Reports

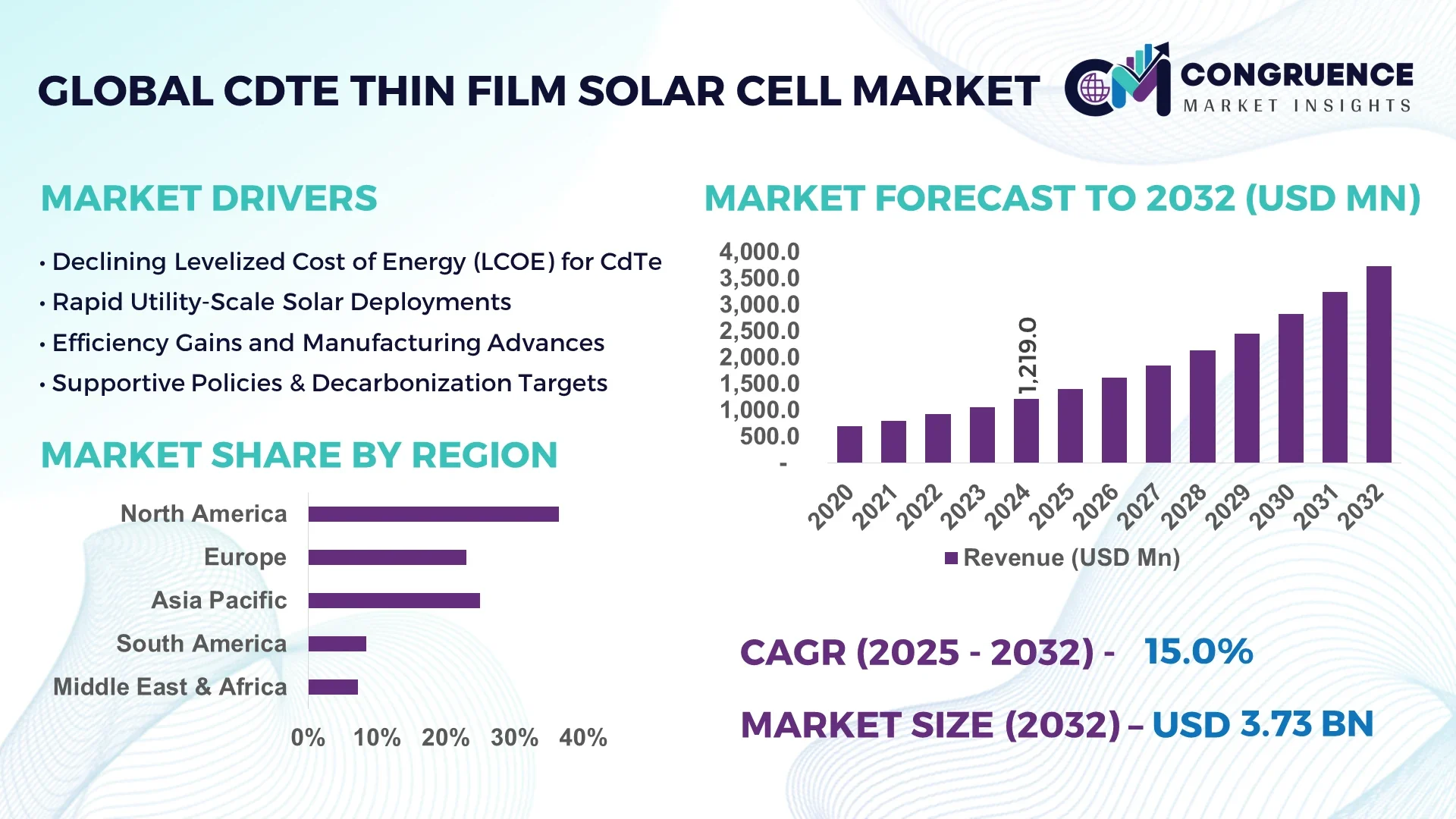

The Global Cadmium Telluride (CdTe) Thin Film Solar Cell Market was valued at USD 1,219 Million in 2024 and is anticipated to reach a value of USD 3,721.2 Million by 2032 expanding at a CAGR of 14.97% between 2025 and 2032.

The United States plays a dominant role in the Cadmium Telluride (CdTe) Thin Film Solar Cell Market, with major manufacturing facilities boasting production capacities exceeding 5 GW per year. Substantial investments have been directed toward next‑generation CdTe deposition lines and module stacking techniques, while industry partnerships with utility-scale solar farms support wide application in large utility projects and rooftop installations. Ongoing R&D advances include enhanced thin‑film alloys and improved cadmium recycling streams to reduce environmental impact.

The Cadmium Telluride (CdTe) Thin Film Solar Cell Market spans key sectors such as utility‑scale solar farms, commercial rooftop installations, and thin‑film integrated building façade modules. Technological innovations include roll‑to‑roll sputtering, tandem CdTe/CIGS stacks, and flexible substrate developments enabling low‑weight installations. Regulatory drivers such as renewable portfolio standards, net metering regulations, and carbon emission targets are shaping policy incentives in major markets. Environmental considerations, including lifecycle cadmium management and module recycling mandates, are influencing design choices. Regional adoption patterns show strong demand in North America and Latin America for large utility projects, while Europe and Asia‑Pacific focus on building‑integrated photovoltaics. Emerging trends include integration with energy storage platforms, smart grid connectivity, and lightweight flexible panels targeting rural electrification. Decision‑makers are increasingly prioritizing modules with high energy density and lower carbon footprints to meet both environmental and financing criteria.

In the Cadmium Telluride (CdTe) Thin Film Solar Cell Market, Artificial Intelligence (AI) is transforming key operational and production processes, delivering measurable efficiencies and improved yields. AI-powered control systems now oversee temperature, deposition rate, and material flow within sputtering chambers, reducing defect rates by over 25% and improving uniformity of thin‑film layers across large substrates. Predictive maintenance systems equipped with machine learning analyze equipment health indicators—such as motor vibrations or chamber pressure fluctuations—to schedule maintenance before unscheduled downtimes, increasing plant utilization by more than 15%. AI-assisted image recognition platforms are being applied for real‑time surface inspection, detecting micro‑defects and impurities at production throughput of thousands of modules per hour, ensuring tight quality control.

Moreover, AI is enabling intelligent energy output forecasting by analyzing module performance under varying weather scenarios and adjusting output predictions within ±3% accuracy. This is critical for utility operators and financiers evaluating project viability. AI-optimized supply-chain and logistics platforms are reducing delivery delays by tracking material availability, lead times, and customs clearance data across global production networks. These advancements demonstrate that in the Cadmium Telluride (CdTe) Thin Film Solar Cell Market, AI is no longer an experimental add-on—it is embedded in production, quality control, and downstream forecasting, driving measurable gains in operational performance and project reliability.

“In late 2024, a U.S. CdTe module manufacturer implemented an AI-based predictive deposition control system that reduced film thickness variability by 18% and cut material waste by 12% across a 2 GW annual production line.”

The Cadmium Telluride (CdTe) Thin Film Solar Cell Market dynamics are shaped by a maturing supply chain, regulatory mandates for renewable energy, and accelerating product innovation. Increasing demand for low‑light performance modules in utility and commercial installations is driving technological refinement, while competition from silicon‑based PV and other thin films adds pressure on pricing and efficiency. Supply chain improvements, including recycled cadmium recovery and stable tellurium sourcing, are becoming increasingly important. Policy interventions such as tax credit extensions and module recycling obligations are shaping procurement and design decisions. Integrating CdTe with energy storage and smart‑grid systems further enhances deployment attractiveness. Industry consolidation and vertical integration are influencing pricing models and vendor strategies. The interplay between improved manufacturing yield, module lifetime, and environmental compliance is central to decision-making for developers, investors, and regulators within the Cadmium Telluride (CdTe) Thin Film Solar Cell Market.

Supportive government policies—such as feed‑in tariffs, module recycling mandates, and renewable portfolio standards—have greatly boosted deployment of cadmium telluride thin film modules. For instance, in several U.S. states, mandated performance requirements for community solar and large commercial installations have increased adoption of CdTe due to its strong performance in diffuse light conditions. Public‑sector RFPs have specifically favored modules with low embodied carbon and high energy yield per watt, influencing procurement decisions and driving investment in manufacturing capacity.

While CdTe offers advantages in low-cost and low-light performance, its efficiency ceilings lag behind advanced crystalline silicon systems. Advanced multi‑junction silicon and PERC processes are delivering higher conversion efficiencies, making some developers hesitant to choose CdTe for long‑term utility projects. Additionally, concerns over cadmium toxicity and recycling complexity introduce regulatory burdens. These issues raise capital expenditure requirements for waste management infrastructure and end-of-life recycling compliance, adding operational complexity.

Cadmium Telluride thin film technology presents strong opportunities in the emerging BIPV segment due to its lightweight, flexible form factor and aesthetic neutrality. Developers of commercial façades and architectural modules are increasingly deploying CdTe in curtain walls, skylights, and canopies. In 2024, pilot projects in Europe and the U.S. reported rooftop and façade installations covering over 400 MW in total. The ability to roll out modules in curved or irregular surfaces without framing systems creates design freedom and cost savings in installation labor.

Regulatory oversight concerning cadmium, a toxic heavy metal, presents recurring challenges. Compliance with hazardous materials handling, module recycling, and end-of-life management is stringent in many markets. For example, facilities must track cadmium residue levels and maintain secure disposal or recycling protocols. Implementation of recycling programs and compliance documentation increases operational overhead by requiring dedicated infrastructure and audits. As a result, manufacturers face higher per-unit cost burdens and liability risks in markets with strict hazardous substance regulations.

Expansion of High-Energy Yield CdTe Modules: Manufacturers are launching CdTe modules with enhanced low-light energy yields and improved temperature coefficients. In 2024, some modules demonstrated energy production increases of over 8% under cloudy conditions compared to earlier generations. These developments are particularly attractive for utility-scale sites in regions with variable irradiance.

Scaling of Roll-to-Roll Flexible Production Lines: New roll‑to‑roll manufacturing systems have enabled thin film module production on flexible substrates at volumes of more than 1 GW annually from pilot lines. Such technology allows lighter, bendable modules suited to curved architectural surfaces and off-grid electrification applications, expanding the deployment horizon for CdTe thin film solutions.

Tandem CdTe/CIGS and Perovskite Integration Pilot Projects: Industry players have initiated tandem module trials combining CdTe with perovskite or CIGS layers, achieving cumulative efficiencies exceeding conventional CdTe modules (up to 22%). These pilots are now underway in both North America and Asia‑Pacific, indicating growing interest in hybrid thin‑film stacks that push efficiency benchmarks.

Deployment of Smart Module Monitoring and IoT Connectivity: CdTe module producers are incorporating integrated temperature, irradiance, and module current sensors—connected via IoT—to enable real‑time performance monitoring. These systems allow predictive output forecasting and automated fault alerts, reducing maintenance intervals and optimizing energy yield in large-scale solar farms.

The Cadmium Telluride (CdTe) Thin Film Solar Cell Market is segmented based on type, application, and end-user, each reflecting distinctive market forces and deployment trends. Type-wise, the market is categorized into modules based on substrate and deposition techniques, with variations in form factor, flexibility, and energy conversion efficiency. These technical attributes play a critical role in determining suitability for specific applications. On the application front, segments such as utility-scale solar farms, commercial rooftops, and building-integrated photovoltaics (BIPV) demonstrate strong adoption due to evolving energy policies and project economics. In terms of end-user segmentation, the market serves a diverse clientele including utility operators, government energy departments, commercial real estate developers, and off-grid electrification programs. Technological integration with smart grid systems and demand for lightweight and flexible modules further influence purchasing behavior across segments. Market participants are tailoring solutions to align with efficiency mandates, architectural aesthetics, and environmental compliance needs.

The market for Cadmium Telluride (CdTe) thin film solar cells is primarily segmented by module type, which includes rigid glass-based modules, flexible substrate modules, and emerging tandem-stack variants. Rigid CdTe modules currently lead the market due to their proven durability, ease of mass production, and high deployment in utility-scale solar farms. Their long lifespan and established supply chains make them the preferred choice for large-scale installations, especially in regions with stable irradiance and flat terrain.

The fastest-growing type is the flexible CdTe module, driven by rising demand for lightweight solar panels suitable for irregular surfaces, transportable structures, and building-integrated photovoltaics. These modules enable installations on curved rooftops, facades, and mobile units without the need for heavy support infrastructure. Advancements in roll-to-roll manufacturing and improved substrate resilience are accelerating their commercial viability.

Tandem CdTe modules, which incorporate multiple junction layers (e.g., CdTe with perovskite or CIGS), are emerging as a niche yet promising segment. These offer improved efficiency in low-light conditions and better temperature coefficients, although scalability and cost remain key challenges. Each module type is carving out relevance based on performance specifications, target application, and deployment environment.

Cadmium Telluride thin film solar cells find application across a spectrum of solar deployment scenarios. Utility-scale solar farms represent the dominant application, as these projects leverage the technology’s cost-effectiveness, superior performance in diffuse light, and reduced land use intensity per watt generated. The ability of CdTe modules to perform consistently in hot and humid conditions makes them a preferred choice for large solar parks in desert and subtropical regions.

The fastest-growing application is building-integrated photovoltaics (BIPV). Increasing demand for energy-efficient buildings and aesthetically integrated solar solutions is boosting this segment. Flexible and frameless CdTe modules are particularly well-suited for curtain walls, skylights, and façade systems. The rise in green building certifications and urban sustainability initiatives is further supporting this growth.

Other applications include commercial rooftops and remote or off-grid installations. In the commercial sector, thin film panels reduce load on rooftops and provide efficient energy solutions without complex structural retrofitting. Off-grid deployments benefit from the technology's low maintenance and favorable energy yield under partial shading, enhancing energy access in rural or disaster-prone areas.

The leading end-user segment in the CdTe thin film solar cell market is utility operators and energy project developers, who prioritize large-scale deployment, cost efficiency, and regulatory compliance. These stakeholders often engage in long-term power purchase agreements (PPAs), where the balance of capital expenditure, efficiency under real-world conditions, and total lifecycle cost favors CdTe technologies. Their projects benefit from the high energy density of modules and the technology’s strong environmental performance.

The fastest-growing end-user group is commercial real estate developers and green building consultants. The growing need for net-zero buildings and compliance with sustainable construction mandates is accelerating their investment in BIPV-compatible CdTe modules. Lightweight and customizable module formats align with modern architectural requirements, allowing energy integration without compromising design aesthetics.

Other relevant end-users include government energy departments, rural electrification agencies, and disaster relief organizations. These groups value CdTe’s rapid deployability, minimal operational overhead, and robust performance in harsh environments. As energy access, sustainability, and grid resilience become national priorities, these end-user groups will continue contributing to diversified market demand.

North America accounted for the largest market share at 36.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2025 and 2032.

The dominance of North America stems from early technology adoption, robust infrastructure, and strong federal incentives supporting clean energy deployment. In contrast, Asia-Pacific’s rapid urbanization, favorable policy reforms, and surge in solar manufacturing investments are accelerating its market trajectory. Europe remains a strong contender with a mature solar ecosystem and regulatory pressure for carbon neutrality. Meanwhile, South America and the Middle East & Africa are emerging as attractive regions due to rising energy access initiatives and favorable climate conditions. Regional dynamics vary significantly based on national energy goals, industrialization, and government support, shaping both demand and innovation pathways in the global Cadmium Telluride (CdTe) Thin Film Solar Cell market.

North America held 36.4% of the global Cadmium Telluride (CdTe) thin film solar cell market in 2024, solidifying its position as the largest regional market. The United States, in particular, drives this dominance through large-scale utility solar projects, supportive federal tax credits, and ongoing investment in renewable energy infrastructure. The Inflation Reduction Act and net-zero goals continue to incentivize both public and private sector adoption. Key industries such as power utilities, commercial real estate, and green construction are boosting demand for high-efficiency CdTe modules. Technological advancements, including AI-enhanced energy management systems and improved module manufacturing efficiencies, are enhancing adoption. Canada is also contributing with growing solar adoption in provinces like Ontario and Alberta, spurred by local sustainability mandates. North America remains a hub for solar R&D and IP generation, helping solidify its leadership in next-gen thin film deployment.

Europe accounted for 28.1% of the global Cadmium Telluride (CdTe) thin film solar cell market in 2024. Major markets such as Germany, France, and the UK are leading adoption due to aggressive climate goals, carbon neutrality targets, and policy-driven subsidies for solar installations. The European Green Deal and the Renewable Energy Directive (RED II) are accelerating the integration of thin film technologies into national energy plans. CdTe modules are being increasingly deployed in commercial rooftops and solar farms due to their performance in temperate climates and urban landscapes. The market is also benefiting from EU-wide support for circular economy practices and recycling mandates, which align well with CdTe's closed-loop manufacturing. Innovations such as lightweight modules for building integration and energy-positive architectural solutions are gaining traction in the region’s densely built environments.

Asia-Pacific ranked as the fastest-growing regional market in 2024, driven by massive demand from China, India, and Japan. China remains the dominant consumer, leveraging its expansive solar farms, domestic production capacity, and state-backed subsidies. India is rapidly catching up with initiatives like PM-KUSUM and increasing rooftop solar adoption in Tier-2 and Tier-3 cities. Japan continues to integrate thin film technologies in residential and industrial spaces, focusing on efficiency and aesthetics. The region benefits from robust infrastructure growth, increasing electrification, and localized production capabilities. Manufacturing trends such as vertical integration, low-cost raw material sourcing, and clean energy export goals are further fueling growth. Asia-Pacific is also emerging as a hotspot for solar research clusters and innovation parks, supporting next-gen CdTe deployment and broader photovoltaic advancements.

In South America, countries such as Brazil and Argentina are driving the regional Cadmium Telluride (CdTe) thin film solar cell market, contributing a growing share to global demand. Brazil, with its National Energy Plan, is heavily investing in solar farms across states like Minas Gerais and Bahia. The region’s favorable solar irradiance, coupled with growing grid expansion projects, is making thin film solutions attractive for large-scale deployment. Argentina’s renewed focus on renewable energy through public-private partnerships is further accelerating demand for CdTe modules. Government incentives, such as tax exemptions and feed-in tariffs, are improving market accessibility. Infrastructure development in rural and remote zones is creating demand for decentralized energy systems, where lightweight and robust thin film modules offer practical advantages. Trade policies facilitating technology importation and regional manufacturing are expected to strengthen South America’s position in the global solar supply chain.

The Middle East & Africa region is experiencing a steady rise in demand for Cadmium Telluride (CdTe) thin film solar cells, particularly in UAE, Saudi Arabia, and South Africa. This growth is driven by national clean energy agendas, such as Saudi Vision 2030 and UAE Energy Strategy 2050, which are pushing for large-scale solar deployment. CdTe modules are favored in this region due to their superior performance in high-temperature, high-dust environments, which are common across desert zones. Local governments are offering long-term power contracts and fiscal incentives to promote solar project development. In Africa, initiatives aimed at rural electrification, such as solar mini-grids and off-grid systems, are contributing to CdTe market expansion. Digital transformation, such as smart grid integration and mobile energy platforms, is complementing the physical deployment of thin film technology. Regional trade partnerships and energy cooperation frameworks are supporting cross-border energy transmission and solar infrastructure growth.

United States – 34.7% Market Share

The U.S. dominates due to its high utility-scale solar project capacity, favorable regulations, and robust R&D ecosystem focused on thin film solar innovation.

China – 28.9% Market Share

China holds a strong position thanks to its massive production capabilities, government-led deployment programs, and expansive solar manufacturing infrastructure.

The Cadmium Telluride (CdTe) Thin Film Solar Cell market is characterized by a moderately consolidated competitive landscape, with approximately 20 to 25 active players globally, including established firms and emerging innovators. First Solar Inc. continues to maintain a leading position, driven by its vertically integrated manufacturing and extensive project pipeline. Competitors in the space are increasingly focusing on strategic partnerships, technology licensing, and expansion of manufacturing capacity to gain a competitive edge. The market has witnessed several mergers and acquisitions, aimed at consolidating R&D expertise and optimizing supply chains for cost efficiency.

Innovation plays a critical role in differentiation, with companies investing heavily in improving module efficiency, durability, and environmental performance. Automation in production, AI-driven monitoring of solar field performance, and development of lightweight and flexible CdTe panels are emerging as key innovation areas. Firms are also exploring recycling and circular economy initiatives to align with sustainability goals, which has become a growing competitive factor, especially in Europe and North America. The competitive intensity is further heightened by localized manufacturing initiatives in Asia-Pacific, aiming to reduce dependence on imports and enhance supply chain resilience. As regulatory support and clean energy demand increase, the competition is expected to shift toward rapid scaling, product differentiation, and digital transformation.

First Solar, Inc.

Calyxo GmbH

Lucintech Inc.

Antec Solar GmbH

U.S. Photovoltaics, Inc.

Advanced Solar Power (Hangzhou) Inc.

Toledo Solar Inc.

D2solar

CTF Solar GmbH

Reon Energy Ltd.

Technological advancements in the Cadmium Telluride (CdTe) Thin Film Solar Cell market are accelerating, focusing on improving energy conversion efficiency, reducing production costs, and increasing environmental sustainability. CdTe thin film technology has gained popularity due to its short energy payback time, high temperature tolerance, and superior performance in low-light and diffuse-light conditions compared to traditional crystalline silicon panels.

Modern CdTe modules have reached efficiency levels of up to 22.3%, with ongoing research aiming to breach the 24% mark using tandem cell architectures and advanced back-contact designs. Innovations in transparent conductive oxides, laser scribing techniques, and dual-junction cell configurations are enabling higher voltage outputs and lower energy losses. Additionally, manufacturers are integrating bifacial module designs, allowing energy generation from both sides of the panel, enhancing yield per square meter.

The use of closed-loop recycling systems for CdTe materials has also emerged as a critical innovation, addressing concerns around cadmium toxicity while improving raw material recovery and sustainability. On the manufacturing front, roll-to-roll deposition techniques and automated in-line quality control systems are increasing throughput and consistency.

Digital integration through IoT-enabled monitoring, predictive maintenance platforms, and AI-based solar optimization tools is enhancing lifecycle performance management. These technologies are helping companies ensure maximum output and lower levelized cost of electricity (LCOE), making CdTe solar technology more competitive across global utility-scale and distributed energy markets.

In January 2024, First Solar began operations at its new Ohio manufacturing facility, increasing its annual production capacity by 3.3 GW. The expansion supports rising demand for domestic clean energy solutions and aligns with the U.S. government’s local content incentives.

In March 2024, Toledo Solar announced a strategic collaboration with the University of Michigan to develop next-gen CdTe cells with higher efficiency and advanced transparent back contacts, targeting applications in building-integrated photovoltaics (BIPV).

In September 2023, Advanced Solar Power (Hangzhou) completed a project in Southeast Asia delivering 100 MW of CdTe modules for an off-grid solar farm. The deployment focused on areas with high humidity and temperature, leveraging CdTe's superior thermal performance.

In November 2023, Calyxo GmbH introduced a new thin-film module line using laser-patterned substrates, aimed at reducing material consumption and enhancing power density for commercial rooftop installations across Europe.

The Cadmium Telluride (CdTe) Thin Film Solar Cell Market Report offers a comprehensive analysis of market dynamics across multiple dimensions, including product types, end-use industries, technology applications, and geographical regions. The report covers the core segmentation of CdTe thin film solar cells by installation type (utility-scale, commercial, residential), deployment model (on-grid, off-grid), and substrate material (rigid, flexible). Additionally, it delves into emerging segments such as building-integrated photovoltaics (BIPV), floating solar applications, and solar-powered charging infrastructure, offering insights into evolving use cases.

Regionally, the market is examined across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed country-level insights highlighting adoption patterns, policy impacts, and infrastructure development. The report addresses key application areas such as solar farms, industrial rooftops, smart cities, and rural electrification projects, where CdTe modules are being increasingly adopted for their efficiency and resilience.

Furthermore, the report outlines the influence of technological trends such as digitization, AI-driven solar optimization, closed-loop recycling processes, and advanced manufacturing practices. It evaluates the regulatory landscape shaping the market and identifies growth opportunities in emerging economies and sectors prioritizing decarbonization. Overall, the report equips decision-makers with actionable intelligence to navigate strategic investments, product development, and market entry or expansion plans within the CdTe solar space.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,219 Million |

| Market Revenue (2032) | USD 3,721.2 Million |

| CAGR (2025–2032) | 14.97% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-user

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Technological Insights, Segment Analysis, Regional and Country-Wise Analysis, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

| Key Players Analyzed | First Solar, Inc., Calyxo GmbH, Lucintech Inc., Antec Solar GmbH, U.S. Photovoltaics, Inc., Advanced Solar Power (Hangzhou) Inc., Toledo Solar Inc., D2solar, CTF Solar GmbH, Reon Energy Ltd. |

| Customization & Pricing | Available on request (10% Customization is Free) |