Reports

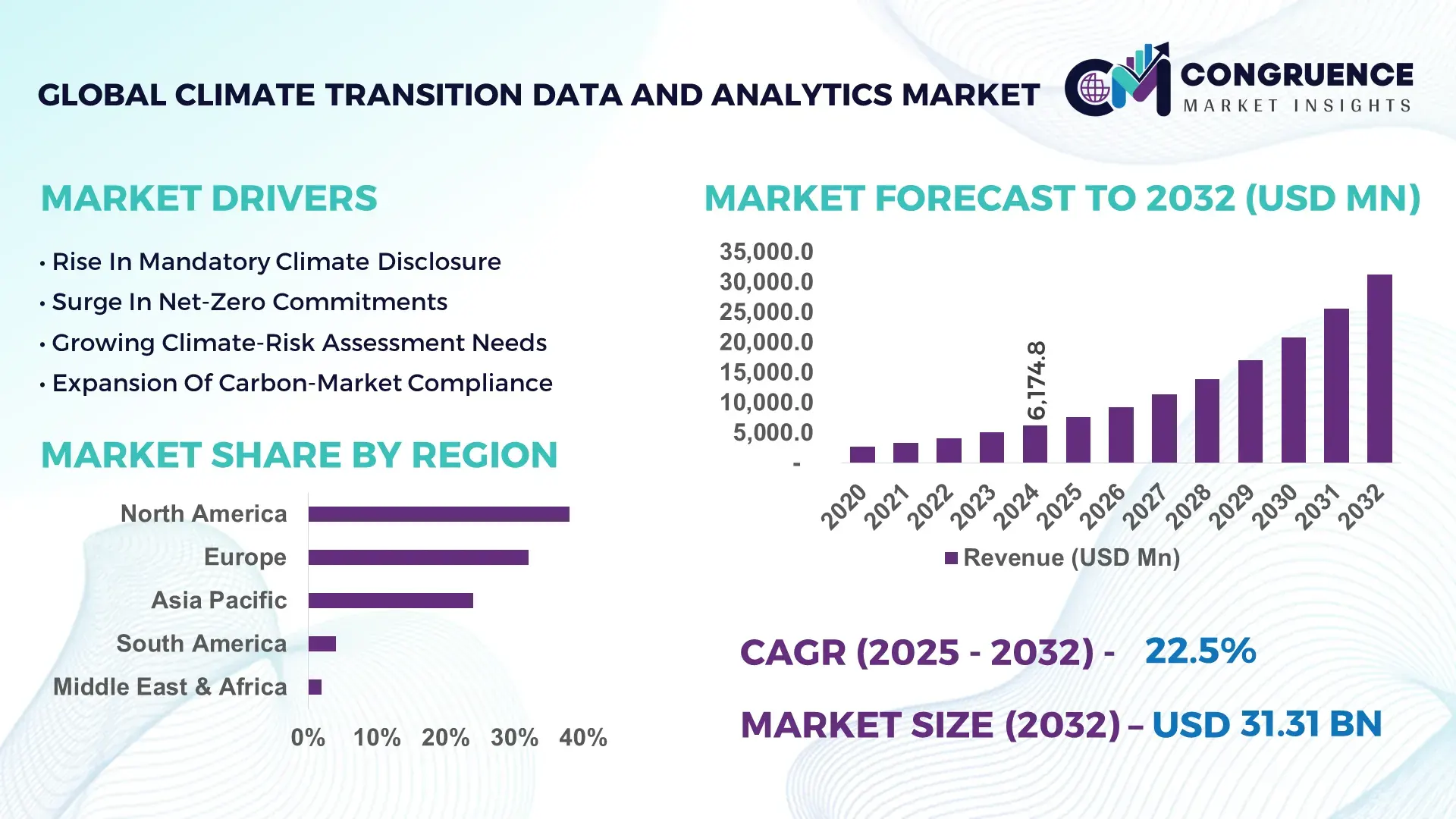

The Global Climate Transition Data and Analytics Market was valued at USD 6,174.8 Million in 2024 and is anticipated to reach a value of USD 31,312.1 Million by 2032 expanding at a CAGR of 22.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This surge is driven by rapid decarbonization mandates and enterprise-wide sustainability reporting requirements.

The United States plays a pivotal role in shaping the Climate Transition Data and Analytics market, supported by advanced digital infrastructure, large-scale corporate ESG commitments, and strong federal backing for climate-tech innovation. With over USD 25 Billion invested in climate-data modernization initiatives since 2020 and more than 3,500 enterprises adopting real-time emissions intelligence tools, the country reports one of the highest integration rates of climate-aligned financial risk models, achieving over 40% penetration across Fortune 500 companies.

Market Size & Growth: USD 6.17 Billion in 2024, projected to reach USD 31.31 Billion by 2032, expanding at 22.5% CAGR; accelerated due to stricter carbon disclosure norms.

Top Growth Drivers: 62% adoption growth in enterprise ESG reporting tools; 48% improvement in climate-risk modeling efficiency; 37% increase in automated carbon accounting systems.

Short-Term Forecast: By 2028, enterprises expected to reduce audit-cycle times by 35% using intelligent climate analytics.

Emerging Technologies: AI-native emissions engines, satellite-driven climate verification models, IoT-enabled real-time carbon sensors.

Regional Leaders: North America projected at USD 11.4 Billion by 2032; Europe at USD 9.7 Billion; Asia Pacific at USD 7.9 Billion, each driving unique low-carbon digitalization patterns.

Consumer/End-User Trends: 58% of large enterprises integrating automated sustainability-performance dashboards; 32% increase in climate-risk analytics deployment by financial institutions.

Pilot or Case Example: In 2026, a national utility deployed predictive climate-risk models, improving infrastructure resilience by 44%.

Competitive Landscape: Market leader holds ~16% share, followed by players offering climate-risk platforms, ESG intelligence systems, and emissions modeling software.

Regulatory & ESG Impact: Emerging carbon-accounting legislation and mandatory climate-risk disclosures accelerating enterprise adoption.

Investment & Funding Patterns: Over USD 9 Billion invested in climate-data startups globally in the past three years, with rising inflows toward AI-driven ESG intelligence tools.

Innovation & Future Outlook: Advancements in geospatial climate intelligence, automated disclosure engines, and transition-scenario modeling are redefining market direction.

Global demand is increasingly shaped by sectors such as energy, finance, manufacturing, and transportation, which collectively contribute more than 60% of analytics consumption. Rapid product innovations like AI-generated emissions baselines, climate-scenario stress testing, and digital MRV systems are accelerating adoption. Strong regulatory signals, rising carbon-price volatility, and regionally diverse sustainability targets fuel demand, while evolving trends such as climate-aligned fintech and science-based transition pathways strengthen market growth.

The Climate Transition Data and Analytics Market plays a strategic role in accelerating global decarbonization, financial resilience, and regulatory compliance. Organizations are increasingly using advanced intelligence systems to quantify transition risks, optimize resource consumption, and align operational planning with net-zero trajectories. The integration of next-generation analytics platforms enables enterprises to track Scope 1, Scope 2, and Scope 3 emissions with high-precision accuracy—improving data reliability by up to 46% compared with legacy spreadsheet-based methods. New-generation AI-driven climate engines deliver 52% improvement compared to traditional lifecycle assessment models, significantly reducing manual processing time.

Regional variations underscore the strategic divergence: North America dominates in volume due to high institutional demand, while Europe leads in adoption with 68% of enterprises using climate-risk analytics to meet stringent sustainability mandates. By 2027, AI-enabled sustainability automation is expected to improve resource-efficiency KPIs by over 33%, reshaping operational decision-making frameworks across industries. In parallel, firms are committing to measurable ESG advancements, including achieving up to 30% emissions-intensity reduction by 2030 through enhanced transition pathway modeling.

A real-world micro-scenario demonstrates the scale of progress: In 2026, a Scandinavian energy provider achieved 41% operational-emissions reduction through the deployment of real-time predictive climate-risk systems integrated with renewable-generation forecasts. Such tangible outcomes highlight the market’s ability to transform decarbonization planning, climate-risk management, and sustainable value creation.

The Climate Transition Data and Analytics Market is now positioned as a foundational enabler of resilience, compliance, and long-term sustainable growth for enterprises navigating the accelerating global transition landscape.

The Climate Transition Data and Analytics Market is evolving rapidly as organizations integrate high-precision emissions tracking, climate-risk forecasting, and sustainability intelligence into core decision systems. Key dynamics include rising regulatory pressures, expansion of digital MRV frameworks, and increasing demand for predictive climate-scenario modeling across heavy industries, BFSI, utilities, and logistics. AI-powered transition tools are transforming corporate reporting, with more than 50% of enterprises seeking automated disclosure capabilities to meet international compliance frameworks. Additionally, geospatial analytics, IoT-based carbon monitoring, and satellite-verified emissions baselines are reshaping the competitive landscape by enabling higher accuracy and real-time data availability. Collectively, these forces are driving strategic market expansion and influencing technology procurement patterns across global value chains.

Rising global climate disclosure mandates are significantly accelerating the Climate Transition Data and Analytics Market by pushing organizations to adopt advanced, auditable, and automated sustainability intelligence systems. With more than 3,000 companies now required to report climate-related financial information under evolving regulations, enterprises are prioritizing standardized, real-time emissions monitoring tools to ensure compliance readiness. ESG audit timelines have tightened by nearly 30% across multiple regions, prompting large corporations to integrate digital MRV platforms to avoid penalties and disclosure discrepancies. The emergence of unified regulatory frameworks across Europe and Asia has further increased deployment of transition-scenario models, enabling businesses to quantify policy-driven risks more accurately. Additionally, financial institutions are scaling climate-risk analytics to meet evolving supervisory expectations, driving a 45% increase in demand for climate-aligned stress-testing systems. These shifts collectively reinforce the strategic necessity of adopting climate transition analytics to meet compliance, reporting, and stakeholder accountability expectations.

The Climate Transition Data and Analytics Market faces significant restraints due to fragmented data ecosystems, inconsistent corporate reporting formats, and the absence of unified global carbon-accounting standards. Many industries still rely on outdated data-collection methods, with more than 40% of enterprises reporting challenges in integrating facility-level emissions data with centralized ESG systems. Variability in measurement methodologies, such as differing approaches to Scope 3 calculations, further complicates accurate reporting. Emerging markets experience infrastructure constraints that limit access to granular climate data, reducing the reliability of transition-pathway modeling. Additionally, interoperability issues across digital platforms hinder seamless exchange of sustainability information between supply-chain partners. These challenges collectively delay enterprise adoption of climate-transition analytics and slow the operationalization of decarbonization strategies.

The digitalization of sustainability planning presents major opportunities for the Climate Transition Data and Analytics Market. As financial institutions integrate climate-risk assessment models into lending, underwriting, and investment frameworks, demand for advanced scenario analytics has surged by more than 50% since 2022. Enterprises are increasingly adopting automated carbon-management platforms to optimize low-carbon procurement decisions, presenting strong expansion prospects for analytics vendors. The rise of digital MRV systems in voluntary carbon markets opens new avenues for tools that verify emissions reductions with 90% greater accuracy than manual assessments. Manufacturing and logistics players are also adopting predictive climate analytics to reduce energy consumption and minimize climate-related supply chain disruptions. These digital transformation opportunities create new revenue pathways for solution providers offering AI-driven climate-transition modeling and automated disclosure engines.

High integration costs and complex governance frameworks pose major challenges for enterprises deploying Climate Transition Data and Analytics systems. Implementing advanced climate-risk engines, IoT-based carbon sensors, and satellite-derived verification modules often requires substantial upfront investment, particularly for mid-sized organizations. More than 47% of companies cite data governance issues—including data ownership, validation, and auditability—as barriers to full-scale adoption. Additionally, aligning enterprise-wide sustainability datasets with IT, finance, and compliance workflows adds operational complexity. Companies operating across multiple geographies face compatibility challenges with region-specific reporting formats and verification requirements. These structural and financial obstacles slow the pace of deployment and limit the scalability of climate-analytics adoption across global supply chains.

• AI-Enhanced Emissions Intelligence: AI-enabled emissions engines are improving data accuracy by up to 45%, enabling enterprises to automate 70% of reporting workflows. Over 52% of large organizations deployed AI-based Scope 3 estimation tools in 2024, indicating rapid adoption of intelligent sustainability systems.

• Surge in Climate-Aligned Financial Modeling: Banks and insurers increased climate-risk portfolio modeling by 38% over the last two years, driven by stricter supervisory expectations. More than 30% of global assets are now stress-tested through climate-scenario models incorporating physical and transition risks.

• Expansion of Satellite-Verified Climate Analytics: Satellite-calibrated emissions verification increased by 56% globally, providing geospatial insights for over 12,000 industrial sites. Enterprises using satellite-integrated transition tools reported a 34% improvement in baseline accuracy and climate-risk detection.

• Growth of Digital MRV and Carbon-Market Automation: Digital MRV adoption rose 41% as carbon-market participants seek auditable, high-fidelity tracking systems. Automated verification reduced manual validation time by nearly 60%, enhancing credibility and accelerating credit issuance in voluntary carbon markets.

The Climate Transition Data and Analytics Market segmentation spans types, applications, and end-user categories, reflecting diverse operational needs across industries. Adoption of advanced analytics is increasing as organizations seek greater visibility into climate risks, emissions performance, and sustainability planning. Types vary from emissions-tracking platforms to climate-scenario modeling systems and digital MRV tools, each serving specialized functions. Applications extend across compliance reporting, risk forecasting, low-carbon investment planning, and operational optimization, driven by growing regulatory and financial pressures. End-users include financial institutions, energy companies, manufacturers, and technology providers, each contributing distinct consumption patterns. Collectively, segmentation highlights the market’s expanding technological breadth and strategic relevance for decision-makers navigating the global climate transition.

The Climate Transition Data and Analytics Market comprises several solution types, each addressing specific aspects of climate-aligned decision-making. Emissions-tracking and carbon-accounting platforms currently lead the segment, accounting for 39% share due to rising mandatory disclosure requirements and enterprise-wide carbon-footprint visibility needs. Climate-scenario modeling tools represent the fastest-growing segment, projected to expand at a CAGR of 27.4%, propelled by financial institutions adopting transition-risk assessment frameworks. Digital MRV systems, geospatial climate-intelligence engines, and climate-aligned asset-management tools collectively hold the remaining 61% share, with strong adoption in industries such as manufacturing, energy, and logistics. The combined influence of these solutions is reshaping enterprise sustainability infrastructure globally.

Applications of Climate Transition Data and Analytics tools span compliance reporting, real-time emissions tracking, climate-risk forecasting, and investment-grade sustainability assessments. Compliance-oriented tools dominate with 42% share as organizations increasingly align with climate-disclosure regulations. Climate-risk analytics follow at 25%, while operational decarbonization tools—used for energy optimization and supply-chain emissions management—are expanding rapidly and expected to surpass 30% adoption by 2032. Additional applications include scenario planning, asset-resilience modeling, and carbon-market validation, together representing the remaining share. In 2024, more than 38% of enterprises globally piloted Climate Transition Data and Analytics solutions for customer-centric sustainability management, while 62% of younger consumers favored brands with transparent climate disclosures.

Financial institutions represent the leading end-user segment with 36% share, driven by rising integration of climate-risk models in investment and lending decisions. Energy and utilities follow at 25%, leveraging real-time transition analytics to optimize generation mix and grid resilience. Manufacturing, transportation, and technology sectors collectively account for the remaining share but are rapidly adopting integrated sustainability intelligence systems. Transition-scenario analytics are the fastest-growing use case with projected adoption CAGR of 26.1%, fueled by stricter compliance mandates and demand for climate-aligned operational planning. In 2024, more than 38% of enterprises initiated pilots for emissions-tracking automation, while 60% of next-generation consumers favored companies with verifiable climate-transition strategies.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24 % between 2025 and 2032.

In 2024, North America saw over 5,400 enterprises deploying climate-transition analytics solutions, led by financial services and energy firms that integrated predictive climate-risk data into strategic planning. The region’s mature regulatory infrastructure and high ESG adoption supported this dominance. Meanwhile, Asia-Pacific is rapidly scaling both in deployment volume and innovation: major markets such as China, India, Japan, and Australia are investing in large-scale carbon-accounting platforms, satellite-enabled climate modeling, and AI-based MRV tools. More than 4,800 climate-data systems were installed in APAC in 2024, reinforcing its position as the fastest-growing region in transition data and analytics.

Why Is AI-Driven Transition Analytics Exploding in Finance and Utilities?

North America commands approximately 38% of the global climate transition data and analytics market, driven by deep integration in financial institutions, utilities, and large enterprises. Key industries such as banking, insurance, and energy are using analytics to model transition risk, price climate-sensitive assets, and manage decarbonization pathways. Regulatory push—from regulators and investors—is accelerating deployment: mandatory climate disclosures, scenario analysis mandates, and sustainability reporting requirements encourage adoption. Technologically, advanced predictive engines combining AI, geospatial data, and real-time emissions are being deployed. A U.S.-based climate-tech firm, for example, uses AI to forecast transition risk for power grids under various net-zero scenarios. Consumer behavior in North America reflects higher enterprise adoption in finance and healthcare, with more corporates using climate-aligned dashboards to engage stakeholders around emissions strategies.

How Are ESG Regulations Fueling Explainable Transition Analytics?

Europe accounts for roughly 32% of the climate transition data and analytics market, with major contributions from Germany, the United Kingdom, and France. European regulatory bodies, such as the EU and regional governments, are driving sustainability and climate reporting through rules like taxonomy alignment and mandatory climate-risk disclosures. Adoption of explainable AI for transition analytics is rising sharply, as firms need transparent and auditable models to comply with EU regulation. European technology providers are rolling out AI-native climate-scenario tools that help companies stress test policies, align with low-carbon pathways, and forecast capital needs. A German data analytics firm has launched a modular tool that integrates climate-scenario modelling into treasury operations. European customers, under regulatory pressure, demand high transparency in climate-intelligence systems, contributing to the region’s strong uptake of sophisticated analytics solutions.

What’s Accelerating Transition Analytics Uptake Across Emerging Economies?

Asia-Pacific is emerging as the second-largest regional market for climate transition data and analytics, characterized by high deployment volume and innovation momentum. Top consuming countries include China, India, Japan, and Australia, which are investing heavily in carbon-accounting platforms, satellite-based emissions models, and real-time climate monitoring systems. Infrastructure trends reflect strong public-private partnerships: governments in China and India are subsidizing climate-data hubs, while fintech and energy firms build climate-scenario engines to support green finance. Innovation hubs in cities like Shanghai, Bangalore, and Singapore are advancing AI-based MRV (Measurement, Reporting, Verification) systems, and local climate-risk firms are scaling their analytics platforms. Regional consumer behavior favors mobile-first, data-driven sustainability reporting: many APAC enterprises are integrating climate dashboards into supply-chain apps, responding to digital-native stakeholders demanding transparent transition metrics.

How Are Latin American Markets Harnessing Climate Analytics for Green Finance?

In Brazil and Argentina, climate transition data and analytics is gaining traction, supported by growing interest in sustainable finance and energy transition. The region represents a meaningful and growing share of the global analytics market, particularly in sectors such as agriculture, mining, and renewable energy. Infrastructure modernization trends—especially in grid decarbonization and bioenergy—are driving demand for transition risk modeling tools. Governments are increasingly crafting incentives and regulatory frameworks for low-carbon investment, stimulating analytics uptake. A Brazilian analytics firm recently began offering climate-risk scenario tools tailored to local assets, helping companies evaluate the financial implications of carbon pricing and regulatory shifts. Regional behavior shows that companies are tying climate analytics to language-localized investor reports, reflecting strong demand for transparent, localised green finance information.

Why Is Climate-Intelligence Becoming Strategic in Emerging MEA Economies?

In the Middle East & Africa, demand for climate transition data and analytics is rising in high-carbon industries such as oil & gas, construction, and utilities. Key markets include the UAE and South Africa, where energy transformation initiatives and sustainability mandates are gaining momentum. Technological modernization is underway: firms are deploying AI-driven carbon tracking, predictive climate-scenario models, and satellite-based verification tools in large infrastructure projects. Local analytics providers are partnering with global climate-tech firms to deliver climate-risk platforms for regional corporates. Consumer behavior shows a growing preference for integrated climate governance systems aligned with national sustainability goals, while governments increasingly mandate climate reporting and risk disclosure for large corporates.

United States: ~38 % share — driven by strong ESG regulatory momentum, massive enterprise adoption of climate-risk analytics, and high capital allocation for green-tech.

China: ~22 % share — propelled by aggressive green finance rollout, large-scale renewables deployment, and government-backed climate-data infrastructure initiatives.

The competition landscape for the Climate Transition Data and Analytics Market is moderately fragmented, with 8–10 major global players commanding roughly 55–60 % of market influence. Leading firms in this sector offer a mix of climate-risk modeling, emissions accounting, geospatial analytics, and scenario planning. Providers are forming strategic alliances with financial institutions, technology platforms, and governments to embed transition data into decision workflows. Partnerships between climate-tech startups and large consultancies are common, enabling joint go-to-market models that sell analytics into sustainability advisory services. Firms are also launching AI-native climate-scenario engines, digital MRV platforms, and real-time transition risk dashboards to differentiate themselves. Innovation is focused on satellite-backed emissions verification, explainable climate AI, and integration of climate intelligence into ERP and treasury systems. While the top five firms dominate, there remains ample room for niche players that specialize in carbon disclosure, regional transition modeling, or science-based target alignment.

Four Twenty Seven (now under Moody’s ESG)

Jupiter Intelligence

One Concern

ClimateAI

Sustainalytics

Plan A (climate software)

Clarity AI

ACCO2 Data Services

Aclima

Persefoni

S&P Global Climate Solutions

The core technologies shaping the climate transition data and analytics market include advanced AI, geospatial intelligence, IoT-enabled sensors, and digital MRV (Measurement, Reporting, Verification) systems. AI models analyze large-scale emissions datasets, financial risk parameters, and forward-looking climate scenarios to produce high-resolution transition analytics. Geospatial tools — including satellite imagery and remote sensing — help validate emissions baselines and verify changes over time, offering accuracy improvements of 30–40%. IoT-based carbon sensors deployed in industrial sites, buildings, and transport fleets enable real-time data capture, allowing systems to track Scope 1 and Scope 2 emissions continuously. Digital MRV platforms streamline compliance by automating data collection and verification, reducing manual workload by over 50%. Scenario-modeling engines combine financial data with climate pathways to stress-test portfolios, while explainable AI techniques ensure transparency in transition decisions. Leading analytics providers are integrating orchestration layers that link climate intelligence with enterprise systems like ERP, treasury, and sustainability reporting tools. These integrated platforms help companies embed strategic transition metrics into core business processes and financial planning, driving data-driven sustainability transformation.

• In June 2024, ZestyAI secured regulatory approval in over 35 U.S. states for its AI-powered property-level climate risk models, enabling insurers to integrate climate-transition analytics into underwriting. Source: www.zesty.ai

• In March 2024, RepRisk launched a climate-risk dataset expansion that now covers over 50,000 companies globally, enhancing its capability to assess transition risk across sectors. Source: www.reprisk.com

• In October 2023, Verisk Analytics introduced a premium climate-scenario analytics dashboard tailored for energy and financial firms, enabling scenario alignment with net-zero emissions trajectories. Source: www.verisk.com

• In April 2024, S&P Global expanded its climate-data platform to include digital MRV functionality, allowing large corporates to automate emissions reporting and track transition progress more precisely. Source: www.spglobal.com

This Climate Transition Data and Analytics Market Report provides a rigorous global assessment of solution types, applications, technologies, deployments, and sector-specific use cases. It examines transition analytics platforms—including emissions accounting, AI-driven scenario modeling, and MRV tools—while profiling how these solutions are deployed across compliance, risk management, finance, and operations. Geographically, the report covers all major regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional maturity, regulatory drivers, and climate-data infrastructure. The study also dissects end-user sectors such as financial services, energy, manufacturing, transport, and technology companies, evaluating their unique needs for climate-risk intelligence. On the technology front, the report explores satellite-based geospatial analysis, IoT sensor integration, and predictive AI models. Strategic analysis is provided through company profiling, partnership trends, and innovation pipelines. The report further addresses emerging themes like digital MRV in carbon markets, climate-finance integration, science-based target alignment, and the role of AI in transition planning—making it a critical guide for decision-makers pursuing sustainable growth and climate-ready strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6,174.8 Million |

|

Market Revenue in 2032 |

USD 31,312.1 Million |

|

CAGR (2025 - 2032) |

22.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Verisk Analytics, ZestyAI, RepRisk AG, Four Twenty Seven (now under Moody’s ESG), Jupiter Intelligence, One Concern, ClimateAI, Sustainalytics, Plan A (climate software), Clarity AI, ACCO2 Data Services, Aclima, Persefoni, S&P Global Climate Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |