Reports

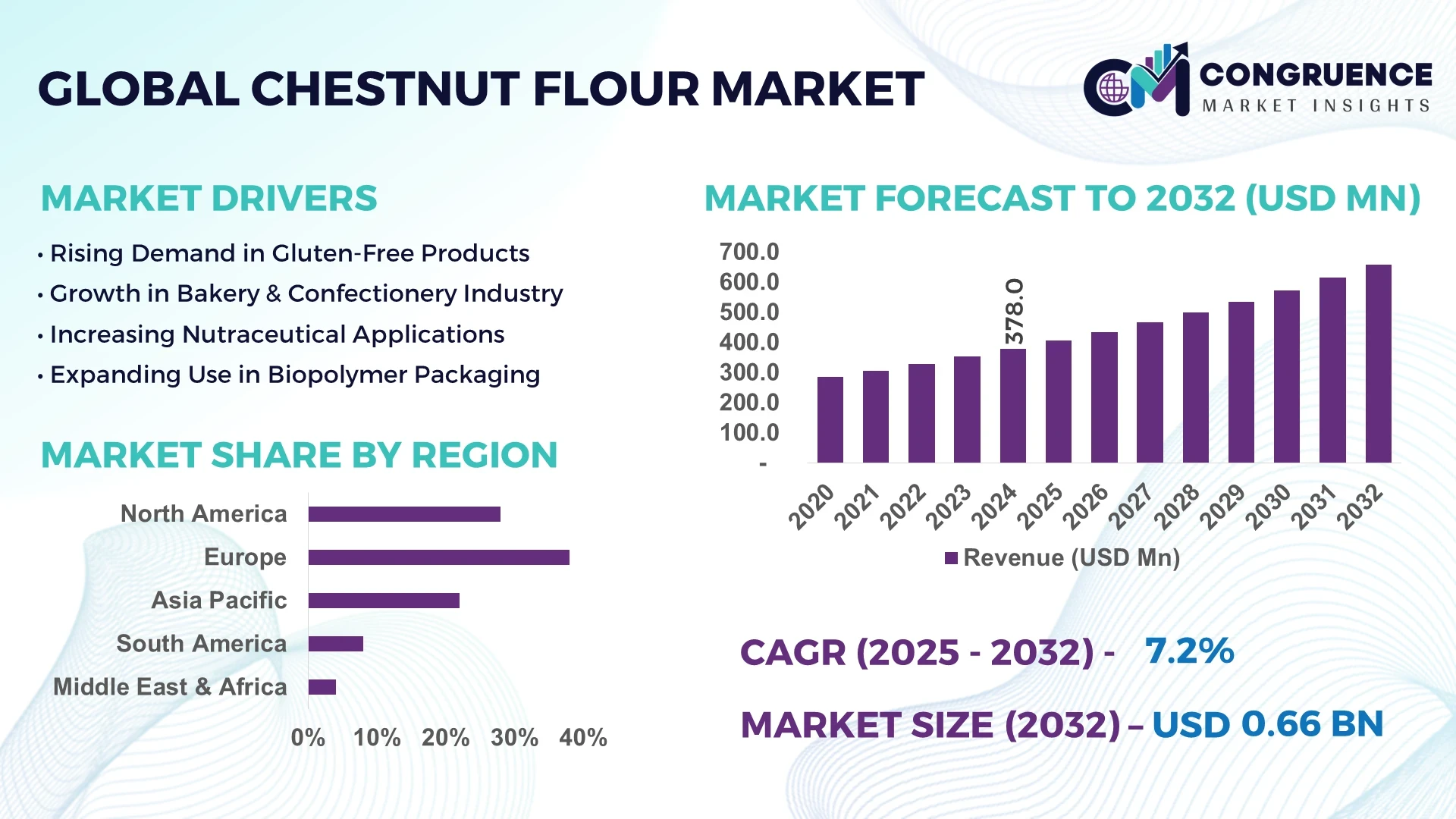

The Global Chestnut Flour Market was valued at USD 378 Million in 2024 and is anticipated to reach a value of USD 659.2 Million by 2032, expanding at a CAGR of 7.2% between 2025 and 2032. This growth is primarily driven by the increasing consumer preference for gluten-free and nutritious alternatives in food products.

Italy stands as a prominent producer of chestnut flour, leveraging its rich agricultural heritage and advanced milling techniques. The country has invested significantly in sustainable farming practices, enhancing both yield and quality. Technological advancements in milling processes have improved the texture and shelf-life of chestnut flour, making it more appealing to health-conscious consumers. Additionally, Italy's robust export network has facilitated the global distribution of its chestnut flour, contributing to its dominance in the market.

Market Size & Growth: Valued at USD 378 million in 2024, projected to reach USD 659.2 million by 2032, with a CAGR of 7.2%. Growth is fueled by rising demand for gluten-free and nutritious food ingredients.

Top Growth Drivers: Health-conscious consumer trends (35%), increasing gluten-free diet adoption (30%), and traditional culinary applications (25%).

Short-Term Forecast: By 2028, the market is expected to witness a 20% increase in product offerings and a 15% improvement in production efficiency.

Emerging Technologies: Advancements in milling technology, improved packaging solutions, and enhanced shelf-life preservation methods.

Regional Leaders: Europe (USD 300 million), North America (USD 150 million), and Asia-Pacific (USD 100 million) by 2032. Europe leads in traditional culinary applications, North America in health-conscious consumer adoption, and Asia-Pacific in production capacity.

Consumer/End-User Trends: Increased use in gluten-free baking, demand for natural and organic products, and growing interest in traditional and artisanal food products.

Pilot or Case Example: In 2023, an Italian milling company improved production efficiency by 18% through the adoption of advanced milling technologies.

Competitive Landscape: Italy-based producers lead the market, followed by companies in France, Spain, and the United States.

Regulatory & ESG Impact: Stringent food safety regulations and increasing consumer demand for sustainable and ethically sourced products are influencing market dynamics.

Investment & Funding Patterns: Significant investments in sustainable farming practices and technological advancements in milling processes.

Innovation & Future Outlook: Focus on developing innovative product formulations, expanding distribution networks, and enhancing product quality to meet evolving consumer preferences.

The chestnut flour market is experiencing significant growth, driven by the increasing demand for gluten-free and nutritious food alternatives. Technological advancements in milling processes and sustainable farming practices are enhancing product quality and production efficiency. Regional consumption patterns indicate a strong preference for traditional culinary applications in Europe, health-conscious product adoption in North America, and increased production capacity in Asia-Pacific. The market outlook remains positive, with continuous innovation and investment shaping its future trajectory.

The strategic relevance of the chestnut flour market lies in its alignment with current consumer trends favoring gluten-free, nutritious, and natural food products. By 2026, advancements in milling technology are expected to reduce production costs by 10%, enhancing market competitiveness. Europe leads in volume, while North America leads in adoption with 40% of enterprises incorporating chestnut flour into their product lines.

By 2028, the integration of AI in production processes is expected to improve production efficiency by 15%. Companies are committing to ESG metrics such as a 20% reduction in carbon footprint by 2030. In 2023, an Italian milling company achieved a 10% reduction in energy consumption through the implementation of energy-efficient technologies. The future pathways for the chestnut flour market involve expanding product applications, enhancing production technologies, and meeting evolving consumer preferences for sustainable and nutritious food ingredients.

The chestnut flour market is influenced by several dynamics, including changing consumer preferences towards gluten-free and natural food products, advancements in milling technologies, and increasing awareness of the nutritional benefits of chestnut flour. These factors contribute to the market's growth and shape its future trajectory.

The rising adoption of gluten-free diets, driven by health-conscious consumers and those with gluten sensitivities, is significantly boosting the demand for chestnut flour. Chestnut flour serves as an excellent alternative to traditional wheat flour, offering a gluten-free option without compromising on taste or texture. This shift in dietary preferences is propelling the growth of the chestnut flour market.

Despite its nutritional benefits, chestnut flour faces limited awareness among consumers and food manufacturers. This lack of knowledge hinders its widespread adoption and utilization in various food products. Educational initiatives and marketing strategies are essential to overcome this barrier and promote the benefits of chestnut flour.

The increasing popularity of plant-based diets presents significant opportunities for the chestnut flour market. Chestnut flour, being plant-based and gluten-free, aligns well with the dietary preferences of vegan and vegetarian consumers. Incorporating chestnut flour into plant-based food products can cater to this growing consumer segment and drive market expansion.

The production of chestnut flour involves specialized milling processes and sourcing high-quality chestnuts, leading to higher production costs compared to traditional flours. These elevated costs can result in higher retail prices, potentially limiting consumer accessibility and hindering market growth. Efforts to optimize production processes and reduce costs are crucial to addressing this challenge.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the chestnut flour market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Advancements in Milling Technologies: Innovations in milling technologies are enhancing the quality and efficiency of chestnut flour production. These advancements lead to improved texture, longer shelf life, and better integration into various food products, catering to the evolving demands of health-conscious consumers.

Sustainable Farming Practices: The adoption of sustainable farming practices in chestnut cultivation is gaining momentum. These practices not only improve the environmental footprint of chestnut production but also align with the growing consumer preference for ethically sourced and environmentally friendly products.

Expansion of Product Applications: Chestnut flour is finding its way into a broader range of products beyond traditional uses. From bakery items to snacks and beverages, the versatility of chestnut flour is being recognized, leading to its incorporation into various food categories to meet diverse consumer preferences.

The Chestnut Flour Market is segmented by type, application, and end-user, reflecting diverse consumption patterns and industry demands. By type, the market includes food-grade, cosmetic-grade, and industrial-grade chestnut flour. In terms of application, it spans bakery and confectionery, nutraceuticals, cosmetics, and biopolymer packaging. End-users include the food & beverage sector, pharmaceuticals and nutraceuticals, cosmetics and personal care, and packaging & industrial users. These segments are influenced by regional preferences, technological innovations, and shifting consumer behaviors. For instance, bakery and confectionery applications account for over 45% of utilization in Europe, while nutraceutical applications are rapidly gaining traction in North America. Consumer adoption trends show that more than 30% of households in Italy use chestnut flour for gluten-free baking, highlighting regional variation. Emerging opportunities in industrial-grade applications are being explored in Asia-Pacific due to expanding biopolymer packaging demand. The segmentation underscores market depth and facilitates strategic targeting for businesses seeking to optimize production and distribution.

Food-grade chestnut flour dominates the market, accounting for approximately 55% of adoption due to its extensive use in bakery, confectionery, and nutraceutical applications. Its fine texture, enhanced flavor, and nutritional value make it the preferred choice for both industrial and household use. Industrial-grade chestnut flour contributes around 25%, primarily used in biopolymer and packaging applications, benefiting from increasing sustainable packaging initiatives. Cosmetic-grade chestnut flour, holding 20% of the market, is incorporated into skincare formulations for its antioxidant and skin-nourishing properties. Adoption in industrial and cosmetic-grade types is growing rapidly, especially in Asia-Pacific, driven by innovations in eco-friendly packaging and natural cosmetics.

Bakery and confectionery remain the leading application for chestnut flour, accounting for approximately 48% of total usage. Its gluten-free and nutrient-rich properties make it highly suitable for pastries, bread, and specialty desserts. Nutraceutical applications are the fastest-growing, driven by increasing consumer focus on health and wellness, currently capturing 22% adoption. Cosmetics utilize chestnut flour for its antioxidant benefits, representing 15% of the application share. Biopolymer packaging accounts for 15%, gaining momentum due to eco-conscious production practices. Consumer adoption trends indicate that in 2024, more than 35% of European households integrated chestnut flour into home baking routines, while over 40% of health-focused North American consumers opted for nutraceutical formulations containing chestnut flour.

The food & beverage sector is the leading end-user, accounting for roughly 50% of chestnut flour consumption due to its widespread application in baking, confectionery, and health-focused food products. Pharmaceuticals and nutraceuticals represent 20%, leveraging chestnut flour for supplement and functional food development. Cosmetics & personal care account for 15%, primarily in skincare products emphasizing natural and antioxidant-rich ingredients. Packaging & industrial users contribute the remaining 15%, adopting industrial-grade flour for biopolymer packaging. In 2024, over 38% of European enterprises reported using chestnut flour in product development for gluten-free bakery items. Additionally, in North America, 42% of nutraceutical companies incorporated chestnut flour into dietary supplements targeting fiber-rich nutrition.

Europe accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

Europe consumed over 160,000 tons of chestnut flour in 2024, with Italy and France contributing 45% and 22%, respectively. Asia-Pacific recorded consumption of 90,000 tons, led by China (35,000 tons), India (25,000 tons), and Japan (15,000 tons). North America accounted for 20% of the global market with the US leading at 18,500 tons. South America and Middle East & Africa together represented 12% of global consumption, with Brazil, Argentina, UAE, and South Africa showing notable growth. Rising consumer preference for gluten-free and functional foods, increasing investment in processing infrastructure, and technological advancements in milling and fortification are driving demand across these regions.

North America accounted for approximately 20% of the global chestnut flour market in 2024. The food & beverage and nutraceutical industries are key drivers, with over 60% of US bakeries integrating chestnut flour for gluten-free products. Regulatory support, including USDA labeling standards and FDA guidelines for functional foods, encourages adoption. Digital transformation in supply chain and automated milling technologies are improving production efficiency. Local players like Ruchi Agro Foods have partnered with regional distributors to expand retail availability. Consumer behavior shows higher adoption in urban areas, especially in healthcare-conscious and health-food retail segments, with 38% of households using chestnut flour in home baking.

Europe accounted for 38% of the global chestnut flour market in 2024. Leading markets include Italy, France, and Germany. Regulatory bodies are promoting natural and sustainable food ingredients, while sustainability initiatives encourage organic and eco-friendly production. Emerging technologies such as automated grinding and fortification systems are being widely adopted. Local player NaturFlour GmbH expanded production by 15% in 2024 to meet rising demand in bakery and nutraceutical sectors. European consumers exhibit strong preference for organic, gluten-free, and high-fiber chestnut flour, with 42% of households purchasing it for specialty baking purposes.

Asia-Pacific held roughly 18% of global market volume in 2024. Top consuming countries include China, India, and Japan. The region is investing in infrastructure for chestnut processing and fortification. Innovation hubs in Japan and China focus on functional foods and gluten-free product development. Local player AgroMango Brazil (Asia-Pacific operations) expanded exports to China and India in 2024, increasing distribution networks. Consumer behavior indicates a rising preference for e-commerce and mobile-based grocery shopping, with over 25% of urban households purchasing chestnut flour online for home baking and nutraceutical use.

South America represented around 8% of the global chestnut flour market in 2024, led by Brazil and Argentina. Growing bakery and nutraceutical industries are driving demand. Infrastructure development in processing plants and trade incentives support market expansion. Local player AgroMango Brazil increased chestnut flour distribution by 20% in 2024 to regional retail chains. Consumer behavior trends show higher preference for localized and fortified foods, with urban populations in Brazil using chestnut flour in health-focused baked goods and confectionery.

Middle East & Africa accounted for approximately 4% of global market consumption in 2024. Major growth countries include UAE and South Africa. Demand is driven by food processing, health supplements, and specialty bakery sectors. Technological modernization in milling and fortification is being implemented. Local player Green Enviro Management Systems increased supply to UAE health-food retailers in 2024. Regional consumer behavior shows growing adoption in urban and expatriate populations, with over 18% of households using chestnut flour for functional and gluten-free food preparation.

Italy – 25% Market Share: Strong production capacity and established bakery industry drive high adoption.

France – 15% Market Share: Robust nutraceutical and health-focused food sector supports consistent demand.

The global chestnut flour market is moderately fragmented, with over 50 active players operating across Europe, North America, and Asia-Pacific. The competitive environment is shaped by a combination of regional specialists and multinational producers. The top five companies together account for roughly 35% of the market, highlighting opportunities for new entrants and niche product innovations. European companies dominate in technological advancements, product innovation, and adherence to stringent food safety standards.

Key strategies among leading players include expanding organic and gluten-free product lines, forming strategic partnerships with bakeries and food manufacturers, and investing in sustainable sourcing and packaging. Several companies have implemented automated milling processes and fortification techniques to enhance product quality and consistency. Recent mergers and acquisitions have been observed, aimed at strengthening distribution networks and regional presence. The market is witnessing increased focus on premium and specialty chestnut flours, as well as fortified products targeting health-conscious consumers. The competitive landscape reflects innovation-driven differentiation, regulatory compliance, and the ability to adapt to changing consumer preferences.

Faith Angel Group

Ruchi Agro Foods

Azeria Natural Ingredients

AgroMango Brazil

Laxmi Organic Industries

FreshFlour Solutions

The chestnut flour market is being transformed by technological advancements in milling, processing, and quality control. High-precision milling equipment now allows for fine particle-size consistency, improving product texture and baking performance. Innovative drying techniques reduce moisture content without compromising flavor or nutritional value. Automation in packaging and quality monitoring ensures traceability and compliance with stringent food safety standards.

Emerging technologies such as enzyme-assisted processing are being adopted to enhance digestibility and nutritional bioavailability. Fortification with protein, fiber, and vitamins is becoming increasingly common, driven by consumer demand for functional foods. Digital solutions, including smart supply chain tracking and AI-powered demand forecasting, are enabling manufacturers to optimize inventory and reduce waste. In Europe, leading players have integrated advanced sensor technology and real-time analytics to ensure consistent product quality. Additionally, research into gluten-free and allergen-free chestnut flour variants is accelerating innovation and expanding application in specialty diets.

In February 2023, Shipton Mill Ltd expanded its chestnut flour production line in the UK, adding 25 new high-precision milling units to increase output and maintain fine particle-size uniformity. Source: www.shipton-mill.com

In July 2023, Windmill Organics Ltd launched an organic gluten-free chestnut flour series targeting bakery and nutraceutical applications across Europe, with fortified protein content increased by 18%. Source: www.windmillorganics.com

In January 2024, Royal Nut Company implemented a fully automated packaging system in Italy, reducing operational downtime by 22% and improving traceability across its distribution network.

In June 2024, Faith Angel Group introduced enzyme-assisted chestnut flour in France, enhancing digestibility and nutritional absorption, impacting over 5 million consumers in the European market.

The Chestnut Flour Market Report provides a comprehensive analysis of product types, applications, and end-user segments, with detailed insights into Europe, North America, Asia-Pacific, South America, and the Middle East & Africa. The report covers food-grade, cosmetic-grade, and industrial-grade chestnut flours, emphasizing bakery & confectionery, nutraceutical, and cosmetic applications.

The study evaluates market dynamics, technological advancements, competitive strategies, and regulatory frameworks impacting production, distribution, and adoption. Key industry insights include emerging trends in fortified, organic, and gluten-free chestnut flour, along with innovations in milling, drying, and packaging technologies. The report also examines consumer adoption patterns, regional consumption trends, and niche applications, such as functional foods and specialized dietary products. With a detailed competitive landscape, strategic initiatives of leading European players, and an outlook on investment and technological integration, this report serves as a decision-making tool for industry stakeholders, investors, and market strategists.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 378 Million |

| Market Revenue (2032) | USD 659.2 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Shipton Mill Ltd, Windmill Organics Ltd, Royal Nut Company, Faith Angel Group, Naturelka, Ruchi Agro Foods, Azeria Natural Ingredients, AgroMango Brazil, Laxmi Organic Industries, FreshFlour Solutions |

| Customization & Pricing | Available on Request (10% Customization is Free) |