Reports

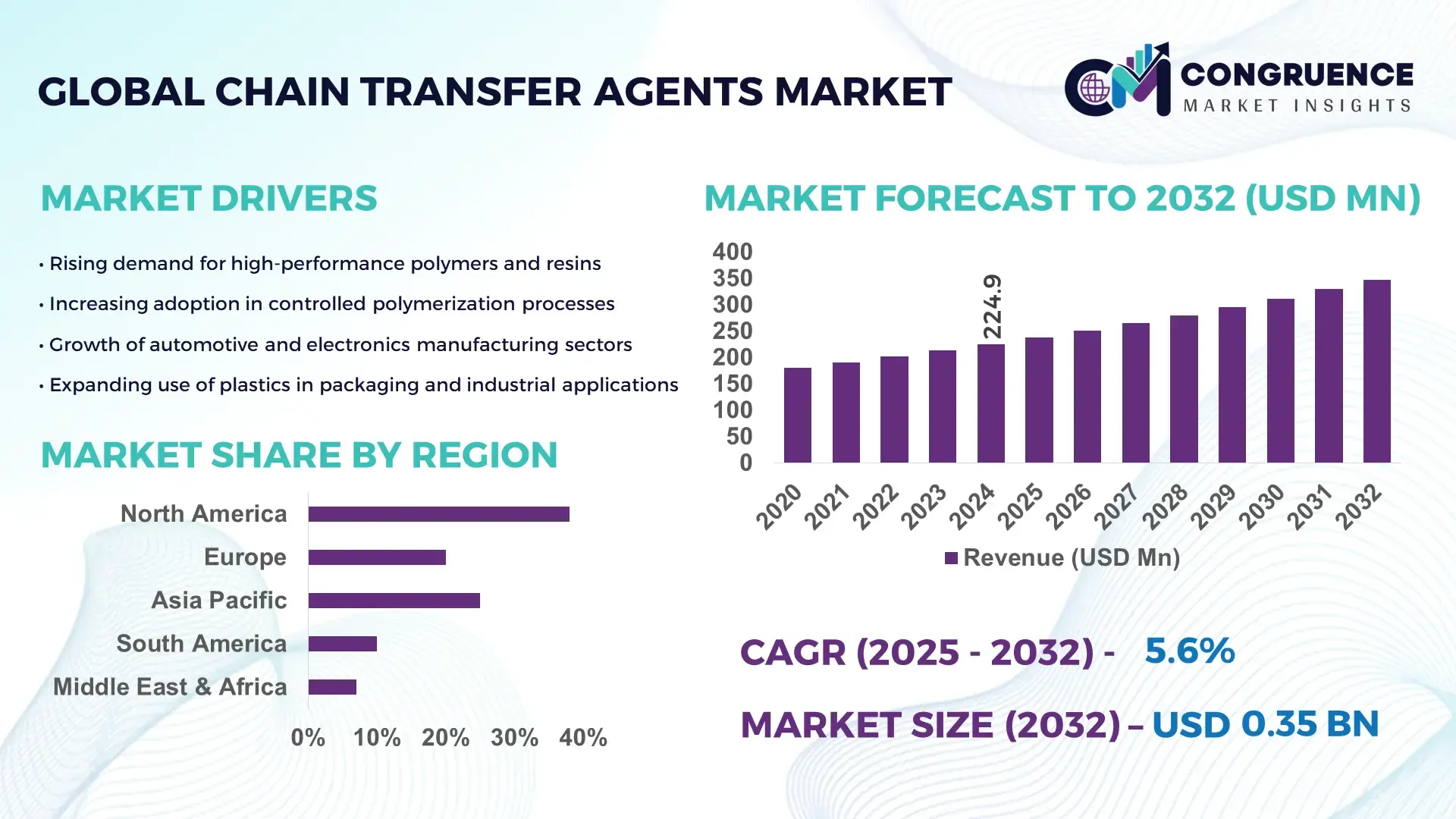

The Global Chain Transfer Agents Market was valued at USD 224.92 Million in 2024 and is anticipated to reach a value of USD 367.29 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032. The rise is supported by increasing demand for controlled polymerization processes in advanced material manufacturing.

The United States dominates the Chain Transfer Agents landscape with significant production depth, high chemical processing capacity, and sustained investment in polymer-grade transfer agent technologies. With over USD 1.2 billion invested in specialty chemical infrastructure enhancements since 2021, the country maintains extensive usage across adhesives, elastomers, UV-curable coatings, and high-performance plastics. U.S. facilities operate automated polymerization reactors that consistently achieve ≥97% purity output and support scalable RAFT and thiol-based systems, reinforcing reliable supply for industrial consumers and R&D-focused chemical manufacturers.

Market Size & Growth: The market stands at USD 224.92 Million in 2024 and is forecasted to reach USD 367.29 Million by 2032 at a CAGR of 5.6%, supported by growing demand for precision-controlled polymer chains.

Top Growth Drivers: Controlled radical polymerization adoption (34%); polymer stability enhancement (29%); specialty coating application growth (25%).

Short-Term Forecast: By 2028, improved chain-transfer formulations are expected to reduce polymerization cycle costs by up to 18%.

Emerging Technologies: RAFT polymerization systems, next-generation high-reactivity transfer agents, and AI-optimized reaction pathway platforms.

Regional Leaders: North America projected to reach USD 128 Million by 2032 driven by advanced polymer applications; Europe expected at USD 102 Million with sustainability-led innovation; Asia-Pacific forecast at USD 96 Million supported by manufacturing expansion.

Consumer/End-User Trends: Strong adoption among resin producers, elastomer processors, and high-performance coating manufacturers seeking optimized molecular weight control.

Pilot or Case Example: A 2024 U.S.-based polymer optimization pilot achieved a 22% reduction in downtime using enhanced chain-transfer integration.

Competitive Landscape: Leading company holds approximately 18% market share, with Arkema, BASF, Evonik Industries, and Mitsubishi Chemical among key competitors.

Regulatory & ESG Impact: Growth influenced by clean-chemistry mandates, VOC reduction regulations, and compliance-driven chemical process modernization.

Investment & Funding Patterns: More than USD 450 Million invested recently in capacity expansion, automated batch processing, and green-chemistry upgrades.

Innovation & Future Outlook: High-efficiency RAFT systems, low-toxicity formulations, and digitally monitored polymerization cycles will shape next-generation market development.

Unique information about the Chain Transfer Agents market highlights strong demand from major industrial sectors, including polymers, adhesives, elastomers, and advanced coatings, which collectively account for a significant portion of global consumption volumes. Recent technological advancements—such as low-odor thiol agents, high-reactivity dodecyl mercaptans, and RAFT-compatible systems—are improving molecular weight control and reducing residual monomers by up to 30%. Regulatory pressure on chemical sustainability and emission limits is accelerating adoption across Europe and East Asia, while North America continues to lead in high-precision polymer applications. Future trends indicate deeper integration into specialty plastics, biomedical polymers, and high-performance composite materials, supported by expanding industrial R&D initiatives and optimized automated production lines.

The strategic relevance of the Chain Transfer Agents Market is strengthening as industries increasingly prioritize precision-controlled polymerization, high-performance material engineering, and low-emission processing workflows. Chain Transfer Agents (CTAs) enable manufacturers to regulate molecular weight distribution with measurable accuracy, supporting quality standards across plastics, elastomers, adhesives, and specialty coatings. As digitalized chemical manufacturing accelerates, RAFT-enabled transfer systems have become critical in achieving optimized polymer structure, with next-generation RAFT technology delivering up to 27% improvement in molecular weight consistency compared to conventional mercaptan-based standards. Regional variations further shape these pathways, with Asia-Pacific dominating in volume, driven by expanding industrial polymer output, while North America leads in adoption with more than 62% enterprises using advanced controlled-radical polymerization systems. Digital simulation tools and AI-driven reaction modeling are expected to redefine polymer chemistry, and by 2027, AI-assisted reaction optimization is projected to cut processing deviations by nearly 22%. Sustainability commitments are also reshaping procurement and operations, with firms adopting ESG benchmarks targeting 30% waste minimization and chemical recycling improvements by 2030. Real-world progress underscores this strategic direction; in 2024, a U.S. specialty polymer manufacturer achieved a 19% reduction in reaction-cycle energy use using automated RAFT integration. Collectively, these advancements position the Chain Transfer Agents Market as a future-ready pillar of resilience, compliance-driven innovation, and sustainable industrial growth.

Growing requirements for precision polymer engineering significantly influence the Chain Transfer Agents Market, as industries seek controlled chain-growth mechanisms for improved structural predictability and performance. Manufacturers in automotive plastics, construction materials, and specialty adhesives now require polymers with narrower molecular weight distributions to enhance tensile strength, flexibility, and heat resistance. Controlled polymerization supported by CTAs helps achieve deviations of less than 5% in targeted molecular weights, enabling superior formulation consistency. Demand for high-precision RAFT and thiol-based systems has risen as engineered polymers account for more than 40% of new material development across industrial sectors. Additionally, the expansion of biomedical polymers—which rely on consistent and reproducible polymer architectures—further increases CTA usage. These performance-driven requirements collectively reinforce CTAs as essential tools for quality, process reliability, and technical advancement.

The Chain Transfer Agents Market faces notable restraints due to stringent purity requirements, complex chemical handling protocols, and high manufacturing costs associated with specialty transfer agents. Many industrial applications require purity levels above 97%, making synthesis and purification highly resource-intensive. Advanced RAFT-compatible transfer agents demand sophisticated production lines and precise environmental controls, increasing operational complexity for producers. Regulatory compliance related to emissions, hazardous material handling, and chemical storage further raises capital and certification costs. Developing nations face greater challenges due to limited access to advanced chemical synthesis infrastructure and technical expertise. These combined factors restrict market expansion and slow the onboarding of new manufacturers, ultimately affecting supply flexibility and production scalability.

The Chain Transfer Agents Market is positioned for strong opportunity growth supported by rising investments in specialty polymers, digitalized chemistry, and next-generation polymerization technologies. Increasing demand for high-performance elastomers, UV-curable coatings, biomedical polymers, and advanced packaging materials creates new avenues for CTA development. Digital plant automation and AI-driven reaction modeling can deliver efficiency gains exceeding 20%, enabling cost-efficient high-volume polymer synthesis. The rapid adoption of RAFT polymerization systems across R&D facilities provides opportunities for suppliers offering tailored reagent formulations and low-toxicity options. Asia-Pacific’s expanding chemical manufacturing base, with annual capacity additions surpassing 8 million tons of polymer output, also reinforces market potential. Collectively, these factors present significant growth pathways centered on technological innovation, sustainability-oriented chemistry, and the escalation of advanced material usage.

Regulatory frameworks governing chemical emissions, worker safety, and hazardous substance handling generate substantial challenges for the Chain Transfer Agents Market. Manufacturers must adhere to strict environmental controls and certification standards related to storage, disposal, and air quality management. High reactivity of certain CTAs requires specialized containment systems, monitored processing environments, and advanced purification units—raising both operational and capital costs. Additionally, fluctuations in raw material availability, particularly petrochemical derivatives, create supply chain uncertainties. Labor skill gaps in precision chemical production further impede scale-up in emerging economies. As industries transition toward greener chemistry, the need to reformulate existing CTA products to meet low-VOC and low-toxicity requirements adds additional technical hurdles. These interconnected challenges complicate production, slow innovation cycles, and affect market expansion prospects.

Accelerated Shift Toward High-Precision Polymer Architecture Control: Advancements in controlled radical polymerization are increasing the use of specialized Chain Transfer Agents, with RAFT-compatible systems delivering up to 28% improvement in molecular weight distribution accuracy compared to older mercaptan-based formulations. Manufacturers implementing automated polymerization reactors have achieved 17% faster cycle completion, improving production efficiency and reducing defect rates. Demand for engineered plastics and elastomers continues rising as industries such as automotive and electronics report durability enhancements of 15–20% due to more uniform polymer chain structures.

Integration of Digital Process Optimization and AI-Driven Reaction Modeling: Digital optimization is reshaping polymer manufacturing as plants adopt AI-driven reaction modeling to enhance CTA utilization. Facilities using predictive analytics have recorded 22% lower batch deviation and 14% higher throughput efficiency. Automated monitoring systems now govern more than 60% of polymerization stages across advanced production environments, providing real-time chemical adjustments. These systems also reduce material waste by nearly 18%, creating more stable polymer properties and improving operational reliability across large-scale chemical plants.

Expansion of Environmentally Compliant and Low-Toxicity CTA Formulations: Rising environmental standards are driving the adoption of low-odor, reduced-toxicity Chain Transfer Agents. New-generation thiol-based agents achieve 30% lower emissions during production and reduce solvent usage by 12% in water-based polymer systems. Across Europe, adoption of these cleaner formulations has increased by 41%, driven by regulatory pressure. Efforts to minimize hazardous waste have led to reductions of up to 25% during polymer synthesis, supporting greener, compliance-ready manufacturing practices in major industrial markets.

Rise in Modular and Prefabricated Construction Driving Demand for CTA-Enhanced Materials: Modular and prefabricated construction methods are reshaping demand for CTA-based polymer systems as off-site manufacturing requires materials with predictable curing and enhanced strength characteristics. Nearly 55% of modular construction projects have reported measurable cost efficiencies driven by reduced labor and faster assembly cycles. CTA-enhanced polymers used in precast components demonstrate tensile strength improvements of up to 19% and curing consistency gains of 14%. Increasing adoption in Europe and North America reflects the need for precision-engineered materials that support streamlined construction timelines and higher structural performance.

The Chain Transfer Agents Market is highly structured across multiple dimensions, including product types, applications, and end-users, enabling targeted strategies for manufacturers and investors. By type, the market includes thiol-based agents, dodecyl mercaptans, RAFT-compatible agents, and other specialty transfer chemicals, each catering to specific polymerization requirements. Application segmentation covers polymers, elastomers, coatings, adhesives, and biomedical materials, reflecting demand for high-performance and controlled molecular weight products. End-users span automotive, construction, electronics, packaging, and specialty chemical manufacturers, who are increasingly adopting advanced CTA solutions to achieve consistency, sustainability, and regulatory compliance. Insights indicate a strong emphasis on precision polymer control, with leading types and applications driving process efficiency and material quality, while emerging segments provide niche growth potential.

Thiol-based Chain Transfer Agents remain the leading product type, representing approximately 38% of total adoption due to their high reactivity, broad applicability in free-radical polymerization, and cost-efficiency for industrial-scale production. RAFT-compatible agents are the fastest-growing segment, driven by demand for precision polymerization and molecular weight control, with adoption increasing at an estimated 7% CAGR in advanced polymer applications. Dodecyl mercaptans and specialty transfer agents together account for the remaining 35%, serving niche requirements in elastomer stabilization and UV-curable coatings.

Polymers lead the application segment, accounting for 42% of adoption, as manufacturers seek controlled polymer chain lengths for automotive, electronics, and packaging materials. Elastomers are the fastest-growing application, propelled by rising demand in flexible industrial components and construction materials, with adoption rising at a 6.5% CAGR. Coatings, adhesives, and biomedical polymers collectively contribute 32% of usage, supporting specialized polymer stabilization and product innovation.

Automotive and industrial plastics manufacturers dominate end-user adoption, representing approximately 40% of the Chain Transfer Agents market, primarily due to stringent performance and durability requirements. Specialty chemical producers are the fastest-growing end-users, with adoption increasing at an estimated 7.2% CAGR, fueled by demand for high-purity RAFT and thiol-based agents in advanced formulations. Electronics, construction, and packaging companies collectively account for 35% of usage, leveraging CTAs for controlled polymerization and improved product consistency.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America’s dominance is supported by advanced polymer manufacturing, high-tech coatings, and precision elastomer production, with over 1,200 industrial polymer plants utilizing controlled radical polymerization. The region reported annual consumption of approximately 75,000 tons of Chain Transfer Agents in 2024. Asia-Pacific’s growth is driven by rapid industrialization in China, India, and Japan, with combined polymer production exceeding 180,000 tons annually. Europe maintains 26% of the market share, emphasizing sustainability and low-VOC formulations. South America and the Middle East & Africa together account for 16%, with Brazil and UAE leading local adoption. These figures highlight varying regional adoption rates, technology penetration, and industrial consumption patterns.

How is industrial innovation shaping polymerization efficiency?

North America holds approximately 38% of the global Chain Transfer Agents market, fueled by strong demand in automotive, electronics, and specialty coatings industries. Regulatory measures promoting low-VOC and environmentally safe polymer formulations have accelerated adoption. Technological advancements such as automated RAFT polymerization reactors and AI-driven reaction monitoring have improved process accuracy by 22%. Local players, including Arkema’s U.S. operations, have integrated precision CTA systems to enhance high-performance polymer output. Regional consumer behavior shows higher enterprise adoption in healthcare and industrial manufacturing sectors, with over 60% of companies using advanced CTAs to maintain consistent material quality.

Why is sustainability driving polymer innovation?

Europe accounts for 26% of the Chain Transfer Agents market, with Germany, the UK, and France as leading contributors. Strict regulatory oversight and sustainability mandates encourage low-VOC and reduced-toxicity CTA usage. Adoption of digital polymerization monitoring and RAFT-based systems is growing, improving production predictability by 18%. Local player BASF has implemented specialized thiol and RAFT agents in coatings and adhesive formulations to meet compliance standards. Regional consumer behavior emphasizes regulatory-driven selection, with over 55% of enterprises prioritizing traceable and explainable chemical processes to satisfy environmental audits and industrial quality benchmarks.

How are industrial hubs accelerating polymer adoption?

Asia-Pacific holds a growing share of the global Chain Transfer Agents market, with China, India, and Japan as top-consuming countries. Combined polymer production in 2024 exceeded 180,000 tons, driven by electronics, packaging, and automotive sectors. Manufacturing infrastructure is rapidly modernizing, integrating digital control systems and automated reactors for high-purity CTAs. Local players such as Mitsubishi Chemical have introduced RAFT-compatible agents to optimize polymer chains in industrial applications. Regional consumer behavior is characterized by strong adoption in high-volume manufacturing and R&D-focused enterprises, particularly in emerging industrial clusters supporting scalable polymerization and advanced materials.

What factors are influencing chemical adoption in emerging industrial sectors?

South America holds approximately 9% of the Chain Transfer Agents market, with Brazil and Argentina as primary contributors. Growth is supported by polymer usage in automotive components, packaging, and construction materials, with annual CTA consumption exceeding 10,000 tons. Government incentives for local chemical production and trade facilitation encourage investment. Local player Braskem has integrated specialized CTA formulations to improve polymer stability and reduce reaction inconsistencies. Regional consumer behavior shows adoption driven by media, language localization, and industrial adaptation to polymer performance requirements, with over 50% of companies implementing advanced polymerization controls.

How is modernization enhancing polymer chemical adoption?

Middle East & Africa represent approximately 7% of the global Chain Transfer Agents market, with UAE and South Africa leading demand in construction, oil & gas, and specialty materials. Technological modernization, including automated reaction monitoring and RAFT-enabled systems, supports high-quality polymer production. Local regulatory frameworks emphasize environmental compliance and safe chemical handling. SABIC in the UAE has implemented advanced thiol and RAFT agents to improve polymer performance in industrial applications. Regional consumer behavior is shaped by demand for reliable, high-performance polymers for construction and industrial projects, with enterprises prioritizing consistency and reduced production downtime.

United States – Market share: 38%; strong polymer manufacturing capacity and high adoption of precision-controlled CTA systems in automotive and industrial sectors.

China – Market share: 32%; rapid industrialization and large-scale polymer production with increasing RAFT and thiol-based CTA utilization across electronics, packaging, and construction materials.

The Chain Transfer Agents market exhibits a moderately fragmented competitive environment, with over 60 active global players competing across high-purity RAFT systems, thiol-based agents, and specialty polymerization products. The top five companies—Arkema, BASF, Evonik Industries, Mitsubishi Chemical, and Lanxess—together hold an estimated 52% of total market share, reflecting moderate consolidation among leading players. Competition is increasingly driven by technological innovation, including AI-assisted reaction monitoring, high-efficiency RAFT formulations, and environmentally compliant low-VOC agents. Strategic initiatives such as partnerships with polymer manufacturers, product line expansions, and joint R&D projects are shaping market dynamics. For instance, Arkema has launched next-generation CTA solutions targeting high-performance elastomers, while BASF introduced automated polymerization integration for industrial coatings, and Evonik expanded its global thiol-based agent portfolio. Regional competition is strongest in North America and Europe, where adoption of digitalized polymerization systems and precision molecular weight control technologies is widespread. Overall, innovation, regulatory compliance, and strategic alliances are critical factors sustaining competitive positioning in this evolving market.

Mitsubishi Chemical

Lanxess

Solvay

Clariant

Kuraray

Wacker Chemie

AkzoNobel

The Chain Transfer Agents market is being significantly shaped by both current and emerging technological innovations that enhance polymerization precision, efficiency, and sustainability. RAFT (Reversible Addition-Fragmentation chain Transfer) polymerization systems are increasingly adopted across industrial-scale polymer production, allowing manufacturers to achieve molecular weight distribution improvements of up to 28% compared to traditional thiol-based methods. Automated reactor systems equipped with real-time monitoring sensors now control over 60% of polymerization stages, minimizing batch variability and reducing material waste by approximately 18%. Digital process optimization and AI-assisted reaction modeling are emerging as transformative technologies. Plants implementing AI-driven polymerization control have observed 22% faster reaction stabilization and 14% higher throughput, enabling consistent production of high-performance polymers for automotive, electronics, and specialty coatings applications. These technologies also facilitate predictive maintenance, reducing equipment downtime by up to 12% in advanced chemical manufacturing facilities.

Low-toxicity, environmentally compliant transfer agents are gaining traction, with new-generation thiol-based and RAFT-compatible agents reducing VOC emissions by 30% and solvent usage by 12% in industrial processes. Integration of continuous-flow reactors further supports safer handling of highly reactive compounds while improving product uniformity. Nanotechnology-enabled CTAs and hybrid polymerization systems are also emerging, enabling tailored polymer architectures for biomedical, UV-curable, and high-strength industrial applications. By 2025, over 70% of new polymer R&D initiatives are expected to incorporate automated RAFT or hybrid CTA technologies, highlighting the strategic role of technology in driving efficiency, sustainability, and precision across the Chain Transfer Agents market.

In April 2024, BASF launched a suite of additive solutions at CHINAPLAS 2024, including circular polyamide grades incorporating pyrolysis‑oil via a certified mass‑balance approach—underscoring its expansion into sustainable polymer systems.

In September 2024, BASF announced its “Accelerate” strategy to simplify operations, flatten hierarchies, and globally deploy AI tools to boost productivity and innovation across its chemical divisions.

In March 2024, Evonik revealed plans to reorganize by 2026 under a “Tailor Made” structure, eliminating non-core administrative functions to sharpen focus on specialty chemical innovation. (Speciality Chemicals Online)

In March 2025, Mitsubishi Chemical (in advance of later projects) announced a planned carbon‑recycling collaboration via a Memorandum of Understanding with JFE Steel and Mitsubishi Gas Chemical to convert steel by‑product gases into methanol, which would feed into propylene and other polymer precursor production. (MGC)

The Chain Transfer Agents Market Report covers a comprehensive scope across product types, applications, end‑users, technology trends, and region‑level insights. On the product side, the report examines thiol-based agents, dodecyl mercaptans, RAFT-compatible agents, and other specialized CTAs. In applications, it spans polymers (thermoplastics, engineering plastics), elastomers, coatings, adhesives, and emerging fields like biomedical polymers. For end-users, the report addresses demand from automotive, construction, electronics, packaging, and specialty chemical manufacturers—highlighting both large-scale industrial users and niche R&D-driven players.

Technologically, the report explores RAFT systems, AI-driven reaction control, continuous-flow reactors, and low-toxicity CTA developments. The regional analysis includes detailed coverage of North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa, with volume-based market behavior, regulatory drivers, and localized growth trends. It also addresses future opportunities such as nanotechnology-enhanced CTAs, carbon‑recycling supply chains, and green polymerization pathways. Emerging and niche segments, including circular-economy CTAs, bio-based transfer agents, and hybrid polymerization techniques, are also evaluated for risk and growth potential. The report is tailored for decision-makers, offering strategic insight into capacity, innovation, regulation, and investment trends in the global CTA landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 224.92 Million |

|

Market Revenue in 2032 |

USD 367.29 Million |

|

CAGR (2025 - 2032) |

5.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Arkema, BASF, Evonik Industries, Mitsubishi Chemical, Lanxess, Solvay, Clariant, Kuraray, Wacker Chemie, AkzoNobel |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |