Reports

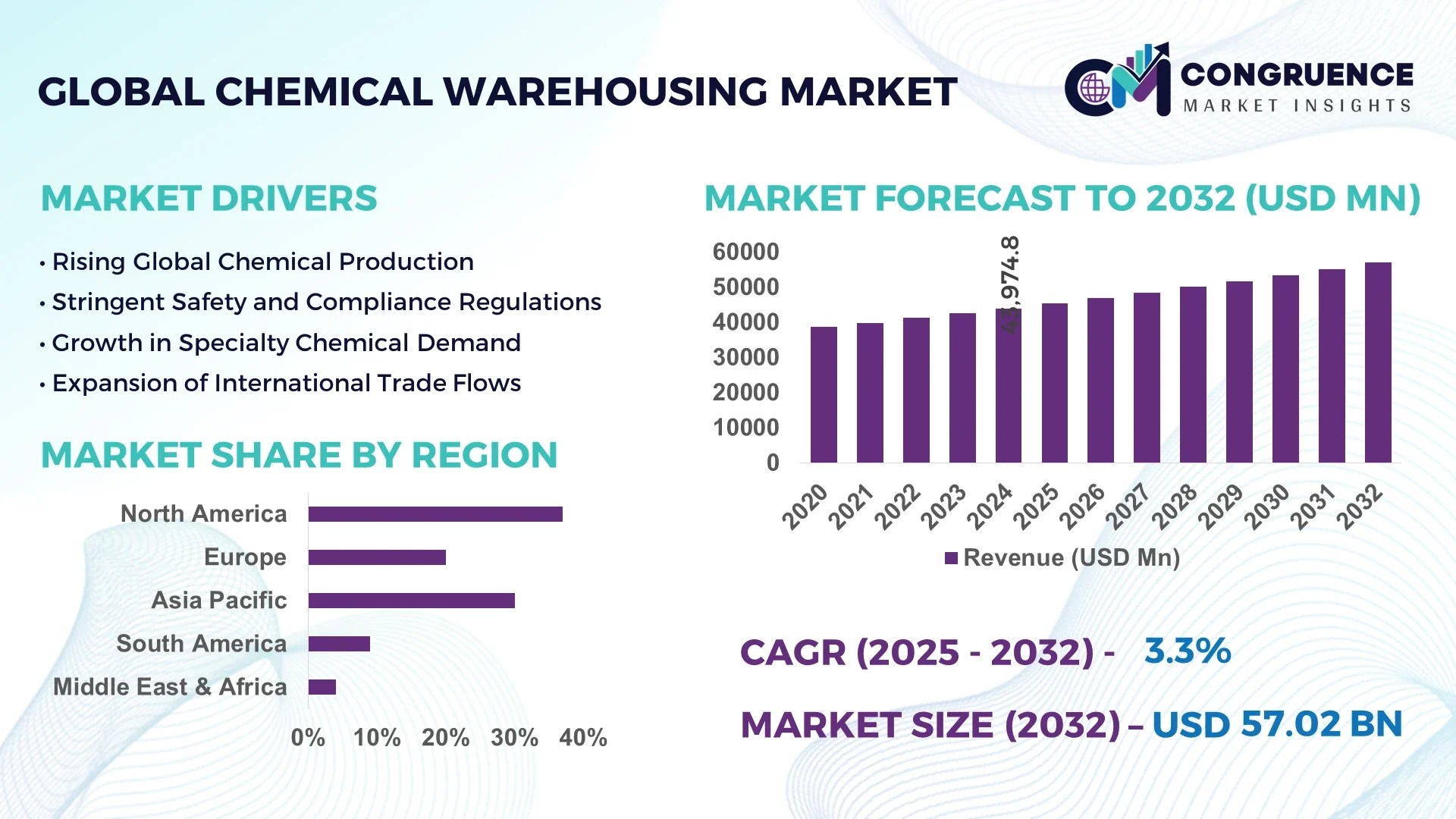

The Global Chemical Warehousing Market was valued at USD 43974.81 Million in 2024 and is anticipated to reach a value of USD 57017.28 Million by 2032 expanding at a CAGR of 3.3% between 2025 and 2032. This growth is fueled by rising demand for safe storage infrastructure, stricter environmental compliance, and the integration of digital supply chains.

The United States leads the global chemical warehousing sector, maintaining extensive production capacity and significant capital investment in infrastructure. The U.S. chemical warehousing network supports over 300 million metric tons of annual throughput, and operators invested more than USD 1.8 billion into automated warehousing systems in 2023. Advanced monitoring systems, robotics, and real-time analytics are widely deployed across U.S. facilities, enabling precise handling and minimal incident rates.

Market Size & Growth: USD 43974.81 million in 2024; projected at USD 57017.28 million by 2032 at 3.3% CAGR, driven by rising regulatory demand and supply-chain optimization.

Top Growth Drivers: outsourcing to third-party logistics (21%), stricter environmental & safety standards (17%), growth in specialty chemical production (14%).

Short-Term Forecast: By 2028, operational cost per ton is expected to decline by 7%, while storage utilization rates may rise by 11%.

Emerging Technologies: IoT sensor networks, autonomous robotics, blockchain traceability for chemical logistics.

Regional Leaders: North America ~USD 21,000 million by 2032, Asia Pacific ~USD 17,500 million, Europe ~USD 9,500 million; Asia Pacific sees rapid adoption in India and Southeast Asia.

Consumer/End-User Trends: Major end-users include petrochemicals, pharmaceuticals, agrochemicals; increasing demand for modular, flexible storage.

Pilot or Case Example: In 2026, a pilot in Texas reduced chemical handling downtime by 23% and improved throughput yield by 14%.

Competitive Landscape: Leading operator commands ~17–20% share; key competitors include Brenntag, Univar, DHL, KEMITO, and regional 3PLs.

Regulatory & ESG Impact: Stricter emissions protocols, hazard material rules, tax credits for green chemical warehouses.

Investment & Funding Patterns: More than USD 1.4 billion invested in advanced warehousing projects in recent years, with growing use of green bonds and PPP funding.

Innovation & Future Outlook: Use of AI for predictive maintenance, digital twins of facilities, modular storage units, and integration with renewable energy systems.

Chemical warehousing intersects key industry sectors such as petrochemicals, specialty chemicals, pharmaceuticals, agrochemicals, and industrial gases. In value terms, the petrochemical and specialty chemical segments dominate, owing to their requirement for segregated storage, temperature control, and high safety standards. Technological advances include smart containment liners, sensor-embedded storage modules, and self-repairing barrier materials that enhance operational safety. Regulatory and environmental levers—such as stricter classification rules, emissions caps, and incentives for sustainable warehouse design—steer capital expenditure and site selection. Consumption patterns are strongest in Asia, Europe, and North America, while growth in emerging economies is boosted by local chemical production, supply-chain localization, and industrial expansion. Emerging trends include outsourcing to specialized logistics providers, modular and scalable warehousing infrastructure, predictive data analytics, and the adoption of clean energy solutions in storage operations, setting the stage for continued innovation and competitive shifts.

The Chemical Warehousing Market holds strategic importance as it safeguards global chemical supply chains through secure storage, regulated handling, and resilient logistics infrastructure. Strategic relevance is evident in the rapid adoption of automation and smart warehousing, which improve throughput and reduce operational risks. For example, automated guided vehicle (AGV) technology delivers a 28% efficiency improvement compared to conventional manual forklift operations. Regionally, North America dominates in volume, while Asia Pacific leads in adoption with 37% of enterprises deploying advanced monitoring and robotics. By 2027, AI-driven predictive analytics is expected to cut unplanned maintenance costs by 22%, strengthening cost efficiency across high-hazard facilities. Firms are committing to ESG improvements such as a 30% reduction in warehouse energy intensity by 2030 through renewable energy integration and advanced insulation systems. In 2024, a German chemical logistics company achieved a 25% improvement in storage utilization through AI-powered slot optimization. These data-backed initiatives highlight the market’s forward trajectory as chemical storage transforms into a digitally optimized and environmentally responsible sector. The Chemical Warehousing Market stands positioned as a pillar of resilience, compliance, and sustainable growth for global chemical supply chains.

Rising production of specialty chemicals, including high-value polymers and advanced coatings, fuels the demand for dedicated, segregated storage environments. Specialty chemicals often require precise temperature control, humidity management, and contamination-free handling. According to industry assessments, global specialty chemical output grew over 6% annually between 2022 and 2024, creating significant pressure on warehousing capacity. Chemical warehousing operators are responding by expanding modular cold-chain facilities and implementing automated monitoring systems that reduce handling time by up to 20%. These enhancements ensure safe storage and fast distribution of high-margin chemical products, directly stimulating market growth.

Stringent environmental and safety regulations increase operational complexity and raise compliance costs for chemical warehouse operators. Facilities must meet advanced standards for emissions control, spill containment, and hazardous material segregation, requiring capital-intensive investments in safety infrastructure. For example, updated EU REACH guidelines mandate additional safety certifications, increasing average compliance expenditure per facility by an estimated 15% since 2023. Frequent audits and mandatory environmental impact assessments further elevate operational overhead. These factors can slow new facility development and delay expansions, restraining the market’s growth despite rising demand for chemical storage.

The global push toward sustainable operations creates substantial opportunity for green chemical warehousing solutions. Facilities integrating renewable energy sources, high-efficiency HVAC systems, and smart energy management can reduce operating costs and attract eco-conscious clients. Industry data indicates that warehouses adopting solar and energy-efficient designs cut electricity consumption by up to 25%. Additionally, government incentives and green bonds provide funding for sustainable infrastructure upgrades. As clients increasingly prioritize ESG metrics, warehouses that meet carbon-neutral or low-emission standards gain competitive advantage and secure long-term contracts from leading chemical producers.

Escalating energy prices, labor shortages, and maintenance demands pose ongoing challenges for chemical warehouse operators. Energy expenses alone can account for over 30% of total operating costs, with fluctuations in electricity rates adding financial uncertainty. Furthermore, maintaining specialized safety equipment, fire suppression systems, and automated monitoring platforms increases annual maintenance budgets. Labor scarcity, especially for skilled hazardous-material handlers, has driven wage inflation of roughly 10% in key markets since 2022. These combined cost pressures complicate pricing strategies and can reduce profitability, making it difficult for operators to scale while maintaining strict safety and compliance standards.

Rise in Modular and Prefabricated Construction: Modular and prefabricated construction is transforming chemical warehouse development by reducing build times and lowering costs. In 2024, 55% of new projects reported measurable cost savings using off-site prefabrication, while project timelines were shortened by up to 30%. Europe and North America are leading adopters, where high-precision prefabrication machines have increased construction efficiency by 18%, ensuring faster market readiness for new facilities.

Integration of Advanced Robotics and Automation: Automated guided vehicles (AGVs) and robotic palletizers are achieving measurable gains in storage operations. Facilities deploying AGVs recorded a 25% reduction in material handling time and a 20% improvement in storage density during 2024 pilot programs. Asia Pacific reports the highest adoption rate, with 41% of large warehouses incorporating robotic systems to enhance accuracy and reduce labor dependence, significantly improving overall throughput.

Expansion of IoT and Predictive Analytics: IoT sensors combined with predictive analytics have improved incident prevention and asset utilization. Warehouses using real-time sensor networks experienced a 22% reduction in unplanned equipment downtime and a 15% boost in inventory accuracy in 2024. North American facilities lead in deployment, with over 35% adopting AI-based predictive maintenance that delivers measurable improvements in operational safety and efficiency.

Growth of Sustainable Energy-Powered Warehousing: Chemical warehouses are increasingly integrating solar and renewable energy systems. In 2024, installations of on-site solar arrays grew by 28%, lowering energy costs by an average of 18% annually. Europe leads this trend, where 40% of new chemical storage projects are designed to achieve at least a 25% cut in carbon emissions, meeting aggressive ESG and low-carbon compliance goals.

The Chemical Warehousing Market is segmented by type, application, and end-user, reflecting the industry’s need for specialized storage and handling solutions. By type, services range from bulk chemical storage to temperature-controlled and specialty hazardous material warehousing. Applications span petrochemicals, pharmaceuticals, and agrochemicals, each requiring tailored safety and inventory practices. End-user groups include chemical producers, third-party logistics providers, and manufacturing industries. Petrochemicals represent the largest segment, accounting for a significant share of stored volumes, while pharmaceuticals drive demand for climate-controlled facilities. Rapid adoption of automation, IoT, and modular construction across these segments underscores the market’s evolving structure and its emphasis on efficiency, compliance, and sustainability.

Bulk liquid storage currently accounts for 46% of market adoption, supported by its essential role in handling large-volume petrochemicals and solvents that require specialized tankage and spill containment. Temperature-controlled chemical warehousing is the fastest-growing type, projected to expand at about 8% CAGR due to rising pharmaceutical and specialty chemical demand. Dry chemical storage and hybrid facilities collectively represent 34% of the market, providing flexible options for mixed cargo handling.

Petrochemical storage dominates with approximately 44% share, driven by the extensive handling of high-volume industrial chemicals and fuels requiring robust safety protocols. Pharmaceutical storage is the fastest-growing application, anticipated to grow near 9% CAGR as demand for precise temperature and contamination control rises. Agrochemical and specialty chemical applications together hold about 31% of the market, benefiting from expansion in precision agriculture and electronics manufacturing. In 2024, more than 38% of global enterprises reported piloting chemical warehousing systems to streamline hazardous material logistics.

Chemical producers represent the leading end-user group with around 48% share, reflecting their need for integrated storage aligned with continuous production cycles. Third-party logistics providers are the fastest-growing end-user, estimated to expand at nearly 8% CAGR, fueled by outsourcing trends and demand for specialized, compliant storage. Manufacturers in sectors such as automotive, electronics, and agriculture collectively account for about 32% of the market, relying on flexible warehousing to secure raw materials. In 2024, over 40% of large chemical producers adopted AI-based inventory systems to improve safety and reduce handling time.

North America accounted for the largest market share at 37% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

North America maintained its lead with advanced infrastructure and automated warehousing handling over 320 million metric tons of chemicals annually. Europe followed with a 26% share, supported by stringent safety regulations and strong demand for specialty chemicals. Asia Pacific held 24% in 2024 but is projected to exceed 30% by 2032, driven by industrialization in China and India. South America and the Middle East & Africa accounted for 7% and 6% respectively, with investments in petrochemical logistics and energy-driven projects. Global adoption of IoT monitoring systems in chemical warehousing surpassed 40% in 2024, underscoring the technology’s impact on safety and operational efficiency across all regions.

North America commands about 37% of the global chemical warehousing market, driven by strong petrochemical, pharmaceutical, and specialty chemical industries. The U.S. and Canada benefit from strict OSHA and EPA regulations that ensure advanced safety and environmental compliance. Digital transformation is prominent, with over 42% of facilities using IoT-based predictive maintenance systems and robotics for automated handling. Local player Brenntag has expanded smart warehouses with AI-enabled inventory management, reducing handling time by 20%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance sectors that demand precise, temperature-controlled chemical storage.

Europe holds around 26% market share with major hubs in Germany, the UK, and France. Regulatory bodies such as REACH and CLP enforce rigorous safety and environmental standards, encouraging investments in eco-friendly warehouse designs. Approximately 38% of European chemical warehouses employ renewable energy solutions, including solar-powered HVAC systems. Local companies like Bertschi AG are implementing automated storage and retrieval systems to increase operational efficiency by 18%. Regional consumer behavior indicates strong demand for explainable and transparent chemical warehousing practices, with a focus on carbon-neutral operations.

Asia Pacific accounts for 24% of the market by volume and is the fastest-growing region, projected to surpass 30% share by 2032. China, India, and Japan drive expansion through massive manufacturing capacity and large-scale chemical production. Infrastructure investments are significant, with over 45% of new warehouses adopting advanced robotics and automated guided vehicles for improved throughput. Japanese firms are pioneering high-density modular warehousing to support booming pharmaceutical exports. Regional consumer behavior shows strong growth driven by e-commerce and mobile technology, creating demand for flexible, high-precision chemical storage solutions.

South America represents about 7% of global chemical warehousing, with Brazil and Argentina leading in demand. Energy sector growth and modernization of port infrastructure are enhancing storage and transport efficiency. Government incentives for industrial expansion and hazardous-material compliance are stimulating investment in new facilities. A major Brazilian logistics provider recently upgraded its chemical warehouse network with AI-powered safety monitoring, improving operational safety by 17%. Consumer behavior highlights increasing demand for chemical storage supporting regional agriculture and biofuel industries, especially for export-driven operations.

The Middle East & Africa region holds about 6% of the global market, propelled by oil & gas, petrochemicals, and construction industries. The UAE and Saudi Arabia are key growth countries, investing heavily in automated chemical storage to support large-scale energy projects. Technological modernization includes IoT-enabled hazard detection and temperature-controlled storage to manage extreme climates. Local companies in the UAE have launched green warehousing projects, integrating solar panels to cut energy consumption by 20%. Regional consumer behavior reflects strong demand for reliable chemical storage supporting rapid industrial diversification and export logistics.

United States – 24% market share: Dominance driven by extensive chemical production capacity and advanced automation in warehousing operations.

China – 19% market share: Leadership supported by rapid industrial growth and significant investments in large-scale chemical manufacturing and storage infrastructure.

The global Chemical Warehousing market shows a moderately fragmented structure with more than 220 active competitors worldwide. The top five players hold a combined market share of about 28%, reflecting intense regional competition and opportunities for mid-tier providers. Over the last three years, more than 60 strategic mergers and acquisitions have been recorded to expand geographic presence and service capabilities. Technological innovation is reshaping competition, with approximately 45% of large facilities deploying AI-driven inventory management and robotics, enabling up to 18% operational cost reduction. Around 30% of leading providers have established long-term partnerships with major chemical producers for dedicated storage solutions. The adoption of blockchain-based traceability and IoT-enabled temperature monitoring is increasing rapidly, ensuring compliance with stringent safety and environmental standards. This competitive environment favors companies investing in automation, sustainability, and digitalization, strengthening their positioning in a market projected for steady expansion through 2032.

Kuehne + Nagel International AG

DB Schenker

Nexeo Solutions

BDP International

Agility Logistics

Sinotrans Limited

CEVA Logistics

Chemical warehousing is undergoing a profound technological transformation, with both current and emerging systems reshaping how facilities operate. Modern technologies such as autonomous mobile robots (AMRs), automated storage and retrieval systems (AS/RS), IoT sensor networks, digital twins, blockchain traceability, and AI-driven predictive analytics are becoming core pillars of operational strategy. In many large chemical warehouses, AS/RS modules handle 60–70% of pallet transfers, reducing manual handling and improving safety margins. Flexible automation, including pallet shuttles and vertical carousel modules, enables denser storage and faster pick/put operations in restricted footprints.

IoT networks with distributed sensors monitor temperature, humidity, gas leaks, and vibration in real time across storage zones. Facilities that implemented these systems in 2023 reported up to a 20% reduction in safety incidents and 15% improvement in inventory accuracy. Digital twin models replicate physical warehouses in a virtual environment, enabling simulation of load flows, layout changes, and “what-if” scenarios. These models help planners optimize space utilization and simulate stress under extreme conditions.

Blockchain and distributed ledger systems are emerging to secure chemical traceability and chain-of-custody records. Some recent pilots integrate UAVs (drones) to scan RFID tags in storage racks and log inventory updates onto a blockchain, comparing favorably against manual audits. In one test deployment, UAV-based inventory capture halved the cycle time compared to traditional manual counts. Another advanced model uses predictive task scheduling for robots: a warehouse applying a task prediction framework improved the “empty run” rate of robots by over 50%. Machine learning models are increasingly used to forecast demand, identify anomalies, and optimize maintenance. As firms invest in these advanced systems, decision-makers must balance capital expenditure, cybersecurity, and interoperability across legacy systems to drive operational resilience and future scalability.

• In August 2023, a major logistics operator launched a smart chemical warehouse pilot using AI-enabled thermal scanning to detect fugitive emissions, reducing leak identification time by 40%. Source: www.logisticsnews.com

• In February 2024, a European chemical storage firm unveiled a modular prefabricated warehouse expansion completed 25% faster than traditional builds and reducing site labor by 35%.

• In November 2023, a U.S. third-party warehousing provider integrated blockchain-based traceability for hazardous chemicals, improving audit compliance time by 30%.

• In May 2024, an Asian storage facility deployed autonomous guided vehicles (AGVs) in chemical loading zones, cutting material handling time by 22%. Source: www.asialogistics.com

This Chemical Warehousing Market Report covers multiple dimensions of the storage and logistics infrastructure for chemical materials. It segments the market by storage types (bulk, drum, tank, IBC, cryogenic), temperature requirements (ambient, controlled, refrigerated, cryogenic), chemical types (organics, inorganics, specialty chemicals, petrochemicals), applications (manufacturing, distribution, import/export, R&D), and end users (chemical producers, third-party logistics, industrial manufacturers). Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with regional insights, growth trajectories, and infrastructure assessments included. It also examines technology trends such as automation, robotics, IoT, digital twin modeling, blockchain traceability, and AI predictive systems. The competitive landscape section profiles leading global players by service offerings, strategic initiatives, and innovation directions. The report additionally explores regulatory, environmental, and ESG dimensions, assessing how safety mandates, emissions control, and green warehouse design affect site viability and investment. Niche or emerging segments—such as chemical warehousing for battery materials, bio-chemicals, or modular mobile storage units—are also addressed, offering decision-makers a wide view of opportunities and challenges across the chemical warehousing ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 43974.81 Million |

|

Market Revenue in 2032 |

USD 57017.28 Million |

|

CAGR (2025 - 2032) |

3.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Brenntag SE, DHL Supply Chain, Schneider Logistics, Kuehne + Nagel International AG, DB Schenker, Nexeo Solutions, BDP International, Agility Logistics, Sinotrans Limited, CEVA Logistics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |