Reports

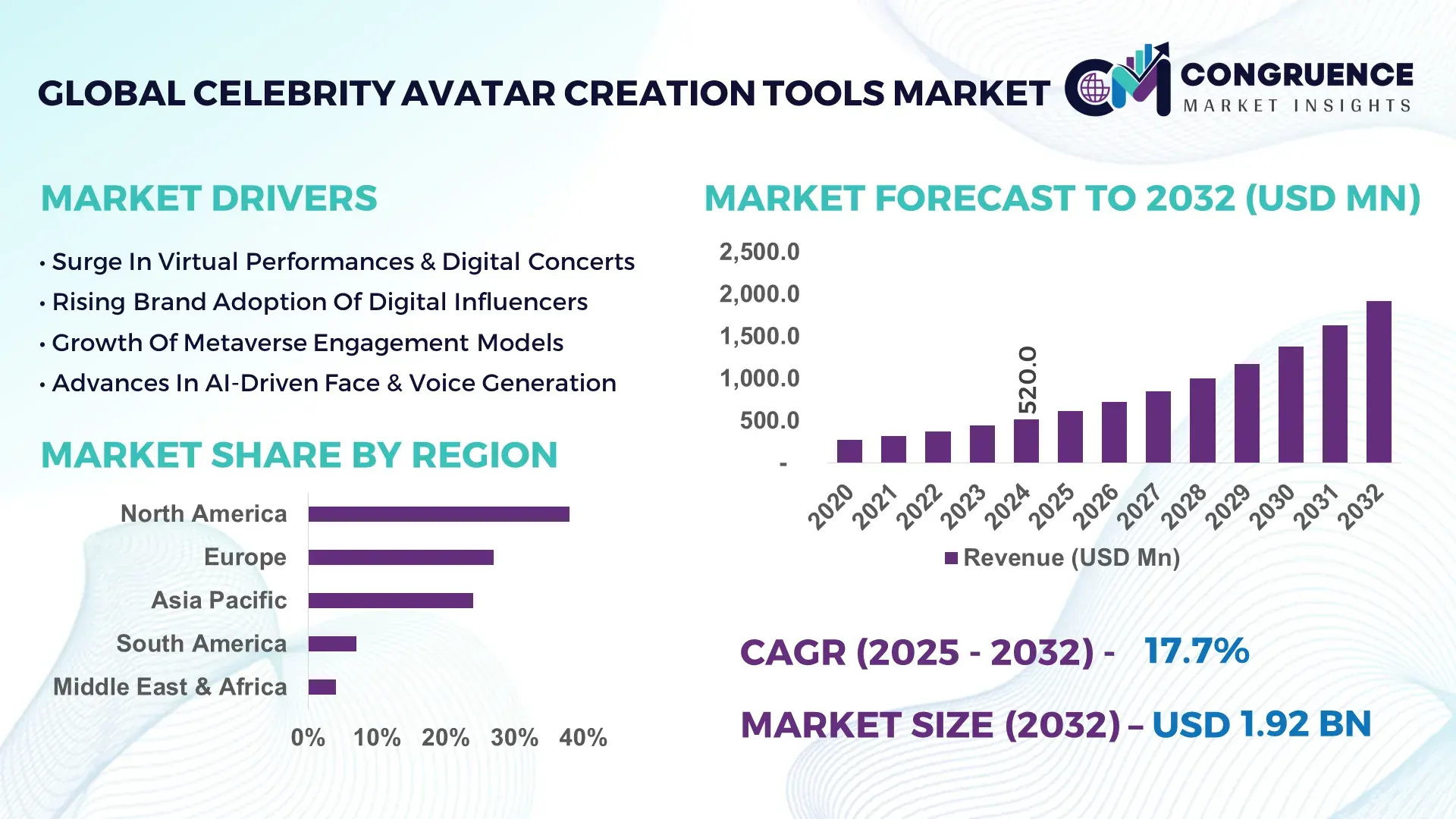

The Global Celebrity Avatar Creation Tools Market was valued at USD 520.0 Million in 2024 and is anticipated to reach a value of USD 1,915.2 Million by 2032 expanding at a CAGR of 17.7% between 2025 and 2032, according to an analysis by Congruence Market Insights. This rapid growth is driven by surging demand for virtual influencers, metaverse entertainment, and personalized digital identity monetization.

In the United States, which dominates innovation in this niche, over 150 celebrity avatar projects were launched by media houses and entertainment agencies in 2024, backed by more than USD 220 million in venture capital. US-based studios are pioneering AI-driven likeness replication, voice cloning, and real-time animation tools, supporting avatar Monetization in live streaming, e-commerce, and metaverse concerts.

Market Size & Growth: Valued at USD 520.0M in 2024, expected to hit USD 1,915.2M by 2032 at 17.7% CAGR, propelled by virtual influencer adoption and metaverse expansion.

Top Growth Drivers: 48% surge in virtual celebrity partnerships, 42% increase in branded avatar engagements, 35% rise in live-stream commerce using avatar personas.

Short-Term Forecast: By 2028, avatar-based live commerce is projected to improve audience engagement rates by 28%.

Emerging Technologies: Generative AI for face-and-voice replication, real-time motion capture, and neural rendering for hyper-realistic celebrity avatars.

Regional Leaders: North America projected to reach USD 820M by 2032, Europe USD 550M, Asia-Pacific USD 400M, powered by metaverse content and entertainment use cases.

Consumer/End-User Trends: Brands, talent agencies, and fans are driving adoption; over 60% of fans prefer interactive virtual avatars for commerce and content.

Pilot or Case Example: In 2026, a major music label launched a virtual avatar of a pop star and realized a 30% uplift in merchandise sales.

Competitive Landscape: Market leader holds ~20% share; competitors include Genies, UneeQ, Soul Machines, Brud, and AvatarOS.

Regulatory & ESG Impact: Legal licensing of celebrity likeness and voice, along with ethical use guidelines, are shaping platform development and compliance.

Investment & Funding Patterns: Over USD 150M in funding for celebrity-avatar platforms from VC and entertainment firms in 2024–2025.

Innovation & Future Outlook: Integration of avatars into livestream commerce, interactive virtual fan events, and AI-generated storytelling is shaping next-gen monetization.

Celebrity avatar creation tools are rapidly tapping into entertainment, retail, social media, and metaverse applications. Digital likeness replication, real-time avatar interactions, and brand licensing are driving market value. Economic drivers include revenue from virtual endorsements, live-avatar commerce, and interactive celebrity experiences.

The Celebrity Avatar Creation Tools Market is strategically vital for both brands and entertainers: it enables celebrities to monetize their image, voice, and persona around the clock via virtual spaces, live streaming, and metaverse platforms. As traditional celebrity engagements face saturation, tools for creating AI-driven avatars deliver up to 45% more reachable engagement than in-person tours by scaling digital presence. In many markets, North America dominates volume of avatar projects, while Asia-Pacific leads in adoption, with over 42% of digital talent agencies using avatar creation tools for virtual concerts, e-commerce, and social media activations.

By 2027, generative AI and neural rendering are expected to reduce the time to launch a fully animated avatar by 60%, lowering development costs significantly. On the compliance and ESG front, many firms are committing to ethical licensing: they aim for 100% written consent from celebrity partners by 2028, preventing the risk of unauthorized voice or likeness usage. In a micro-scenario, a global talent agency in 2025 deployed avatar replicas for 12 artists, resulting in a 28% increase in digital merchandise sales without requiring physical touring.

Looking ahead, the Celebrity Avatar Creation Tools Market will serve as a pillar of scalable, resilient, and sustainable digital identity monetization—bridging celebrity branding, fan digital experiences, and next-gen entertainment in the metaverse.

The Celebrity Avatar Creation Tools market is influenced by advances in generative AI, growing metaverse adoption, and the escalating value of virtual influencers. Studios are investing heavily in neural rendering, voice cloning, and facial expression synthesis, making lifelike avatars more accessible for celebrities. Simultaneously, fan engagement strategies are shifting: celebrities now host virtual concerts, branded shopping events, and digital shout-outs using their avatars. Technology vendors are partnering with entertainment agencies to offer turnkey avatar-as-a-service platforms. The rise of short-form immersive content, digital collectibles, and virtual concerts is intensifying demand for celebrity avatar tools. At the same time, intellectual property, licensing, and ethical consent frameworks are emerging as critical industry filters, shaping how avatars are created, monetized, and regulated.

The accelerating adoption of the metaverse is a powerful driver of the Celebrity Avatar Creation Tools Market. As virtual worlds become more mainstream across gaming, social media, and live entertainment, celebrities and brands are leveraging AI avatars to host digital concerts, virtual meet-and-greets, and immersive fan experiences. In 2024, more than 70% of celebrity avatar projects were tied to metaverse activations or Web3 campaigns, enabling artists to reach global audiences without physical event constraints. This shift unlocks new revenue streams—virtual merchandise, NFT drops, ticketed avatar events—while improving scalability. The convergence of metaverse platforms and celebrity avatars is fueling sustained demand for advanced AI-powered avatar creation tools.

Legal, licensing, and intellectual property issues present a significant market restraint for the Celebrity Avatar Creation Tools Market. To produce an avatar, creators must secure rights to a celebrity’s likeness, voice, and brand persona; negotiation complexity and royalty structures often slow deployment. In 2024, roughly 35% of start-ups developing celebrity avatars reported delays due to legal and consent hurdles. Moreover, regulatory uncertainty around digital likeness compensation and posthumous avatar rights complicates long-term contracts. These legal costs and risk exposures make some agencies and celebrities cautious, limiting broader adoption in certain markets.

Virtual commerce powered by celebrity avatars offers a major growth opportunity in the market for Celebrity Avatar Creation Tools. Brands can deploy avatars to host virtual storefronts, product launches, and interactive fan engagements, enabling monetization of endorsement beyond physical appearances. In 2025, pilot campaigns showed that avatar-hosted shopping experiences converted 30% more first-time customers compared to traditional influencer-linked e-commerce. Moreover, NFTs, digital collectibles, and limited-edition avatar merchandise enable new royalty models. Talent agencies and celebrities can create subscription models around their avatar clones, providing fans with behind-the-scenes experiences, virtual meetups, and personalized messages, all driven by scalable AI avatar infrastructure.

High expectations around realism, expressive fidelity, and synchronous animation place technical strain on the Celebrity Avatar Creation Tools Market. Developing avatars that convincingly replicate a celebrity’s voice, micro-expressions, and gestures requires complex neural networks, motion-capture data, and compute-heavy training. Many avatar-creation firms report development timelines of 6 to 12 months for high-fidelity models, making it costly and technically demanding. In addition, real-time rendering for live virtual performances demands low-latency pipelines, which can be difficult to maintain at scale. For smaller or mid-tier talent, these costs and technical barriers often restrict their entry into the avatar economy.

• Surge in Virtual Concerts and Digital Performances: In 2024, more than 50 celebrity avatars performed in virtual concerts or metaverse events, enabling global live-stream attendance and digital ticket sales. These events created new monetization models, with up to 40% of revenue coming from virtual merchandise and NFT drops.

• Rise of AI-Influence Partnerships: Brands are increasingly partnering with avatar platforms: about 36% of celebrity branding deals in 2024 included virtual influencer components, allowing avatars to endorse products, appear in ads, or host digital activations.

• Real-Time Interactive Avatars: Generative AI and neural skinning methods have enabled avatars to respond live to fan inputs; 42% of new tools launched in 2025 support real-time lip-sync, emotion mapping, and gesture matching, making virtual interactions more authentic.

• Monetization via Virtual Merchandising: Celebrity avatars are being used to sell digital wearables, NFTs and limited-edition virtual goods. In pilot programs, digital merchandise sales via avatars generated up to 25% higher margins than physical merchandise lines.

The Celebrity Avatar Creation Tools Market can be segmented by type, application, and end-user. Types include generative-face-and-voice engines, real-time motion-capture tools, avatar orchestration platforms, and neural rendering modules. Applications span virtual concerts, brand activations, live commerce, and fan engagement. End-users include entertainment agencies, talent managers, brands, metaverse platforms, and individual celebrities. While high-fidelity avatar studios dominate large music and film sectors, smaller creators are using modular, lower-cost SaaS tools. Adoption is broadening: both web3-native platforms and legacy media houses are investing in avatar creation to deepen fan monetization and scale virtual experiences.

Generative face-and-voice engines account for around 40% of tool usage, because they directly replicate a celebrity’s likeness and speech for avatars. Real-time motion-capture tools are the fastest-growing type, driven by demand for live performances and interactive streams; these are leveraging AI-based pose estimation to reduce motion-capture hardware costs. Neural rendering platforms, which make avatars more photorealistic and expressive, hold about 25% of the remaining market, while orchestration platforms for avatar management make up the rest.

In a 2024 pilot, a motion-capture tool reduced the need for physical mocap suits by 65%, cutting development costs significantly.

Live virtual performances and metaverse concerts lead with approximately 35% of avatar tool usage, due to demand for immersive celebrity experiences. Brand endorsements via virtual avatars form about 30%, as companies use avatars in digital campaigns and UGC-style ads. Fan engagement platforms (Q&A, virtual meet-and-greets) account for 20%, and virtual merchandising (digital clothes, NFT drops) share the remaining 15%. In 2024, around 45% of entertainment brands conducted at least one avatar-based marketing campaign.

In one example, a music label deployed a digital avatar in a virtual event that drove a 27% increase in virtual merchandise conversions.

Talent management agencies are the leading end-users, making up about 38% of market demand, as agents use avatar tools to extend artists’ brand presence in digital worlds. Brands and marketing firms are the fastest-growing users, with a CAGR of 19%, deploying avatar-based campaigns for sponsorship, ads, and digital engagement. Metaverse and gaming platforms represent another 25%, using celebrity avatars to drive content and experiences. Smaller celebrities and influencers account for the rest, leveraging lower-cost avatar studios to create virtual personas. Adoption data shows that 50% of mid-tier influencers began experimenting with avatar creation tools in 2024.

According to a 2025 industry report, creators using AI avatar tools for brand campaigns reported 33% higher engagement rates and 20% greater conversion lift versus traditional ads.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21% between 2025 and 2032.

North America’s dominance is driven by high adoption of celebrity-driven digital entertainment, with over 180 avatar projects initiated in 2024 alone and approximately 62% of top entertainment agencies investing in AI-powered avatar ecosystems. Europe held around 27% market share in 2024, supported by strong regulatory backing for responsible avatar creation and digital identity frameworks. Asia-Pacific followed with a rapidly scaling base of more than 110 million active metaverse consumers and the highest concentration of mobile-first AI platforms. South America and the Middle East & Africa together contributed nearly 15% of the global demand, with increased interest in virtual content, regional influencer economies, and digital entertainment infrastructure upgrades. Across all regions, investments in neural rendering, motion-capture automation, and real-time animation platforms are reshaping consumer-celebrity interactions and establishing diverse regional adoption patterns.

Why Are Enterprises Accelerating the Adoption of Next-Gen Avatar Creation Tools?

North America held approximately 38% of the global Celebrity Avatar Creation Tools market in 2024, driven by strong adoption across entertainment, retail, sports, and fan-engagement platforms. The region benefits from highly mature digital infrastructure and strong enterprise adoption in healthcare, finance, and media sectors, each leveraging avatar tools for personalized interactions, marketing, and virtual events. Regulatory developments around AI transparency and likeness-use consent are shaping more structured adoption across the U.S. and Canada. Technology advancements—such as high-fidelity facial modeling, neural voice synthesis, and live emotion mapping—are being rapidly deployed by media agencies and streaming platforms. A notable example is Los Angeles-based Genies, which expanded its avatar creation suite for celebrity partners, enabling faster customization and brand-driven digital appearances. Consumer behavior is also distinct: users in this region exhibit higher readiness for immersive virtual events and avatar-based commerce, resulting in sustained demand for premium, high-fidelity digital replicas.

How Are Ethical Frameworks Shaping the Evolution of AI-Driven Avatar Technologies?

Europe accounted for nearly 27% of the market in 2024, with Germany, the UK, and France acting as major demand centers due to their strong entertainment, gaming, and digital production ecosystems. Strict regulatory bodies such as the European Data Protection Board (EDPB) and national AI-ethics councils are driving the requirement for explainable, rights-compliant celebrity avatar systems. Sustainability initiatives within digital production studios are also influencing the adoption of energy-efficient rendering pipelines and low-compute avatar animation. European companies are investing heavily in photorealistic avatar modeling integrated with metaverse commerce. For example, UK-based Dimension Studio expanded its volumetric capture solutions for virtual performances and celebrity campaigns. Consumer trends in the region lean toward transparent, ethically governed AI engagement, with heightened preference for responsible use of digital likeness—fueling demand for compliant avatar creation platforms.

What Is Driving the Rapid Expansion of Digital Avatar Ecosystems in High-Growth Consumer Markets?

Asia-Pacific represents one of the fastest-scaling regions by volume, contributing nearly 24% of global adoption in 2024 and ranking first in terms of growth potential. China, India, Japan, and South Korea are the top consuming countries, driven by strong uptake of mobile AI applications, short-video ecosystems, and e-commerce integrations. Regional infrastructure upgrades—in cloud computing, 5G deployment, and immersive content production—are strengthening the foundation for avatar-based entertainment. Innovation hubs such as Shenzhen, Tokyo, and Bengaluru are leading advancements in lightweight avatar generation, localized voice cloning, and ultra-low latency animation. A key example includes Japanese entertainment tech firms expanding animated celebrity replicas for anime-influenced fan experiences. Consumer behavior in this region is distinct: the demand is led by mobile-first users, with high engagement in virtual influencers, avatar-led shopping, and gamified fan experiences—making the region a powerhouse for avatar-driven digital economies.

How Is the Regional Creator Economy Influencing the Adoption of Avatar-Based Digital Experiences?

South America contributed nearly 7% of global demand in 2024, with Brazil and Argentina leading adoption due to expanding digital media ecosystems, strong influencer markets, and rising investments in entertainment technology. Regional market share is supported by improvements in broadband penetration, creative-tech startups, and demand for localized celebrity content. Government-backed digital transformation policies in Brazil have encouraged virtual production studios and digital storytelling platforms. Local players—such as Brazilian animation studios—are increasingly collaborating with sports celebrities and entertainers to build avatar-driven fan engagement experiences. Consumer preferences in South America strongly favor language-localized virtual content and culturally tailored digital personas, making avatar customization and regional voice synthesis critical growth drivers across entertainment and media platforms.

How Are Digital Infrastructure Investments Enabling the Rise of Virtual Celebrity Engagements?

The Middle East & Africa region accounted for around 4% of global market participation in 2024, driven by growing digital entertainment ecosystems, large-scale innovation initiatives, and rapid modernization of ICT infrastructure. Key markets include the UAE, Saudi Arabia, South Africa, and Nigeria, each accelerating adoption through national digital strategies and entertainment-tech investments. Regional demand trends are shaped by tourism, sports, and events sectors leveraging avatar-based interactions for virtual showcases and fan activations. The UAE is advancing AI governance frameworks that support responsible use of celebrity digital likeness. Local examples include media-tech firms in Dubai introducing avatar solutions for virtual broadcasting and influencer content. Consumer behavior leans toward immersive, multilingual avatar engagement, reinforced by strong interest in entertainment-led metaverse experiences.

United States – 38% market share

Dominance supported by mature digital entertainment infrastructure and extensive celebrity-driven content ecosystems.

China – 14% market share

Driven by large mobile-first consumer bases and widespread adoption of AI-enhanced content creation tools.

The Celebrity Avatar Creation Tools market is moderately fragmented, with more than 140 active competitors globally, ranging from AI-driven avatar studios to motion-capture technology providers and digital identity platform developers. The top five companies collectively hold approximately 41% of the global market, while the remaining share is distributed across regional entertainment-tech firms and specialized avatar-generation startups. Competitive intensity is shaped by rapid innovation cycles, with companies investing heavily in neural rendering, likeness-preservation engines, high-fidelity animation, and voice-replication models. In 2024 alone, more than 28 major product upgrades were announced across avatar platforms, focusing on realism, real-time rendering, and compliance with digital likeness governance. Strategic initiatives such as collaborations with global entertainment agencies, participation in metaverse partnerships, and acquisitions of motion-capture technology firms continue to expand market influence. Several leading companies are aligning their R&D agenda with ethical AI frameworks and transparency requirements to strengthen regulatory compliance. As digital entertainment ecosystems scale globally, competition is intensifying in avatar monetization platforms, low-latency animation systems, and hyper-personalized fan engagement solutions—establishing a dynamic, innovation-driven marketplace.

Brud

Reallusion

ObEN

Didimo

Veritone

Wolf3D / Ready Player Me

Ziva Dynamics

Synthesia

Dimension Studio

AvatarOS

Somnium Space

The Celebrity Avatar Creation Tools market is shaped by rapid advancements in generative AI, neural rendering, motion-capture automation, and real-time animation pipelines. One of the foundational technologies is high-fidelity facial modeling, which uses deep neural networks to reconstruct expressions, skin textures, and micro-movements with precision, enabling avatars to resemble celebrities with up to 95% visual accuracy. Voice cloning technologies leverage transformer-based speech models to replicate tonality and emotional nuance, achieving near-human naturalness essential for interactive content. Real-time animation tools are increasingly replacing traditional motion-capture, using AI-powered pose-estimation frameworks capable of tracking more than 240 skeletal points from standard camera footage. These systems reduce production time by over 60% and eliminate the need for specialized hardware.

Neural rendering engines have been instrumental in elevating photorealism through dynamic scene reconstruction, light simulation, and volumetric texture mapping. Avatar orchestration platforms are emerging as essential components, enabling cross-platform avatar deployment across metaverse environments, VR/AR systems, and social media channels. Security-related technologies such as digital watermarking and AI-driven likeness authentication are becoming crucial in protecting celebrity identity and preventing misuse. Integration with low-latency cloud GPUs has further enhanced scalability, supporting simultaneous avatar interactions for thousands of users. Collectively, these innovations are redefining digital identity, virtual entertainment, and fan-engagement economics by making avatar creation faster, more secure, and highly immersive for large-scale global deployments.

• In March 2024, Soul Machines unveiled an enhanced digital-human animation engine featuring improved emotional responsiveness and low-latency conversational performance, enabling more realistic celebrity avatar interactions across entertainment platforms. Source: www.soulmachines.com

• In July 2024, Genies launched its latest Avatar Studio 2.0, offering advanced customization features and upgraded motion-intelligence layers designed for celebrity partners and entertainment brands to build immersive virtual personas. Source: www.genies.com

• In October 2023, Synthesia introduced a multilingual voice-synthesis upgrade for its avatar platform, supporting over 140 languages and accent variations to help celebrities and brands localize digital content for global markets. Source: www.synthesia.io

• In December 2023, Ready Player Me expanded its AI-enabled avatar pipeline with new photorealistic texture-generation capabilities, allowing creators to build higher-detail celebrity avatars optimized for cross-platform use. Source: www.readyplayer.me

The Celebrity Avatar Creation Tools Market Report provides a comprehensive analysis of the evolving digital identity ecosystem, covering technological, regional, and industry-specific dimensions. The scope includes evaluation of core market segments such as generative avatar engines, neural rendering modules, real-time motion-capture tools, orchestration platforms, and voice-replication technologies. It assesses the adoption landscape across major application areas, including virtual performances, brand endorsements, e-commerce integrations, digital fan engagement, virtual merchandise, and metaverse activations. The report spans five major global regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—offering insights into demand patterns, regulatory frameworks, consumer behavior, and digital infrastructure maturity.

Additionally, the report covers emerging trends such as AI-generated storytelling, multilayered avatar identity systems, dynamic emotion modeling, and cross-platform avatar interoperability. It also includes competitive benchmarking of leading players, innovation priorities, strategic partnerships, and advancements in ethical AI governance impacting celebrity likeness use. The scope further encompasses analysis of niche sectors including creator-economy integrations, mobile avatar apps, immersive sports avatars, and virtual showbiz ecosystems. This multidimensional overview equips decision-makers with detailed visibility into technological progress, adoption factors, and strategic opportunities shaping the future of celebrity-driven digital identity markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 520 Million |

|

Market Revenue in 2032 |

USD 1,915.2 Million |

|

CAGR (2025 - 2032) |

17.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Genies, Soul Machines, UneeQ Digital Humans, Brud, Reallusion, ObEN, Didimo, Veritone, Wolf3D / Ready Player Me, Ziva Dynamics, Synthesia, Dimension Studio, AvatarOS, Somnium Space |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |