Reports

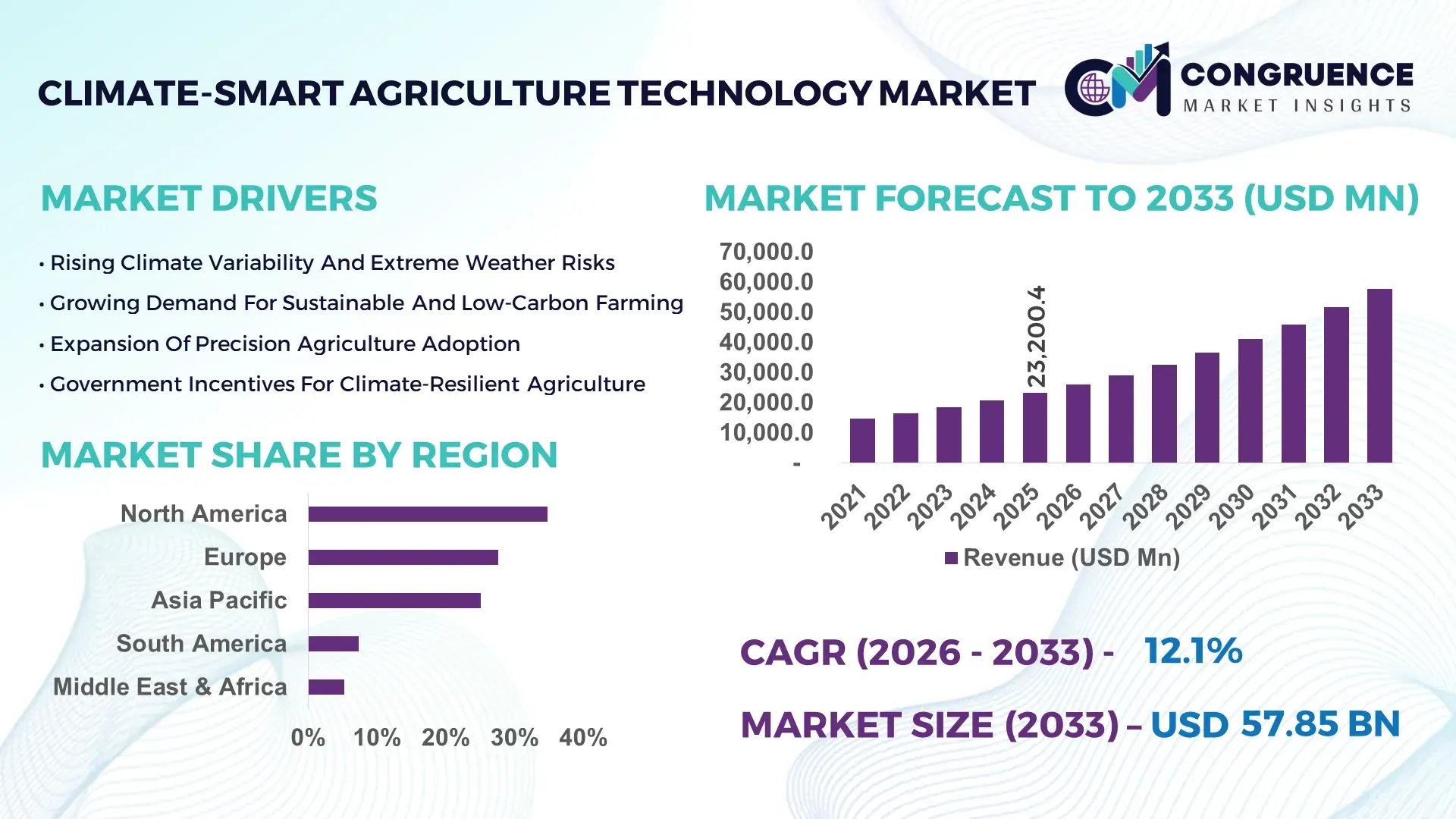

The Global Climate-Smart Agriculture Technology Market was valued at USD 23,200.4 Million in 2025 and is anticipated to reach a value of USD 57,854.9 Million by 2033 expanding at a CAGR of 12.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by rising demand for precision farming, resource-efficient irrigation, and carbon-reducing agricultural practices.

The United States dominates the Climate-Smart Agriculture Technology market through extensive agricultural production capacity, advanced mechanization, and sustained investment in precision farming technologies. In 2025, over 98 million hectares of farmland in the country utilized some form of climate-smart or precision agriculture solution, supported by more than USD 4.6 billion in public and private investments in smart irrigation, soil analytics, and climate-resilient crop systems. Precision nutrient management tools were deployed across 42% of large-scale farms, while AI-driven crop monitoring platforms were used in more than 31,000 commercial farming operations. Agricultural drones and sensor-based irrigation systems together covered nearly 27% of irrigated farmland, reflecting rapid technological adoption.

Market Size & Growth: Valued at USD 23,200.4 million in 2025, projected to reach USD 57,854.9 million by 2033 at 12.1% CAGR, driven by demand for precision and sustainable farming technologies.

Top Growth Drivers: Precision irrigation adoption (49%), sensor-based crop monitoring (38%), carbon-reduction farming practices (26%).

Short-Term Forecast: By 2028, smart irrigation systems are expected to reduce water usage per hectare by 24%.

Emerging Technologies: AI-driven crop analytics, IoT soil sensors, autonomous electric farm machinery.

Regional Leaders: North America projected at USD 19.4 billion by 2033 with precision farming adoption; Europe at USD 14.8 billion driven by sustainability mandates; Asia Pacific at USD 16.2 billion supported by digital agriculture expansion.

Consumer/End-User Trends: Over 44% of large farms are adopting sensor-based irrigation and automated nutrient management systems.

Pilot or Case Example: In 2024, a precision farming pilot reduced fertilizer use by 21% while maintaining crop yield levels.

Competitive Landscape: John Deere leads with around 18% share, followed by Trimble, AGCO, CNH Industrial, and Climate Corporation.

Regulatory & ESG Impact: Carbon farming incentives and water-use regulations accelerating adoption of climate-smart solutions.

Investment & Funding Patterns: Over USD 12.3 billion invested globally between 2023–2025 in agri-tech and climate-smart solutions.

Innovation & Future Outlook: Integration of AI crop models, satellite imaging, and autonomous farm equipment shaping next-generation agriculture.

Precision farming accounts for nearly 46% of technology adoption, followed by smart irrigation at 28% and climate-resilient crop analytics at 26%. Innovations include AI-driven yield prediction, automated irrigation control, and carbon monitoring tools. Government sustainability incentives, rising water scarcity, and increasing global food demand are key factors shaping regional consumption and long-term market evolution.

The Climate-Smart Agriculture Technology Market is strategically vital as global agriculture transitions toward sustainable, resource-efficient, and climate-resilient production systems. Climate-smart technologies integrate precision farming tools, IoT sensors, and AI-based crop analytics to optimize water, fertilizer, and energy usage. AI-driven precision irrigation delivers up to 32% water savings compared to conventional flood irrigation systems, while improving crop yield consistency.

Regionally, Asia-Pacific dominates in volume due to extensive agricultural land and government-backed digital farming programs, while Europe leads in adoption with over 58% of large farms using at least one climate-smart technology platform. By 2028, AI-powered crop modeling is expected to improve yield forecasting accuracy by 27%, enabling more efficient resource allocation and risk management.

Sustainability and ESG commitments are accelerating technology adoption. Agricultural firms and cooperatives are targeting 30% reductions in greenhouse gas emissions from farming operations by 2030 through carbon-smart practices and efficient input management. In 2024, a European smart irrigation initiative achieved a 22% reduction in water consumption across more than 180,000 hectares using AI-driven soil moisture monitoring systems.

Future pathways emphasize autonomous electric farm equipment, satellite-based crop monitoring, and carbon credit integration platforms. By 2027, sensor-based nutrient management systems are expected to reduce fertilizer overuse by 25%. These advancements position the Climate-Smart Agriculture Technology Market as a pillar of agricultural resilience, regulatory compliance, and sustainable food production.

The Climate-Smart Agriculture Technology market is shaped by growing environmental concerns, water scarcity, and the need for higher agricultural productivity. Precision irrigation systems, AI-based crop analytics, and sensor-driven soil monitoring tools are enabling farmers to optimize resource usage. Demand is increasing across large-scale commercial farms and cooperatives seeking improved yield stability and cost efficiency. Government incentives for carbon reduction and sustainable farming practices are accelerating technology adoption. At the same time, advances in satellite imaging, autonomous machinery, and data analytics are enhancing farm-level decision-making, improving crop performance, and reducing environmental impact.

Water scarcity is a major driver for the Climate-Smart Agriculture Technology market. Agriculture accounts for nearly 70% of global freshwater consumption, making efficient irrigation systems critical. Smart irrigation technologies reduce water use by up to 30% while maintaining or improving crop yields. In 2025, over 45% of newly installed irrigation systems in developed agricultural regions incorporated sensor-based automation. These systems optimize watering schedules based on soil moisture and weather forecasts, improving efficiency and reducing operational costs for farmers.

Despite long-term benefits, high initial investment costs remain a barrier. Precision farming equipment, IoT sensors, and automated irrigation systems can cost 20–40% more than traditional farming tools. In developing regions, nearly 36% of small and medium-sized farms delay adoption due to limited financing options. Lack of technical expertise and digital infrastructure further slows implementation, particularly in rural areas.

Carbon credit programs present significant opportunities for the Climate-Smart Agriculture Technology market. Climate-smart practices such as reduced tillage and precision fertilizer application can lower farm-level emissions by up to 18%. In 2025, more than 22 million hectares of farmland globally were enrolled in carbon farming initiatives. These programs provide additional revenue streams for farmers adopting climate-smart technologies, accelerating market expansion.

Climate-smart systems rely on data from multiple sources, including sensors, satellites, and farm equipment. Lack of standardized data platforms creates interoperability challenges, limiting seamless integration. In 2025, nearly 29% of farmers reported difficulties integrating data across different precision farming tools. These technical barriers increase implementation complexity and reduce potential efficiency gains.

Expansion of Precision Irrigation Systems: In 2025, over 49% of newly installed irrigation systems incorporated sensor-based automation, reducing water usage by up to 28% and improving crop yield stability by 19%.

Growth of AI-Based Crop Monitoring Platforms: Approximately 37% of large farms adopted AI-powered crop analytics in 2024, improving disease detection accuracy by 33% and reducing pesticide use by 21%.

Adoption of Autonomous Electric Farm Equipment: Around 22% of large agricultural operations deployed autonomous or electric tractors by 2025, reducing fuel consumption by 26% and lowering maintenance costs by 18%.

Rise of Satellite-Based Climate Monitoring: Nearly 41% of precision agriculture platforms integrated satellite imaging in 2025, improving weather prediction accuracy by 24% and enabling better crop planning decisions.

The Climate-Smart Agriculture Technology market is segmented by technology type, application, and end-user categories, reflecting diverse agricultural needs across regions. Technologies include precision irrigation, soil and crop monitoring systems, and autonomous farm equipment. Applications span crop production, livestock management, and greenhouse operations. End-user demand varies between large commercial farms, agricultural cooperatives, and smallholder farmers, each with different resource and technology requirements.

Precision irrigation systems account for approximately 46% of adoption due to their direct impact on water savings and yield optimization. Soil and crop monitoring technologies represent about 31%, enabling data-driven decision-making. However, autonomous and electric farm machinery is the fastest-growing segment, expected to expand at over 13% CAGR, driven by labor shortages and sustainability goals. Other technologies, including climate analytics platforms and carbon monitoring tools, collectively represent 23% of adoption.

In 2025, a national irrigation modernization program deployed sensor-based systems across 2.1 million hectares, reducing water consumption by 24%.

Crop production remains the leading application with a 54% share, supported by widespread adoption of precision irrigation and nutrient management tools. Livestock management accounts for 23%, while greenhouse and controlled-environment agriculture is the fastest-growing application, expanding above 11% CAGR due to water efficiency and climate control requirements. Other applications, including agroforestry and aquaculture, represent 23%. In 2025, more than 41% of large farms adopted at least one climate-smart technology solution.

In 2024, climate-smart irrigation and crop monitoring tools were deployed across over 3,000 greenhouse facilities, reducing water consumption by 27%.

Large commercial farms represent the leading end-user segment at 49%, driven by their capacity to invest in advanced technologies. Agricultural cooperatives are the fastest-growing segment, expanding at over 12% CAGR as shared technology platforms reduce costs. Smallholder farmers and government agricultural projects collectively account for 51% of adoption. In 2025, more than 38% of agricultural enterprises reported piloting climate-smart technologies to improve sustainability.

In 2025, a national agricultural digitization initiative equipped over 600,000 farmers with climate-smart tools, improving resource efficiency by 23%.

North America accounted for the largest market share at 34.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2026 and 2033.

North America deployed climate-smart technologies across more than 118 million hectares of farmland in 2025, with precision irrigation systems covering nearly 46 million hectares and sensor-based nutrient management used on 39% of commercial farms. Europe represented 27.6% of global adoption, supported by sustainability mandates across more than 52 million hectares of regulated agricultural land. Asia-Pacific accounted for 25.1%, with China, India, and Japan collectively deploying climate-smart tools across over 210 million hectares of cultivated land. South America held 7.3% of demand, driven by soybean, maize, and sugarcane farms adopting precision irrigation across 18 million hectares. Middle East & Africa represented 5.2%, with smart irrigation systems covering over 9.4 million hectares across arid agricultural zones.

How are precision irrigation and digital farming platforms transforming large-scale commercial agriculture?

North America accounted for approximately 34.8% of the Climate-Smart Agriculture Technology market in 2025, supported by strong adoption across commercial grain, soybean, and corn farming operations. More than 62% of large farms deployed sensor-based irrigation systems, while AI-powered crop monitoring tools were used across over 41 million hectares. Government-backed sustainability initiatives promoted water-efficient irrigation and carbon-smart farming practices, with over 19 million hectares enrolled in carbon reduction programs. Technological advancements include autonomous tractors, satellite-driven crop analytics, and integrated farm management platforms. A regional agricultural equipment provider deployed autonomous electric tractors across 4,800 farms, reducing fuel consumption by 24%. Consumer behavior in the region shows strong enterprise-level adoption among large-scale agricultural operations and agribusiness corporations.

Why are sustainability mandates accelerating adoption of precision farming solutions?

Europe represented approximately 27.6% of the Climate-Smart Agriculture Technology market in 2025, with Germany, France, and the UK accounting for nearly 64% of regional demand. Over 52 million hectares of farmland were subject to sustainability regulations encouraging water efficiency and carbon reduction. Precision irrigation systems were installed across 44% of commercial farms, while digital soil monitoring platforms covered more than 23 million hectares. The region is witnessing strong adoption of satellite-based crop monitoring, automated nutrient application, and low-emission farm machinery. A European agri-tech firm expanded its smart irrigation solutions across 7,200 farms, reducing water usage by 21%. Consumer behavior is shaped by regulatory compliance requirements, driving demand for sustainable and data-driven agricultural technologies.

What factors are driving large-scale adoption of digital agriculture across emerging farming economies?

Asia-Pacific accounted for approximately 25.1% of the global Climate-Smart Agriculture Technology market in 2025, with China, India, and Japan as the largest consuming countries. The region deployed climate-smart solutions across more than 210 million hectares of farmland, supported by government-backed digital agriculture initiatives. Smart irrigation covered nearly 58 million hectares, while AI-based crop monitoring tools were used in over 19 million farming operations. Technology hubs in China and Japan are advancing autonomous farming machinery and precision nutrient management systems. A regional agri-tech company deployed IoT-based irrigation platforms across 3.2 million hectares, improving water efficiency by 26%. Consumer behavior reflects rapid adoption among small and medium-sized farms using mobile-based agricultural applications.

How are export-oriented farms adopting precision agriculture to improve productivity?

South America accounted for approximately 7.3% of the Climate-Smart Agriculture Technology market in 2025, led by Brazil and Argentina. Brazil represented nearly 61% of regional demand, supported by large-scale soybean and sugarcane farms deploying precision irrigation across more than 12 million hectares. Government incentives for sustainable farming practices reduced equipment import duties by up to 8%, encouraging technology adoption. Precision fertilizer management tools were used across 38% of export-oriented farms. A regional agri-tech provider implemented climate-smart crop monitoring systems across 6,500 farms, improving yield consistency by 18%. Consumer behavior in the region is tied to export-driven crop production and large commercial farming operations.

Why are water scarcity and irrigation modernization driving climate-smart technology demand?

The Middle East & Africa accounted for approximately 5.2% of global Climate-Smart Agriculture Technology demand in 2025, with UAE, Saudi Arabia, and South Africa leading adoption. Smart irrigation systems covered more than 9.4 million hectares across arid and semi-arid regions. Government modernization programs invested over USD 2.8 billion in water-efficient agriculture infrastructure. Controlled-environment agriculture and greenhouse systems expanded across 18,000 hectares using sensor-driven irrigation and climate control technologies. A regional agricultural technology provider deployed smart irrigation solutions across 2,300 farms, reducing water consumption by 29%. Consumer behavior reflects premium technology adoption in Gulf countries and cost-efficient irrigation solutions across African agricultural economies.

United States Climate-Smart Agriculture Technology Market – 28.4%: Extensive adoption of precision irrigation, autonomous farm equipment, and carbon-smart farming programs.

China Climate-Smart Agriculture Technology Market – 19.7%: Large-scale deployment of digital agriculture platforms and smart irrigation across extensive cultivated land.

The Climate-Smart Agriculture Technology market is moderately fragmented, with more than 65 active global and regional competitors offering precision irrigation, farm automation, crop analytics, and carbon monitoring solutions. The top five companies collectively account for approximately 42% of global adoption, supported by strong equipment portfolios and integrated digital platforms.

Between 2023 and 2025, more than 90 strategic partnerships were announced across the agri-tech ecosystem, including collaborations between equipment manufacturers, satellite imaging providers, and agricultural software companies. Over 120 new product launches focused on AI-based crop analytics, autonomous machinery, and sensor-driven irrigation systems during the same period. Competitive positioning is increasingly driven by integrated platforms combining hardware, software, and data analytics. Technology providers are investing in predictive analytics, carbon accounting tools, and autonomous farm equipment to differentiate offerings and improve resource efficiency across large-scale agricultural operations.

John Deere

Trimble Inc.

AGCO Corporation

CNH Industrial

The Climate Corporation

Kubota Corporation

Yara International

Raven Industries

Lindsay Corporation

Netafim

Taranis

Granular

Technological innovation in the Climate-Smart Agriculture Technology market is centered on precision irrigation, AI-driven crop analytics, and autonomous farming systems. Sensor-based irrigation systems can reduce water consumption by up to 30% while maintaining crop yield levels. AI-powered crop monitoring platforms improve disease detection accuracy by nearly 35%, enabling timely intervention and reducing pesticide use by over 20%.

Satellite imaging is becoming a core component of climate-smart agriculture, with over 41% of precision farming platforms integrating satellite data for weather prediction and crop health analysis. Autonomous electric tractors and robotic harvesting systems are improving labor productivity by up to 28% and reducing fuel consumption by nearly 25%. Soil nutrient monitoring sensors are also advancing, providing real-time data that can reduce fertilizer overuse by up to 22%.

Emerging technologies include carbon monitoring platforms that track farm-level emissions and generate carbon credits, as well as digital twin models of agricultural fields that simulate crop performance under different climate conditions. Integration of IoT devices, cloud-based analytics, and mobile applications is enabling farmers to manage operations remotely, improving decision-making efficiency and sustainability across large-scale agricultural systems.

In March 2025, John Deere introduced an upgraded autonomous tractor platform with AI-driven navigation, enabling fully driverless field operations across large farms and improving fuel efficiency by nearly 20%. Source: www.deere.com

In November 2024, Trimble launched an advanced precision irrigation control system integrating satellite data and soil sensors, reducing water usage by up to 25% across pilot farms. Source: www.trimble.com

In September 2024, AGCO expanded its smart farming portfolio with an AI-based crop monitoring platform deployed across more than 2 million hectares of farmland. Source: www.agcocorp.com

In May 2024, CNH Industrial introduced a new autonomous electric tractor prototype designed for precision farming, reducing operational emissions by approximately 30% compared to diesel models. Source: www.cnhindustrial.com

The Climate-Smart Agriculture Technology Market Report provides a comprehensive assessment of technologies, applications, and end-user segments across global agricultural systems. The scope includes precision irrigation systems, AI-based crop analytics, soil and nutrient monitoring sensors, autonomous farm machinery, and carbon monitoring platforms designed to improve sustainability and productivity.

Applications analyzed include crop production, livestock management, greenhouse operations, and agroforestry. The report evaluates the adoption of climate-smart solutions across large commercial farms, agricultural cooperatives, smallholder farms, and government-backed agricultural projects. More than 380 million hectares of farmland globally are assessed for climate-smart technology adoption potential.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for major agricultural producers. The report also covers emerging segments such as carbon credit farming, satellite-based crop monitoring, and autonomous electric farm equipment. It provides strategic insights into technology deployment, resource efficiency improvements, regulatory impacts, and competitive positioning relevant to equipment manufacturers, agri-tech firms, agricultural cooperatives, and sustainability-focused investors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 23,200.4 Million |

|

Market Revenue in 2033 |

USD 57,854.9 Million |

|

CAGR (2026 - 2033) |

12.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Topcon Agriculture, Valmont Industries, CropX, John Deere, Trimble Inc., AGCO Corporation, CNH Industrial, The Climate Corporation, Kubota Corporation, Yara International, Raven Industries, Lindsay Corporation, Netafim, Taranis, Granular |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |