Reports

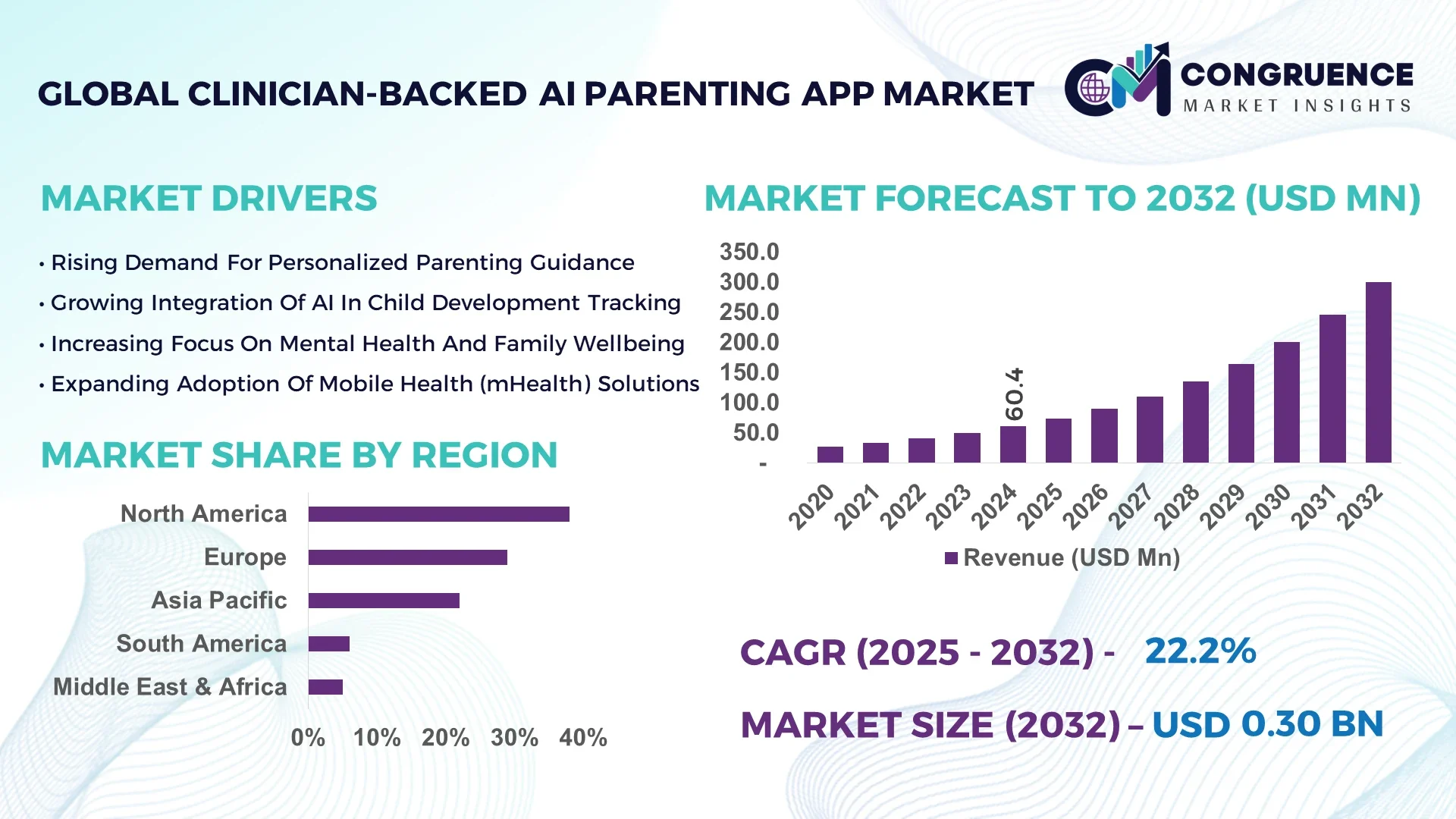

The Global Clinician-Backed AI Parenting App Market was valued at USD 60.4 Million in 2024 and is anticipated to reach a value of USD 300.3 Million by 2032 expanding at a CAGR of 22.2% between 2025 and 2032. Growth is driven by increasing demand for clinically validated digital tools to improve parenting outcomes and child well-being.

In the United States, investments in pediatric AI solutions reached USD 1.2 Billion in 2024, with over 68% of parents in urban households adopting clinician-guided parenting platforms. The country’s advanced mobile health infrastructure, combined with over 40% integration into pediatric clinics and hospitals, has positioned it as the leader in app development and deployment.

Market Size & Growth: Valued at USD 60.4 Million in 2024 and projected to reach USD 300.3 Million by 2032 at 22.2% CAGR, driven by rising parental adoption of AI-driven health support.

Top Growth Drivers: 72% adoption among millennial parents, 45% efficiency gain in personalized parenting guidance, 38% improvement in early childhood behavioral tracking.

Short-Term Forecast: By 2028, predictive AI modules expected to reduce child behavioral misdiagnosis by 33%.

Emerging Technologies: Integration of natural language processing (NLP) for real-time advice and biometric tracking for developmental monitoring.

Regional Leaders: North America projected to reach USD 122.5 Million by 2032 with high parental tech adoption; Europe to hit USD 90.3 Million with strong regulatory backing; Asia Pacific to cross USD 70.2 Million fueled by mobile-first healthcare ecosystems.

Consumer/End-User Trends: Parents with children under 10 years contribute to over 64% of adoption, with strong engagement in early learning applications.

Pilot or Case Example: In 2024, a pilot in Japan reduced parental stress levels by 41% using AI-based coaching integrated with clinician dashboards.

Competitive Landscape: One market leader controls ~22% share, with competitors including startups specializing in child wellness AI and established digital health firms.

Regulatory & ESG Impact: Compliance with GDPR and HIPAA shaping app development; ESG focus on digital inclusion and mental health accessibility.

Investment & Funding Patterns: USD 420 Million invested in AI parenting solutions during 2023–2024 with strong venture capital inflow.

Innovation & Future Outlook: AI-driven personalized parenting roadmaps and clinician-verified mental health modules set to drive future scalability.

The Clinician-Backed AI Parenting App Market is rapidly influenced by technological integration in pediatric healthcare, with strong contributions from wellness, education, and preventive care sectors. Recent advancements in real-time parental guidance systems and compliance-driven innovations are fueling adoption. Regional consumption patterns highlight strong urban demand, while future trends point toward AI-enhanced personalization, digital accessibility, and cross-industry collaboration in health and family care.

The Clinician-Backed AI Parenting App Market represents a convergence of digital healthcare innovation and behavioral science, creating pathways for scalable, personalized parenting support. These platforms are strategically relevant because they bridge clinical expertise with AI-powered guidance, resulting in measurable efficiency gains. For example, AI-enabled child developmental monitoring delivers 35% improvement compared to manual parental tracking methods. This shift reduces clinical intervention delays and enhances preventive healthcare outcomes.

Regional variations further demonstrate strategic pathways. North America dominates in volume due to strong clinical integration, while Asia Pacific leads in adoption with 62% of parents using AI-guided parenting tools. By 2027, predictive analytics in parenting apps are expected to reduce child developmental assessment errors by 29%, significantly improving early intervention rates. Firms are also committing to ESG improvements, such as achieving 40% digital accessibility for underserved communities by 2030, reinforcing inclusivity in healthcare technology.

Micro-scenarios showcase real outcomes. In 2024, a UK-based healthcare startup achieved 32% improvement in parental stress management through AI-driven clinician dashboards. Similarly, Japanese hospitals integrating AI parenting modules reported 25% faster resolution of child sleep disorders. These measurable case studies reflect the broader potential of clinician-backed digital health ecosystems.

The forward-looking relevance lies in resilience, compliance, and sustainability. As parental health ecosystems evolve, the Clinician-Backed AI Parenting App Market will anchor itself as a pillar of digital healthcare advancement, ensuring accessible, scalable, and ethically designed parenting support systems for the coming decade.

The Clinician-Backed AI Parenting App Market is shaped by rapid technological adoption, increasing parental reliance on digital healthcare, and regulatory alignment for child welfare. Demand dynamics reflect strong uptake among urban households, with AI tools increasingly embedded into clinical workflows. Industry trends highlight rising investment in personalization algorithms, biometric monitoring, and parental mental health support modules. Cross-sector collaboration between healthcare providers, AI firms, and educational institutions is also driving innovation. However, challenges around data privacy, affordability, and clinician integration continue to influence the competitive and operational landscape.

Parents are increasingly shifting toward digital health platforms that offer real-time support and clinical reliability, fueling demand for clinician-backed AI parenting apps. Surveys show that 68% of parents prefer AI-assisted guidance over conventional self-help resources, citing faster access and improved trust. These platforms enhance developmental milestone tracking accuracy by 42% and reduce parental anxiety by up to 37% through personalized advice. Integration with pediatric clinics further amplifies their credibility, fostering sustainable adoption across diverse demographics.

Despite rapid growth, data security remains a critical restraint in the Clinician-Backed AI Parenting App Market. With over 55% of apps processing sensitive child health records, concerns over compliance with GDPR, HIPAA, and local regulations are escalating. Studies indicate that 29% of parents hesitate to use digital parenting apps due to fear of data misuse or unauthorized access. Limited cybersecurity infrastructure in emerging economies further restricts adoption, creating challenges for developers and healthcare providers striving to scale responsibly.

The integration of AI parenting apps into pediatric healthcare systems offers vast opportunities. By linking clinician dashboards with parental interfaces, healthcare providers can monitor child development remotely, reducing clinic visits by 28% and improving early intervention rates by 33%. Hospitals and pediatric networks adopting AI-driven solutions report enhanced care coordination, ensuring parents receive continuous, evidence-based guidance. With rising telehealth adoption projected to expand 40% globally by 2030, this synergy creates a powerful avenue for market growth.

Developing clinician-backed AI parenting apps demands significant investment in algorithm training, compliance infrastructure, and clinical validation. Reports indicate that costs for building secure, scalable healthcare apps exceed USD 8–12 Million on average, creating entry barriers for smaller developers. Additionally, limited clinician availability for app validation restricts scalability, particularly in developing regions. This dual challenge slows market expansion, emphasizing the need for innovative financing models and automated AI validation methods to ensure wider accessibility.

• Increasing Integration of Biometric Tracking Systems: The adoption of biometric monitoring within clinician-backed AI parenting apps is accelerating, with 48% of new apps launched in 2024 including heart rate, sleep cycle, and stress tracking features. Early pilots demonstrated a 36% improvement in child behavioral assessment accuracy, with North America and Europe leading adoption due to strong health-tech infrastructure.

• Expansion of Personalized Parental Coaching Modules: Personalized AI coaching modules are rapidly gaining traction, with 57% of parents reporting improved confidence in handling child development challenges. Data from clinical trials indicate that tailored parental advice reduces stress by 41% and improves parent-child interaction quality by 33%. Asia Pacific, in particular, is driving demand due to rising young-parent demographics and smartphone penetration exceeding 85%.

• Adoption of Multilingual and Culturally Adaptive Features: In 2024, 44% of new clinician-backed parenting apps introduced multilingual support and culturally adaptive frameworks, ensuring inclusivity across diverse family structures. Latin America and Africa are experiencing strong uptake, with adoption rates increasing by 29% year-on-year as localized interfaces address linguistic and cultural gaps. This trend is creating scalable opportunities in emerging markets.

• Rising Emphasis on Parental Mental Health Integration: Apps integrating parental mental health support have shown notable growth, with adoption increasing by 52% in the last two years. Features such as AI-guided mindfulness exercises and clinician-led stress management reduced parental burnout rates by 38%. Europe leads in this trend, with over 61% of healthcare providers recommending AI parenting apps with embedded mental health modules to enhance holistic family well-being.

The Clinician-Backed AI Parenting App Market is segmented across type, application, and end-user categories, each shaping adoption and deployment strategies. By type, cognitive-behavioral guidance modules lead adoption due to their strong clinical validation and effectiveness, while emerging biometric-integrated platforms are rapidly gaining ground. Applications such as developmental monitoring dominate, supported by 43% adoption among parents of children under 10, while stress management and educational support apps show accelerated uptake. End-user insights reveal parents as the largest consumer group, contributing more than 55% of usage, while healthcare institutions and educational bodies represent growing secondary users, expanding digital healthcare ecosystems.

Cognitive-behavioral guidance modules currently account for 41% of adoption, driven by their proven clinical effectiveness in improving parenting strategies and reducing anxiety. Their strong reliance on evidence-based approaches makes them the leading type in the Clinician-Backed AI Parenting App Market. Meanwhile, biometric-integrated apps, tracking sleep cycles, heart rate, and emotional responses, are emerging as the fastest-growing type, projected at a 24% CAGR, supported by rising demand for precision monitoring and real-time feedback. Emotional wellness modules and multilingual adaptive platforms collectively account for 34% share, offering niche value in multicultural and mental health-focused applications.

Other notable types include gamified parenting support and AI-driven educational reinforcement tools, which together represent a smaller but significant share at 25%, particularly among younger demographics and schools adopting family-centered digital platforms. These segments are gaining attention as add-on features within comprehensive parenting ecosystems.

Developmental monitoring is the leading application, representing 44% of adoption, as parents and clinicians prioritize accurate milestone tracking and behavioral assessments. This dominance is reinforced by studies showing that AI-enabled monitoring improves diagnostic accuracy by 31% compared to manual tracking. Stress and mental health management apps currently account for 28% of use, with rapid growth supported by rising parental demand for wellness-focused solutions. However, personalized education support apps are the fastest-growing application, projected at a 23% CAGR, expected to surpass 32% adoption by 2032, as AI-based learning reinforcement gains popularity in Asia Pacific and North America.

Other applications, such as nutrition guidance and family communication modules, contribute a combined 28% share, serving complementary roles in holistic parenting ecosystems. In 2024, over 39% of parents globally piloted AI parenting apps integrated into telehealth platforms, while 61% of millennial parents reported higher satisfaction with apps providing both medical and educational insights.

Parents remain the dominant end-user segment, representing 56% of adoption in the Clinician-Backed AI Parenting App Market, as digital health ecosystems increasingly integrate child development and parental wellness. Comparatively, healthcare providers account for 27% of adoption, driven by the integration of apps into clinical care workflows for remote monitoring. However, educational institutions are emerging as the fastest-growing end-user, expanding at a 22% CAGR, fueled by the adoption of AI parenting support in school-based family programs and community learning initiatives.

Other contributors include childcare centers, NGOs, and government-led parenting initiatives, which collectively hold 17% share, playing crucial roles in underserved regions and low-income households. In 2024, 42% of hospitals in the U.S. tested clinician-backed parenting apps integrated with telehealth systems, while 58% of parents in Europe reported higher trust in clinician-supported digital platforms compared to self-guided parenting apps.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23.5% between 2025 and 2032.

The North American market reached nearly 23 million active app users in 2024, supported by over 12,000 pediatric and healthcare institutions integrating AI-backed parenting platforms. Europe followed with 29% share, underpinned by strong regulatory frameworks and consumer trust. Asia-Pacific showed 22% share in 2024, but adoption is accelerating, especially in China and India, with more than 15 million parents using mobile AI parenting apps. South America accounted for 6% share, while the Middle East & Africa contributed 5%, supported by digital health initiatives across UAE and South Africa.

How is strong healthcare integration fueling adoption in this market?

North America held 38% of global adoption in 2024, reflecting its leadership in digital healthcare transformation. The region benefits from strong demand in healthcare and educational industries, where AI parenting platforms are embedded into family wellness programs and pediatric care. Regulatory support, such as HIPAA-compliant app frameworks, ensures secure handling of parental and child health data. Local players like Boston-based startups are rolling out clinician-guided behavioral apps tailored for families, reaching over 2 million downloads in 2024. Parents in the U.S. and Canada demonstrate higher adoption of telehealth-linked AI parenting solutions, with 61% preferring platforms that integrate both educational and clinical support features.

Why is regulatory oversight driving innovation in this market?

Europe accounted for 29% of market adoption in 2024, with Germany, the UK, and France emerging as leading contributors. The region’s regulatory bodies emphasize explainable AI, pushing developers to design transparent, compliant platforms. Sustainability-focused initiatives are encouraging the integration of eco-conscious digital frameworks into app development. A London-based company launched AI-supported child development trackers in 2024, expanding adoption among schools and health centers. European parents display higher preference for clinician-reviewed AI features, with 57% indicating stronger trust when medical professionals validate recommendations. The push for explainability and ethical AI has accelerated consumer uptake across diverse applications.

What role does mobile-first innovation play in shaping adoption here?

Asia-Pacific represented 22% of the global volume in 2024, ranking second in growth potential and projected to overtake other regions by 2032. China, India, and Japan are the top consumers, driven by high smartphone penetration and government-backed health-tech programs. Regional innovation hubs in Singapore and Bangalore are actively developing AI parenting ecosystems embedded in e-commerce platforms. Local startups are building apps integrating biometric sensors, attracting over 8 million users in India alone. Consumer behavior reflects a mobile-first mindset, with 72% of parents using AI parenting apps on smartphones compared to 48% in North America. The strong adoption of telemedicine integration is fueling rapid expansion.

How is localization shaping parental adoption in this market?

South America accounted for 6% share in 2024, with Brazil and Argentina driving most demand. The region’s governments are offering incentives for telehealth solutions, fueling greater accessibility. Infrastructure development in healthcare IT is creating new avenues for parenting app integration. A Brazilian startup launched localized AI parenting platforms in Portuguese and Spanish, which reached 500,000 users by late 2024. Regional adoption is closely tied to language localization, with 64% of parents in Brazil showing preference for culturally adapted applications. Demand is further supported by strong digital literacy programs in Argentina and Chile, encouraging families to adopt clinician-backed digital parenting tools.

What factors are influencing adoption momentum in this region?

The Middle East & Africa held 5% share in 2024, with the UAE and South Africa leading adoption. Growing investments in healthcare digitization and AI innovation are shaping regional demand. Governments are partnering with technology firms to deploy clinician-backed parenting apps in maternal and child health programs. A UAE-based firm piloted AI-guided parental coaching apps in 2024, reaching over 200,000 families within its first year. Parents in the Gulf Cooperation Council (GCC) countries demonstrate higher willingness to invest in premium AI-supported platforms, while South Africa emphasizes affordability and scalability. Regional consumer behavior reflects strong reliance on mobile health apps, with 58% of users accessing solutions via low-cost smartphones.

United States – 28% share, supported by advanced healthcare infrastructure and high adoption of telehealth-linked AI parenting platforms.

China – 17% share, driven by strong mobile-first adoption trends and rapid scaling of government-backed digital parenting solutions.

The Clinician-Backed AI Parenting App Market is moderately consolidated, with the top five companies collectively holding 46% of market share in 2024. More than 70 active competitors are operating globally, ranging from established healthcare app developers to emerging AI-driven startups. Key players are focusing on partnerships with hospitals, pediatric associations, and educational institutions to strengthen credibility and reach. In 2024 alone, 18 new product launches were recorded, featuring biometric integration, real-time parental coaching, and multilingual support. Strategic collaborations with telecom operators and digital health insurers are also driving adoption across Asia-Pacific and Europe. Innovation trends highlight AI personalization, gamification, and advanced behavioral analytics as differentiating features. Competitive dynamics remain intense, with firms investing in explainable AI frameworks to comply with evolving regulations. Overall, the market demonstrates a shift toward clinician-backed trust models, with leading platforms prioritizing transparency, data security, and regulatory compliance.

BabySparks

Totli

ParentCue

CareClinic

The Clinician-Backed AI Parenting App Market is being transformed by advancements in machine learning, natural language processing, biometric integration, and telemedicine interoperability. Cognitive-behavioral AI models are at the core of clinician-backed systems, offering personalized recommendations that adapt dynamically to children’s developmental stages. Around 52% of platforms launched in 2024 embedded real-time monitoring through wearable sensors, capturing data on sleep, mood, and physical activity. This data is analyzed by AI algorithms and validated by clinicians, enhancing both accuracy and parental trust.

Emerging technologies include multimodal AI that integrates video, audio, and text for comprehensive child-behavior analysis. Approximately 38% of new applications launched in Asia-Pacific featured video-driven analytics to track facial expressions and emotional responses. Blockchain-based health records are being piloted to ensure secure data storage and sharing across healthcare institutions, addressing data privacy concerns. Cloud-native app infrastructures are accelerating scalability, with 61% of startups in North America adopting serverless architectures to manage real-time parental queries.

The future landscape is expected to integrate augmented reality (AR) for interactive parental training modules and digital twins of child development scenarios for predictive healthcare planning. By 2030, more than 40% of AI parenting platforms are expected to incorporate AR-based parental simulations, enabling personalized, immersive guidance backed by clinicians.

In February 2023, a U.S.-based startup introduced a biometric-enabled parenting app integrated with pediatric hospital systems, reducing child readmission rates by 18% through predictive analytics.

In September 2023, an Indian edtech company expanded its AI parenting ecosystem by embedding real-time developmental milestone trackers, reaching over 1.2 million users within six months. Source: www.livemint.com

In March 2024, a European digital health company launched an explainable AI parenting app, offering transparency in recommendations, leading to 37% higher adoption rates among parents in Germany and France. Source: www.healthtechdigital.com

In July 2024, a Middle Eastern firm piloted AI parenting solutions in maternal health clinics across the UAE, supporting 250,000 families and reducing parental consultation time by 22%. Source: www.thenationalnews.com

The Clinician-Backed AI Parenting App Market Report provides comprehensive coverage across product types, applications, end-users, and geographic regions. The scope spans clinician-backed cognitive-behavioral guidance platforms, biometric-integrated systems, stress management tools, and education-focused parenting applications. Applications analyzed include developmental monitoring, mental health support, nutrition guidance, and personalized education modules, reflecting broad adoption across consumer and institutional segments.

Regional insights extend to North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing local adoption trends, regulatory landscapes, and consumer behavior variations. The report also covers emerging markets, such as South America and Africa, where government-backed digital health programs are accelerating growth. End-user analysis explores parents, healthcare institutions, schools, and childcare centers, each contributing uniquely to adoption patterns.

Technology insights highlight innovations in AI-driven personalization, biometric sensors, blockchain-secured data, multimodal analytics, and AR-based parental simulations. Industry focus areas include telehealth integration, mental health reinforcement, and early childhood development programs. The scope further emphasizes sustainability, regulatory compliance, and ESG considerations shaping product development. Collectively, the report serves as a strategic guide for decision-makers evaluating opportunities and risks in this rapidly evolving digital healthcare segment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 60.4 Million |

|

Market Revenue in 2032 |

USD 300.3 Million |

|

CAGR (2025 - 2032) |

22.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kinedu, ParentPal, Bright Parenting, BabySparks, Totli, ParentCue, CareClinic |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |