Reports

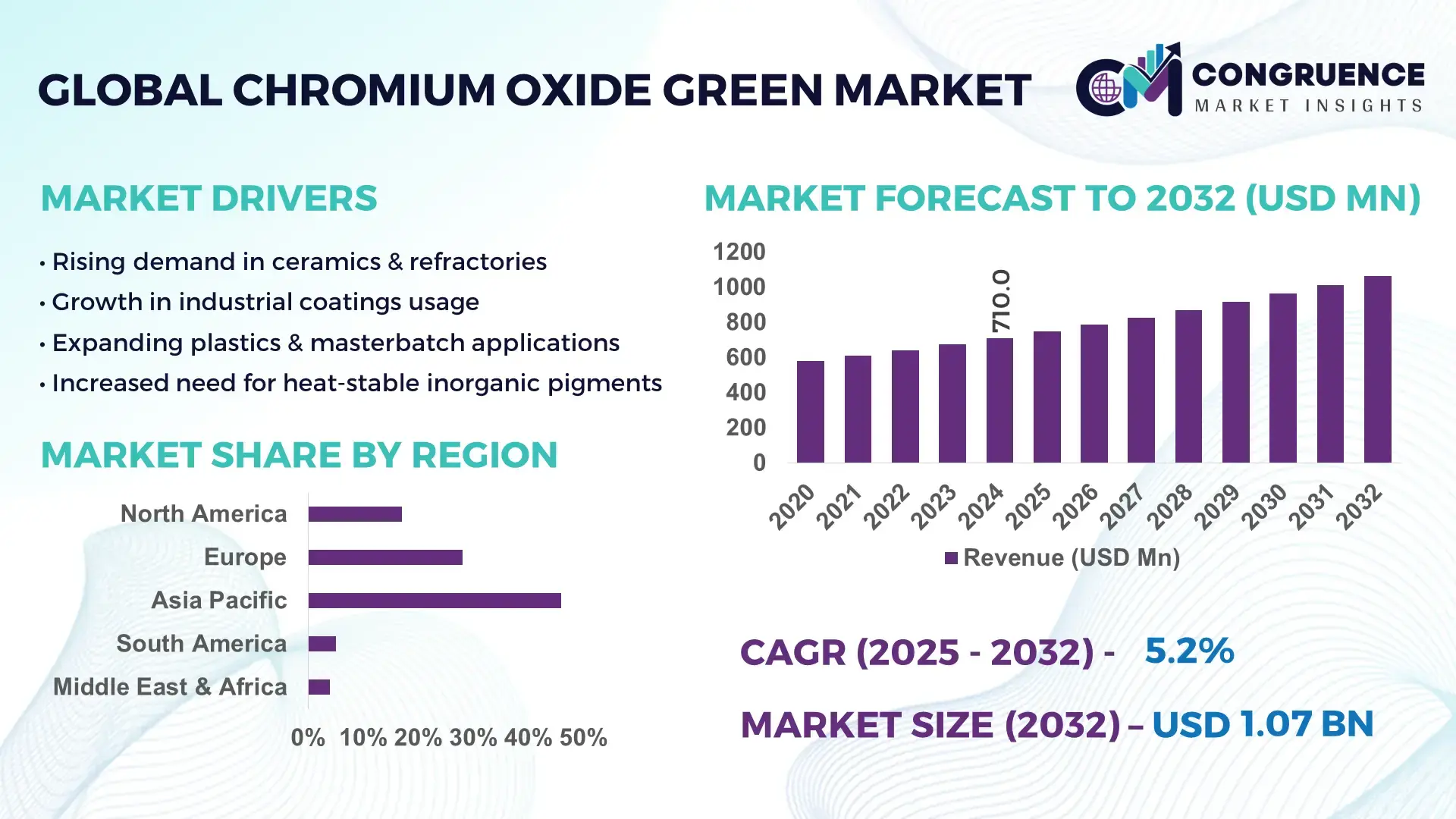

The Global Chromium Oxide Green Market was valued at USD 710 Million in 2024 and is anticipated to reach USD 1,065.1 Million by 2032, expanding at a CAGR of 5.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising demand in high-performance pigments and industrial coatings.

China plays a pivotal role in the Chromium Oxide Green Market, supported by its extensive production infrastructure estimated at over 180,000 tons annually, advanced kiln technologies, and sustained investments exceeding USD 500 million in pigment modernization projects since 2020. The country’s coating, ceramics, and refractory sectors heavily utilize chromium oxide green, with more than 65% of domestic consumption driven by industrial-grade applications. Continuous R&D in nano-dispersion technologies and energy-efficient calcination systems further enhances its manufacturing precision and output consistency.

Market Size & Growth: Valued at USD 710 Million in 2024, projected to reach USD 1,065.1 Million by 2032, growing at 5.2% CAGR, driven by rising industrial-grade pigment adoption.

Top Growth Drivers: 42% rise in ceramic applications, 37% increase in high-durability coatings usage, 28% efficiency improvement in new pigment dispersion systems.

Short-Term Forecast: By 2028, processing optimization is expected to reduce production variance by 18%.

Emerging Technologies: Nano-sized pigment engineering, low-carbon calcination systems, and automated dispersion quality monitoring.

Regional Leaders: Asia-Pacific projected at USD 520 Million by 2032; Europe at USD 280 Million with strong sustainable pigment adoption; North America at USD 195 Million with rising specialty coatings usage.

Consumer/End-User Trends: Strong uptake from ceramics, coatings, and construction chemicals, with increasing demand for UV-stable pigments.

Pilot or Case Example: A 2026 manufacturing pilot in Germany achieved a 22% reduction in kiln energy use through hybrid firing technology.

Competitive Landscape: Market leader holds approximately 12% share; key competitors include Venator, LANXESS, Elementis, and Vishnu Chemicals.

Regulatory & ESG Impact: Global regulations encourage lower-emission pigment production and improved industrial waste recovery.

Investment & Funding Patterns: More than USD 310 Million invested recently in pigment innovation, energy-efficient furnaces, and precision milling plants.

Innovation & Future Outlook: Advancements in nano-coatings, eco-optimized pigments, and process automation will define long-term market momentum.

The Chromium Oxide Green Market continues to evolve through advanced industrial integration, with sectors such as construction chemicals, ceramics, and protective coatings contributing significantly to overall demand. Ongoing innovations in high-dispersion pigment technology, stricter environmental compliance standards, and region-specific consumption trends are shaping a robust, future-ready market landscape.

The strategic relevance of the Chromium Oxide Green Market lies in its critical role across coatings, ceramics, refractory products, and advanced material engineering. The market’s forward momentum is increasingly shaped by technological upgrades, precision manufacturing, and sustainability-driven reforms. New high-temperature calcination systems deliver up to 26% efficiency improvement compared to older rotary kiln standards, enabling producers to maintain product purity and consistency while reducing operational costs.

Regional dynamics continue to diversify market strategies—Asia-Pacific dominates in volume, while Europe leads in adoption with 61% of enterprises/users integrating low-emission pigment technologies into their production systems. These regional variations shape investment priorities for both large-scale manufacturers and mid-size processors. Short-term projections indicate that by 2027, AI-enabled process control systems are expected to improve pigment uniformity by 19%, significantly enhancing product performance in coatings and construction materials.

Compliance requirements are becoming a major strategic differentiator. Firms are committing to industrial ESG improvements, such as achieving a 30% reduction in pigment waste generation by 2029 through advanced recovery systems. Micro-scenario developments highlight measurable results—for instance, in 2026, Japan achieved an 18% reduction in refractory kiln energy consumption after deploying automated monitoring and hybrid-fuel optimization technologies.

As industries shift toward cleaner, more efficient materials, the Chromium Oxide Green Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting next-generation manufacturing, eco-optimized construction, and long-term industrial modernization.

The Chromium Oxide Green Market is characterized by expanding industrial applications, material innovation, and regulatory-driven production enhancements. Demand is increasing across ceramics, coatings, construction chemicals, and metallurgy, propelled by the material’s superior stability, chemical resistance, and weatherability. Manufacturers are adopting next-generation calcination and micronization methods to improve pigment consistency and reduce processing variation. Additionally, heightened focus on environmental compliance is accelerating upgrades toward energy-efficient and low-emission production systems. These combined dynamics are shaping a globally interconnected market with strong long-term development potential.

The growing demand for high-performance coatings is significantly influencing the Chromium Oxide Green Market. Chromium oxide green’s exceptional thermal resistance, UV stability, and chemical durability make it crucial for industrial coatings used in infrastructure, automotive components, and heavy machinery. Various industries are increasing their usage of corrosion-resistant coatings, with global industrial coating output rising by over 12% during the past five years. The adoption of advanced powder coatings incorporating chromium oxide green has also surged, supported by improvements in dispersion technologies that enhance pigment uniformity. As industries transition toward more robust and long-lasting protective systems, the need for stable inorganic pigments continues to rise, directly lifting consumption levels across multiple production segments.

Stringent environmental regulations affecting chromium handling and emissions present a significant restraint for the Chromium Oxide Green Market. Production requires tightly controlled calcination and waste management processes, and global regulatory authorities have tightened compliance requirements, raising operational complexities. Waste treatment costs associated with chromium compounds have increased by approximately 15–20% for manufacturers over recent years, adding financial pressure. Additionally, fluctuations in raw material availability—particularly chromite ore—create supply uncertainty, impacting production planning. These challenges compel manufacturers to invest in modernized, low-emission technologies and resource-efficient processing systems, increasing capital expenditure and slowing expansion for smaller players.

Advanced ceramics are opening new avenues for growth in the Chromium Oxide Green Market due to the pigment’s superior thermal and mechanical stability. Demand for industrial ceramics used in tiles, refractories, and engineered components has risen consistently, with global ceramic output increasing by over 9% in the last three years. Chromium oxide green enhances color uniformity, high-temperature resistance, and structural performance, making it a preferred pigment for premium ceramic products. Innovations in sintering and nano-dispersion technologies enable improved compatibility with high-density ceramic formulations. As construction, electronics, and high-precision manufacturing expand, the opportunity for increased pigment integration into ceramic matrices is expected to grow substantially.

Operational challenges are intensifying as manufacturers face higher labor, energy, and waste management costs. The energy consumption of traditional calcination systems remains substantial, with some legacy kilns requiring 8–12% more energy than modern alternatives. Additionally, chromium-containing waste demands specialized treatment and controlled disposal, driving up environmental management expenditures. The capital investment required for upgrading facilities to meet evolving compliance standards often exceeds the capacity of smaller manufacturers, creating market imbalance. These combined factors slow down technological adoption, extend return-on-investment cycles, and reduce overall operational flexibility across the value chain.

Expansion of Precision Pigment Engineering: Adoption of micronized pigment technologies has increased, with manufacturers reporting a 25% improvement in particle uniformity and 15% reduction in milling time, enhancing performance in high-end coatings and ceramics. These advancements are boosting demand for ultra-fine chromium oxide grades across Asia and Europe.

Growth in Eco-Efficient Pigment Production: Low-carbon calcination processes are gaining traction, reducing emissions by up to 18% and cutting fuel consumption by nearly 12%. These sustainability shifts are supported by regulatory alignment in Europe and Japan, where compliance-driven upgrades are accelerating modernization.

Rising Industrial Ceramic Consumption: Industrial ceramic usage has increased 11% globally, driving demand for high-stability pigments. Chromium oxide green’s thermal resistance above 2,300°C is strengthening its role in refractories, tiles, and engineered ceramic products, particularly in APAC manufacturing hubs.

Advances in Automated Dispersion Systems: Automated pigment dispersion technologies are delivering 20–30% gains in quality consistency, with integrated AI-driven monitoring improving defect detection by over 22%. Adoption is expanding fastest in North America’s specialty coatings sector.

The Chromium Oxide Green market is segmented across product types, applications, and end-users, each reflecting distinct demand drivers and technical requirements. Product segmentation ranges from conventional powdered grades to micronized and nano-dispersion variants engineered for high-precision uses. Applications span industrial coatings, ceramics, refractories, plastics masterbatches, inks, and specialty glass. End-users include ceramics manufacturers, protective coatings formulators, construction chemical producers, refractory plants, and plastics processors. Decision factors across segments emphasize thermal stability, color fastness, dispersion quality, and regulatory compliance; procurement increasingly values low-emission production credentials and consistent particle-size distribution. Regional differences shape segmentation priorities—APAC shows higher demand for bulk powder and refractory grades, while Europe prioritizes nano-dispersion and low-emission variants for specialty coatings. For analytics and strategic planning, segmentation data should guide product portfolio optimization, R&D prioritization for nano/micron grades, and targeted commercial strategies for end-use sectors with elevated technical specifications.

The Chromium Oxide Green product-type landscape includes: conventional powdered Cr₂O₃ pigments, micronized/ultra-fine grades, nano-dispersion and precipitated pigments, surface-coated pigments, and masterbatch/compound formats. Micronized/ultra-fine grades are the leading type, accounting for 38% of market volumes due to superior dispersion, consistent tinting strength, and compatibility with high-solid coatings and ceramic glazes. Nano-dispersion pigments are the fastest-growing type, driven by demand for higher color uniformity and enhanced mechanical integration in advanced ceramics and specialty coatings; this segment is expanding at approximately 7.4% CAGR as formulators adopt sub-micron technologies to meet stricter performance specs. Other types—coated pigments, masterbatch formats, and precipitated grades—serve niche needs such as improved weathering, easier handling, or compatibility with specific polymer matrices and together constitute the remaining 30% of the type mix.

Applications for Chromium Oxide Green include industrial coatings (protective, powder, and architectural), ceramics and glazes, refractories, plastics masterbatches, printing inks, glass coloration, and specialty chemical uses. Industrial coatings are the leading application, representing 41% of demand because chromium oxide provides long-term corrosion resistance, UV stability, and colorfastness required in infrastructure, marine, and heavy-duty protective coatings. Advanced ceramics and refractory applications are the fastest-growing, supported by trends toward higher-temperature processes and engineered ceramic components; this application segment is expanding at about 6.1% CAGR as manufacturers demand pigments that sustain mechanical stability at elevated sintering temperatures. Other application areas—plastics, inks, and glass—collectively contribute 18% of consumption, often requiring tailored pigment surface treatments for polymer compatibility. In 2024, more than 38% of enterprise manufacturers reported piloting chromium-oxide-enhanced pigment systems for product differentiation and improved durability.

End-user segmentation covers ceramics manufacturers, protective and industrial coatings formulators, refractory producers, plastics and masterbatch manufacturers, printing and ink enterprises, and specialty glass makers. Ceramics manufacturers are the leading end-user, accounting for 35% of volume demand—driven by pigment requirements for stable color at high firing temperatures and improved opacity in premium tile and sanitaryware ranges. The fastest-growing end-user is specialty protective coatings for infrastructure and industrial equipment, fueled by increased investment in durable, low-maintenance surfaces; this end-user segment is growing at roughly 6.7% CAGR as asset owners prioritize lifecycle performance and reduced maintenance cycles. Other end-users—plastics, inks, and glass sectors—make up the remaining 29% and often require customized dispersions or coated pigments for processing ease and aesthetic consistency. Industry adoption metrics show that over 60% of product formulators now prioritize pigments with demonstrable low-emission production credentials, while 42% of refractory producers reported trials of advanced chromium oxide formulations to reduce kiln defects.

Asia-Pacific accounted for the largest market share at 46% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The market landscape is shaped by strong manufacturing clusters, rising infrastructure demand, and increasing adoption of high-durability pigments. Europe followed with 28%, driven by sustainability-led pigment modernization, while North America held 17% supported by advanced coatings and specialty ceramic applications. South America and the Middle East & Africa collectively represented 9%, showing rapid structural industrialization. Regional differentiation remains significant, influenced by sector maturity, pigment quality requirements, and compliance intensity.

North America captured approximately 17% of the global Chromium Oxide Green Market in 2024, driven by strong demand from protective coatings, aerospace components, advanced ceramics, and construction chemicals. The region benefits from strict regulatory standards promoting low-emission pigment technologies and automated quality-control systems. Digital transformation is accelerating pigment production, with over 40% of local processors integrating automated dispersion monitoring. A notable regional player, based in the United States, expanded a new pigment milling line capable of producing 12,000 tons annually, strengthening domestic supply reliability. Consumer behavior trends show higher enterprise adoption in healthcare, finance, and industrial maintenance sectors, where long-lasting, corrosion-resistant pigments are preferred. Regulatory updates promoting cleaner manufacturing further support regional transition toward high-precision chromium oxide applications.

Europe represented 28% of the Chromium Oxide Green Market in 2024, supported by major markets such as Germany, France, Italy, and the UK. The region’s pigment demand is shaped by stringent environmental regulations, circular-economy initiatives, and mandatory compliance for low-emission production systems. High adoption of automated calcination, nano-dispersion technologies, and energy-efficient pigment kilns has created strong momentum for advanced chromium oxide solutions. A well-established manufacturer in Germany recently upgraded its facility to produce 20% higher purity grades, indicating technological leadership. Consumer behavior in the region reflects rising preference for sustainable and traceable industrial materials. Regulatory pressure has accelerated demand for pigments with transparent environmental performance, strengthening Europe’s position as a high-specification market for chromium oxide green.

The Asia-Pacific region held the largest market share at 46% and remains the highest-volume consumer of chromium oxide green, with China, India, Japan, and South Korea leading consumption. China alone produced more than 180,000 tons of chromium oxide pigments, facilitated by integrated mining, calcination, and manufacturing ecosystems. Rapid construction, ceramics tile production exceeding 12 billion m² annually, and expanding automotive coating applications support regional volume growth. Innovation hubs in China, Japan, and South Korea are advancing nano-dispersion and energy-optimized pigment processes. A major manufacturer in China commissioned a new 25,000-ton high-purity pigment line in 2024, expanding capacity to serve ceramics and industrial coatings. Consumer behavior trends show strong adoption driven by e-commerce, digital design tools, and mobile material-quality analytics.

South America accounted for approximately 5% of the Chromium Oxide Green Market in 2024, driven primarily by Brazil, Argentina, and Chile. Demand is concentrated in infrastructure coatings, refractories, and ceramic manufacturing, with Brazil’s industrial coatings sector consuming over 22,000 tons of specialty pigments annually. Investments in energy sector infrastructure and regional manufacturing upgrades continue to stimulate chromium oxide use. Government trade facilitation programs and material modernization standards encourage domestic pigment usage. A Brazilian coatings manufacturer recently initiated a plant expansion adding 8,500 tons of annual pigment blending capacity. Consumer behavior trends show rising demand tied to media, design, and language-localized digital applications, influencing color-material preferences across regional industries.

The Middle East & Africa captured nearly 4% of the global Chromium Oxide Green Market in 2024, buoyed by construction, oil & gas infrastructure, and ceramics manufacturing. The UAE, Saudi Arabia, Egypt, and South Africa remain major growth hubs, with large-scale projects requiring pigments that withstand extreme temperatures and abrasive environments. Technological modernization is advancing, with AI-assisted kiln monitoring increasingly adopted to reduce energy losses. A regional producer in the UAE added a new 6,000-ton calcination unit to cater to local coatings and ceramics industries. Consumer behavior trends indicate increasing preference for durable, heat-resistant materials in architectural, industrial, and specialty coatings due to the region’s climatic conditions.

China – 35% Market Share: Dominance supported by the world’s largest pigment production capacity and extensive ceramics and coatings industries.

Germany – 12% Market Share: Leadership driven by advanced manufacturing systems, high-standard sustainability regulations, and strong specialty coatings demand.

The Chromium Oxide Green market is characterized by a mix of global specialty chemical manufacturers, regional pigment producers, and numerous smaller traders and custom compounders. There are over 100 active competitors worldwide, spanning large integrated producers to niche micronizing and dispersion specialists. Market positioning ranges from high-volume commodity suppliers to technology-driven premium producers focusing on nano-dispersion and low-emission manufacturing. Strategic initiatives across the sector in 2023–2024 included capacity upgrades (new lines ranging from 6,000 to 25,000 tons/year), facility modernizations, long-term raw-material supply agreements, and targeted product launches for high-purity and coated pigment grades. Partnerships between pigment makers and ceramic or coatings formulators for co-development projects account for an increasing share of R&D activity, while several mid-sized players pursued regional consolidation to improve logistics and scale.

Innovation trends shaping competition include advanced calcination technologies that can reduce energy consumption by up to 15–18%, automated dispersion and inline particle monitoring improving batch consistency by 20–30%, and surface-coating chemistries that extend pigment lifetime in harsh environments. The market is moderately concentrated at the top: the combined share of the top 5 companies is estimated in the range of 45–55%, reflecting the presence of sizable multinational producers alongside numerous regional specialists. Price sensitivity exists in bulk commodity segments, while premium and specialty segments exhibit higher margins and technological entry barriers. This multi-tiered competitive landscape requires firms to balance capital-intensive process upgrades, compliance investments, and targeted commercial partnerships to sustain growth and protect margins.

Venator

Ferro Corporation

Venator

Synthesia

Tronox

Current and emerging technologies are reshaping production economics, product performance, and compliance in the Chromium Oxide Green market. Core process technologies—advanced calcination, precision micronization, and controlled hydro/precipitation routes—remain central to product quality. Modern calcination kilns and hybrid-fuel systems have demonstrated energy reductions of 10–18% versus legacy rotary systems, enabling producers to meet stricter emissions constraints while improving thermal stability of pigment crystals. Precision micronization and air-classification enable tighter particle size distributions (D50 reductions from typical 3–5 μm down to 0.6–1.5 μm in premium grades), enhancing tint strength and dispersion in high-solid formulations.

Nano-dispersion and surface-functionalization technologies allow chromium oxide pigments to integrate more effectively in polymer matrices and advanced ceramic suspensions, improving opacity and mechanical compatibility. Automated inline dispersion monitoring—using laser diffraction and image-analysis systems—has reduced batch-to-batch variance by 20–30% in production trials, supporting higher first-pass yield in coatings and glaze lines. Digital transformation is also advancing: AI-driven process control systems and predictive maintenance tools are being adopted for kiln temperature profiling and mill-load optimization, which can cut unplanned downtime by more than 15–20% in modernized plants.

Environmental and circular technologies are increasingly important. Waste recovery and effluent treatment upgrades, combined with resource-efficient synthesis routes, allow manufacturers to meet evolving regulatory constraints and demonstrate lower embodied emissions. Additive manufacturing and digital color matching tools are creating downstream opportunities—enabling formulators to prototype pigment performance quickly and reduce time-to-market for customized chromatic formulations. For decision-makers, the technology landscape implies rising capital intensity but also potential for differentiated, higher-margin offerings through product performance, sustainability credentials, and digital-enabled quality assurance.

In August 2024, LANXESS announced it will continue chromium oxide pigment production at its Krefeld-Uerdingen site, reversing prior plans to sell the business; the move preserves about 50 jobs and follows improved raw-material contracts and cost reductions to stabilize operations. Source: www.lanxess.com

In April 2024, Venator published and launched its 2024 Sustainability Report, highlighting enhanced operational data capture and reporting across 2023–2024 and renewed commitments to low-impact pigment production and transparency in environmental metrics. Source: www.venatorcorp.com

In August 2023, LANXESS initiated its “FORWARD!” efficiency program, targeting substantial permanent cost reductions (initial one-time savings and program measures reported in 2023) as part of wider business-optimization actions affecting pigment operations and processing footprints. Source: www.lanxess.com

In 2024 (reported in the 2023–24 annual disclosures), Vishnu Chemicals documented installed capacities and operational metrics for chromium chemicals and pigments, reporting large installed capacities (tens of thousands of metric tonnes) across its manufacturing network and detailing modernization steps to support higher-purity pigment production. Source: www.vishnuchemicals.com

This report covers the full value chain and commercial landscape of chromium oxide green (Cr₂O₃) pigments and related product forms, including pigment-grade powders, micronized/ultra-fine grades, nano-dispersions, coated pigments, and masterbatch/compound formats. It analyzes segmentation by type, application (coatings, ceramics and glazes, refractories, plastics masterbatches, printing inks, specialty glass), and end-user verticals (ceramics manufacturers, protective coatings formulators, refractory producers, plastics processors, inks and specialty glass makers). Geographic scope includes detailed region-wise coverage—Asia-Pacific, Europe, North America, South America, and Middle East & Africa—along with major country profiles (e.g., China, Germany, India, United States, Brazil) and production-capacity assessments.

The report examines technology and process trends such as advanced calcination, micronization, precipitation routes, nano-dispersion, surface functionalization, and digital quality-control implementations. It assesses manufacturing footprints (typical line capacities spanning 6,000–25,000 tons/year), capital-intensity of modernization projects, and environmental compliance requirements including waste treatment and emissions controls. Competitive dynamics are covered with a focus on product differentiation strategies, top-company positioning, partnership models, capacity expansions, and regional consolidation moves. Commercial considerations include supply-chain factors (chromite feedstock access, long-term raw-material contracts), logistics and distribution models for bulk versus specialty grades, and customer-driven specifications in high-performance coatings and engineered ceramics.

The report also explores emerging niches—such as chromium-oxide-enabled high-temperature ceramics, advanced pigment systems for additive-manufactured components, and pigment formulations tailored for circular-economy manufacturing—and provides decision-oriented insights for R&D prioritization, investment planning, and market-entry strategies. The scope is structured to serve executives, product managers, technical leads, and investors seeking a granular yet actionable view of technical, commercial, and regulatory levers shaping the chromium oxide green market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 710 Million |

| Market Revenue (2032) | USD 1,065.1 Million |

| CAGR (2025–2032) | 5.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & ESG Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | LANXESS, Elementis plc, Vishnu Chemicals Limited, Venator, Ferro Corporation, Venator, Synthesia, Tronox |

| Customization & Pricing | Available on Request (10% Customization Free) |