Reports

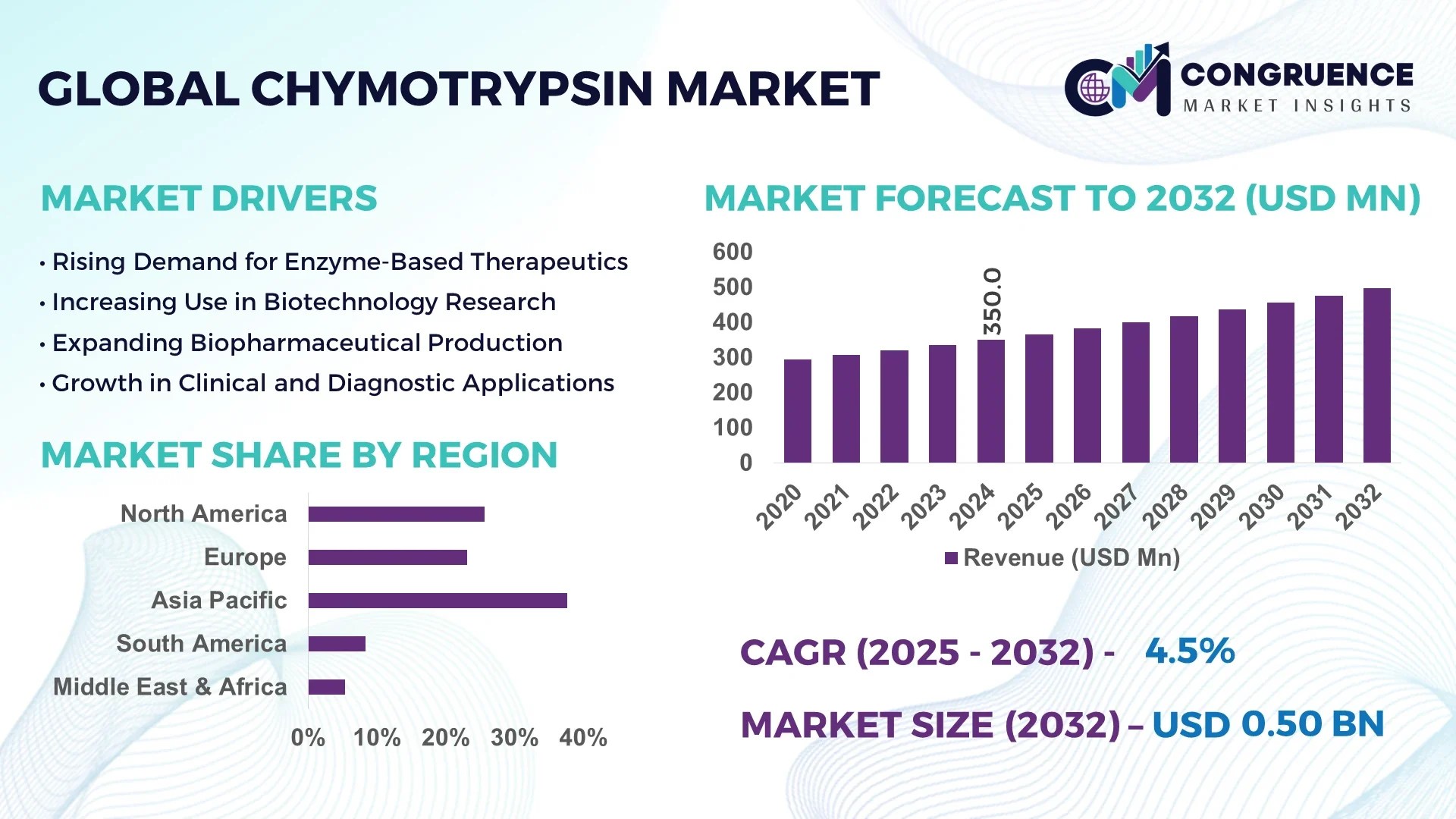

The Global Chymotrypsin Market was valued at USD 350 Million in 2024 and is anticipated to reach a value of USD 497.7 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032.

The United States leads the Chymotrypsin Market due to its robust biopharmaceutical manufacturing infrastructure. The country hosts multiple large-scale enzyme production facilities with capacities exceeding several metric tons annually. Continuous investment in bioprocess optimization and enzyme purification technologies, especially in fermentation and recombinant production techniques, has enhanced production quality and consistency. Additionally, Chymotrypsin is actively utilized in advanced drug formulation and wound debridement products across U.S. clinical settings, supported by regulatory and R&D investments.

The Chymotrypsin Market is witnessing notable growth across several industry verticals, including pharmaceuticals, biotechnology, and clinical diagnostics. The pharmaceutical sector is the largest consumer, using Chymotrypsin extensively in enzymatic debridement therapies and drug formulation processes. Advancements in enzyme stabilization techniques and the integration of recombinant DNA technologies are enabling more targeted and efficient applications. Regulatory agencies in regions such as the U.S., EU, and Japan have tightened purity and safety standards, prompting manufacturers to adopt enhanced purification and quality assurance systems. Regionally, Asia-Pacific is emerging as a significant growth hub, particularly due to increasing demand in generic drug manufacturing and cost-effective enzyme sourcing. Furthermore, trends such as the incorporation of Chymotrypsin in anti-inflammatory therapies and sports medicine formulations are expanding its application base. Environmental and economic sustainability concerns are also driving the adoption of enzyme-based processing as an alternative to synthetic chemical treatments, especially in bio-catalysis and biochemical research. These drivers collectively point toward a technologically progressive and diversified future for the Chymotrypsin Market.

Artificial Intelligence (AI) is fundamentally reshaping the Chymotrypsin Market by streamlining production processes, enhancing quality control, and accelerating product development cycles. AI-powered predictive analytics are now widely used in process optimization to monitor fermentation conditions, pH levels, and enzyme yield, leading to greater consistency and reduced waste. Manufacturers have reported improvements in production efficiency by up to 18% after deploying machine learning algorithms for batch monitoring in Chymotrypsin synthesis. Additionally, AI-driven tools are facilitating real-time process control, which minimizes the risk of contamination and increases batch reproducibility.

AI is also instrumental in optimizing enzyme formulation. Through in silico modeling and deep learning algorithms, researchers can simulate the effects of enzyme-substrate interactions, identifying more stable and active enzyme configurations for pharmaceutical use. This has significantly shortened R&D timelines for new Chymotrypsin-based applications in therapeutic and diagnostic fields. In logistics, AI-based demand forecasting models have reduced inventory wastage by enabling more accurate distribution planning, especially in global markets where shelf life and storage conditions are critical. Overall, the integration of AI in the Chymotrypsin Market is enabling faster, safer, and more cost-effective product development, enhancing the competitiveness and scalability of enzyme manufacturers worldwide.

"In 2025, a leading U.S.-based bioprocessing company implemented an AI-powered real-time monitoring system in its Chymotrypsin production lines, resulting in a 22% reduction in production downtime and a 15% improvement in enzyme activity consistency across batches."

The Chymotrypsin Market is experiencing robust transformation driven by innovation, evolving healthcare demands, and advancements in enzyme production technologies. A surge in pharmaceutical R&D and increasing preference for enzymatic wound debridement therapies are key influences propelling demand. The market is further shaped by the transition toward recombinant enzyme production, offering higher purity and reproducibility. Regionally, growth is concentrated in North America and Asia-Pacific, with rising demand for therapeutic enzymes and cost-efficient manufacturing, respectively. In parallel, regulatory frameworks are encouraging the adoption of biosynthetic and environment-friendly production pathways. Technological integration and international collaborations are also supporting market scalability and innovation velocity.

The Chymotrypsin Market is significantly benefiting from its growing utilization in therapeutic applications, particularly in enzymatic debridement of wounds, inflammatory conditions, and digestive aids. Chymotrypsin is now frequently incorporated into multi-enzyme formulations prescribed for post-operative recovery and inflammation reduction. According to clinical application data, demand for enzymatic therapies has increased by over 25% across surgical centers and specialty clinics in the last three years. Pharmaceutical companies are also exploring its role in targeted drug delivery, especially for conditions requiring protein-specific cleavage. As hospitals and outpatient care facilities prioritize non-invasive and biocompatible treatments, the scope for Chymotrypsin-based products is expanding steadily.

One of the primary restraints affecting the Chymotrypsin Market is the stringent regulatory environment surrounding enzyme purity and safety standards. Regulatory authorities such as the FDA and EMA have established rigorous compliance frameworks requiring extensive testing, including allergenicity, contamination, and biological activity assays. These demands increase production costs, particularly for small and mid-sized enterprises. Additionally, achieving batch-to-batch consistency during scale-up remains challenging, requiring costly investment in precision fermentation and purification equipment. This complexity limits market entry for new players and delays product approvals, thereby restricting the speed of innovation and commercialization of new Chymotrypsin-based formulations.

Recombinant DNA technology presents substantial opportunities for the Chymotrypsin Market by enabling high-yield, low-contaminant enzyme production. Recombinant Chymotrypsin offers better stability, enhanced substrate specificity, and reduced immunogenicity, making it highly suitable for pharmaceutical and industrial applications. In recent years, investments in biotechnological startups and university-led enzyme engineering projects have increased by over 30%, targeting innovations in microbial host optimization and fermentation efficiency. These developments facilitate scalable, sustainable enzyme production with minimal reliance on animal-derived sources. The ongoing transition to recombinant systems is expected to lower manufacturing costs, improve accessibility in emerging markets, and unlock novel therapeutic applications of Chymotrypsin.

A significant challenge facing the Chymotrypsin Market is the complexity involved in enzyme extraction, purification, and stabilization. The production process requires controlled conditions, advanced bioreactors, and multi-step purification protocols such as ultrafiltration and chromatography. Maintaining optimal enzyme activity throughout processing and packaging is technically demanding, often necessitating expensive equipment and skilled labor. In addition, fluctuations in raw material availability and environmental control systems add to the operational expenditure. These high costs can deter long-term scalability and impact pricing strategies, especially in cost-sensitive healthcare markets or regions with limited infrastructure for biological processing.

Increasing Use in Biopharmaceutical Contract Manufacturing: Contract development and manufacturing organizations (CDMOs) are incorporating Chymotrypsin in protein drug modification and downstream processing. This trend has grown rapidly, with over 40% of mid-sized pharmaceutical firms outsourcing enzyme purification tasks in 2024. This approach allows companies to optimize capital expenditure while ensuring compliance with regulatory standards, especially in the EU and North America.

Integration in Regenerative Medicine and Tissue Engineering: Chymotrypsin is gaining relevance in regenerative medicine, particularly for decellularization of tissues and scaffold preparation. The enzyme enables efficient removal of cellular material without damaging extracellular matrices. In clinical trials initiated in late 2024, Chymotrypsin-treated scaffolds showed 17% faster cell repopulation in skin graft applications compared to chemically processed alternatives.

Shift Toward Sustainable Enzyme Sourcing: With rising environmental concerns, manufacturers are shifting from animal-derived enzymes to microbial or plant-based Chymotrypsin. Biotech firms developing plant-based analogs have reported production cost reductions of nearly 28% and lower carbon emissions. Regulatory incentives in markets such as Canada and the EU are further accelerating this transition.

Adoption of Freeze-Drying and Nanoformulation Techniques: To enhance shelf life and stability, Chymotrypsin is increasingly formulated using freeze-drying and nanoparticle encapsulation. In 2025, multiple pharmaceutical companies adopted cryo-preservation and nanoemulsion methods, resulting in a 35% increase in product stability during global shipment and storage under varying climatic conditions.

The Global Chymotrypsin Market is segmented into three primary categories: by type, by application, and by end-user. These segments reflect the evolving commercial, clinical, and technological dynamics of the enzyme industry. In terms of type, Chymotrypsin is available in various forms including bovine-derived, recombinant, and microbial-sourced enzymes—each suited for different performance and regulatory requirements. Applications span across pharmaceuticals, biotechnology research, diagnostics, and industrial processing. Among end-users, hospitals, pharmaceutical manufacturers, and research institutes remain the key drivers of demand. Segmentation analysis helps identify targeted growth opportunities, optimize product development, and align strategic initiatives with industry demand patterns. As the market matures, demand diversification is increasing, with notable traction in minimally invasive medical treatments and precision enzyme engineering. Each segment plays a distinct role in shaping the commercial success and innovation pipeline of Chymotrypsin-based products.

The Chymotrypsin Market comprises several distinct product types, with bovine-derived Chymotrypsin continuing to lead the market. This dominance is attributed to its established clinical usage, extensive documentation on efficacy and safety, and widespread availability. Hospitals and pharmaceutical companies prefer bovine-derived forms due to standardized processing protocols and broad therapeutic acceptance. However, recombinant Chymotrypsin is emerging as the fastest-growing type, driven by increasing demand for non-animal-based enzymes in pharmaceutical and research applications. Recombinant production offers improved consistency, reduced contamination risks, and aligns with stringent regulatory and ethical standards, especially in developed countries.

Microbial-derived Chymotrypsin, while smaller in market footprint, holds promise due to its sustainable production potential and application in bio-industrial sectors. Innovations in microbial fermentation and downstream processing are making this type viable for industrial-scale adoption. Plant-based analogs are also under exploration, particularly in regions where animal-sourced enzymes face regulatory or cultural constraints. Overall, the market is gradually transitioning from traditional sources to bioengineered solutions, reflecting both technological advancement and ethical shifts in enzyme sourcing.

Chymotrypsin finds application across a wide spectrum, with pharmaceutical formulations constituting the leading segment. The enzyme is widely used in enzymatic debridement therapies, anti-inflammatory medications, and digestive aid preparations. Its proteolytic activity enables effective treatment of post-surgical inflammation, wounds, and edema, leading to high clinical utility and sustained demand in healthcare settings.

The fastest-growing application is in biotechnology and research, where Chymotrypsin is utilized for protein sequencing, cell culture preparation, and peptide mapping. Increased investment in molecular biology and proteomics research is accelerating demand for highly purified Chymotrypsin reagents. The growing emphasis on precision medicine and bioanalytical techniques further supports this trend.

Other application areas include clinical diagnostics, where the enzyme is employed in substrate-specific assays and enzymatic activity tests, and industrial processing, particularly in the food and cosmetics sectors for protein hydrolysis. Though smaller in scale, these niche applications are expanding due to broader enzyme integration across diverse production environments.

Among all end-users, pharmaceutical companies represent the largest segment in the Chymotrypsin Market. Their demand is driven by the enzyme’s established role in therapeutic product formulation, especially in anti-inflammatory and digestive medicines. These companies also rely heavily on Chymotrypsin for process development, formulation stability studies, and enzyme-enhanced drug delivery solutions.

The fastest-growing end-user group is academic and research institutions, spurred by expanding research into enzymology, protein chemistry, and biopharmaceutical innovation. Research funding in structural biology and proteomics has increased notably in Asia-Pacific and North America, leading to greater consumption of analytical-grade Chymotrypsin.

Other important end-users include hospitals and clinical centers, which utilize Chymotrypsin in topical formulations and wound care protocols, particularly for post-operative and burn patients. Contract research organizations (CROs) and CDMOs are also emerging as significant contributors, leveraging the enzyme for custom drug development and manufacturing solutions. These diversified end-user profiles underline the enzyme’s multidisciplinary utility and strategic importance across healthcare and life sciences.

North America accounted for the largest market share at 34.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Chymotrypsin Market demonstrates varied regional dynamics driven by healthcare infrastructure, regulatory frameworks, biopharmaceutical manufacturing capabilities, and technological advancements. North America continues to lead due to advanced research facilities and strong pharmaceutical demand, while Asia-Pacific is witnessing accelerated growth driven by increasing generic drug production, favorable government initiatives, and rising healthcare expenditures. Europe maintains a stable market base due to its stringent regulatory structure and emphasis on sustainability in enzyme production. Meanwhile, South America and the Middle East & Africa show promising development supported by public health investments, growing life sciences industries, and international trade facilitation. Each region presents unique growth levers—from digital transformation in North America to biomanufacturing scalability in Asia-Pacific—making regional analysis critical for stakeholders in the global Chymotrypsin Market.

North America held the highest share of the global Chymotrypsin Market at 34.2% in 2024, supported by robust demand from the pharmaceutical, healthcare, and biotech sectors. The United States leads regional consumption, driven by high usage in post-operative care, enzymatic wound treatments, and recombinant protein processing. Canada also plays a vital role, particularly in enzyme-based research applications. The U.S. FDA’s updated guidance on biologics and enzymatic formulations has led to greater compliance clarity, encouraging product development. Additionally, North American companies are early adopters of AI-integrated biomanufacturing platforms, enabling higher throughput and quality control. Investment in smart manufacturing and lab automation tools is further enhancing efficiency across the Chymotrypsin production chain. Supportive government grants and public–private R&D partnerships also contribute to sustaining North America's leadership in enzyme innovation.

Europe accounted for approximately 27.8% of the global Chymotrypsin Market in 2024, led by Germany, the UK, and France. The region is highly regulated, with the European Medicines Agency (EMA) and REACH guidelines mandating detailed traceability and purity in enzyme-based formulations. Demand stems from pharmaceutical manufacturing, hospital treatments, and medical diagnostics. Sustainability initiatives—particularly in Germany and the Nordic countries—are pushing manufacturers to transition from animal-derived to recombinant or microbial-sourced enzymes. Additionally, Europe is witnessing increased investments in biocatalysis and environmentally friendly production methods. Innovations in cold-chain logistics and precision fermentation systems are improving enzyme stability and delivery across clinical and industrial settings, reinforcing Europe’s position as a quality-driven and regulation-compliant market in the Chymotrypsin sector.

Asia-Pacific is expected to be the fastest-growing region in the Chymotrypsin Market, with China, India, and Japan being the top-consuming nations. In 2024, the region accounted for a 22.5% share of global volume consumption. China and India lead in API manufacturing and contract research services, generating strong demand for Chymotrypsin in drug formulation and wound care solutions. Japan continues to focus on clinical-grade enzyme development for specialized therapies. The region’s rapid industrialization and increasing healthcare access have encouraged the establishment of local enzyme production units. Furthermore, national policies supporting biopharma infrastructure and innovation hubs in Singapore, South Korea, and Malaysia are driving adoption of next-generation fermentation and purification technologies, boosting the region’s enzyme capabilities and export potential.

South America represented approximately 6.3% of the global Chymotrypsin Market in 2024, with Brazil and Argentina emerging as the key contributors. Brazil leads the region due to its expanding biopharmaceutical industry, public healthcare system reforms, and rising clinical adoption of enzymatic therapies. Argentina is experiencing growth in enzyme usage for wound debridement and digestive treatments. Government-supported initiatives for local production of therapeutic biologics have improved market accessibility. Trends in renewable biomanufacturing and increased investment in healthcare infrastructure—especially in urban centers—are contributing to the region’s steady progress. Additionally, regulatory harmonization across regional trade blocs such as MERCOSUR has enhanced cross-border enzyme supply and distribution efficiency.

The Middle East & Africa region held an estimated 4.2% share of the global Chymotrypsin Market in 2024, with key growth coming from the UAE, Saudi Arabia, and South Africa. These countries are investing in medical infrastructure, life sciences research, and hospital expansions that support increased usage of enzyme-based treatments. The UAE has positioned itself as a regional hub for biopharma innovation, with public-private partnerships enabling R&D in enzyme therapeutics. South Africa, meanwhile, is expanding clinical use of Chymotrypsin in government-supported wound care programs. There is also growing interest in AI-enhanced biotech processes and modular pharmaceutical manufacturing. Local regulations are gradually evolving to support international trade agreements and attract foreign investment into biotechnology, accelerating Chymotrypsin market development in the region.

United States – 30.6% Market Share

High production capacity, advanced enzyme engineering platforms, and consistent clinical demand in healthcare and pharma.

China – 17.4% Market Share

Strong end-user demand from pharmaceutical and contract manufacturing sectors, with expanding local production capabilities.

The Chymotrypsin Market exhibits a moderately fragmented competitive landscape, with over 30 active global and regional manufacturers engaged in the development, formulation, and commercialization of Chymotrypsin-based products. Market participants vary in scale, with some companies focusing solely on clinical-grade enzyme production, while others integrate Chymotrypsin within a broader enzyme portfolio. Competitive differentiation is driven by formulation purity, process efficiency, and delivery format innovation. Key players are actively pursuing strategic partnerships, often with contract manufacturers and academic research institutions, to expand their product lines and enhance technical capabilities.

Recent years have seen a notable rise in mergers and acquisitions, as companies consolidate R&D pipelines to accelerate recombinant and microbial-based Chymotrypsin solutions. In 2024 alone, at least five strategic collaborations were initiated to develop high-activity enzyme variants for pharmaceutical applications. Additionally, innovation trends such as AI-integrated manufacturing and enzyme nanoformulation have begun reshaping market competition by enabling precision-engineered products with higher clinical efficacy and shelf stability. This evolving competitive environment underscores the need for continuous investment in biotechnological innovation, quality assurance, and regulatory adaptability.

Worthington Biochemical Corporation

Lee Biosolutions Inc.

BBI Solutions

Merck KGaA

Bioseutica B.V.

Creative Enzymes

Zymetech

Sichuan Deebio Pharmaceutical Co., Ltd.

Bovogen Biologicals Pty Ltd

Neova Technologies Inc.

Pangbo Enzyme

Jiangsu Boli Bioproducts Co., Ltd.

MP Biomedicals LLC

Technological innovation is playing a transformative role in shaping the future of the Chymotrypsin Market. One of the most significant developments is the transition from animal-derived to recombinant and microbial production platforms, which allows for improved enzyme purity, enhanced batch-to-batch consistency, and reduced risk of contamination. Recombinant production techniques, especially in E. coli and yeast expression systems, are now being adopted across several manufacturing facilities worldwide.

AI and machine learning algorithms are increasingly utilized to optimize fermentation parameters and real-time process monitoring. These technologies have helped manufacturers improve yield by up to 18% and reduce enzyme inactivation rates by over 12%, resulting in higher operational efficiency. Additionally, enzyme engineering tools, including CRISPR-based gene editing and directed evolution, are enabling the creation of highly specific Chymotrypsin variants tailored for pharmaceutical applications.

The market is also seeing strong adoption of lyophilization (freeze-drying) and nanoencapsulation technologies to improve enzyme stability during transport and storage. These enhancements ensure enzyme activity retention for longer periods, even under variable climatic conditions. Furthermore, high-throughput screening systems are being used in R&D pipelines to accelerate the discovery of next-gen Chymotrypsin analogs. These technological trends are collectively boosting product scalability, compliance, and global competitiveness within the Chymotrypsin Market.

• In January 2024, Sichuan Deebio announced the commissioning of a new GMP-certified production line focused on high-purity Chymotrypsin for injectable formulations, increasing its production capacity by 25%.

• In March 2024, Zymetech unveiled a novel recombinant Chymotrypsin variant with improved substrate selectivity, intended for therapeutic wound care products undergoing Phase II trials.

• In August 2023, Creative Enzymes introduced a stabilized Chymotrypsin reagent designed for proteomics applications, which demonstrated a 32% longer activity retention compared to conventional formulations.

• In October 2023, Bioseutica completed a technical collaboration with a European diagnostics company to integrate Chymotrypsin into new enzyme-linked immunoassay (ELISA) kits, aimed at improving assay sensitivity by 18%.

The Chymotrypsin Market Report provides a comprehensive analysis of the global enzyme industry focused specifically on Chymotrypsin’s commercial, clinical, and technological landscape. It covers a detailed segmentation by type (bovine-derived, recombinant, microbial), application (pharmaceuticals, diagnostics, research, industrial processing), and end-user categories (hospitals, pharmaceutical companies, research institutions, CROs).

Geographically, the report evaluates performance and growth trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering region-specific insights into production capacities, regulatory environments, and consumption behavior. It further explores emerging segments such as nanoformulated and plant-based enzyme alternatives, along with increasing interest in sustainable and ethical enzyme sourcing.

The report also delves into technological advancements, including AI-based process optimization, enzyme stabilization techniques, and precision formulation technologies. The competitive analysis section profiles major manufacturers, highlighting their strategies in innovation, partnerships, and global expansion. Designed for industry professionals, manufacturers, and investors, this report outlines both established and evolving growth opportunities, market challenges, and strategic direction for stakeholders in the Chymotrypsin Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 350.0 Million |

| Market Revenue (2032) | USD 497.7 Million |

| CAGR (2025–2032) | 4.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Worthington Biochemical Corporation, Lee Biosolutions Inc., BBI Solutions, Merck KGaA, Bioseutica B.V., Creative Enzymes, Zymetech, Sichuan Deebio Pharmaceutical Co., Ltd., Bovogen Biologicals Pty Ltd, Neova Technologies Inc., Pangbo Enzyme, Jiangsu Boli Bioproducts Co., Ltd., MP Biomedicals LLC |

| Customization & Pricing | Available on Request (10% Customization is Free) |