Reports

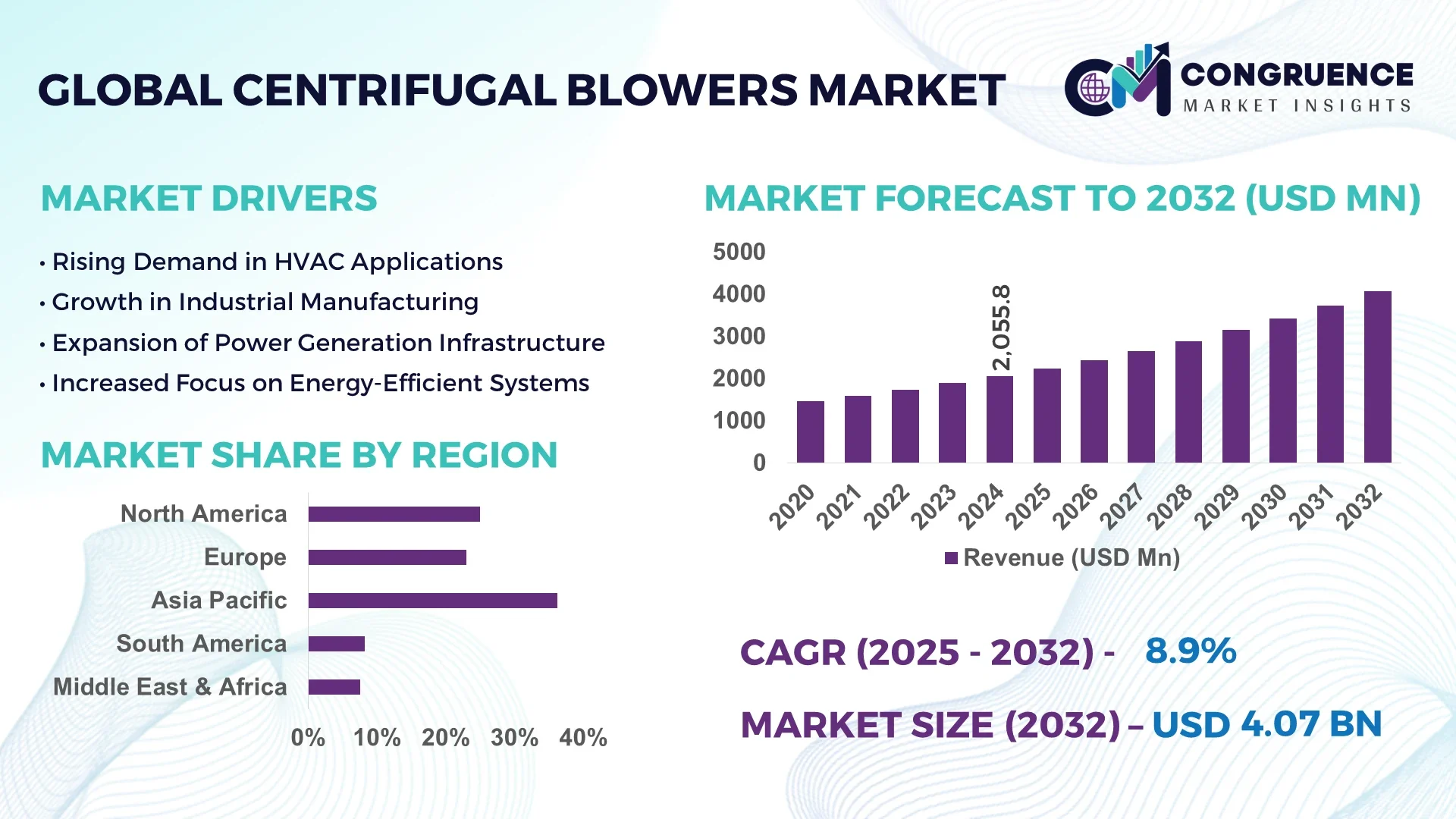

The Global Centrifugal Blowers Market was valued at USD 2055.75 Million in 2024 and is anticipated to reach a value of USD 4066.26 Million by 2032 expanding at a CAGR of 8.9% between 2025 and 2032.

The United States dominates the centrifugal blowers market, leading in both production capacity and demand for advanced industrial ventilation solutions. This dominance is supported by significant investments in HVAC systems, manufacturing industries, and pollution control technologies that extensively use centrifugal blowers.

Globally, the centrifugal blowers market is driven by escalating industrialization and the expanding demand for efficient air handling systems across sectors such as power generation, chemical processing, and wastewater treatment. In 2024, the industrial sector accounted for over 40% of the total market share, reflecting robust usage in manufacturing plants and energy facilities. Technological advancements in blower design, including energy-efficient motors and aerodynamically optimized impellers, have improved performance metrics like airflow and pressure generation. Additionally, stringent environmental regulations have increased the adoption of centrifugal blowers in pollution control and exhaust systems. Asia-Pacific accounts for approximately 35% of global consumption, with rapid urbanization fueling demand for commercial HVAC systems that incorporate centrifugal blowers. Overall, market dynamics emphasize product innovation, growing infrastructure projects, and replacement demand as critical factors shaping the global centrifugal blowers industry.

Artificial Intelligence (AI) is rapidly revolutionizing the centrifugal blowers market by enhancing operational efficiency, predictive maintenance, and system optimization. Advanced AI algorithms analyze real-time performance data from centrifugal blowers to detect anomalies and predict potential failures before they occur, reducing downtime and maintenance costs. Smart sensors integrated with AI enable continuous monitoring of vibration, temperature, and airflow parameters, allowing operators to optimize blower performance dynamically according to changing environmental or process conditions.

AI-driven automation in centrifugal blowers is also facilitating energy savings by adjusting motor speeds and airflow based on demand patterns. For example, machine learning models can fine-tune blower operations in HVAC systems, improving energy efficiency without compromising airflow requirements. The integration of AI with Industrial Internet of Things (IIoT) platforms allows centralized control and remote diagnostics of centrifugal blowers, improving operational transparency across industrial sites. Moreover, AI-powered design software assists engineers in optimizing blower components for aerodynamic efficiency and noise reduction, accelerating the development cycle and reducing prototyping costs. These technological advances are not limited to new installations; retrofitting existing centrifugal blower units with AI-based control systems is increasingly common, further driving market growth. In 2024 alone, over 30% of centrifugal blower manufacturers have adopted AI-enabled condition monitoring solutions, demonstrating widespread industry acceptance. Overall, AI is setting new benchmarks for reliability, energy efficiency, and smart automation within the centrifugal blowers market, transforming traditional systems into intelligent, self-optimizing units.

"In early 2024, a leading centrifugal blower manufacturer launched an AI-integrated blower monitoring platform that reduced unplanned downtime by 25% and enhanced predictive maintenance accuracy by over 40%, marking a significant advancement in operational reliability."

Centrifugal blowers are crucial in wastewater treatment processes for aeration and odor control. In 2024, wastewater treatment facilities accounted for nearly 20% of the global centrifugal blower installations. With urban populations growing and environmental standards tightening, there is heightened demand for efficient, high-capacity blowers that support biological treatment stages. Governments across Europe and Asia have launched over 120 major wastewater infrastructure upgrades, emphasizing energy-efficient aeration systems. Modern centrifugal blowers, offering reduced noise levels and superior oxygen transfer efficiency, are rapidly replacing older units. These advancements are enabling lower energy consumption and improved treatment outcomes, making centrifugal blowers indispensable in both municipal and industrial wastewater facilities.

Despite their benefits, traditional centrifugal blowers often suffer from high power consumption, especially in continuous-use environments like cement plants and steel mills. In 2024, analysis showed that older centrifugal blower units consumed up to 30% more energy compared to modern energy-efficient models. This inefficiency makes them less attractive for energy-conscious sectors and small to mid-sized enterprises with limited budgets. Furthermore, the initial capital cost of upgrading to high-efficiency or variable-speed blower systems can be prohibitive. These challenges, combined with rising electricity prices in major industrial economies, are acting as a barrier to widespread centrifugal blower deployment in cost-sensitive regions.

The rising global consumption of packaged and processed food is driving investment in hygienic air movement systems, where centrifugal blowers are vital. In 2024, food and beverage processing plants accounted for approximately 15% of centrifugal blower demand, with increasing usage in drying, cooling, and dust extraction processes. Compliance with sanitary standards such as FDA and EU food safety regulations necessitates the use of stainless steel centrifugal blowers with non-contaminating design features. Moreover, innovations in easy-to-clean, corrosion-resistant materials are expanding their adoption. As food manufacturers expand production lines and automation, the need for precise airflow control makes centrifugal blowers a preferred choice in processing environments.

Growing awareness of occupational health and increasing enforcement of noise pollution laws are pressuring manufacturers to reduce acoustic emissions from centrifugal blowers. In 2024, regulatory agencies in North America and Europe introduced more stringent decibel limits for industrial equipment, pushing companies to invest in noise-dampening technologies. However, integrating these features significantly raises product development and production costs. Additionally, retrofitting older industrial setups with sound-attenuated blower systems is often complex and expensive, limiting adoption. As a result, companies face challenges in balancing regulatory compliance with affordability and operational performance, especially in densely populated urban and suburban industrial zones.

• Integration of Variable Frequency Drives (VFDs): The increasing focus on energy efficiency across industrial sectors is driving the adoption of centrifugal blowers equipped with Variable Frequency Drives (VFDs). These VFDs allow for dynamic airflow control based on real-time system demands, significantly reducing energy wastage. In 2024, over 45% of newly installed centrifugal blowers in industrial plants featured VFD compatibility. Industries such as petrochemicals, pharmaceuticals, and power generation are transitioning to VFD-integrated systems to lower operational costs and meet stringent emission standards. This trend is further supported by government incentives encouraging the use of energy-saving equipment in manufacturing.

• Growing Preference for Oil-Free Centrifugal Blowers: There is a noticeable shift toward oil-free centrifugal blowers in industries requiring contamination-free air, such as food processing, electronics manufacturing, and cleanroom operations. In 2024, demand for oil-free blower systems grew by nearly 30%, with manufacturers introducing advanced, lubricant-free models that reduce the risk of air contamination. These systems not only support compliance with international cleanliness regulations but also reduce maintenance downtime, a critical requirement in 24/7 operational environments. This trend is especially pronounced in North America and East Asia, where hygiene and air purity standards are particularly stringent.

• Rising Use of Composite and Lightweight Materials: To enhance energy efficiency and reduce installation complexity, manufacturers are increasingly using composite and lightweight materials in centrifugal blower design. In 2024, about 35% of newly developed models incorporated composite impellers and lightweight casings, reducing equipment weight by up to 20%. These design improvements simplify transportation and lower structural support requirements, making them ideal for retrofit applications and compact facilities. The chemical and cement industries, in particular, are adopting lightweight centrifugal blowers for space-restricted environments where traditional units are not viable.

• Smart Monitoring and Predictive Maintenance Technologies: Digital transformation in manufacturing is boosting demand for smart centrifugal blowers integrated with sensors and IoT connectivity. These systems enable real-time condition monitoring, predictive maintenance alerts, and remote diagnostics, improving system reliability and extending operational life. In 2024, nearly 40% of centrifugal blower manufacturers offered models embedded with smart diagnostic tools. The integration of cloud-based platforms also allows operators to track performance metrics and energy usage remotely. This trend is gaining traction in Europe and the Asia-Pacific region, where smart factory initiatives and Industry 4.0 frameworks are being rapidly adopted.

The centrifugal blowers market is segmented based on type, application, and end-user, with each segment offering distinct growth opportunities and performance benchmarks. Among the segments, backward-curved and radial blowers are witnessing high demand due to their superior energy efficiency and space-saving designs. Application-wise, usage in HVAC systems and wastewater treatment dominates the market, reflecting global trends in infrastructure and environmental management. From an end-user perspective, industrial manufacturing remains the largest consumer, followed by the power generation and food processing sectors. These segmentation categories help manufacturers and stakeholders tailor products and strategies to meet industry-specific demands and accelerate deployment in emerging markets.

Centrifugal blowers are categorized into radial, forward-curved, backward-curved, and airfoil types. In 2024, backward-curved centrifugal blowers held the largest market share, accounting for nearly 37% of the global volume, due to their high static efficiency and low noise output, making them ideal for industrial HVAC systems and cleanroom environments. Radial blowers followed closely, gaining preference in abrasive environments such as cement and steel manufacturing due to their robust design and ability to handle particulate-laden air. Forward-curved blowers are typically used in compact systems like home HVACs and electronic cooling, while airfoil types, though niche, are gaining ground in specialized energy recovery and turbine applications. The fastest-growing segment is the backward-curved blowers, with demand surging particularly in Asia-Pacific and Europe, where efficiency regulations and green building standards are more stringent. Their balance between performance, maintenance, and energy use is driving wider adoption across several industrial applications.

The centrifugal blowers market sees applications across various domains, including HVAC systems, wastewater treatment, industrial ventilation, chemical processing, and power plants. In 2024, HVAC systems emerged as the dominant application segment, representing over 30% of market share globally, driven by rising construction activities, increased focus on indoor air quality, and rapid urbanization. Wastewater treatment applications are growing rapidly as governments invest in sustainable infrastructure and water management systems, particularly in Asia-Pacific and the Middle East. Industrial ventilation remains critical for operations in heavy industries such as metalworking, food processing, and textiles. Chemical processing and power generation also contribute significantly, especially where corrosive environments demand durable blower systems. Wastewater treatment is expected to be the fastest-growing segment through 2032 due to regulatory pressures on pollution control and growing public sector investments in municipal infrastructure. This application growth is supported by rising environmental awareness and the integration of advanced blower systems into treatment facilities.

Key end-user segments in the centrifugal blowers market include industrial manufacturing, commercial facilities, energy and utilities, food and beverage processing, and pharmaceuticals. In 2024, industrial manufacturing accounted for over 40% of total demand, with consistent usage in metal fabrication, cement, pulp and paper, and chemical sectors. The commercial segment, comprising office buildings, malls, and institutional infrastructure, is gaining traction with growing HVAC needs driven by urbanization. The energy and utilities segment utilizes blowers in turbine operations, coal handling, and emissions control, making it a critical yet stable market. The food and beverage sector leverages oil-free centrifugal blowers for hygienic operations, while pharmaceutical industries rely on them for dust-free cleanroom environments. Among these, the fastest-growing end-user segment is pharmaceuticals, supported by the global expansion of clean manufacturing facilities and stringent regulatory environments requiring contaminant-free air systems. The shift toward smart factories and sterile production environments is accelerating the adoption of high-efficiency centrifugal blowers in pharmaceutical applications.

Asia-Pacific accounted for the largest market share at 36.2% in 2024, however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

The Asia-Pacific region benefits from rapid industrialization, increasing urban infrastructure projects, and strong demand in countries like China, India, and Japan. This region's leadership in cement, steel, and electronics manufacturing drives centrifugal blower consumption. North America follows with a significant share of 28.4%, driven by HVAC modernization and environmental regulations. Europe held 21.6% of the market share in 2024, with sustainability trends accelerating adoption in wastewater treatment. Meanwhile, the Middle East & Africa market, despite a smaller base of 6.8%, is projected to expand rapidly due to oil and gas investments and growing construction activity. South America contributed 7% in 2024, with Brazil and Argentina fueling industrial demand. These figures highlight varying regional maturity levels and emerging opportunities across sectors.

"Driven by HVAC Upgrades and Industrial Modernization"

The North American centrifugal blowers market is witnessing steady growth owing to increased spending on energy-efficient HVAC systems and industrial process upgrades. In 2024, North America held 28.4% of the global market share, with the U.S. accounting for more than 70% of the regional demand. The adoption of centrifugal blowers is high in commercial construction, oil & gas refineries, and municipal wastewater treatment facilities. Retrofitting projects in existing industrial plants are also driving replacement demand. Additionally, regulatory mandates on air quality and energy efficiency are boosting deployment across government and healthcare buildings. Canada’s mining and metallurgy industries are further contributing to the regional uptake of radial and backward-curved blowers. The rising popularity of digital monitoring systems and smart blower technology among industrial users is enhancing product performance and energy savings, which continues to shape the future trajectory of centrifugal blowers in the region.

"Anchored by Environmental and Energy Efficiency Regulations"

Europe’s centrifugal blowers market remains robust, with the region contributing 21.6% to global market share in 2024. Countries such as Germany, France, Italy, and the UK are leading adopters due to strict environmental and air-quality regulations. Wastewater treatment, cleanroom applications, and industrial drying systems are key verticals where centrifugal blowers are widely used. Germany represents the largest market within the region, accounting for over 30% of Europe’s total demand, especially from the chemical and pharmaceutical sectors. Energy recovery systems integrated with blowers are gaining popularity as European industries push for carbon-neutral operations. The European Union’s investment in green infrastructure and circular economy initiatives is directly influencing centrifugal blower demand. Additionally, manufacturers are increasingly focusing on compact, low-noise, and high-efficiency blowers to comply with stringent building codes, making Europe a key innovation hub for centrifugal blower technologies.

"Dominated by Infrastructure and Manufacturing Boom"

Asia-Pacific dominated the global centrifugal blowers market with a share of 36.2% in 2024, driven by rapid urbanization and industrial growth across China, India, and Southeast Asia. China alone contributed over 48% of the regional market share, largely fueled by expansive infrastructure projects, cement and steel industries, and environmental treatment plants. India followed as a high-growth market, with increasing adoption in pharmaceuticals, textiles, and power generation sectors. Japan and South Korea also exhibited strong demand for advanced centrifugal blowers in electronics manufacturing and precision engineering. Government-led smart city missions and clean air initiatives are amplifying the need for efficient ventilation and air handling systems. Additionally, the competitive landscape in Asia-Pacific has intensified with local players offering cost-effective solutions, spurring innovations in lightweight materials, impeller designs, and motor technologies tailored to regional industry needs.

"Fuelled by Industrial Expansion in Brazil and Argentina"

South America accounted for 7% of the global centrifugal blowers market in 2024, with Brazil and Argentina leading regional consumption. The demand is driven by process industries such as food & beverage, cement, pulp and paper, and bioethanol production. Brazil alone contributed nearly 55% of the regional market, benefiting from industrial automation projects and energy recovery systems. Argentina is experiencing increased investment in chemical and plastic manufacturing, which requires high-performance air movement solutions. Additionally, the rise in urban construction and wastewater management in mid-sized cities is contributing to market growth. Despite some macroeconomic challenges, public and private sector investments in infrastructure and sustainable energy are supporting centrifugal blower adoption. The presence of localized manufacturing facilities and growing emphasis on energy efficiency standards are shaping future procurement strategies for industries across the continent.

"Gaining Traction from Oil & Gas and Infrastructure Projects"

The Middle East & Africa (MEA) region represented 6.8% of the global centrifugal blowers market in 2024 but is poised for the fastest growth by 2032. Saudi Arabia, the UAE, and South Africa are the leading contributors to regional demand. In the Middle East, centrifugal blowers are increasingly utilized in petrochemical complexes, oil refineries, and district cooling systems. Saudi Arabia held the largest share in MEA, at over 40%, driven by mega-projects under the Vision 2030 initiative. The UAE’s urban development and water recycling initiatives are further expanding blower usage. Meanwhile, in Africa, the focus on improving sanitation infrastructure, particularly in Nigeria and Kenya, is fostering centrifugal blower installations in wastewater treatment facilities. The region’s shift toward renewable energy and large-scale industrial zones is creating a positive outlook for technologically advanced and energy-efficient blowers, especially those integrated with remote monitoring and control systems.

China: 17.4% – Due to its dominant manufacturing sector, large-scale infrastructure projects, and extensive use of centrifugal blowers in cement, steel, and power plants.

United States: 15.2% – Owing to widespread applications in HVAC, water treatment, petrochemicals, and energy-efficient industrial systems.

The centrifugal blowers market is characterized by a competitive landscape marked by both global giants and region-specific manufacturers catering to diverse industrial needs. Leading companies are emphasizing product innovation, energy efficiency, and low-noise solutions to maintain competitive differentiation. In 2024, over 60% of the market share was captured by the top 10 players, indicating moderate market consolidation. Strategic mergers and acquisitions are on the rise, particularly among players looking to expand regional reach and diversify application portfolios. For instance, manufacturers are investing heavily in compact blower designs with integrated variable frequency drives (VFDs), which are gaining popularity in HVAC and industrial drying sectors. Meanwhile, regional players in Asia-Pacific are focusing on cost-effective models to compete with established Western brands. Additionally, partnerships with government and private organizations in wastewater treatment and renewable energy are creating growth platforms for mid-sized players. The presence of strong aftermarket service networks is another crucial differentiator in securing long-term contracts and customer loyalty.

Howden Group

Atlas Copco AB

Ingersoll Rand

Hitachi Industrial Equipment Systems Co., Ltd.

Gardner Denver

Cincinnati Fan

Shandong Zhangqiu Blower Co., Ltd.

Greenheck Fan Corporation

AERZEN Maschinenfabrik GmbH

Kaeser Kompressoren SE

Tuthill Corporation

Elektror airsystems gmbh

Manrose Manufacturing Ltd.

Technological innovation in the centrifugal blowers market is transforming the performance, energy efficiency, and application versatility of these industrial components. One of the key developments is the integration of variable frequency drives (VFDs), allowing real-time speed control to match airflow demands and reduce energy consumption. Over 40% of newly installed centrifugal blowers in 2024 included VFDs, highlighting this trend's momentum. Another significant advancement is the rise of high-efficiency impeller designs, including backward-inclined and airfoil blades that improve airflow while reducing noise and mechanical losses.

Material innovation is also gaining attention. The use of composite materials and corrosion-resistant alloys has enabled longer operational life in chemically aggressive environments, such as wastewater treatment and chemical processing. Furthermore, manufacturers are incorporating smart sensor systems for predictive maintenance, vibration monitoring, and remote diagnostics. These systems are being adopted in sectors like oil & gas, where downtime is costly.

Noise reduction technologies, such as acoustic insulation and aerodynamic casing designs, are becoming standard, particularly in commercial HVAC applications. Additionally, digital twin and simulation-based engineering are being employed to optimize blower design before physical prototyping. These technologies are pushing the market toward greater efficiency, reliability, and sustainability across all industrial sectors.

In January 2024, Siemens introduced the "SirioVent SSi" series of centrifugal blowers integrated with variable speed drives (VSDs). This innovation allows for precise control of airflow based on specific application needs, optimizing energy consumption and reducing operational costs.

In March 2024, Ebm-Papst unveiled its "RadiCal" impeller blades featuring a backward-curved design. These blades optimize airflow and minimize energy losses, contributing to enhanced energy efficiency in centrifugal blower applications.

In May 2024, Howden launched centrifugal blowers with impellers optimized using Computational Fluid Dynamics (CFD). This advancement enables detailed analysis of airflow patterns within the blower, allowing for designs that minimize energy losses and maximize efficiency.

In June 2024, ABB introduced a range of centrifugal blowers integrated with their variable speed drives. These blowers offer improved efficiency and controllability, providing complete drive-motor-blower packages tailored for specific industrial applications.

The Centrifugal Blowers Market Report offers a comprehensive evaluation of the global market, focusing on key trends, growth drivers, restraints, and emerging opportunities across industrial sectors. The scope of this report includes in-depth segmentation analysis by type, application, and end-user, offering granular insights into market behavior and product demand. Types such as multistage, single-stage, and high-pressure blowers are assessed for their roles across diverse applications including air handling, gas extraction, material conveying, and cooling systems. The report highlights the significant adoption of single-stage centrifugal blowers due to their compact design, energy efficiency, and ease of installation in manufacturing, water treatment, and HVAC applications.

The market's geographic scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing country-level demand with detailed insights into top-performing and fastest-growing regions. End-users such as chemical, power generation, mining, food & beverage, and wastewater treatment industries are deeply examined, showcasing trends in modernization, automation, and environmental regulation compliance. The report also emphasizes advancements in technology, including smart sensors, energy-efficient motors, and variable frequency drives, which are reshaping centrifugal blower efficiency and reliability. This market report is intended to support decision-making for manufacturers, investors, policymakers, and technology developers by providing actionable intelligence on current and future market conditions globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2055.75 Million |

|

Market Revenue in 2032 |

USD 4066.26 Million |

|

CAGR (2025 - 2032) |

8.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Howden Group, Atlas Copco AB, Ingersoll Rand, Hitachi Industrial Equipment Systems Co., Ltd., Gardner Denver, Cincinnati Fan, Shandong Zhangqiu Blower Co., Ltd., Greenheck Fan Corporation, AERZEN Maschinenfabrik GmbH, Kaeser Kompressoren SE, Tuthill Corporation, Elektror airsystems gmbh, Manrose Manufacturing Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |