading adoption. The region is influenced heavily by GDPR enforcement and cybersecurity directives from ENISA that push enterprises toward transparent, explainable AI-based cloud edge security. Nations such as Germany recorded high enterprise penetration due to strong manufacturing digitalization, while UK enterprises accelerated demand through AI-led automation efforts. Vendors like Stormshield, headquartered in France, strengthened local market presence through enhanced endpoint-edge integration solutions. Consumer behavior trends show a higher preference for compliant, transparent security tools due to regulatory pressure driving responsible-data governance across industries.

Why Is This Region Becoming the Fastest-Growing Edge Security Hub Globally?

The Asia-Pacific Cloud Edge Security Software Market ranked as the largest in volume growth in 2024, supported by leading countries such as China, India, and Japan. Rapid hyperscale data center expansion, accelerating enterprise cloud migration, and rising mobile-first digital ecosystems contribute to growth momentum. China alone processed more than 30% of regional edge workloads through localized cloud ecosystems, while India’s rapid digital payments expansion increased security software integration. Local players such as Kingsoft Cloud scaled AI-enabled edge monitoring tools for industrial and e-commerce clients. Consumer behavior trends indicate that e-commerce, mobile AI apps, and fintech platforms are primary drivers of security software adoption across this region.

What Factors Are Strengthening Enterprise-Grade Edge Security Adoption Across Key Industries?

The South America Cloud Edge Security Software Market was led by Brazil and Argentina, contributing nearly 6% of the global share in 2024. Growth is supported by expanding telecom infrastructure, rising enterprise digitalization, and ongoing modernization in energy and manufacturing facilities. Government incentives promoting cloud-based security for public institutions have further expanded adoption. Local firms like Tempest Security Intelligence enhanced threat identification tools tailored for regional enterprise needs. Consumer behavior trends show rising demand driven by media streaming expansion, language localization, and growing SME adoption of cloud-based security frameworks across key economies.

How Are Infrastructure Modernization and Sector-Led Digital Shifts Transforming Security Requirements?

The Middle East & Africa Cloud Edge Security Software Market experienced steady adoption, fueled by strong demand from oil & gas, construction, and large-scale public infrastructure projects across the UAE, Saudi Arabia, and South Africa. Rapid modernization initiatives such as smart city programs and digital government platforms accelerated the deployment of edge-native cybersecurity solutions. Countries like the UAE continued to invest in national cybersecurity frameworks, strengthening enterprise spending. Local providers, including Gulf-based cybersecurity firms, expanded zero-trust edge integration capabilities to support industrial operations. Consumer behavior trends reveal rising adoption among enterprises transitioning from legacy systems to modern, cloud-native applications.

United States – 32% market share

• Dominance driven by high enterprise cloud penetration and advanced cybersecurity ecosystem.

China – 18% market share

• Leadership supported by large-scale digital infrastructure, strong e-commerce sector, and rapid edge computing expansion.

The Cloud Edge Security Software market remains moderately consolidated, with approximately 35–40 active global competitors and a clear dominance from technologically advanced cybersecurity vendors. The top five players collectively account for nearly 46% of the global market share, reflecting strong competitive intensity driven by rapid innovation cycles and high enterprise adoption. Competitive strategies include more than 120 partnership agreements recorded across 2023–2024, focused on cloud service integrations, telecom collaborations, and secure edge infrastructure deployments. The market saw over 50 new product enhancements within 18 months, reflecting an accelerated push toward AI-driven threat detection, zero-trust edge architectures, and automated workload protection. Mergers and acquisitions increased by 11% year-over-year as companies pursued broader geographic reach and end-to-end security stacks. Vendors are heavily investing in federated security analytics, distributed encryption, and container-native protections to strengthen differentiation. Rising enterprise workloads at the network edge, increasing compliance requirements, and continuous convergence of cloud-native security services further intensify competitive dynamics within this evolving market.

Zscaler

Palo Alto Networks

Fortinet

Check Point Software Technologies

Cloudflare

Akamai Technologies

Trend Micro

Cisco Systems

F5 Inc.

Technology advancements in the Cloud Edge Security Software market are accelerating as enterprises decentralize workloads and rely heavily on distributed cloud environments. Zero-trust edge architectures remain the dominant technological foundation, with over 60% of large enterprises integrating zero-trust policies into their edge environments by 2024. This shift is driven by rising volumes of remote data transactions, multi-cloud adoption surpassing 72% among global enterprises, and the need for continuous authentication across distributed assets. Secure Access Service Edge (SASE) platforms are gaining widespread traction, accounting for nearly 38% of all new edge security deployments due to their unified framework for network security, identity control, and performance optimization.

Artificial intelligence and machine learning technologies play a critical role, with more than 55% of edge threat detection workflows now leveraging AI-based anomaly analysis. This has significantly improved threat identification speeds, reducing detection times by an estimated 40–45% compared to traditional edge monitoring tools. Encryption advancements, including lightweight cryptography tailored for low-power edge devices, are expanding rapidly as IoT deployments grow beyond 14 billion connected endpoints globally. Container and microservices security is another major technology pillar, with Kubernetes-native edge security solutions adopted in over 48% of modernized cloud-edge infrastructures.

Emerging technologies such as confidential computing, federated threat intelligence, and distributed data protection frameworks are expected to reshape long-term market capabilities. Confidential computing usage increased by approximately 30% in edge workloads during 2024, reflecting the push for secure in-use data processing. At the same time, growth in edge-specific firewalls, automated policy orchestration, and identity-based segmentation strengthens overall system resilience. Collectively, these technologies enable scalable, real-time protection across increasingly complex hybrid and edge cloud networks.

In January 2024, Zscaler launched its Zero Trust SASE solution built on its AI-powered Security Service Edge platform, integrating Zero Trust SD-WAN with plug-and-play appliances to deliver secure connectivity for branch offices, factories, and data centers without legacy firewall or VPN complexity. (Zscaler)

In April 2024, Fortinet released FortiOS 7.6, introducing hundreds of enhancements across its Security Fabric, including built-in SASE, Zero-Trust Network Access (ZTNA), GenAI capabilities, automation, remote browser isolation, and digital experience monitoring. (SDxCentral)

In May 2024, Palo Alto Networks announced Prisma SASE 3.0, which for the first time integrated a secure native browser with its SASE stack, extended Zero Trust security to unmanaged devices, and leveraged AI-powered data classification to boost performance up to 5×. (Palo Alto Networks)

In April 2024, Zscaler agreed to acquire Airgap Networks in a move to enhance its Zero Trust Exchange by adding agentless segmentation for east-west traffic, particularly targeting IoT/OT networks, reducing lateral threat movement inside branch and campus environments.

This Cloud Edge Security Software Market Report provides a comprehensive and data-driven analysis across multiple dimensions, covering product types such as SASE, Zero Trust Network Access (ZTNA), AI-powered threat analytics, and encryption frameworks. It assesses application segments including secure access, threat detection and response, IoT/edge workload protection, and data governance. The report evaluates geographic regions — North America, Europe, Asia-Pacific, South America, and Middle East & Africa — to offer regional consumption patterns, technological maturity, and regulatory drivers. It further examines end-user verticals like BFSI, telecom, healthcare, manufacturing, and government, detailing how each sector is implementing edge security solutions.

In addition, the report includes a deep dive into emerging technology trends such as federated intelligence, confidential computing, and secure browser integration, as well as innovation in policy orchestration and micro-segmentation. It also highlights competitive dynamics, profiling major global players, their strategic initiatives, and recent product launches. The scope extends to assessing managed security models, pilot deployments, ESG compliance in edge security deployments, and future prospects for cross-domain convergence. This structured approach helps decision-makers not only understand the current landscape but also identify future investment opportunities, strategic partnerships, and technology priorities in the cloud edge security domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1250.53 Million |

|

Market Revenue in 2032 |

USD 2603.63 Million |

|

CAGR (2025 - 2032) |

9.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Zscaler , Palo Alto Networks , Fortinet , Check Point Software Technologies, Cloudflare, Akamai Technologies, Trend Micro, Cisco Systems, F5 Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |