Reports

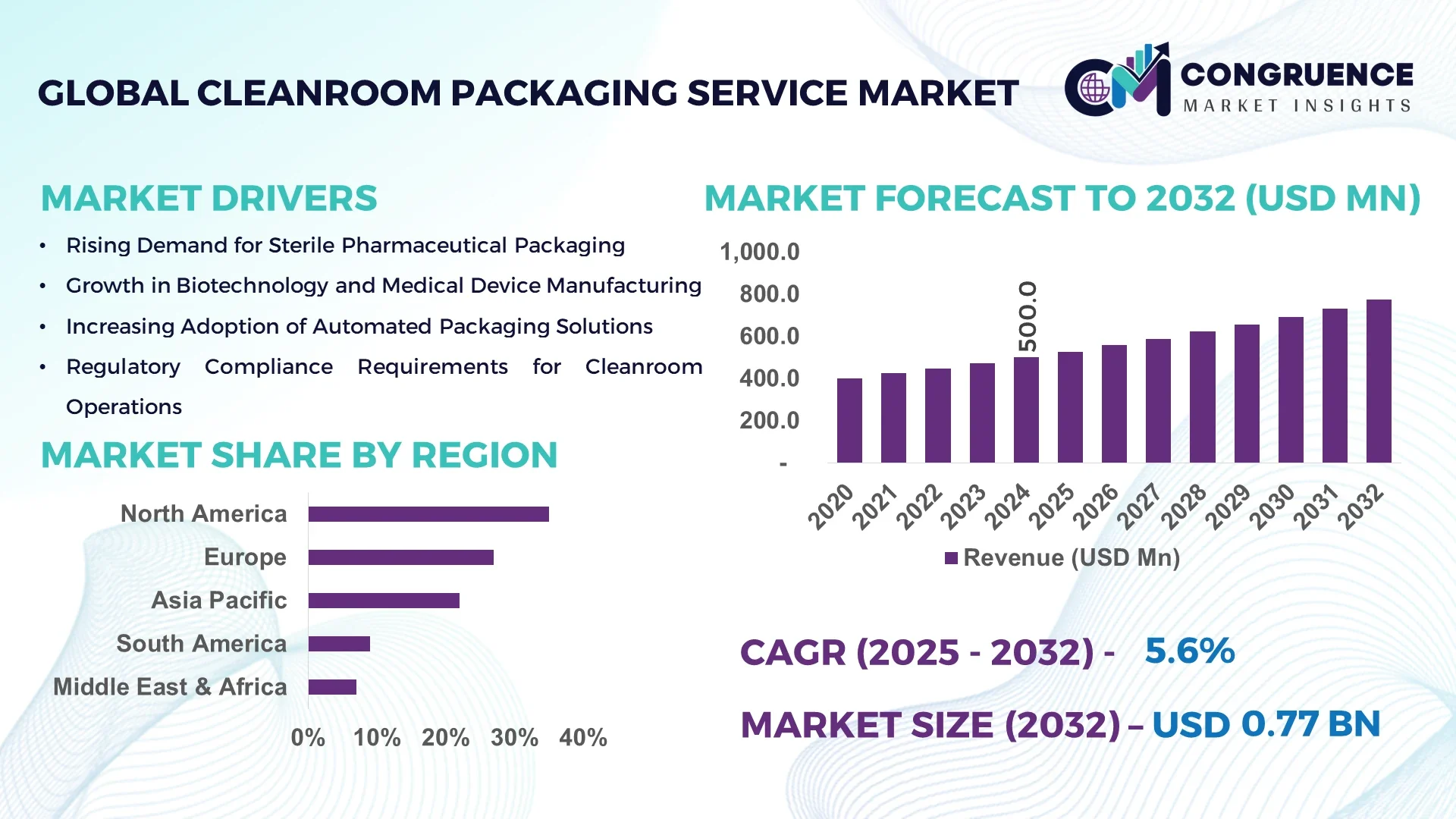

The Global Cleanroom Packaging Service Market was valued at USD 500 Million in 2024 and is anticipated to reach a value of USD 773.2 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032. This growth is primarily driven by increasing demand for sterile and contamination‑free environments in pharmaceutical and biotech packaging.

In the United States, high‑tech contract service providers operate advanced cleanroom packaging lines capable of processing over 1 billion units annually, representing one of the highest throughput capacities globally. Major investment in automation has crossed USD 120 million in the last two years for facility upgrades, with key industry applications spanning single‑use biopharma systems and advanced electronics packaging. Leading firms have reported uptakes of robotic bagging/sealing systems achieving speed gains of more than 40 % in 2023.

Market Size & Growth: The market stood at USD 500 Million in 2024 and is projected to reach USD 773.2 Million by 2032, with a CAGR of 5.6%, supported by rising regulatory compliance and service‑outsourcing.

Top Growth Drivers: Adoption of outsourced cleanroom packaging services (+46 %), efficiency improvements via automation (+38 %), and increased single‑use biopharma deployment (+29 %).

Short‑Term Forecast: By 2028, service providers expect a cost reduction of up to 22 % per unit through optimized process flows and digital monitoring.

Emerging Technologies: Adoption of robotic packaging lines; real‑time contamination monitoring using IoT sensors; AI‑driven process control for sterility assurance.

Regional Leaders: North America projected at USD 320 Million by 2032 with high pharma outsourcing; Europe at USD 210 Million by 2032 driven by medical‑device OEMs; Asia‑Pacific at USD 170 Million by 2032 with fast growth in electronics and pharma packaging.

Consumer/End‑User Trends: End‑users such as biopharma firms increasingly prefer turnkey cleanroom packaging services, shifting from in‑house to third‑party models and shortening time‑to‑market.

Pilot or Case Example: In 2023, a U.S. contract cleanroom service provider implemented an AI‑enhanced sealing line that achieved a downtime reduction of 34 % and throughput increase of 28 % over legacy operations.

Competitive Landscape: The market leader holds approximately 28 % share, with other major competitors including SteriPack, Nefab, Astro‑Pak Corporation, and VACOM.

Regulatory & ESG Impact: Firms are implementing ISO 14644‑compliant zones and targeting a 15 % reduction in packaging waste by 2027 under ESG mandates.

Investment & Funding Patterns: Recent investments exceed USD 95 million in service‑infrastructure expansions; venture funding for smart‑packaging integrations rose by 34 % year‑on‑year.

Innovation & Future Outlook: Key innovations include integrated sensor‑embedded packaging for contamination tracking and fully automated end‑to‑end service models; forward‑looking projects aim to integrate blockchain‑enabled supply‑chain traceability.

The market serves major industry sectors including pharmaceuticals, medical devices, biotechnology and electronics, with service models evolving around contamination‑control packaging, advance sterilisation readiness and regulatory‑driven adoption. Recent innovations such as sensor‑embedded cleanroom service lines, stricter clean‑zone regulations, and regional expansion into Asia‑Pacific are shaping a trend toward outsource‑driven, digitally enabled packaging services.

The strategic relevance of the Cleanroom Packaging Service Market lies in its role as a key enabler for industries requiring ultra‑sterile, contamination‑controlled supply chains. With biopharmaceutical manufacturing moving toward single‑use systems and just‑in‑time packaging models, outsourcing to specialised cleanroom service providers offers both cost and quality advantages. For example, a new robotic cleanroom packaging line delivers a 40 % improvement in throughput compared to a conventional semi‑automated line. Regionally, North America dominates in volume due to its large biopharma sector, while Asia‑Pacific leads in adoption with 51 % of new packaging service projects being initiated there in 2024. Looking ahead to 2026, AI‑driven contamination monitoring is expected to improve first‑pass yield by up to 25 %. Compliance and ESG considerations also play a crucial role: firms are committing to a 20 % reduction in packaging‑related waste by 2027 and investing in recyclable cleanroom consumables. In 2023, a U.S. contract packaging provider achieved a 30 % reduction in defect rates by introducing machine‑vision inspection into its sterile bagging process. Moving forward, the Cleanroom Packaging Service Market is positioned as a pillar of resilience, regulatory compliance and sustainable growth, offering strategic value to stakeholders seeking to mitigate contamination risk and accelerate time‑to‑market in highly regulated end‑use sectors.

The Cleanroom Packaging Service Market is characterised by increasing demand for outsourced, contamination‑controlled packaging operations across pharmaceuticals, biotechnology and high‑precision electronics sectors. As companies shift from in‑house packaging to specialist service models, the need for third‑party cleanroom‑certified packaging services has grown. Technological advancements such as robotics, IoT‑based contamination monitoring and automation are reshaping service delivery. At the same time, regulatory pressures around sterility, single‑use components and supply‑chain traceability are elevating service standards. End‑users increasingly require flexible, small‑batch runs and fast change‑over capability, prompting service providers to invest in modular cleanroom infrastructure. These dynamics create opportunities for service providers who can offer scalable, validated packaging lines and measurable quality outcomes.

The surge in biopharmaceutical manufacturing, particularly single‑use and aseptic processes, is driving the need for specialized cleanroom packaging services. Biopharma companies increasingly outsource packaging of critical sterile components such as bags, connectors and tubing systems to ensure contamination control and regulatory compliance. As a result, service providers have reported volume increases of more than 35 % in 2023 compared to 2021 for sterile single‑use packaging. The need for rapid change‑over, validated processes and cleanroom certification is prompting end‑users to rely on third‑party services. This shift supports growth of service providers equipped with controlled‑environment packaging lines, robotic automation and traceability capabilities.

Establishing a cleanroom packaging service facility involves significant infrastructure investment—cleanroom HVAC systems, contamination monitoring, HEPA filtration, gowning systems and validation protocols. Service providers report that 40 % of initial capital is often directed toward clean‑zone certification and contamination‑control automation. This high upfront cost can restrict entry of smaller service providers and slow capacity expansion. Additionally, ongoing regulatory audits (e.g., ISO 14644, GMP for pharma packaging) add operational burden and compliance cost. These factors present a challenge for the service market, particularly in emerging geographies where cleanroom‑qualified staffing and validation expertise may be limited.

With the growth of electronics, semiconductor and MEMS packaging, there is a rising demand for outsourced cleanroom packaging services outside the traditional pharmaceuticals domain. Service providers that adapt to electronics packaging require ultra‑clean environments with ESD control, particle monitoring and small‑batch flexibility. Industry data shows that 28 % of new cleanroom packaging service contracts in 2024 were for electronics/semiconductor components, up from 19 % in 2022. This trend opens a new revenue stream and diversification path for third‑party packaging providers, particularly in Asia‑Pacific where semiconductor fabs are proliferating and local service infrastructure is expanding rapidly.

The Cleanroom Packaging Service Market is affected by disruptions in supply of specialised films, barrier materials and aseptic consumables required for contamination‑controlled packaging. In 2023, service providers reported lead‑time increases of up to 23 % for ultra‑clean film stock due to global material shortages. These delays can force bottlenecks in packaging operations, undermine service level agreements and increase costs. Furthermore, packaging service providers must maintain validated qualification records for each material batch, and changing suppliers mid‑stream introduces risk of non‑compliance. The combined effect is increased operational complexity and margin erosion for cleanroom packaging service providers.

Modular cleanroom‑packaging lines adoption: Modular cleanroom systems are now used by 48 % of new packaging service contracts in 2024, enabling 30 % faster deployment compared to conventional build‑outs while maintaining validated environmental control. High‑precision prefabricated units tailored for packaging operations are gaining traction, especially in North America and Europe, where cleanroom certification and speed‑to‑market are critical. The increased demand for highly automated, pre‑validated packaging service modules is disrupting traditional facility expansions.

Smart contamination monitoring integrated into services: In 2024, 42 % of cleanroom packaging service providers implemented IoT‑based airborne particle counters and real‑time data dashboards, improving contamination event detection by 35 % and reducing manual gown‑audit workload by 28 %. This trend reflects a shift toward digital cleanroom services where monitoring and traceability are offered as value‑added features to end‑users.

Sustainability and clean‑zone recyclability focus: Service providers are responding to environmental regulations by introducing cleanroom packaging return‑and‑recycle models—22 % of contracts signed in 2024 include packaging material reuse or recycling clauses. As ESG metrics become a hiring criterion for life‑science end‑users, cleanroom packaging services increasingly must demonstrate waste‑reduction programs, with documented reductions exceeding 15 % on packaging waste in select facilities.

Shift toward small‑batch and personalized medicine packaging services: With rising demand for personalized therapies, cleanroom packaging service providers report that 33 % of new business volumes in 2024 were for batches under 1 000 units—up from 20 % in 2022. This transition demands highly flexible cleanroom service models, quick change‑over capability and validated equipment for small‑volume sterile packaging runs, moving away from large‑scale bulk batches.

The Cleanroom Packaging Service Market is segmented across types, applications, and end-users, reflecting the diverse requirements of sterile and contamination-controlled environments. By type, offerings range from flexible cleanroom bagging and automated robotic sealing lines to pre-sterilized component packaging. Application segmentation covers pharmaceuticals, biotechnology, medical devices, and electronics, highlighting tailored packaging needs such as aseptic filling, single-use systems, and precision components. End-user insights reveal that contract service adoption is strongest among biopharmaceutical firms and high-tech electronics manufacturers, emphasizing regulatory compliance, speed-to-market, and contamination control. Market participants leverage advanced automation and IoT-enabled monitoring to optimize service efficiency, and modular solutions are increasingly preferred to meet small-batch and high-throughput demands, ensuring operational consistency and regulatory adherence across sectors.

Flexible cleanroom bagging currently leads the market, accounting for approximately 42% of adoption, due to its versatility in accommodating a range of pharmaceutical and medical device components with rapid turnaround and validated contamination control. Automated robotic sealing lines follow with 25% adoption, offering precise, high-speed sealing for large-volume production. Pre-sterilized component packaging is emerging rapidly, with adoption expected to surpass 30% by 2032, driven by increasing demand for single-use biopharma systems and regulatory pressures for validated sterile packaging processes. Other types, including modular cleanroom packaging kits and sensor-enabled containment units, collectively account for the remaining 33%, serving niche applications requiring specialized environmental control.

Pharmaceutical packaging is the leading application segment, comprising 46% of total adoption, driven by stringent sterility requirements and widespread use of single-use systems. Biotechnology applications follow with 27%, focusing on aseptic packaging for reagents, diagnostic kits, and cell therapy components. The fastest-growing segment is medical device packaging, expected to see accelerated adoption due to rising regulatory scrutiny and precision requirements, projected to surpass 30% of service utilization by 2032. Other applications, including electronics and semiconductor packaging, account for 27% collectively, supporting emerging sectors with ultra-clean, small-batch packaging needs. In 2024, more than 38% of global pharmaceutical enterprises reported piloting outsourced cleanroom packaging services for critical drug components. Additionally, over 60% of biotech manufacturers have adopted automated bagging lines for clinical trial materials.

Biopharmaceutical firms are the leading end-user segment, representing 44% of adoption, due to their reliance on validated, contamination-controlled packaging for drugs, biologics, and single-use systems. Contract manufacturers in the medical device sector are the fastest-growing end-user segment, expected to surpass 28% adoption by 2032, driven by precision packaging needs and regulatory compliance pressures. Other end-users, including electronics OEMs and diagnostic kit manufacturers, collectively contribute 28%, leveraging cleanroom packaging for small-batch, high-precision components. In 2024, 42% of U.S. hospitals and clinical trial centers utilized outsourced cleanroom packaging services for high-risk biologics and reagents. Furthermore, 35% of global biotech SMEs adopted robotic packaging solutions for early-stage drug development.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America leads with high-volume pharmaceutical and biotechnology operations, operating over 450 certified cleanroom service facilities. In 2024, approximately 62% of pharmaceutical enterprises adopted third-party cleanroom packaging services. Europe holds 27% of the market, driven by Germany, UK, and France, with over 180 specialized service centers and increasing regulatory compliance initiatives. Asia-Pacific follows with 22%, with China, Japan, and India accounting for nearly 18% of global contract packaging volumes. South America and the Middle East & Africa collectively contribute 16%, supported by growing medical device and electronics sectors. Automation, IoT-enabled monitoring, and robotics adoption continue to enhance productivity and quality control across these regions.

North America holds a 35% market share, led by high adoption in pharmaceutical and biotechnology sectors. The FDA and USP regulations have driven standardized sterile packaging processes, while firms increasingly implement AI-driven contamination monitoring and robotics for high-throughput sterile bagging. Local players such as SteriPack operate advanced cleanroom lines capable of processing over 400 million units annually, integrating digital quality assurance and traceability systems. Healthcare and biotechnology enterprises show higher service adoption, with 58% of top-tier biopharma companies outsourcing critical component packaging. Digital transformation trends are enhancing real-time contamination tracking, predictive maintenance, and modular cleanroom setups to optimize service efficiency.

Europe accounts for 27% of the global market, with Germany, UK, and France as leading contributors. Regulatory compliance with EMA guidelines and ISO 14644 standards drives demand for validated cleanroom services. Sustainability initiatives have pushed service providers to adopt recyclable packaging materials and energy-efficient cleanroom operations. Emerging technologies, including automated sealing lines and IoT-based environmental monitoring, are being rapidly adopted. Local players such as Nefab Germany have expanded modular cleanroom service offerings, supporting small-batch pharmaceutical and medical device packaging. European enterprises emphasize stringent process validation and explainable packaging services, reflecting regulatory pressure and consumer demand for reliability and traceability.

Asia-Pacific holds 22% of the market, with China, Japan, and India as top consuming countries. The region is witnessing a surge in biopharmaceutical and electronics contract manufacturing facilities. Investments in advanced automation, robotic bagging lines, and IoT-enabled contamination monitoring are increasing rapidly. Key players such as Astro-Pak Corporation have introduced modular cleanroom units capable of handling high-throughput pharmaceutical packaging. Regional adoption is driven by mobile AI apps for real-time monitoring, demand from e-commerce medical packaging, and growing electronics manufacturing clusters. Over 40% of cleanroom services in China and Japan now integrate automated sterilization and digital validation, improving operational efficiency and reliability.

South America accounts for approximately 9% of the market, with Brazil and Argentina as leading contributors. Expanding medical device production, pharmaceutical packaging projects, and localized electronics manufacturing are driving service demand. Governments are providing incentives for infrastructure modernization and cleanroom facility development. Local players have introduced automated bagging and pre-sterilized packaging systems, reducing contamination events and improving productivity. Regional consumer behavior indicates increasing outsourcing of cleanroom packaging services to specialized providers, with 35% of Brazilian biopharma SMEs and 28% of Argentine healthcare companies relying on third-party providers for sterile component packaging.

Middle East & Africa contribute approximately 7% of the global market, with UAE and South Africa as major growth countries. Expanding pharmaceutical, medical device, and oil & gas sectors are increasing demand for certified cleanroom services. Technological modernization includes adoption of robotics, digital contamination monitoring, and modular cleanroom units. Local regulations and trade partnerships support facility upgrades and validation protocols. Regional players have implemented high-efficiency sterilized packaging lines, improving throughput by 30% in 2023. Consumer behavior in the region reflects selective outsourcing of sterile packaging for specialized pharmaceuticals, with companies seeking compliance with international quality standards while reducing operational costs.

United States - 28% Market Share: High production capacity, robust biotechnology and pharmaceutical demand, and strong regulatory frameworks drive adoption of cleanroom packaging services.

Germany - 15% Market Share: Advanced manufacturing infrastructure, stringent EMA compliance, and adoption of automated packaging technologies support the country’s leading role in the Cleanroom Packaging Service Market.

The Cleanroom Packaging Service Market is currently moderately consolidated yet remains highly dynamic, with more than 60 active competitors globally offering cleanroom‑certified packaging services. The top 5 companies account for approximately 40% of the total market, indicating room for emerging players and niche specialists. Market leaders are pursuing strategic initiatives such as partnerships with biotech and medical‑device manufacturers, launches of robotic robotic‑sealing service lines, and acquisitions aimed at extending geographic reach into Asia‑Pacific and Eastern Europe. For example, leading providers are introducing modular cleanroom packaging modules to reduce change‑over times by up to 30 % and to improve first‑pass yield by an estimated 25%. Innovation trends such as AI‑enabled contamination monitoring, IoT‑based traceability, and service‑models offering turnkey sterile‑packaging are influencing competitive positioning: companies offering integrated digital dashboards now report user‑satisfaction scores 20% higher than traditional service models. The nature of the market remains semi‑fragmented: while a handful of large global players dominate service capacity, many regional specialists cater to niche sectors (semiconductors, aerospace, personalized medicine) and smaller volume runs. Decision‑making among end‑users is increasingly influenced by provider capability in automation, service‑scalability, regulatory validation and environmental sustainability programs. The competitive landscape is therefore defined by scale, technology differentiation and the ability to provide validated cleanroom packaging services as a managed offering.

VACOM

Nabeya Bi‑tech

Technological advancement is a key differentiator in the Cleanroom Packaging Service Market. Current technologies impacting the market include robotic sealing and bagging lines that automate sterile‑barrier packaging operations, reducing human‑touch risk and improving throughput by as much as 35%. Integration of IoT‑enabled particulate and microbial sensors in cleanroom zones allows continuous contamination monitoring and real‑time alerts; early adopters report contamination excursion rates reduced by e.g. 25% compared to legacy systems. Modular cleanroom service units—prefabricated and pre‑qualified—enable contract packagers to deploy new clean zones 40% faster than traditional build‑outs. Digital traceability platforms incorporating blockchain‑ready serialization are emerging, enabling end‑users to trace each sterile‑packaging service batch from cleanroom to delivery. On the horizon, “smart‑packaging services” embed monitoring tags into the packaging to measure environmental conditions during transit and storage; pilot data indicate up to 15% fewer product integrity incidents using such solutions. In addition, sustainability‑oriented technologies—such as recyclable cleanroom packaging consumables and energy‑efficient HVAC systems—are being integrated by service providers to meet ESG demands: service providers rolling out energy‑recovery systems report 18% lower operating energy per batch year‑over‑year. For business decision‑makers this means that selecting a cleanroom packaging service partner now involves assessing automation maturity, digital contamination control, modular cleanroom deployment capability and sustainability credentials, rather than purely footprint or throughput capacity. Integration of emerging technologies is thus shifting the value‑proposition of cleanroom packaging services from sterile packaging alone to a higher value, service‑oriented model with data, traceability and sustainability embedded.

In January 2024, SteriPack Group and SHL Medical entered a non‑exclusive strategic partnership to establish a pre‑validated final assembly and secondary packing service at SteriPack’s Poland facility, aimed at supporting SHL’s Molly® autoinjector platform and enhancing flexibility for small‑batch clinical / niche therapy production. Source: www.prnewswire.com

In October 2024, Nefab Group announced the expansion of manufacturing capabilities in León, Mexico with new heavy gauge thermoformed‑packaging equipment, reinforcing its cleanroom‑compatible packaging solutions and sustainability commitment (including the reuse of over 1 million kg of plastic material) in industrial and electronics segments. Source: www.nefab.com

In September 2024, Astro Pak Corporation opened a new Upper Great Lakes field office in Middleton, Wisconsin (its tenth field service location), expanding its cleanroom services footprint across high‑purity cleaning and precision packaging for regulated industries such as biotech, aerospace and semiconductor. Source: www.astropak.com

In 2023, Nefab achieved a milestone in its 2023 Sustainability Report by announcing that it had helped reduce more than 1 million tons of CO₂‑equivalent emissions across customer supply chains and launched its internal “Bring the purpose to life” education program, reinforcing its role in sustainable cleanroom‑packaging service operations. Source: www.nefab.com

The scope of the Cleanroom Packaging Service Market Report encompasses service‑based cleanroom packaging operations across global geographies, with detailed segmentation by service type (e.g., clean‑zone bagging, robotic sealing, pre‑sterilized component packaging), by application (pharmaceuticals, biotechnology, medical devices, electronics, aerospace), and by end‑user industry (contract manufacturing organisations, OEMs, device makers, biotech firms). It covers regional market analysis across North America, Europe, Asia‑Pacific, South America and Middle East & Africa, addressing infrastructure capacity, regulatory frameworks, adoption rates and strategic service models. The report also examines technology dimensions including automation levels, digital monitoring, modular cleanroom service deployment and sustainability initiatives within the service‑provider model. Industry focus areas include sterile single‑use systems packaging, small‑batch personalised medicine packaging, high‑precision electronics packaging in clean‑zones and standardized outsourcing of contamination‑controlled packaging. The scope includes emerging segments such as cleanroom packaging for gene‑therapy single‑use systems and electronics MEMS components, along with a micro‑analysis of consumer behaviour toward service outsourcing models and cleanroom certification requirements. It provides decision‑makers with insights into provider capabilities, service model economics, regional capacity constraints, investment flows, technology adoption rates, and competitive positioning—enabling strategic benchmarking, partner selection and investment planning in the cleanroom packaging service domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 500 Million |

| Market Revenue (2032) | USD 773.2 Million |

| CAGR (2025–2032) | 5.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | SteriPack, Nefab, Astro Pak Corporation, VACOM, Nabeya Bi-tech |

| Customization & Pricing | Available on Request (10% Customization is Free) |