Reports

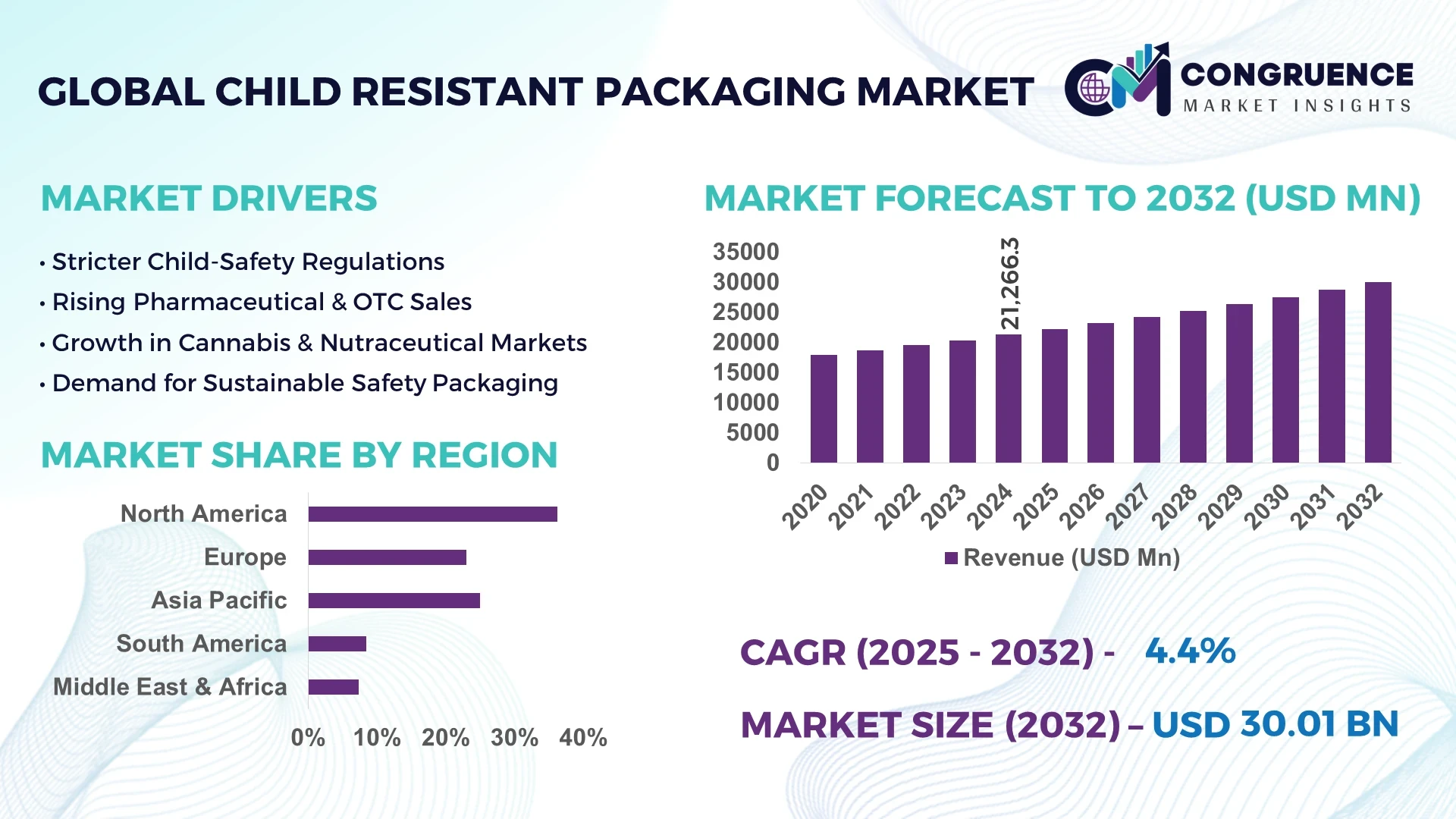

The Global Child Resistant Packaging Market was valued at USD 21,266.28 Million in 2024 and is anticipated to reach a value of USD 30,012.04 Million by 2032 expanding at a CAGR of 4.4% between 2025 and 2032.

The United States leads the global landscape in child resistant packaging due to its advanced production capacity, robust investment in smart packaging R&D, and extensive application across the pharmaceutical and cannabis sectors. American manufacturers are also integrating digital traceability and tamper-evident features using sensor-enabled packaging materials.

The Child Resistant Packaging Market is undergoing notable transformation, with significant contributions from the pharmaceutical, cannabis, household chemical, and personal care sectors. Pharmaceutical packaging continues to lead demand, particularly in compliance-driven markets such as North America and Western Europe. Cannabis legalization in regions like Canada and parts of the U.S. has fueled demand for compliant child-safe containers, pouches, and blister packs. Environmentally conscious innovations are reshaping product development—biodegradable and recyclable CR packaging solutions are gaining traction. Regulatory frameworks, such as the U.S. Poison Prevention Packaging Act and EU regulations, have intensified product testing and certification protocols. Technological innovations like multi-layer barrier materials, intuitive locking mechanisms, and tamper-proof seals are reshaping design trends. Growing consumer awareness about child safety, combined with an uptick in e-commerce distribution of OTC medications and cannabis products, is accelerating adoption globally. Additionally, the market is witnessing a gradual shift toward sustainable child resistant formats that balance safety, compliance, and environmental impact.

AI is bringing transformative changes across the Child Resistant Packaging Market by enabling predictive design, automating compliance checks, and streamlining production lines. Advanced AI algorithms are now being used to model user interaction behaviors—especially in homes with children—to design safer, more intuitive packaging formats. This technology helps reduce trial-and-error in prototyping and accelerates time-to-market for new packaging designs. In manufacturing settings, AI-powered vision systems inspect closures and locking mechanisms in real-time, enhancing quality control while reducing manual inspection costs and error rates.

Moreover, AI integration in digital twins allows packaging engineers to simulate wear-and-tear, ensuring long-term safety and durability of child-resistant containers. These models also support product customization for varied user demographics, including seniors and individuals with disabilities. In terms of regulatory compliance, AI platforms are being used to automatically scan packaging designs against legal requirements, reducing costly reworks and approval delays. The Child Resistant Packaging Market is also leveraging machine learning to optimize supply chain logistics—minimizing raw material waste and reducing lead times through predictive demand analytics.

Natural language processing (NLP) tools are employed by manufacturers to analyze consumer feedback and identify usability issues, thereby enhancing user-centric packaging innovation. These combined applications of AI not only drive operational efficiency but also help brands achieve faster certification under regulatory frameworks. Overall, the strategic deployment of AI is evolving the Child Resistant Packaging Market into a more agile, responsive, and innovation-focused industry.

“In April 2024, a leading U.S.-based packaging firm implemented an AI-powered robotic vision system that achieved a 98.6% accuracy rate in identifying micro-defects in child resistant closures during high-speed production, reducing quality control costs by 35% and improving product safety compliance timelines by nearly 22%.”

The Child Resistant Packaging Market is driven by regulatory enforcement, rising consumer safety awareness, and industry-specific demands, particularly from pharmaceuticals and legalized cannabis. Heightened focus on child safety compliance across international markets continues to shape packaging innovations and certifications. Manufacturers are shifting toward eco-conscious materials that fulfill both sustainability and safety standards, reflecting a dual-priority approach by stakeholders. Additionally, digital transformation in packaging—via smart labeling, sensor integration, and AI-driven quality assurance—has accelerated process optimization and market responsiveness. With increasing adoption in non-pharmaceutical verticals such as household chemicals and CBD-infused wellness products, the market is diversifying in application. However, stringent testing requirements and shifting global compliance laws remain ongoing variables influencing the pace of commercialization and product rollout strategies.

The global expansion of legalized medical and recreational cannabis has become a significant catalyst for the Child Resistant Packaging Market. In North America, states such as California, Colorado, and New York require cannabis products to comply with child-resistant packaging laws. This trend has triggered demand for compliant packaging formats including opaque pouches, locking containers, and reclosable tubes. Canada’s national cannabis legislation further mandates standardized child-safe closures and tamper-proof packaging features. These requirements have pushed manufacturers to develop cost-effective, multi-layer barrier solutions tailored to the cannabis supply chain. Moreover, cannabis edibles and concentrates—often packaged in small containers—necessitate innovation in tamper resistance and accidental ingestion prevention. This regulatory push has created an entirely new application sector, expanding the market scope significantly and intensifying competition among packaging solution providers.

The financial and logistical burden of meeting international child-resistant packaging standards remains a pressing restraint in the market. Compliance testing under regulations such as 16 CFR 1700.20 in the U.S. involves rigorous procedures, including panels of children and adults to test ease of access and usability. These trials are both time-consuming and expensive, often requiring multiple iterations before approval. Additionally, the growing demand for eco-friendly packaging materials adds another layer of complexity—biodegradable materials often underperform in mechanical resistance tests, necessitating costly reinforcements or hybrid materials. Smaller manufacturers and startups are particularly impacted, facing barriers to entry due to limited R&D budgets and long testing cycles. The challenge of balancing sustainability, child safety, and user convenience without exceeding production costs is slowing down product development pipelines and limiting market participation for newer players.

The rising global emphasis on eco-friendly materials presents a major opportunity for the Child Resistant Packaging Market. Brands and manufacturers are investing in recyclable, compostable, and biodegradable packaging formats that maintain safety without compromising environmental responsibility. For instance, plant-based polymers and paperboard with engineered locking mechanisms are gaining traction among sustainable packaging innovators. The EU’s proposed green packaging regulations, alongside voluntary corporate ESG initiatives, are encouraging large-scale adoption of low-impact materials in CR-certified formats. Moreover, consumer preference for brands that align with sustainability goals is influencing procurement strategies across pharma, personal care, and cannabis verticals. Emerging technologies in material science, such as water-soluble films with child-resistant overlays and monomaterial pouch innovations, are expected to unlock new segments and enhance market differentiation in the years ahead.

One of the persistent challenges in the Child Resistant Packaging Market is achieving a balance between safety and accessibility. While child resistance is a regulatory necessity, many packaging solutions unintentionally create barriers for elderly or disabled users. Arthritis patients and senior citizens often struggle with press-and-turn or squeeze-and-pull mechanisms, leading to non-compliance or misuse. These concerns are especially critical in pharmaceutical packaging where timely medication access is vital. Packaging engineers face the complex task of designing closures that meet legal child resistance standards while remaining user-friendly for adults with dexterity limitations. This usability gap has prompted legal scrutiny and product recalls in certain markets, compelling manufacturers to re-evaluate design standards and invest in inclusive innovation. Striking this balance without compromising regulatory compliance or increasing costs remains an industry-wide challenge.

• Expansion of Reclosable Flexible Packaging Formats: Reclosable pouches and zipper-lock bags are gaining momentum within the Child Resistant Packaging market, especially across the cannabis and nutraceutical industries. These formats combine tamper-evident features with convenient resealability, satisfying both compliance and consumer usability. In 2024, child resistant reclosable pouches accounted for over 32% of flexible CR packaging sold in North America. Brands prefer these due to cost-effectiveness, branding potential, and improved shelf appeal. Material advancements in laminated films and barrier coatings are enabling better moisture, oxygen, and odor protection while maintaining certified child resistance.

• Growth in Smart Packaging Integration: Smart packaging is influencing product innovation in child resistant formats through embedded NFC chips, QR codes, and digital authentication labels. These elements not only deter tampering and counterfeiting but also offer traceability across supply chains. In Europe and North America, over 18% of newly launched CR packaging for pharmaceuticals in 2024 included some form of smart labeling. This surge is driven by regulatory compliance requirements, e-commerce growth, and rising consumer demand for transparent product information.

• Surge in Custom CR Packaging for Cannabis Products: As legal cannabis markets expand, so does the demand for custom-designed child resistant packaging tailored to edibles, concentrates, and pre-rolls. In 2024, over 1.4 billion cannabis units were sold with child resistant packaging in the U.S. alone. Brands are investing in visually distinct and compliant designs that enhance shelf differentiation while adhering to state-specific regulatory mandates. The push toward brand-owned packaging formats with proprietary safety mechanisms is reshaping competition and innovation across cannabis packaging providers.

• Shift Toward Sustainable Child Safe Packaging: There is a clear movement toward eco-friendly child resistant packaging solutions. Manufacturers are increasingly adopting recyclable mono-material structures and compostable containers, particularly in the personal care and household chemical sectors. In 2024, over 25% of new CR packaging introduced in these segments were labeled as sustainable. These formats are designed to reduce environmental impact without compromising safety features. Recyclable rigid plastics with built-in locking systems and biodegradable films with engineered closures are leading this transition.

The Child Resistant Packaging market is segmented by type, application, and end-user, offering a diversified landscape driven by safety standards, consumer usability, and industry-specific regulations. In terms of types, the market includes push-and-turn caps, squeeze-and-pull systems, reclosable pouches, blister packs, and others—each addressing unique usage scenarios and compliance requirements. Applications range across pharmaceuticals, cannabis, personal care products, and household chemicals, with pharmaceuticals remaining the dominant application due to global medication safety standards. However, emerging segments such as legalized cannabis and wellness supplements are rapidly gaining traction. Regarding end-users, the primary users include pharmaceutical companies, cannabis product manufacturers, chemical producers, and FMCG brands. Pharmaceutical companies remain the core end-user group, while cannabis manufacturers are experiencing the fastest adoption due to stringent packaging laws and product diversity. Across all segments, the trend is toward customizable, sustainable, and user-friendly designs that meet both regulatory and consumer demands.

Push-and-turn caps continue to lead the Child Resistant Packaging market in 2024, dominating due to their longstanding regulatory approval, cost efficiency, and integration into prescription and OTC drug bottles. Their ease of mass production and compatibility with standard container formats makes them the preferred option for pharmaceutical companies globally. Meanwhile, reclosable pouches are the fastest-growing type, especially in cannabis and nutraceutical packaging. These pouches offer resealability, compliance, and branding flexibility, particularly for single-dose or edible product packaging. Squeeze-and-pull systems are being used in personal care and cleaning products where the packaging must ensure safety without frustrating adult users. Blister packs remain relevant in unit-dose pharmaceutical packaging and have witnessed technological advancements in material design to improve seal integrity. Other types, including slide-box mechanisms and locking tins, are gaining popularity in niche segments like luxury cannabis goods and travel-size personal care products. This variety reflects the increasing specialization and design-driven differentiation across the industry.

Pharmaceuticals remain the leading application for child resistant packaging, reflecting ongoing global mandates for child safety in medication distribution. With widespread use in prescription drugs, OTC medications, and liquid therapeutics, this application represents the backbone of the market. In 2024, over 65% of certified CR packaging units were linked to pharmaceutical uses. Cannabis packaging is the fastest-growing application area, driven by legalization across North America and expanding consumer product varieties such as edibles, concentrates, and vape products. Stringent packaging regulations requiring both tamper-evident and child resistant properties are accelerating innovation in this segment. Household chemicals—particularly cleaning agents, laundry pods, and pest control products—also require child resistant solutions due to their toxic nature. Personal care products, such as essential oils and nutraceuticals, are beginning to incorporate CR packaging, especially in premium segments. As more industries adopt safety-first packaging frameworks, application diversity in the CR market continues to broaden.

Pharmaceutical companies are the largest end-users in the Child Resistant Packaging market, accounting for a majority of global packaging deployments due to decades of compliance enforcement under poison prevention regulations. These organizations demand high-volume, cost-effective CR formats compatible with automated filling systems, particularly for tablets, liquids, and capsules. Cannabis product manufacturers represent the fastest-growing end-user group, reflecting rapid legalization trends and evolving packaging mandates. This segment actively invests in customized, brand-specific CR solutions that comply with complex regional regulations. Chemical manufacturers, especially those in consumer cleaning and pesticide industries, are also notable end-users due to the necessity of keeping hazardous products away from children. Personal care and wellness brands are entering the market more aggressively, driven by demand for safer packaging in aromatherapy oils, dietary supplements, and herbal remedies. These brands are increasingly integrating child resistance as part of broader consumer trust and sustainability strategies, influencing packaging design and procurement decisions.

North America accounted for the largest market share at 36.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

The Child Resistant Packaging market in North America is mature, bolstered by strong demand from pharmaceutical and cannabis industries, stringent regulatory compliance, and extensive R&D investments. Meanwhile, Asia-Pacific’s rapid industrialization, expanding pharmaceutical production, and increasing child safety regulations are creating a favorable landscape for market expansion. Countries like China and India are scaling up production capacities and adopting smart packaging technologies, propelling regional growth. Europe holds a significant share due to sustainability mandates and material innovation across major economies. Latin America and the Middle East & Africa show emerging potential, supported by infrastructure development and evolving regulatory frameworks. Technological adoption, evolving safety standards, and cross-border trade dynamics continue to influence regional market trajectories across all continents.

Smart Label Integration Enhancing Safety and Compliance

North America held a 36.2% share of the global Child Resistant Packaging market in 2024, led primarily by strong adoption in pharmaceuticals, legalized cannabis, and household chemical segments. The U.S. dominates regional demand, fueled by advanced compliance protocols under the Poison Prevention Packaging Act and growing investments in sustainable, digital-ready packaging. Canada follows closely, driven by cannabis legalization, which mandates certified child resistant containers for all formats including edibles and concentrates. Regulatory support from federal and state agencies continues to shape innovation and design parameters. North American companies are integrating smart label technologies and tamper-evident RFID tags to enhance traceability and ensure regulatory conformity. Automation in quality checks and the shift toward lightweight, recyclable CR packaging also define ongoing technological advancements.

Eco-Certified Materials Driving Packaging Innovation

Europe captured 28.5% of the Child Resistant Packaging market in 2024, with Germany, the UK, and France leading adoption across pharmaceutical and personal care sectors. The European Medicines Agency and national regulators enforce stringent CR requirements, pushing companies to invest in standardized, user-friendly packaging formats. EU-wide sustainability mandates, including the Single-Use Plastics Directive, are encouraging the use of compostable and recyclable child resistant materials. Germany’s focus on circular packaging models and the UK's push for sustainable healthcare packaging are influencing broader regional trends. Digital authentication features and intelligent packaging systems are gaining traction among premium product lines. Collaborative projects across the EU are promoting cross-border compliance and harmonization of safety testing standards.

High-Speed Production Driving Regional Demand Surge

Asia-Pacific ranks as the fastest-growing region by volume in the Child Resistant Packaging market. China, India, and Japan are the top consumers, collectively driving a major shift toward localized, high-speed CR production to meet growing pharmaceutical and FMCG demand. In 2024, regional manufacturers ramped up investment in automation and smart tooling to support mass production of CR pouches, blister packs, and locking closures. Government initiatives to enforce pharmaceutical safety packaging in India and digital tracking mandates in China are strengthening compliance frameworks. Japan’s aging population is also influencing ergonomic innovations in CR packaging design. Innovation hubs in Singapore and South Korea are accelerating research into biodegradable CR formats using plant-based polymers and smart sensors.

Cannabis Legalization Catalyzing Packaging Reform

In 2024, South America held an estimated 5.8% share of the global Child Resistant Packaging market, with Brazil and Argentina leading demand. Brazil’s expanding pharmaceutical production base and Argentina’s evolving cannabis legalization have spurred interest in certified child resistant containers. Infrastructure development in regional industrial parks is attracting international packaging manufacturers. There is increasing adoption of sustainable and tamper-proof packaging in agrochemicals and household cleaning products. Government incentives for domestic packaging innovation, especially in Brazil’s energy sector, are indirectly boosting demand for CR solutions. Latin American trade policies now include safety compliance mandates for chemical and medical exports, reinforcing the importance of certified packaging standards across industries.

Industrial Safety Demands Boosting Packaging Compliance

Middle East & Africa accounted for approximately 4.3% of the Child Resistant Packaging market in 2024. Regional demand is shaped by safety needs in oil & gas, industrial chemicals, and expanding pharmaceutical sectors. The UAE and South Africa are key growth countries, with rising implementation of international safety and packaging standards. Local regulations are gradually aligning with EU and U.S. protocols, prompting increased certification requirements for packaging exporters. The region is witnessing technological modernization, including digital barcode systems for traceability and semi-automated CR packaging lines. In the consumer segment, increasing awareness around child safety is leading to adoption of locking closures and tamper-resistant formats in home care products. Trade partnerships with Asia-Pacific and Europe are further accelerating the introduction of advanced packaging technologies.

United States – 30.8% market share

Strong end-user demand across pharma and cannabis sectors supported by high production capacity and strict regulatory compliance.

China – 17.6% market share

Rapid industrial expansion and investment in automated CR packaging systems driving robust market growth.

The Child Resistant Packaging market is marked by intense competition, with over 80 globally active manufacturers vying for innovation leadership and regulatory compliance. Market participants are strategically positioned across North America, Europe, and Asia-Pacific, with the U.S., Germany, and China serving as primary hubs for technological advancement and high-volume production. Leading players continue to expand product portfolios through acquisitions and co-development agreements, particularly in high-growth segments like cannabis packaging and sustainable pharmaceutical solutions.

Product differentiation through patented closure mechanisms, smart labeling features, and ergonomic design is a key strategy. In 2024, over 30% of newly released CR packaging solutions included smart technology such as tamper-evident indicators and digital traceability. Competitive dynamics are further influenced by sustainability goals, with companies investing in recyclable mono-materials, compostable films, and low-impact adhesives. Mergers and joint ventures between packaging manufacturers and raw material providers are accelerating R&D pipelines. Regional players are gaining ground by offering localized, regulation-compliant CR formats at competitive pricing. As regulatory frameworks evolve and cross-border trade expands, companies are also scaling testing and certification capabilities to maintain global market access.

Berry Global Inc.

Gerresheimer AG

Pretium Packaging LLC

Amcor Plc

Origin Pharma Packaging

Kaufman Container

Global Closure Systems

Comar LLC

MJS Packaging

Bilcare Ltd.

Technological innovation continues to redefine the Child Resistant Packaging market, with advancements focused on enhancing safety, sustainability, and efficiency. Smart packaging technologies, including RFID-embedded closures and tamper-evident seals with digital verification, are being adopted in pharmaceutical and cannabis packaging. These innovations offer real-time product authentication and consumer engagement while meeting stringent compliance standards.

Automation in packaging lines has significantly increased production efficiency. In 2024, over 40% of new CR packaging production facilities incorporated robotic assembly systems for precision in closure alignment and quality control. AI-powered vision systems are being utilized to detect micro-defects in caps and closures, enhancing product reliability and reducing error rates by up to 90%. Digital twin simulations are also aiding in stress-testing CR mechanisms, optimizing designs for both child safety and adult accessibility.

Material science is another key focus area. Manufacturers are developing biodegradable, compostable, and recyclable materials that meet CR certification requirements. Examples include mono-material pouches with engineered locking layers and plant-based polymers used in press-and-turn caps. Thermoforming technology is enabling stronger blister packs with minimal plastic content. Additionally, 3D printing is being explored for rapid prototyping of complex locking systems. These technological advancements are driving differentiation, compliance, and speed-to-market across high-demand sectors.

• In March 2024, Origin Pharma Packaging launched a new range of recyclable PET child resistant bottles for liquid pharmaceuticals, engineered with tamper-evident dropper caps and tested for adult accessibility across multiple demographics.

• In November 2023, Berry Global announced the expansion of its CR packaging portfolio with the introduction of an eco-friendly push-and-turn cap using 50% post-consumer recycled resin, optimized for OTC medication containers.

• In February 2024, Gerresheimer AG integrated digital printing technology into its CR packaging production lines, enabling serialized, track-and-trace labeling for regulatory compliance in EU pharmaceutical exports.

• In August 2023, Pretium Packaging unveiled a lightweight, child-resistant closure specifically for cannabis flower jars, featuring a proprietary locking mechanism and 20% reduction in plastic usage compared to previous models.

The Child Resistant Packaging Market Report provides a comprehensive assessment of market dynamics, technologies, applications, and regional developments shaping the global landscape. The report examines all major product segments including push-and-turn caps, reclosable pouches, blister packs, squeeze-and-pull systems, and advanced locking mechanisms. It explores their adoption across core application areas such as pharmaceuticals, cannabis, household chemicals, and personal care. Geographically, the report covers market trends and strategic insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Specific attention is given to top-performing countries like the United States, China, Germany, Canada, and India. Regional policy frameworks, safety regulations, and import-export trends are factored into the competitive analysis.

The report analyzes current technologies influencing market evolution, such as smart labeling, automated inspection systems, biodegradable materials, and AI-driven design tools. It also investigates supply chain transformations, sustainable sourcing practices, and customization strategies impacting product innovation. Emerging segments such as cannabis packaging and eco-compliant CR formats are also explored. Targeted at packaging manufacturers, material suppliers, investors, and regulatory bodies, the report provides data-driven insights to guide strategic decisions. It serves as a valuable tool for benchmarking innovation, evaluating competitive positioning, and identifying high-growth opportunities in this safety-critical packaging sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 21266.28 Million |

|

Market Revenue in 2032 |

USD 30012.04 Million |

|

CAGR (2025 - 2032) |

4.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Berry Global Inc., Gerresheimer AG, Pretium Packaging LLC, Amcor Plc, Origin Pharma Packaging, Kaufman Container, Global Closure Systems, Comar LLC, MJS Packaging, Bilcare Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |