Reports

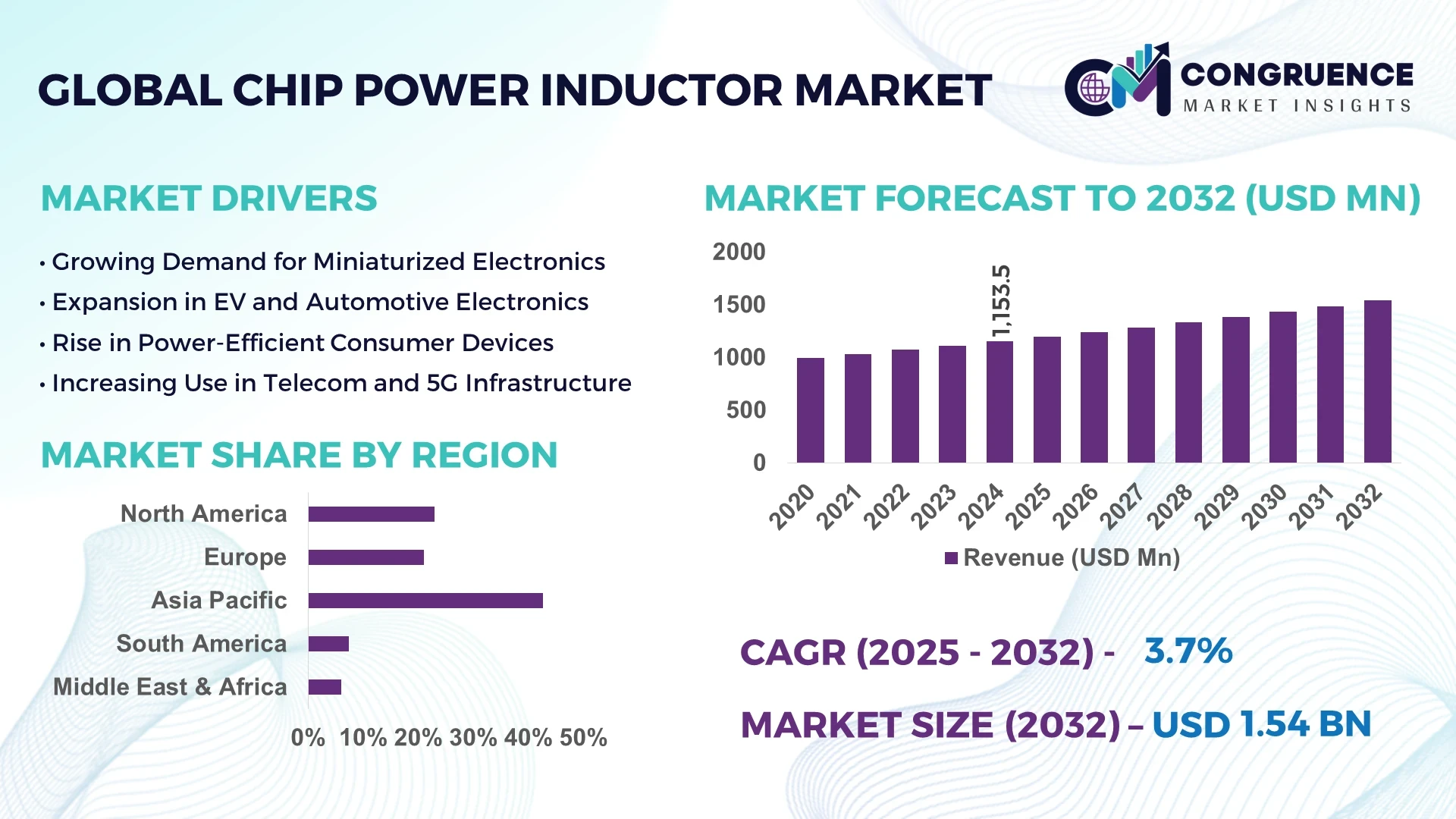

The Global Chip Power Inductor Market was valued at USD 1,153.5 Million in 2024 and is anticipated to reach a value of USD 1,542.57 Million by 2032 expanding at a CAGR of 3.7% between 2025 and 2032.

Japan maintains a leading position in the Chip Power Inductor market, backed by its expansive production capacity, high-precision manufacturing capabilities, and continuous investments in miniaturization technologies for automotive and consumer electronics applications.

The Chip Power Inductor Market is increasingly influenced by the growing integration of compact power solutions in consumer electronics, automotive infotainment, and 5G telecommunications infrastructure. Sectors such as automotive electronics and portable devices contribute significantly to the overall market demand, driven by their requirements for stable voltage regulation and high-efficiency energy conversion. The rise of smart devices and electric vehicles is fueling the need for chip-sized power components that deliver high current tolerance and thermal reliability. Technological advances such as ultra-low DCR (DC resistance) inductors and magnetic shielding innovations are reshaping performance expectations. Regulatory support for miniaturized electronics and environmentally compliant components is further accelerating the shift toward high-efficiency chip inductors. Additionally, with increasing regional consumption in East Asia and North America, manufacturers are focusing on scalable production capabilities and developing application-specific inductor variants to align with evolving performance benchmarks and environmental directives.

Artificial Intelligence (AI) is rapidly transforming the Chip Power Inductor Market by enabling precision-driven advancements in design, manufacturing, and quality assurance. AI-driven modeling tools are optimizing electromagnetic field simulations, allowing engineers to accurately predict inductor behavior under varying operating conditions. This leads to reduced design cycles and significantly faster prototyping in high-demand sectors like automotive electrification and IoT devices. AI-powered automation in manufacturing lines enhances defect detection through real-time image processing and predictive analytics, thereby improving yield rates and reducing waste.

In the Chip Power Inductor Market, AI is also playing a critical role in optimizing supply chain operations. Machine learning algorithms forecast material requirements and adjust procurement schedules to avoid delays and overstocking, particularly for rare earth metals and core materials. Moreover, AI-enhanced predictive maintenance systems are being embedded within production equipment to minimize downtime, ensuring consistent quality and cost efficiency.

On the product development side, AI is guiding the creation of application-specific inductors by analyzing vast usage data from consumer electronics and electric vehicles. This allows for fine-tuned customization of inductor values, tolerances, and thermal behaviors, helping manufacturers meet diverse global standards. By integrating AI technologies across R&D and production workflows, companies in the Chip Power Inductor Market are gaining a competitive edge through smarter, leaner, and more scalable operations, enabling faster market responsiveness and long-term sustainability.

“In March 2024, a major Japanese semiconductor firm integrated AI-based inductor modeling into its in-house electronic design automation (EDA) tools, resulting in a 22% reduction in development time for next-gen chip power inductors used in EV battery management systems.”

The Chip Power Inductor Market is undergoing a dynamic transformation driven by technological innovations, rising demand from advanced electronics, and increased adoption in electric vehicles (EVs) and 5G infrastructure. With growing demand for high-efficiency, compact, and thermally stable components, industries such as automotive, telecommunications, and consumer electronics are integrating chip power inductors into their circuit architectures. Regional growth patterns indicate robust development in Asia-Pacific due to concentrated manufacturing hubs, while North America is witnessing innovation-led expansion. The evolution of surface-mount technology and miniaturized magnetic components is further shaping product development trends. Additionally, market dynamics are being influenced by stricter environmental compliance standards and increasing use of AI in product design and testing processes.

As the global automotive industry transitions toward hybrid and electric powertrains, the demand for high-performance chip power inductors is accelerating. These components are crucial in onboard chargers, battery management systems, and DC-DC converters, where stable power delivery is essential. The growing trend of vehicle electrification—driven by regulatory pushes and consumer preference—is significantly expanding inductor applications in both passenger and commercial vehicles. According to recent industry analyses, over 70% of EV power modules now incorporate advanced chip power inductors for voltage regulation and EMI suppression. Their compact size and thermal resilience make them ideal for the constrained environments in electric drivetrains, amplifying their relevance across automotive platforms.

One of the primary restraints in the Chip Power Inductor Market is the volatility in prices of raw magnetic materials such as ferrites and rare earth metals. These materials form the core of inductors and directly influence product cost and availability. Global supply chain instability, coupled with geopolitical tensions affecting export channels—particularly for rare earth elements from countries like China—has led to unpredictable pricing patterns. Additionally, the mining and refinement of these materials are subject to environmental restrictions, which further tightens supply. As a result, manufacturers are experiencing cost pressures that constrain their ability to offer competitive pricing, especially in high-volume production environments like consumer electronics.

The ongoing global rollout of 5G networks and the explosive growth in IoT (Internet of Things) devices are creating substantial opportunities within the Chip Power Inductor Market. These advanced applications require highly efficient, miniature inductors capable of operating at high frequencies and in compact PCB layouts. Chip power inductors are increasingly used in RF modules, power amplifiers, and antenna tuning circuits in smartphones, smart home appliances, and industrial IoT gateways. With billions of devices projected to be connected via 5G over the next few years, demand for high-frequency inductors with low power loss and improved signal integrity is set to soar, encouraging further product innovation and diversification.

One of the most pressing challenges in the Chip Power Inductor Market is achieving continuous miniaturization while maintaining or improving electrical performance. As manufacturers push toward smaller, thinner consumer electronics and denser automotive circuit designs, inductors must be compact without compromising on current handling, efficiency, or EMI shielding. However, shrinking the size of inductors often leads to increased heat generation, reduced inductance values, and weaker magnetic shielding. Designing products that can meet demanding electrical and thermal specifications within smaller footprints requires cutting-edge materials and manufacturing techniques, adding complexity and cost. This trade-off presents a persistent engineering challenge for companies seeking to balance size, performance, and reliability.

• Surge in High-Frequency, Miniaturized Inductors for Smartphones: With the continuous evolution of smartphone architectures, chip power inductors are being designed to support increasingly high-frequency operations in compact form factors. Manufacturers are launching inductors operating above 10 MHz, suitable for RF and power supply applications within space-constrained designs. Leading smartphone OEMs are now integrating chip inductors as small as 1.0 x 0.5 mm, which offer high inductance density and stable thermal performance. These developments are catering to thinner phone designs with higher power requirements and energy efficiency standards.

• Integration in On-Board Chargers for EVs: The automotive sector has begun widespread adoption of chip power inductors within on-board charging (OBC) modules and battery management systems. Advanced inductors that handle higher current ratings while minimizing core losses are being implemented in 400V and 800V vehicle platforms. By 2025, EVs using dual-inductor configurations for fast charging and DC-DC voltage conversion are expected to rise significantly. This trend is prompting innovation in high-saturation magnetic materials that support stable operation under variable load conditions.

• Demand from Wearables and Healthcare Electronics: Chip power inductors are seeing increasing usage in compact medical wearables and health-monitoring devices. These products require ultra-miniature inductors that consume minimal power while providing noise suppression and voltage regulation. Devices like portable ECG monitors and insulin pumps are pushing demand for micro-inductors in the sub-0603 size class. Manufacturers are optimizing inductors for biocompatibility and long-term stability, especially for wearables used in continuous patient monitoring.

• Growth in Industrial Automation and Robotics: Industrial robots and automation control systems now rely heavily on chip power inductors for power supply integrity and EMI filtering. In high-speed industrial PCs and programmable logic controllers (PLCs), inductors ensure power stability and electromagnetic compatibility. Robotics manufacturers are prioritizing inductors with wide operating temperature ranges and high mechanical reliability. This has led to a growing preference for ruggedized chip inductors in industrial sectors operating in harsh environments, including heavy machinery and smart factory setups.

The Chip Power Inductor Market is segmented based on type, application, and end-user categories. Each segment plays a vital role in shaping the overall market direction. By type, variations are defined by structure, size, and current-handling capabilities, catering to different circuit complexities. Application-wise, inductors are utilized in power management systems, RF modules, and filtering applications across industries. End-user segments include automotive, consumer electronics, telecommunications, and industrial automation—each presenting unique integration needs and performance expectations. While consumer electronics continue to dominate the usage landscape, the automotive and industrial sectors are emerging as innovation-driven domains. This segmentation offers critical insight into where product customization, manufacturing investments, and R&D are most concentrated, supporting long-term market scalability.

Shielded chip power inductors are the leading type in the market, widely preferred for their excellent EMI suppression and stability in high-frequency circuits. They are heavily used in smartphones, tablets, and automotive control modules. The fastest-growing type is the molded chip power inductor, which is gaining momentum due to its high mechanical strength, thermal resistance, and compact structure. Molded types are ideal for high-current applications such as powertrains in electric vehicles and fast-charging devices. Wire-wound chip inductors, though not the dominant type, serve specialized uses requiring high inductance values and are mostly adopted in industrial and telecommunications hardware. Multi-layer chip inductors offer better frequency characteristics and are mainly used in miniaturized devices. Their smaller size makes them attractive for wearable tech and portable health devices. Each type meets distinct application-specific needs, reinforcing the diversity and complexity of the chip power inductor market landscape.

Power supply applications represent the dominant share of the chip power inductor market, particularly in smartphones, laptops, and automotive electronics. These inductors ensure voltage stability and filtering efficiency in battery-powered and AC-DC converted systems. The fastest-growing application is within RF and communication circuits, fueled by the global rollout of 5G and increased wireless device usage. In these high-frequency systems, chip power inductors play a critical role in impedance matching and noise filtering. Chip inductors are also gaining relevance in LED drivers, ensuring consistent current flow and protecting sensitive circuits. Other emerging applications include voltage regulators and microprocessor power modules in industrial control systems. The broad utility of chip inductors across these areas highlights their importance in both energy management and signal integrity, aligning with current and future electronics design trends.

Consumer electronics is the leading end-user segment, absorbing a significant volume of chip power inductors across mobile phones, tablets, and gaming devices. This dominance is supported by the constant demand for lightweight, power-efficient components in compact devices. The fastest-growing end-user is the automotive sector, driven by increasing electrification and the integration of advanced driver-assistance systems (ADAS). Vehicles now require robust inductors for applications like engine control units, infotainment systems, and battery converters. The industrial automation segment also contributes steadily to the market, deploying chip power inductors in programmable logic controllers and embedded systems used in smart factories. Telecommunications infrastructure and medical electronics, while smaller segments, are experiencing notable growth due to expanding network coverage and the proliferation of compact diagnostic tools. These diversified end-user trends reflect the critical role chip power inductors play across modern electronic ecosystems.

Asia-Pacific accounted for the largest market share at 42.6% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 4.3% between 2025 and 2032.

The dominance of Asia-Pacific is driven by large-scale manufacturing hubs in China, Japan, and South Korea, where electronics and automotive industries lead in integrating chip power inductors into advanced circuit designs. The availability of skilled labor, strong domestic supply chains, and government-backed innovation in component miniaturization are also contributing factors.

In comparison, North America is experiencing accelerated investment in EV infrastructure and advanced semiconductor design, spurring demand for high-performance chip inductors. The region’s regulatory support for electric mobility and digital transformation across industrial automation platforms is driving product integration. Europe follows closely, leveraging strict environmental compliance standards and sustainability goals that align with efficient electronic components. Meanwhile, South America and the Middle East & Africa are showcasing steady adoption supported by energy infrastructure modernization and growing telecom investments. Each region presents unique growth triggers, positioning chip power inductors as an essential component in next-gen electronic solutions.

High Adoption of Smart Automotive and Semiconductor Platforms Boosts Regional Demand

North America held 23.8% of the global chip power inductor market in 2024, with robust growth fueled by the rapid expansion of electric vehicle production and smart consumer electronics. Automotive manufacturers across the U.S. and Canada are increasingly incorporating chip inductors into onboard power systems and battery modules. Meanwhile, the semiconductor industry benefits from strong domestic policy support aimed at boosting chip manufacturing. Regulatory initiatives like the CHIPS Act are encouraging localized component sourcing, including inductors, for critical infrastructure. Advanced manufacturing practices, coupled with AI-enhanced quality control systems, are streamlining production processes. In parallel, telecom companies are upgrading network hardware, increasing the use of chip power inductors in 5G base stations and signal filtering systems.

Sustainability Goals and Electrification Drive Advanced Component Integration

Europe accounted for 21.5% of the global chip power inductor market in 2024, with Germany, the UK, and France leading consumption volumes. The region’s green transition initiatives are driving widespread adoption of energy-efficient components across automotive and industrial applications. In Germany, for instance, the push for electric mobility has increased the use of chip power inductors in EV control systems. The European Union’s RoHS and WEEE directives have encouraged manufacturers to adopt recyclable and low-toxicity materials in chip inductor production. Furthermore, the integration of chip inductors into next-gen telecommunications and industrial automation systems is gaining traction, supported by AI-driven design tools and rapid digital transformation across smart factories.

Large-Scale Electronics Manufacturing and Material Innovations Shape Regional Growth

Asia-Pacific leads global chip power inductor consumption with the highest volume output, supported by advanced manufacturing ecosystems in China, Japan, and South Korea. China’s electronics industry is driving mass adoption of chip inductors across consumer electronics, particularly smartphones and wearables. Japan continues to invest in miniaturized magnetic materials, enabling high-efficiency inductors for compact electronics and hybrid vehicles. South Korea is focusing on semiconductor-grade chip inductors in 5G and high-performance computing. Regional infrastructure advancements, combined with government R&D incentives, are further stimulating innovation. Technology clusters such as Shenzhen and Tokyo remain global hubs for inductor design and integration, anchoring Asia-Pacific’s leadership in both demand and supply.

Infrastructure Expansion and Electronic Import Growth Create New Avenues

In South America, Brazil and Argentina are at the forefront of chip power inductor adoption, contributing to a 4.9% regional market share in 2024. Brazil's energy modernization projects, including smart grid installations and renewable power integration, have created a growing need for durable, high-efficiency inductors. Argentina’s expansion in consumer electronics assembly is also increasing the import and usage of chip inductors, particularly for mid-range devices. With government policies promoting digital infrastructure and tax relief on certain electronic imports, local manufacturers are gradually increasing demand. However, production remains dependent on external suppliers, leaving room for domestic manufacturing to scale in the coming years.

Industrial Digitalization and Electrification of Key Sectors Strengthen Market Base

The Middle East & Africa region is experiencing rising demand for chip power inductors, particularly in the UAE and South Africa. In 2024, the region held a 3.6% share of the global market. The oil & gas and construction industries are adopting industrial automation systems that rely on chip inductors for power management and circuit stabilization. UAE’s investments in smart city infrastructure and South Africa’s renewable energy projects are driving advanced component integration. Governments are offering favorable trade agreements and customs duty exemptions on imported high-tech electronics, further stimulating the market. Additionally, local telecom sectors are expanding 5G rollout plans, boosting the need for RF-compatible chip inductors in base stations and mobile devices.

Japan – 21.3% market share

High production capacity and specialization in ultra-miniature inductor design for automotive and consumer electronics.

China – 19.8% market share

Strong end-user demand from mass electronics manufacturing and expanding 5G infrastructure networks.

The Chip Power Inductor market is characterized by a moderately consolidated competitive landscape, with over 30 active global and regional players consistently engaged in product innovation and strategic expansion. Leading companies focus on differentiating their offerings through advanced magnetic material technologies, reduced form factor designs, and enhanced current-handling capabilities. A significant number of market participants are emphasizing R&D investments aimed at developing high-frequency and thermally stable inductors to cater to 5G, electric vehicle, and IoT applications.

Strategic collaborations and supply chain partnerships are becoming common, particularly among players aiming to strengthen their presence in the Asia-Pacific and North American markets. Recent years have seen several key product launches in the high-density molded inductor segment, which is gaining traction in compact and energy-sensitive device categories. Mergers and acquisitions have also played a pivotal role in consolidating market share and technological expertise. Moreover, competitive dynamics are influenced by manufacturers integrating AI and machine learning into production systems to enhance precision and yield optimization. This innovation-centric competition is encouraging faster product development cycles, improved quality assurance, and scalability for customized applications across automotive, consumer electronics, and industrial verticals.

TDK Corporation

Murata Manufacturing Co., Ltd.

Panasonic Industry Co., Ltd.

Vishay Intertechnology, Inc.

Taiyo Yuden Co., Ltd.

Bourns, Inc.

Samsung Electro-Mechanics

Sumida Corporation

Würth Elektronik GmbH & Co. KG

Chilisin Electronics Corp.

The Chip Power Inductor Market is witnessing substantial technological evolution driven by advances in materials science, miniaturization, and high-frequency design capabilities. One of the key developments is the adoption of ferrite and metal composite materials, which provide improved magnetic saturation, reduced core losses, and better thermal stability under high current loads. These materials enable chip inductors to perform efficiently in compact designs, essential for next-generation devices like ultra-slim smartphones and wearable electronics. Another significant technological shift involves the integration of surface-mount technology (SMT) for automated and high-precision assembly. SMT-compatible chip inductors are now available in ultra-small sizes such as 0402 and 0603 formats, optimized for densely packed PCBs in IoT and RF applications. Moreover, advancements in molded inductor structures have enabled higher mechanical strength and vibration resistance, making them suitable for automotive electronics and harsh industrial environments.

AI-driven simulation tools are also impacting inductor design. Manufacturers are leveraging machine learning algorithms to optimize magnetic flux distribution, reduce EMI emissions, and enhance electrical performance. This data-driven design methodology shortens development cycles and leads to more customized solutions for applications like battery management systems and high-efficiency power converters. Furthermore, emerging innovations such as hybrid inductor configurations, combining the benefits of wire-wound and multilayer structures, are entering pilot production. These hybrid solutions aim to strike a balance between high inductance and compact form factors, opening doors to specialized uses in 5G base stations, AR/VR devices, and energy storage applications. The continued focus on material innovation, automated manufacturing, and smart design tools is setting the foundation for scalable, high-performance chip power inductor solutions across diversified electronics markets.

• In March 2024, TDK Corporation announced the launch of a new series of wire-wound chip power inductors designed for automotive DC-DC converters, offering operating temperatures up to 150°C and current ratings of up to 20A for robust EV power management systems.

• In December 2023, Murata expanded its manufacturing line in Japan to include automated AI-based inspection systems for chip inductors, improving quality control and reducing inspection time by 35%, targeting large-scale consumer electronics production.

• In May 2024, Taiyo Yuden introduced a compact 1005-size multilayer chip power inductor designed for 5G smartphones and high-frequency communication devices, enabling efficient performance within limited PCB space while maintaining low loss characteristics.

• In September 2023, Würth Elektronik launched a new line of shielded molded SMD power inductors tailored for industrial IoT applications, featuring enhanced mechanical reliability and reduced EMI for use in PLCs and edge computing modules.

The Chip Power Inductor Market Report provides an in-depth analysis of the global market across multiple dimensions, covering product types, application sectors, end-users, and geographic regions. It includes detailed segmentation by type such as shielded, unshielded, molded, wire-wound, and multilayer chip inductors, offering insights into their use cases, design attributes, and evolving integration in electronics. Application-focused analysis spans power supplies, RF modules, LED drivers, voltage regulators, and battery management systems, identifying sector-specific demands and customization trends.

The report also examines end-user domains such as automotive, consumer electronics, industrial automation, telecommunications, and healthcare electronics. Special attention is given to emerging end-user trends like electric vehicles, 5G-enabled devices, and wearable medical technologies, which are driving demand for miniaturized and high-frequency inductors.

Geographically, the report covers key regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, providing regional breakdowns based on volume trends, manufacturing capacity, and regulatory influence. It further highlights technology innovations impacting the market—such as AI-assisted design, new magnetic materials, and automated assembly processes—allowing stakeholders to understand competitive drivers and future growth opportunities. The scope encompasses both established and emerging segments, offering strategic insights tailored for manufacturers, investors, engineers, and procurement professionals involved in the global electronics supply chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1153.5 Million |

|

Market Revenue in 2032 |

USD 1542.57 Million |

|

CAGR (2025 - 2032) |

3.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type Shielded Chip Power Inductors Molded Chip Power Inductors Wire-Wound Chip Power Inductors Multi-Layer Chip Power Inductors Others By Application Power Supply RF and Communication Circuits LED Drivers Voltage Regulators Microprocessor Power Modules Others By End-User Consumer Electronics Automotive Industrial Automation Telecommunications Medical Electronics Others |

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

TDK Corporation, Murata Manufacturing Co., Ltd., Panasonic Industry Co., Ltd., Vishay Intertechnology, Inc., Taiyo Yuden Co., Ltd., Bourns, Inc., Samsung Electro-Mechanics, Sumida Corporation, Würth Elektronik GmbH & Co. KG, Chilisin Electronics Corp. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |