Reports

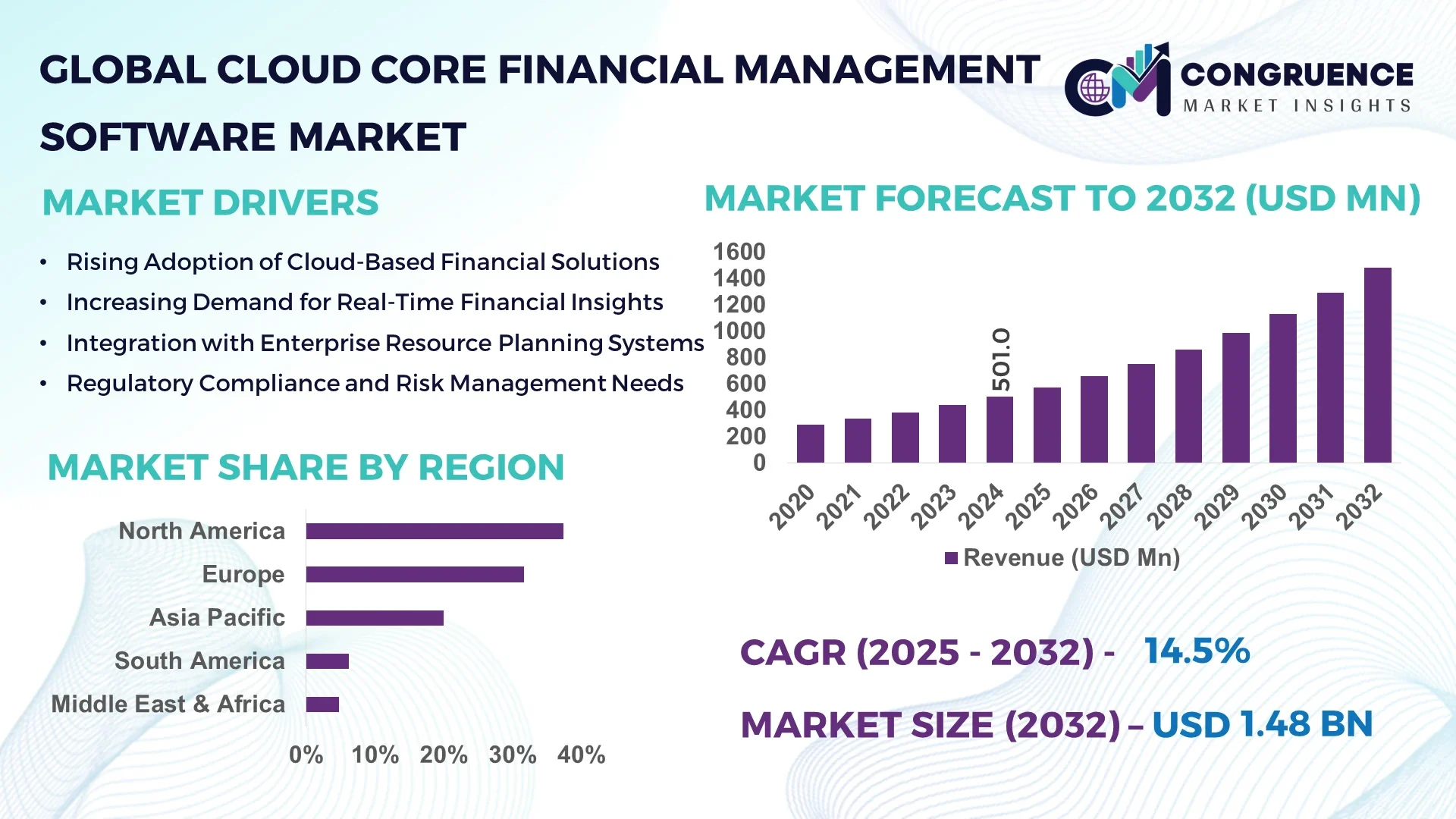

The Global Cloud Core Financial Management Software Market was valued at USD 501 Million in 2024 and is anticipated to reach a value of USD 1,480.1 Million by 2032 expanding at a CAGR of 14.5% between 2025 and 2032. This growth is driven by accelerating enterprise digitization, shift from on-premise to SaaS, and heightened regulatory demands for financial transparency.

In the United States, the dominant country in this space, annual investment in cloud financial platforms exceeded USD 1.2 billion in 2023 alone, with more than 70% of Fortune 500 firms deploying or upgrading cloud-native core financial solutions. U.S. firms have driven technological leadership with machine-learning forecasting modules processing over 3 trillion transactional entries annually, and regularly pilot blockchain-based automated reconciliation in large banks. The U.S. also leads in segmentation adoption: nearly 65% of cloud core deployments serve manufacturing, insurance, and financial services verticals, and consumer adoption for mid-market ERPs in states such as California and Texas exceeds 45%.

Market Size & Growth: USD 501 Million in 2024, projected USD 1,480.1 Million by 2032, CAGR ~14.5% — driven by digital transformation and compliance pressures

Top Growth Drivers: cloud adoption surge (42 %), process automation efficiency (34 %), regulatory compliance demand (24 %)

Short-Term Forecast: By 2028, financial process automation is expected to cut operational costs by 18 % and reduce month-end close times by 22 %

Emerging Technologies: AI/ML financial forecasting, blockchain-based reconciliation, embedded analytics in ERP

Regional Leaders: North America (~USD 580 Million by 2032), Europe (~USD 350 Million by 2032), Asia Pacific (~USD 300 Million by 2032) — with Asia Pacific showing fastest year-on-year deployment growth

Consumer/End-User Trends: Mid-size firms increasingly favor subscription SaaS; adoption in banking, fintech, insurance rising rapidly

Pilot or Case Example: In 2025, a U.S. bank cut reconciliation time by 40 % using an AI-based cloud core module pilot

Competitive Landscape: Market leader holds ~22 % share, with key competitors including Workday Financials, Oracle Cloud ERP, SAP S/4HANA Cloud, Sage Intacct

Regulatory & ESG Impact: Stricter financial transparency rules (e.g. XBRL mandates), carbon reporting requirements pushing integration

Investment & Funding Patterns: Over USD 350 million in venture funding into fintech/ERP startups in 2024, increasing strategic investments by incumbents

Innovation & Future Outlook: Focus on automation, predictive analytics, integration with ESG and risk modules, move toward composable finance architectures

In global markets, manufacturing, financial services, and retail verticals command the largest share of cloud core adoption. Innovations—such as AI-augmented financial close, continuous audit modules, API-first architectures, and real-time regulatory compliance engines—are reshaping product roadmaps. Consumption is strongest in mature economies with digital infrastructure; emerging markets are accelerating due to growing cloud penetration, regulatory mandates, and capital expenditure constraints driving preference for SaaS solutions.

The strategic relevance of the Cloud Core Financial Management Software Market is profound: by centralizing financial operations in the cloud, organizations can leverage real-time data, dynamic modeling, and embedded intelligence to outpace traditional systems. As companies move beyond static ledgers to predictive, continuous finance workflows, cloud core systems become a backbone for agility and resilience. For instance, AI/ML forecasting delivers 25 % improvement compared to legacy rule-based systems in predicting cash flows and liquidity. North America dominates in deployment volume and R&D investment, while Asia Pacific leads in enterprise adoption rate with over 35 % of mid-sized firms deploying cloud core solutions by 2026.

Over the next 2–3 years, by 2028, integration of generative AI with financial planning (FP&A) is expected to reduce budgeting cycle time by up to 30 %. Firms are also committing to ESG metrics: for example, many finance teams aim for 20 % reduction in paper usage or improved carbon accounting by 2030 through embedded reporting modules. In 2025, a European retailer achieved a 28 % drop in closing errors and a 15 % cut in audit overhead by implementing a blockchain-enabled cloud core pilot.

Together, these trajectories position Cloud Core Financial Management Software not just as a transactional tool, but as a pillar of organizational resilience, compliance, and sustainable growth. It will underpin governance, performance forecasting, audit transparency, and adaptability in volatile environments, making it central to the future enterprise value chain.

The Cloud Core Financial Management Software Market dynamics are shaped by accelerating digital transformation across enterprises, rising regulatory complexity, and a shift from legacy on-premise systems to SaaS. Increasing demand for real-time financial insights, predictive planning, and continuous audit capabilities pushes vendors to enhance modularity, interoperability, and AI/ML integration in core modules (GL, AP/AR, fixed assets). The growth in cross-cloud ecosystems and open APIs encourages platformization. Meanwhile, macroeconomic uncertainty prompts cost control, making subscription models more attractive. Clients demand faster deployment, easier upgrades, and embedded compliance tools. Cloud native vendors invest heavily in security, scalability, and data sovereignty to address enterprise concerns. Integration with other enterprise systems (HR, SCM, CRM) further drives the evolution of cloud core offerings.

Automation and real-time analytics are central to the market’s expansion. Enterprises are under pressure to shorten financial close cycles and strengthen internal controls. With automation, repetitive journal entries, intercompany reconciliations, and accruals can be handled autonomously, freeing finance teams to focus on strategy. Real-time analytics enables instantaneous variance detection and cash forecasting. Many organizations report process time reductions of 25 % to 35 % after adoption of these capabilities. These enhancements make cloud core systems attractive, especially as CFOs demand faster, insight-driven finance operations. The promise of data-driven decision support—versus static monthly reports—makes adoption more urgent.

One major restraint is the complexity of integrating legacy systems and migrating vast amounts of historical financial data to cloud core platforms. Enterprises often have decades of ledger, fixed asset, intercompany, and audit trail data that must be cleansed, validated, and reconciled before migration. Poor data quality, mismatched schemas, and inconsistent business logic can slow or derail rollouts. Moreover, customization in legacy ERP systems (often 10- to 20-year old) may lack clear documentation, complicating mapping. Many firms cite multi-month migration timelines, unanticipated cost overruns, and in some cases data integrity issues during cutover, leading to reluctance or phased rollouts. These complexities impose significant barrier to full-scale adoption.

Integration with ESG reporting, carbon accounting, and regulatory compliance modules presents a compelling opportunity. As regulatory regimes—ranging from carbon taxes to nonfinancial disclosure mandates—intensify, companies seek unified finance platforms that embed ESG metrics, automated reporting, and audit trails. Cloud core systems that can natively handle ESG data collection, validation, scenario modeling, and compliance workflows can capture new demand. Additionally, cross-linking ESG metrics with financial forecasts and risk models strengthens decision support. In jurisdictions with new sustainability disclosure rules, early movers embedding ESG in finance may win mandates and client trust. This creates an avenue for vendors to extend functionality and deepen client engagement.

Security, data privacy, and fragmented local regulations represent formidable challenges. Enterprises are wary of storing sensitive financial data off-premise, especially across borders and in jurisdictions with strict data sovereignty laws. Variations in requirements (e.g. GDPR in Europe, CCPA in California, India’s data localization rules) force vendors to support multiple deployment models, encryption regimes, and audit traceability. Any breach or noncompliance risk can lead to severe penalties and reputational loss. Vendors must continuously invest in certifications, multi-tenant isolation, encryption, and regulatory audit capabilities. In addition, evolving standards and frequent changes in compliance laws require ongoing updates, placing heavy burdens on vendor R&D and client trust.

Modular and composable finance architectures accelerating: More than 60 % of new deployments in 2025 adopted modular, plug-and-play components over monolithic suites; this trend enables faster upgrades and tailored integrations.

Embedded AI/ML and predictive capabilities rising: By 2026, over 50 % of cloud core platforms will include predictive cash flow modeling and anomaly detection out of the box, reducing manual forecasting errors by up to 30 %.

Real-time continuous close gaining traction: Approximately 45 % of finance organizations aim to transition from period-end close to continuous close within 3 years, enabling real-time financial visibility.

ESG/Compliance modules increasingly bundled: Nearly 40 % of new cloud core contracts in 2025 include built-in ESG reporting or carbon accounting functionality as a mandatory add-on, reflecting tighter regulatory and stakeholder expectations.

The Global Cloud Core Financial Management Software Market demonstrates well-defined segmentation across type, application, and end-user categories. By type, solutions are classified into Cloud Accounting, Financial Planning & Analysis (FP&A), Enterprise Resource Planning (ERP)-Integrated Modules, and Risk & Compliance Management systems. Applications span across Banking, Insurance, Manufacturing, Retail, and Professional Services. End-users primarily include Large Enterprises, Small and Medium-Sized Enterprises (SMEs), and Public Sector Organizations. The market exhibits diverse adoption behaviors, with large enterprises emphasizing integration and scalability, while SMEs prioritize affordability and modular deployment. With increasing digitalization and automation, demand for real-time analytics, AI-based forecasting, and ESG-aligned compliance modules continues to rise globally, reinforcing the market’s evolution toward intelligent, adaptive, and interoperable cloud financial ecosystems.

Cloud Accounting currently leads the market, accounting for 41% of total adoption due to its critical role in automating bookkeeping, consolidations, and financial closures across global subsidiaries. Its ease of integration with payroll and billing functions further enhances its dominance. In comparison, Financial Planning & Analysis (FP&A) tools represent 29% of market adoption, driven by CFOs seeking real-time forecasting and scenario modeling capabilities. However, Risk & Compliance Management systems are emerging as the fastest-growing segment, projected to expand at a CAGR of 16.2%, fueled by increasing regulatory scrutiny, audit automation, and ESG-linked disclosures. ERP-Integrated Modules and niche solutions collectively hold the remaining 30% market share, primarily serving mid-tier organizations focused on interoperability.

Among all applications, Banking and Financial Services dominate with 37% adoption, attributed to high regulatory compliance needs, transaction volume, and cross-border financial processing. Manufacturing follows with 24% adoption, benefiting from tighter integration between supply chain data and financial operations. The Retail and E-commerce segment, however, is the fastest-growing, anticipated to expand at a CAGR of 15.4%, supported by digital payment proliferation and omni-channel accounting requirements. Insurance and Professional Services collectively account for the remaining 39% of use cases, emphasizing expense tracking and client billing precision. In 2024, approximately 46% of global enterprises reported using cloud-based financial systems for payment automation and real-time visibility. Moreover, 52% of CFOs highlighted analytics-based cloud platforms as key to improving decision speed and risk control.

Large Enterprises lead the adoption landscape with 48% market share, primarily due to complex financial structures and multi-entity consolidation needs. Small and Medium-Sized Enterprises (SMEs) follow with 33%, leveraging modular cloud finance tools to reduce IT overhead and improve agility. However, the Public Sector is the fastest-growing end-user, projected to expand at a CAGR of 14.8%, driven by government initiatives to modernize accounting, enhance transparency, and adopt standardized reporting frameworks. The remaining 19% includes non-profit organizations and educational institutions, where adoption centers on grant management and compliance. In 2024, more than 40% of SMEs worldwide piloted cloud-based accounting tools for budget control, while 55% of large enterprises integrated AI-driven compliance monitoring to strengthen audit accuracy.

North America accounted for the largest market share at 37.4% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2025 and 2032.

North America’s leadership stems from its mature enterprise ecosystem, robust cloud infrastructure, and widespread adoption of financial digitalization among Fortune 500 firms. Europe followed with 31.6% share, reflecting the region’s emphasis on financial compliance and ERP modernization. Asia Pacific, driven by strong SME digitization in China, India, and Japan, is witnessing rapid adoption of scalable, cloud-native financial management platforms. Meanwhile, Latin America and the Middle East & Africa collectively contributed around 11% of global demand, supported by growing digital transformation initiatives, particularly in banking, telecom, and public administration sectors.

North America held approximately 37.4% of the global Cloud Core Financial Management Software market in 2024, led by the U.S. and Canada. The region’s demand is primarily driven by banking, financial services, healthcare, and technology enterprises, which increasingly rely on cloud-native solutions for compliance automation and multi-entity financial consolidation. Regulatory frameworks such as SOX and the U.S. SEC’s digital reporting standards have accelerated the adoption of transparent, audit-ready cloud systems. Major players like Oracle Corporation continue to expand AI-driven accounting modules to enhance automation and analytics. North American enterprises show strong consumer behavior toward customized, modular software solutions, emphasizing data security and integration across hybrid cloud ecosystems, particularly in finance and healthcare verticals.

Europe accounted for nearly 31.6% of the market share in 2024, led by key economies such as Germany, the U.K., and France. The region’s market is shaped by strict compliance with GDPR and financial transparency regulations from the European Banking Authority (EBA), prompting companies to adopt advanced, explainable, and audit-traceable financial software. Technological adoption trends include integration of AI-driven analytics, automated reconciliation, and cloud ERP unification to meet reporting standards and sustainability disclosure frameworks. Local players such as Unit4 are investing in cloud modernization for enterprise resource planning (ERP) and financial automation across public and private sectors. European consumer behavior reflects a strong preference for compliance-first, sustainability-aligned financial tools, with heightened demand in public sector and regulated industries.

Asia-Pacific represents the fastest-growing regional market, contributing nearly 20% of global demand in 2024 and ranking first in volume expansion. Top consuming nations include China, India, and Japan, where government-backed digitization programs and SME digital finance adoption are transforming the landscape. Rapid growth in e-commerce, fintech, and manufacturing digitization is propelling cloud-based accounting and core financial management solutions. Innovation hubs such as Bangalore, Shenzhen, and Tokyo are fostering new SaaS development and AI-based cloud platforms for real-time financial insights. Local providers like Kingdee International Software Group are expanding integrated accounting and procurement solutions for domestic enterprises. Regional consumer behavior demonstrates strong adoption among SMEs, driven by affordability, mobile accessibility, and integration with AI-enabled analytics for finance automation.

South America held around 6.2% of the global market share in 2024, with Brazil and Argentina being the major contributors. Demand is rising from sectors such as financial services, manufacturing, and retail, where cloud adoption enhances transparency and operational efficiency. Governments across the region are offering tax incentives and digital transformation grants to encourage SME cloud adoption. The fintech ecosystem—particularly in Brazil’s open banking framework—has boosted software integration and financial reporting automation. Local companies like Totvs S.A. have introduced advanced ERP modules embedded with cloud finance analytics, targeting regional enterprises. South American users exhibit strong preference for language-localized interfaces and media-integrated accounting platforms, reflecting diverse consumer behavior across Spanish and Portuguese-speaking economies.

The Middle East & Africa accounted for approximately 4.8% of the total market in 2024, with UAE, Saudi Arabia, and South Africa leading regional adoption. The surge in demand stems from oil & gas diversification, construction, and public sector digitalization projects, alongside strong investments in financial cloud infrastructure. Regulatory initiatives, such as the UAE’s national digital economy strategy and Saudi Vision 2030, have encouraged enterprises to adopt secure and scalable cloud accounting solutions. Regional technology modernization is further driven by government partnerships with international software vendors. Local IT firms, such as Sage Middle East, are offering customized modules for real-time budget tracking and payroll management. Consumers increasingly favor mobile-accessible, compliance-oriented platforms, especially within growing SME clusters.

United States – 31% Market Share: Dominates due to advanced cloud infrastructure, strong enterprise adoption, and heavy investment in AI-driven financial automation.

China – 14% Market Share: Leads in volume growth owing to large-scale SME digitization, rapid fintech innovation, and increasing integration of ERP and AI cloud systems across sectors.

The Cloud Core Financial Management Software Market is moderately consolidated, with approximately 50 active global competitors shaping the competitive landscape. The top five companies—including Workday, Oracle, SAP, Sage, and Microsoft—together control around 65% of the market, demonstrating a strong influence over product innovation, enterprise adoption, and technological standards. Market competition is driven by continuous product launches, strategic partnerships with cloud infrastructure providers, and mergers or acquisitions aimed at expanding regional footprints and portfolio capabilities. Innovation trends focus on AI/ML-enabled predictive analytics, real-time reconciliation, embedded ESG reporting, and composable finance architectures. Vendors are increasingly offering modular subscription models to attract SMEs while maintaining advanced analytics and integration features for large enterprises. Regional differentiation is notable, with North America emphasizing AI-powered forecasting and Europe focusing on compliance-driven solutions. Companies are investing in cybersecurity measures, interoperability, and cross-industry integrations, which remain critical for retaining enterprise clients. Overall, the market is highly competitive, technology-driven, and evolving rapidly to meet the demands of digital-first finance operations worldwide.

Sage Intacct

Microsoft Corporation

NetSuite

Kingdee International Software Group

Unit4

Epicor Software Corporation

The Cloud Core Financial Management Software Market is witnessing rapid technological transformation, with AI/ML-driven automation enabling predictive cash flow, anomaly detection, and automated reconciliations. Blockchain and distributed ledger technology are being integrated to enhance auditability, reduce fraud risk, and enable faster intercompany transactions. Robotic Process Automation (RPA) is increasingly used to handle repetitive accounting tasks, accelerating month-end close processes by up to 30% in enterprise deployments. Cloud platforms now incorporate API-first architectures, supporting seamless interoperability with HR, SCM, CRM, and ESG reporting systems. Embedded analytics and visualization dashboards provide finance teams with real-time insights, scenario modeling, and performance monitoring. Furthermore, multi-cloud and hybrid deployments are emerging to meet data sovereignty and regional compliance requirements. Emerging technologies also include predictive tax compliance tools, continuous audit modules, and AI-based financial risk management engines, enabling proactive decision-making and enhanced operational resilience. Regional adoption trends reveal North America prioritizing AI and RPA integration, Europe emphasizing regulatory compliance technologies, and Asia-Pacific focusing on mobile-accessible finance solutions. Collectively, these innovations position cloud core systems as a strategic backbone for scalable, secure, and intelligent financial management.

In March 2023, Workday launched Adaptive Planning 2023, integrating advanced AI modules to enable scenario-based financial forecasting and real-time budget adjustments, enhancing decision-making for over 5,000 global enterprise clients. Source: www.workday.com

In August 2023, Oracle expanded its Fusion Cloud Financials suite with blockchain-powered intercompany reconciliation features, reducing cross-border transaction errors by 28% and accelerating audit cycles. Source: www.oracle.com

In January 2024, SAP introduced S/4HANA Cloud for Finance, integrating predictive analytics dashboards and automated ESG reporting tools, enabling organizations to track sustainability metrics in alignment with regulatory mandates. Source: www.sap.com

In May 2024, Sage Intacct released a multi-entity management module for midsize enterprises, allowing real-time consolidation of 1,200+ financial entities across North America and Europe, improving reporting accuracy and operational efficiency. Source: www.sage.com

The Cloud Core Financial Management Software Market Report provides a comprehensive examination of global and regional dynamics, covering product types, applications, end-user industries, and technological advancements. Key product types include Cloud Accounting, FP&A, ERP-Integrated Modules, and Risk & Compliance Management systems, while applications span banking, insurance, manufacturing, retail, and professional services. End-user insights differentiate adoption among large enterprises, SMEs, and public sector organizations, highlighting behavioral trends, deployment strategies, and industry-specific requirements. Geographically, the report encompasses North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering a detailed understanding of regional consumption patterns, regulatory frameworks, and technology penetration. Technology coverage includes AI/ML, blockchain, RPA, predictive analytics, continuous close platforms, and composable finance architectures.

The report also addresses emerging areas, such as ESG reporting, mobile-accessible finance platforms, and integration of cross-functional enterprise modules, providing actionable insights for strategic planning, investment decision-making, and competitive positioning. Designed for business leaders, analysts, and decision-makers, the report delivers a clear view of market opportunities, innovations, and future directions while supporting evidence-based planning across diverse global financial ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 501 Million |

| Market Revenue (2032) | USD 1,480.1 Million |

| CAGR (2025–2032) | 14.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Workday, Inc., Oracle Corporation, SAP SE, Sage Intacct, Microsoft Corporation, NetSuite, Kingdee International Software Group, Unit4, Epicor Software Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |