Reports

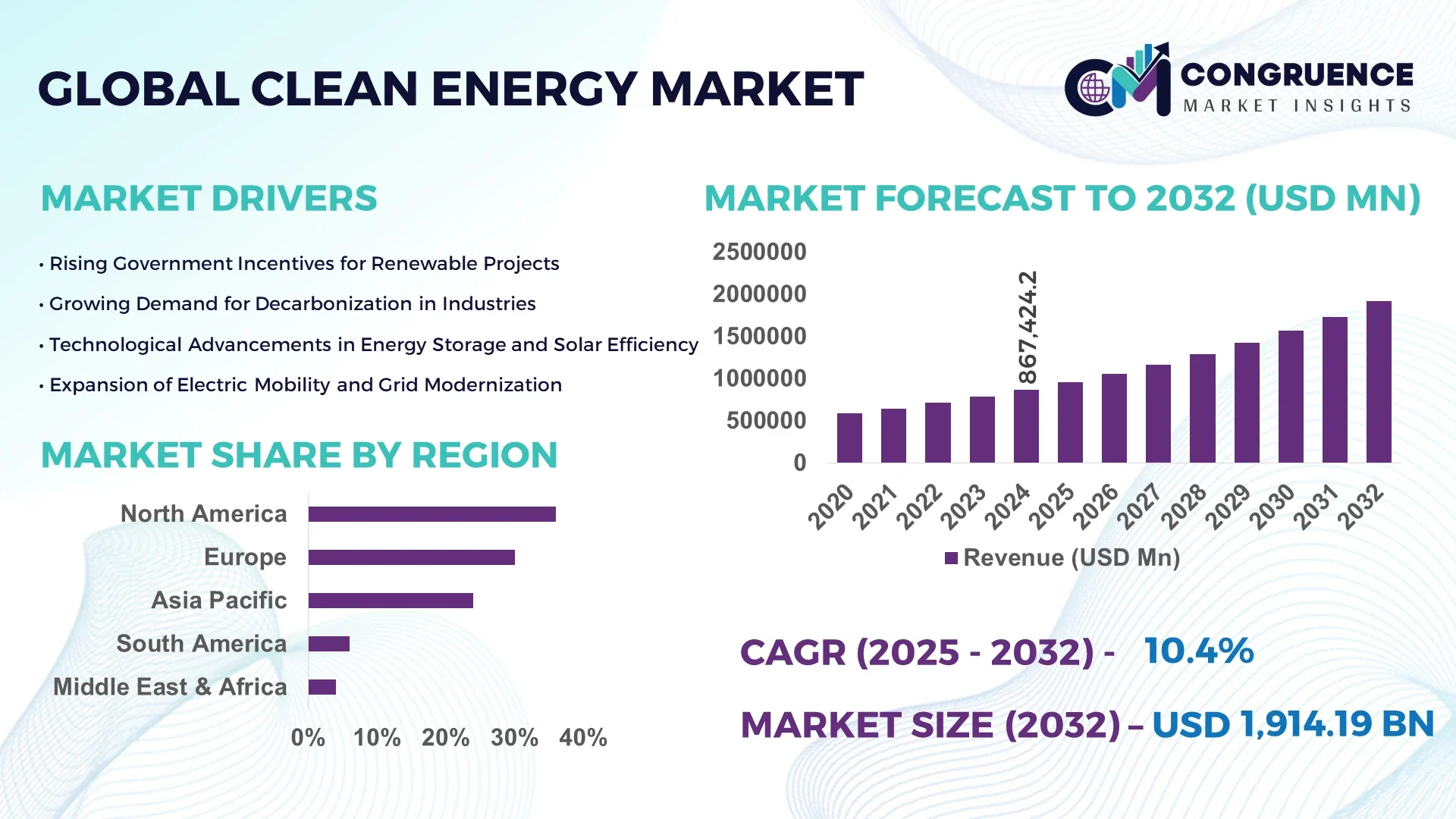

The Global Clean Energy Market was valued at USD 867,424.2 Million in 2024 and is anticipated to reach a value of USD 1,914,185.9 Million by 2032 expanding at a CAGR of 10.4% between 2025 and 2032. Growth is driven by accelerating investments in renewable infrastructure, grid-scale energy storage, and decarbonization mandates.

China plays a dominant role in the Clean Energy market, contributing a staggering volume of capacity additions annually. In 2024, China added over 373 GW of renewable capacity, bringing its total installed clean energy capacity beyond 1,878 GW. Its clean energy sector directly contributed more than 10% to its GDP growth in that year. Investment levels reached 13.6 trillion yuan, while innovation in battery, solar, and electric vehicle integrations anchored its technological leadership. Chinese consumer adoption of rooftop solar systems and distributed energy solutions also rose sharply, with residential solar deployment surpassing 8 GW.

Market Size & Growth: Valued at USD 867,424.2 Million in 2024, projected to reach USD 1,914,185.9 Million by 2032 at 10.4% CAGR, driven by global decarbonization initiatives.

Top Growth Drivers: 48% adoption of renewables among utilities, 35% improvement in energy storage efficiency, 27% electrification rate increase in transport.

Short-Term Forecast: By 2028, grid-level storage capacity is expected to improve round-trip efficiency by 22%.

Emerging Technologies: Solid-state batteries, green hydrogen electrolysis, and AI-driven grid optimization.

Regional Leaders: Asia-Pacific projected at USD 820,000 Million by 2032, Europe around USD 540,000 Million, North America about USD 410,000 Million.

Consumer/End-User Trends: 59% of corporate buyers aspiring for 100% renewable procurement; residential solar installations growing above 25%.

Pilot or Case Example: In 2026, Germany deployed a smart microgrid pilot reducing peak load by 18% across a municipal area.

Competitive Landscape: A leading renewable infrastructure developer holds about 14% share, followed by 5–7 major technology and EPC firms.

Regulatory & ESG Impact: Carbon pricing, clean energy mandates, and green bonds encouraging uptake.

Investment & Funding Patterns: Over USD 700 Billion invested globally in clean energy projects in recent years; venture capital focusing on energy storage firms.

Innovation & Future Outlook: Integrated hybrid renewable + storage hubs and sector coupling (power-to-X) will define next-gen deployments.

Energy generation by wind, solar, hydro, and storage now underpins sectors such as transport, industry, and buildings, with solar and wind contributing over 60% of new capacity additions. Green hydrogen and long-duration storage are emerging into commercial scale. Policy incentives, cost declines, and cross-sector hybridization are transforming regional consumption patterns and creating urgency for innovation in the clean energy arena.

The Clean Energy Market holds strategic significance as the backbone of the global energy transition, enabling carbon neutrality and stable energy supply. Comparative benchmarks indicate that modern solid-state battery systems deliver 18% higher energy density compared to conventional lithium-ion cells, enabling more efficient grid storage and EV range. Asia-Pacific dominates in volume capacity additions, while Europe leads adoption in corporate procurement, with 72% of large enterprises reporting renewable energy commitments.

By 2027, AI-based grid orchestration is expected to reduce curtailment losses by 24%, enabling more renewable integration without grid stress. Firms are committing to ESG metrics such as 30% reduction in scope-2 emissions by 2030. In 2025, a Scandinavian utility achieved a 21% reduction in balancing costs via predictive load forecasting powered by AI and hybrid storage systems. Such micro-scenarios illustrate how clean energy solutions deliver measurable operational gains.

Strategically, the Clean Energy Market is evolving as a resilient infrastructure layer that links power, mobility, industry, and storage. Positioned at the intersection of policy, technology, and capital, the market is becoming a foundational pillar for sustainable growth, climate compliance, and energy security across nations.

The Clean Energy Market is shaped by dynamic forces including rapid cost declines in renewables and storage, evolving regulatory architectures, and shifting demand patterns across sectors. As solar and wind equipment costs fall, grid operators increasingly adopt energy storage and demand flexibility platforms. Industrial sectors are electrifying operations, while transportation is migrating toward electric mobility. Across regions, the pace of adoption varies—Asia-Pacific leads in installations, Europe advances corporate procurement, and North America invests heavily in offshore wind. At the same time, competition for critical minerals, supply-chain constraints, and policy volatility inject uncertainty. Overall dynamics balance aggressive growth, technology convergence, and strategic risk management.

Policy and regulatory mandates are foundational drivers for the Clean Energy Market. Many countries have set net-zero targets, compelling utilities and governments to phase out fossils. Incentives such as feed-in tariffs, tax credits, renewable portfolio standards, and carbon pricing have stimulated investment; for instance, over 90 nations currently operate some form of carbon pricing. Governments also underwrite large-scale grid upgrades and storage subsidies, encouraging faster deployment. These mandates create predictable demand and de-risk capital for large-scale clean energy projects. Institutional investors now require ESG alignment, making clean energy projects more attractive. As a result, policy-driven decarbonization is a keystone accelerator of market growth.

Supply chain constraints remain a significant restraint on the Clean Energy Market. The reliance on critical minerals such as lithium, cobalt, nickel, and rare earth elements creates bottlenecks. In 2024, price volatility in lithium compounds increased by 32%, squeezing margins. Manufacturing capacity for solar panels and battery cells has struggled to scale at the same pace as demand, leading to lead times of 12–18 months for key components. Transportation and logistic disruptions further exacerbate delays. Coupled with tariffs and geopolitical trade tensions, these constraints slow project rollouts and raise costs, impeding faster adoption of clean energy systems.

Long-duration energy storage presents a transformative opportunity in the Clean Energy Market. As renewable penetration increases, grid operators need storage solutions that go beyond short-term batteries. Technologies such as flow batteries, compressed air energy storage, and hydrogen-based storage can deliver 10–100 hours of discharge, enabling baseload renewable supply. Some utilities are piloting storage projects that maintain grid reliability during multi-day intermittency periods. Industrial consumers also seek behind-the-meter storage to hedge against volatility. This opportunity opens a new frontier for investment, innovation, and long-term integration of renewables into firm energy systems.

Financing and capital cost volatility pose critical challenges for the Clean Energy Market. Large-scale clean energy and storage projects require upfront capital, often spanning 20–30 years. Rising interest rates raise the cost of capital and compress return margins. For example, in 2023–24, project financing rates increased by 150 bps across many markets, diminishing bankability. Currency risk in emerging markets also adds complexity. Developers must manage regulatory uncertainty, off-take contract risk, and commodity price volatility, making financing structuring more complex. These financial headwinds introduce execution risk and slow deployment in many regions.

• Surge in Renewable Capacity Additions: In 2024, global renewable energy capacity growth reached 15.1%, with Asia accounting for over 66% of the increase, largely driven by solar expansions.

• Rise of Hybrid Renewable + Storage Hubs: More than 28% of new clean energy projects announced in 2024 were hybrid systems combining solar or wind with battery storage to deliver dispatchable power.

• Corporate Renewable Procurement Accelerates: Over 59% of global corporations have adopted clean energy procurement goals, with virtual power purchase agreements (VPPAs) increasing by 23% year-over-year.

• Green Hydrogen & Sector Coupling Expansion: In 2024, announced clean hydrogen capacity doubled, and coupling strategies linking industry, power, and transport grew in pilot programs across multiple regions.

The Clean Energy Market is segmented by type (solar, wind, hydropower, bioenergy, energy storage, hydrogen), by application (power generation, transport electrification, industrial decarbonization, grid modernization), and by end-user (utilities, industrial users, commercial & residential, mobility). Solar and wind dominate new capacity additions; energy storage and hydrogen are rapidly emerging. Utilities account for majority demand, but industrial and commercial sectors are accelerating uptake. Residential segments contribute through rooftop solar and distributed storage. Each segment offers unique adoption patterns and investment dynamics tailored to regional and sectoral mandates.

Solar energy leads deployment, accounting for over 38% of total installed clean energy capacity additions, owing to falling module costs and favorable installation economics. Wind energy follows with approximately 27%, particularly strong in offshore and onshore installations. Energy storage (batteries, pumped hydro, flow batteries) is the fastest-growing type, with projected deployment growth rates exceeding 20% in many markets due to grid stability needs. Hydropower, bioenergy, and hydrogen technologies together contribute around 20% of capacity but are critical in specific geo-regions and seasonal balancing. The combined share of these remaining types is roughly 12%.

According to a 2024 international energy report, over 585 GW of new renewable capacity was added globally, of which solar made up more than 75% of the increase.

Power generation is the leading application, encompassing over 50% of clean energy deployment, as utilities replace conventional plants with renewables and storage. Transport electrification follows with around 22%, driven by EV adoption and charging infrastructure. Industrial decarbonization (process heat, electrified manufacturing) represents about 15%. Grid modernization and demand response systems make up the remaining 13%. Transport electrification is the fastest-growing application, supported by policies and consumer push, with projections showing it may exceed 25% share in some markets. In 2024, more than 38% of industrial players globally initiated clean energy systems for internal power use, while over 45% of consumers preferred EVs tied to renewable tariffs.

According to a 2024 IEA report, renewable power and grid investments surpassed fossil fuel investments for the first time in history.

Utilities remain the leading end-user, accounting for roughly 45% share, responsible for integrating large-scale solar, wind, and storage into grids. Industrial users follow with about 28%, as manufacturers adopt clean power to reduce carbon footprints. Commercial and residential segments collectively hold 18%, particularly in rooftop solar and behind-the-meter storage. Mobility and transport users account for the remaining 9%, leveraging clean energy through EV charging networks. The fastest-growing end-user is the industrial sector, driven by corporate mandates, with growth rates exceeding 18%. In 2024, over 42% of corporations globally initiated renewable procurement for manufacturing operations, and more than 60% of Gen Z–led startups prefer integrating clean energy solutions from inception.

According to a 2025 industry forecast, clean energy adoption by SMEs grew by 22%, enabling more than 500 mid-size companies to decarbonize operations across manufacturing and logistics.

North America accounted for the largest market share at 36% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2025 and 2032.

North America’s dominance stems from a mature renewable energy infrastructure, with the United States alone contributing more than 28% of the global clean energy demand. Europe followed closely, holding nearly 30% of the market share in 2024, with Germany, France, and the UK being primary contributors to offshore wind and solar PV adoption. Asia-Pacific, although holding around 24% in 2024, is projected to witness the highest acceleration in adoption due to rapid urbanization, large-scale government initiatives in China and India, and rising energy needs of over 1.5 billion households. South America represented 6% in 2024, led by Brazil’s investments in hydropower. Meanwhile, the Middle East & Africa accounted for 4%, driven by UAE and South Africa’s solar projects. The regional disparities highlight the role of infrastructure readiness, regulatory frameworks, and economic drivers in shaping clean energy adoption.

What Factors Are Driving Strong Demand For Clean Energy Solutions In This Market?

North America held a commanding 36% share of the global clean energy market in 2024, fueled by strong adoption across power generation, manufacturing, and transportation sectors. The U.S. government’s Inflation Reduction Act of 2022 significantly accelerated renewable energy projects by providing tax credits for solar and wind installations. Technological advancements such as AI-powered grid management and digital twins are being deployed for efficiency. Local players like NextEra Energy are expanding solar and wind projects, with a portfolio exceeding 45 GW of installed capacity. Consumer behavior shows higher adoption of clean energy in enterprise-driven industries such as healthcare and finance, where sustainability commitments are deeply integrated into operational models.

How Is Regulatory Pressure Shaping The Future Of Clean Energy Adoption In This Market?

Europe accounted for 30% of the clean energy market in 2024, with Germany, the UK, and France being the most prominent contributors. Regulatory bodies such as the European Commission enforce strict carbon neutrality targets under the “Fit for 55” package, driving investment into wind, solar, and hydrogen energy. Technological adoption is strong, with offshore wind capacity surpassing 32 GW across EU nations. Companies like Ørsted are heavily investing in offshore wind expansion and sustainability initiatives. Consumer adoption reflects growing demand for traceable and explainable clean energy, particularly in manufacturing and heavy industries, where compliance with ESG standards has become mandatory.

Why Is This Market Emerging As The Fastest Growing Hub For Clean Energy Deployment?

Asia-Pacific represented 24% of the global clean energy market in 2024, ranking second in overall volume. China, India, and Japan lead adoption, collectively accounting for more than 70% of the region’s renewable capacity. Manufacturing trends show a rapid rise in solar PV production, with China controlling over 80% of global photovoltaic supply chains. India has been scaling up wind and solar parks, targeting 450 GW by 2030. Regional innovation hubs like Shenzhen and Bengaluru are advancing battery storage technologies. Local players such as Goldwind in China are expanding wind energy solutions globally. Consumer behavior highlights rapid uptake driven by e-commerce platforms and smart-city initiatives, enabling faster adoption of renewable-powered digital infrastructure.

What Role Do Local Policies And Infrastructure Investments Play In Expanding Clean Energy Adoption?

South America captured 6% of the global clean energy market in 2024, with Brazil and Argentina being the key contributors. Brazil dominates due to its extensive hydropower infrastructure, which supplies more than 60% of its electricity needs. Argentina has been increasingly investing in wind projects across Patagonia. Government incentives, including subsidies for renewable energy installations, are further supporting growth. Local firms are expanding bioenergy and hydropower capabilities. Consumer behavior is tied to localized needs, with strong demand in urban regions for affordable, decentralized energy systems. Demand in this market is also influenced by media campaigns and localization of renewable energy education programs, particularly in Brazil.

What Key Drivers Are Accelerating The Adoption Of Clean Energy In This Market?

The Middle East & Africa held 4% of the clean energy market share in 2024, with UAE and South Africa emerging as primary growth engines. Regional demand is supported by diversification policies in oil-exporting nations, shifting focus toward solar and wind power. Technological modernization trends include large-scale solar projects such as the Mohammed bin Rashid Al Maktoum Solar Park in Dubai. Local companies and joint ventures are expanding hybrid energy systems combining solar and storage. South Africa, facing grid instability, is rapidly deploying renewable microgrids. Consumer behavior varies, with adoption higher in industries such as construction and oil & gas where energy efficiency measures are gaining importance.

United States – 28% market share

Strong demand is driven by large-scale investment in wind and solar projects supported by favorable government policies and private sector commitments.

China – 22% market share

Dominance comes from its global leadership in solar panel manufacturing and rapid domestic deployment of renewable power infrastructure.

The global clean energy market is highly competitive, with over 500 active companies participating across solar, wind, hydro, bioenergy, and emerging hydrogen segments. The top five companies collectively hold around 32% of the global market share, indicating a moderately consolidated structure with regional fragmentation. Leading players such as NextEra Energy, Iberdrola, Ørsted, Enel, and Vestas are shaping the industry through large-scale investments and long-term strategic commitments. Market competition is characterized by continuous innovation in solar PV modules, offshore wind turbines exceeding 14 MW capacity, and breakthroughs in green hydrogen electrolyzers. Strategic initiatives such as mergers, joint ventures, and cross-border partnerships are prominent; for example, major utilities are collaborating with technology providers to integrate AI-based energy management systems and advanced storage solutions. Many firms are strengthening their positioning by scaling battery storage capacity, which is projected to surpass 400 GWh globally by 2030. The market is witnessing strong momentum in sustainability-linked financing, where competitors compete not only on installed capacity but also on ESG performance metrics. Companies are also investing in digital twin technology and predictive maintenance systems, giving them a competitive edge in operational efficiency and lifecycle cost reduction.

Iberdrola, S.A.

Vestas Wind Systems A/S

Siemens Gamesa Renewable Energy

Enel Green Power S.p.A.

Brookfield Renewable Partners L.P.

First Solar, Inc.

Canadian Solar Inc.

Technological advancements are transforming the clean energy market, with solar, wind, storage, and hydrogen technologies taking center stage. Solar PV has achieved significant efficiency gains, with commercially available modules surpassing 23% efficiency, while bifacial panels and perovskite-silicon tandem cells are driving further cost reductions and scalability. Wind technology is also advancing rapidly, with offshore turbines now exceeding 14 MW capacity, enabling fewer installations to generate higher output. Floating wind farms are emerging as a critical solution for regions with limited shallow waters.

Energy storage technologies, particularly lithium-ion and sodium-ion batteries, are gaining prominence, with global storage capacity expected to cross 400 GWh by 2030. Grid-scale batteries and hybrid renewable-storage systems are being deployed to address intermittency challenges. Hydrogen technology is also a major frontier, with electrolysis efficiency improving to over 80%, supporting green hydrogen production for industrial and transportation applications.

Digital technologies such as AI, IoT, and blockchain are increasingly integrated into clean energy operations. AI-based predictive analytics is optimizing wind turbine performance, while blockchain is being used for peer-to-peer renewable energy trading. Smart grid innovations and digital twins are enabling more resilient and flexible networks. Collectively, these emerging technologies are reshaping market competitiveness and enabling broader adoption of sustainable energy solutions.

In May 2024, Siemens Gamesa announced the installation of its new 14 MW offshore wind turbine in Denmark, setting a benchmark for Europe’s offshore capacity expansion and paving the way for large-scale coastal wind integration. Source: www.siemensgamesa.com

In March 2024, Enel Green Power launched a 3 GW hybrid solar and battery storage project in Italy, marking one of the largest integrated renewable facilities in Europe designed to stabilize grid reliability. Source: www.enelgreenpower.com

In December 2023, China commissioned the world’s largest solar plant with over 3.5 GW capacity in Xinjiang province, significantly boosting Asia-Pacific’s renewable output and supporting local industrial demand. Source: www.chinadaily.com

In July 2023, the U.S. Department of Energy announced $1.2 billion funding for hydrogen hubs, accelerating the commercialization of green hydrogen technologies across multiple states. Source: www.energy.gov

The scope of the Clean Energy Market Report encompasses a comprehensive analysis of renewable energy sources, technologies, and end-user industries across global markets. The report covers solar, wind, hydro, geothermal, bioenergy, and hydrogen as key segments, analyzing their adoption patterns and deployment strategies. It also highlights hybrid systems, including solar-plus-storage and wind-hydrogen integration, which are reshaping the energy landscape.

Geographically, the report examines regional adoption across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into market share distribution and policy frameworks. For instance, while North America leads in large-scale wind and solar installations, Asia-Pacific is the fastest-growing region due to manufacturing dominance and expanding energy demand.

The scope also includes applications across industrial, commercial, and residential sectors, with special attention to transportation electrification, smart cities, and decentralized energy systems. Technological advancements in solar PV, offshore wind, battery storage, and hydrogen are analyzed in detail, with supporting data on efficiency improvements and deployment capacity. Additionally, the report explores industry focus areas such as ESG compliance, carbon neutrality commitments, and sustainability-linked financing. By covering both mainstream and emerging clean energy solutions, the report provides decision-makers with a holistic view of the global market’s opportunities, challenges, and long-term outlook.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 867,424.2 Million |

|

Market Revenue in 2032 |

USD 1,914,185.9 Million |

|

CAGR (2025 - 2032) |

10.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NextEra Energy, Inc., Iberdrola, S.A., Vestas Wind Systems A/S, Ørsted A/S, Siemens Gamesa Renewable Energy, Enel Green Power S.p.A., Brookfield Renewable Partners L.P., General Electric Renewable Energy, First Solar, Inc., Canadian Solar Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |