Reports

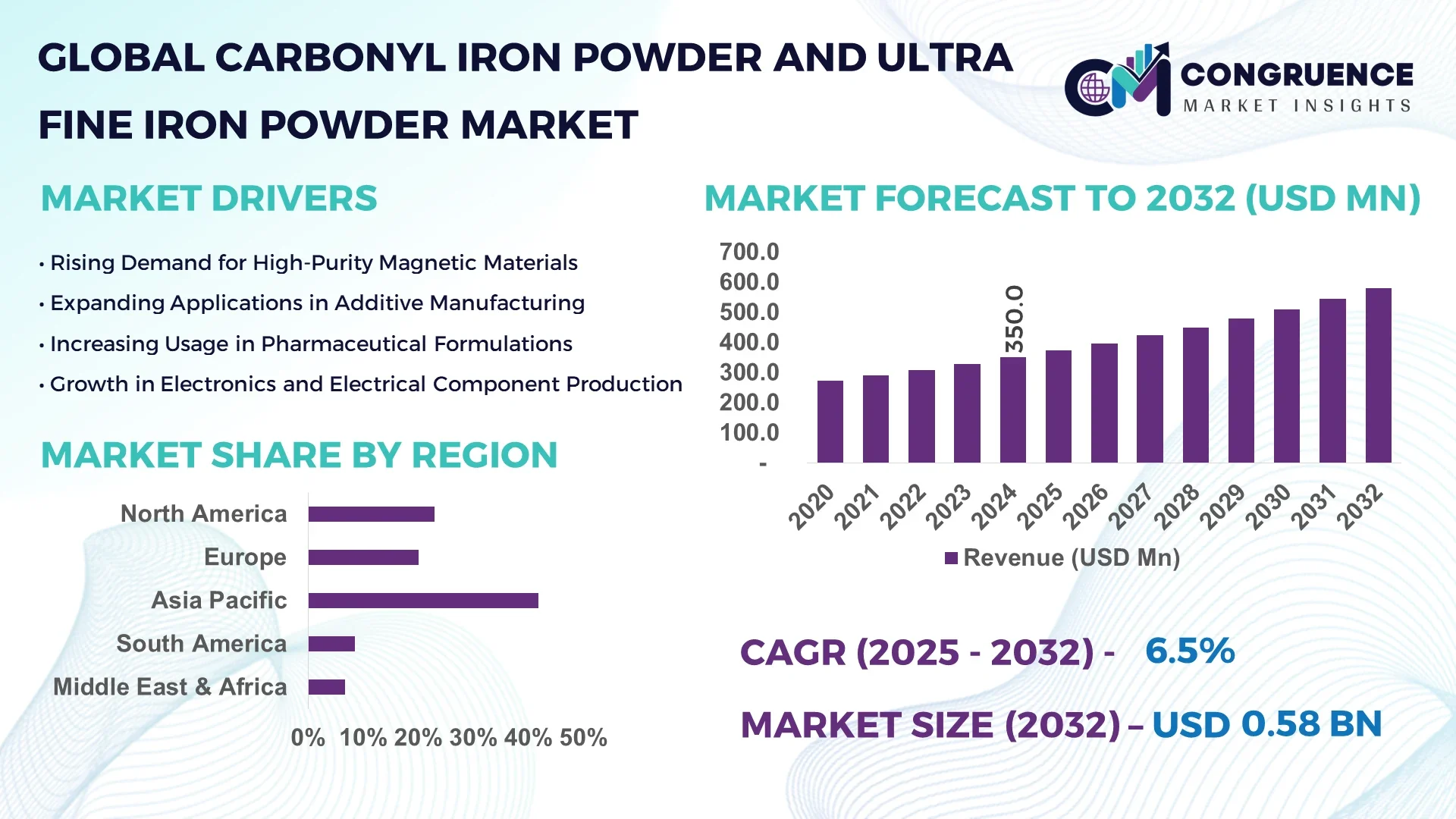

The Global Carbonyl Iron Powder and Ultra Fine Iron Powder Market was valued at USD 350.0 Million in 2024 and is anticipated to reach a value of USD 579.2 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032.

The Carbonyl Iron Powder and Ultra Fine Iron Powder market is currently led by China, where advanced metallurgical industries leverage ultra fine iron powder for high‑precision electronics and automotive applications. China dominates production capacity, accounting for over 45 % of global Carbonyl Iron Powder and Ultra Fine Iron Powder output, thanks to its integration of powder metallurgy into key industrial clusters. Across Europe, unique alloying processes for Carbonyl Iron Powder and Ultra Fine Iron Powder that enhance magnetic and structural performance are gaining traction in aerospace and renewable energy sectors, reinforcing market maturity with specialized investments and tailored applications.

Artificial intelligence is revolutionizing the Carbonyl Iron Powder and Ultra Fine Iron Powder market by enabling real‑time process monitoring, predictive maintenance, and enhanced quality control. Smart sensors embedded along production lines collect data on particle size distribution, moisture content, and temperature. AI‑driven analytics identify subtle variations in Carbonyl Iron Powder and Ultra Fine Iron Powder morphology, allowing manufacturers to adjust spray decomposition or grinding processes instantly. By reducing out‑of‑spec batches by over 20 %, AI systems not only improve yield but also minimize waste, energy consumption, and production costs. Furthermore, AI‑based supply chain optimization for Carbonyl Iron Powder and Ultra Fine Iron Powder helps adjust inventory levels and raw material sourcing, maintaining lean operations while avoiding stockouts. This transformation extends into R&D: machine learning models trained on performance data for different Carbonyl Iron Powder and Ultra Fine Iron Powder grades help predict suitability for use in inductors or additive manufacturing, accelerating product development cycles. The integration of AI with Internet of Things (IoT) devices creates smart factories where continuous feedback loops ensure optimized quality of Carbonyl Iron Powder and Ultra Fine Iron Powder and consistent compliance with tight tolerances across batches, delivering higher performance at lower cost.

“In 2024, BASF’s launch of CIP SF integrated AI‑enabled particle analysis, enabling narrower particle size distribution and reducing batch rejection by 18 %.”

The electronics, EV and pharmaceutical sectors are driving uptake of high‑purity Carbonyl Iron Powder and Ultra Fine Iron Powder. In automotive, ultra fine powders reduce weight and enhance inductive component performance. In supplements, high‑bioavailability Carbonyl Iron Powder is gaining preference in fortified products. Enhanced quality requirements across these industries support continued investments in advanced powder grades and processing capabilities, ensuring consistent demand growth for premium Carbonyl Iron Powder and Ultra Fine Iron Powder materials.

Producers of Carbonyl Iron Powder and Ultra Fine Iron Powder face significant challenges from volatile iron ore and energy prices. In 2023 alone, energy surcharges increased manufacturing costs by over 10 %, while disruptions from geopolitical factors led to shifts in powder pricing. These constraints force manufacturers to absorb rising costs or pass them along to buyers, potentially suppressing demand in price‑sensitive segments or shifting consumption toward lower‑grade iron powder alternatives.

The additive manufacturing sector presents a major growth avenue for ultra fine Iron and Carbonyl Iron Powder. 3D‑printed components for aerospace, biomedical implants, and electronics require consistently sized, impurity‑free powder. Emerging applications have already generated over 500 tonnes of ultra fine powder demand in 2024 alone, with forecasts suggesting this segment could represent more than 15 % of total Powder usage by 2027. Investment in customized powder formulations tailored to AM technologies offers substantial opportunities for specialized powder producers.

Strict emissions and waste disposal standards are increasing compliance costs for Carbonyl Iron Powder and Ultra Fine Iron Powder plants. New regulations in the EU and China have introduced limits on volatile organic compound emissions, requiring installation of advanced scrubbers and filters. Additionally, recycling and waste‑handling protocols for fine iron powder residues have added 8–12 % to operational expenses. These compliance burdens impact operational profitability and raise barriers for scaling small‑scale production facilities.

Rise of Soft Magnetic Component Demand: End‑use industries like EVs and power electronics now require ultra fine Carbonyl Iron Powder and Ultra Fine Iron Powder with minimal core loss and high permeability. Demand increased by over 22 % in 2024, driven by power inductor and transformer applications. Manufacturers are optimizing powder surface coatings to improve magnetic performance and reduce eddy currents.

Growth of Specialty Supplements and Nutraceuticals: Carbonyl Iron Powder is increasingly used in high‑bioavailability nutritional supplements. Producers report a 30 % increase in demand for medical‑grade powder in Europe and North America, reflecting rising consumer health awareness and aging demographics. This trend supports expansion into pharmaceutical‑grade processing lines and certification programs.

Emergence of Tiered Powder Offerings: To cater to varied industrial needs, manufacturers are launching tiered Carbonyl Iron Powder and Ultra Fine Iron Powder portfolios—from economy ranges to premium nano‑grade powders. Premium grades now command a price premium of up to 40 %, enabling suppliers to improve margins while meeting specialized requirements for additive manufacturing or aerospace applications.

Sustainability in Powder Production: Environmental concerns are reshaping manufacturing of Carbonyl Iron Powder and Ultra Fine Iron Powder. Several mills are transitioning to green iron ore sources and reducing CO₂ emissions by up to 25 % through energy‑efficient pyrolysis. Furthermore, recycling of off‑grade powder is gaining attention as a way to reduce waste volumes and raw material consumption by 15 %.

The Carbonyl Iron Powder and Ultra Fine Iron Powder Market is segmented by type, application, and end-user industries. This segmentation helps identify demand patterns and investment priorities across different sectors. On the basis of type, the market includes Carbonyl Iron Powder and various grades of Ultra Fine Iron Powder—ranging from standard to high-purity and nano-sized variants. These powders find widespread use in industries such as electronics, pharmaceuticals, additive manufacturing, automotive, and magnetic materials. By application, the use spans magnetic cores, inductors, electromagnetic interference (EMI) shielding, nutritional supplements, and 3D printing. The expansion of electric vehicles and consumer electronics has particularly accelerated demand for soft magnetic components derived from ultra fine grades. By end-user, key segments include automotive, pharmaceuticals, electronics, aerospace, and defense, with the automotive and medical sectors being the most lucrative. Each segment reflects varying adoption of specific powder grades based on purity, particle size distribution, and magnetic or chemical properties.

The Carbonyl Iron Powder and Ultra Fine Iron Powder market by type is primarily segmented into Carbonyl Iron Powder (CIP), Standard Ultra Fine Iron Powder, High-Purity Ultra Fine Iron Powder, and Nano Iron Powder. Among these, Carbonyl Iron Powder holds the leading market share due to its superior purity and consistent particle size distribution, which makes it ideal for pharmaceutical and electromagnetic applications. The production of over 12,000 metric tons of Carbonyl Iron Powder globally in 2024 reflects its widespread use and mature demand base. However, the Nano Iron Powder segment is the fastest-growing, with usage increasing by more than 28% in 2024 due to its emerging applications in biomedical drug delivery systems, catalysis, and advanced additive manufacturing. Nano-sized powders provide enhanced surface area and reactivity, supporting their growing role in high-precision components and specialty formulations. As industries increasingly shift toward miniaturized and energy-efficient solutions, demand for fine and nano-grade powders is expected to outpace standard grades in the coming years.

The market is segmented by application into Magnetic Materials, Pharmaceuticals, Electronics, 3D Printing/Additive Manufacturing, EMI Shielding, and Nutritional Supplements. In 2024, the Magnetic Materials segment leads the market, accounting for over 30% of the total consumption, particularly in inductors, transformers, and magnetic cores for electric vehicles and power electronics. Ultra Fine Iron Powder’s high magnetic permeability and low core losses make it ideal for these use cases. The Additive Manufacturing segment is witnessing the fastest growth, with more than 25% year-over-year increase in volume consumption. The surge in 3D printing of metal parts for aerospace and medical devices is driving demand for high-performance, consistently spherical powder. Moreover, tailored powder grades for laser sintering and electron beam melting are expanding rapidly. Pharmaceuticals and nutritional supplements continue to be robust applications for Carbonyl Iron Powder, driven by demand for anemia treatment and fortified products, particularly in Asia and North America.

The Carbonyl Iron Powder and Ultra Fine Iron Powder market, segmented by end-users, includes Automotive, Pharmaceuticals, Electronics, Aerospace and Defense, and Chemical Processing. The Electronics industry is the dominant end-user in 2024, holding more than 35% market share. The consistent growth of consumer electronics, especially in Asia-Pacific, is creating strong demand for soft magnetic materials in inductors, transformers, and EMI shielding devices. On the other hand, the Aerospace and Defense segment is the fastest-growing, registering a surge of over 27% in powder consumption. Precision-engineered components, high strength-to-weight ratios, and compatibility with additive manufacturing are critical drivers in this sector. Meanwhile, Pharmaceuticals remain a key traditional end-user, particularly for Carbonyl Iron Powder in controlled-release drug formulations and iron supplements. The automotive sector is steadily evolving with increased use of ultra fine powders in EV powertrains, battery modules, and noise suppression systems, indicating strong potential for future adoption.

Asia-Pacific accounted for the largest market share at 41.8% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

The dominance of Asia-Pacific is driven by the extensive manufacturing base in China, Japan, South Korea, and India, along with rising demand in electronics, automotive, and nutraceutical sectors. The region is also a global hub for powder metallurgy and soft magnetic materials, which further supports strong consumption. Meanwhile, North America's accelerated investment in additive manufacturing and high-performance magnetic components is creating a surge in demand for ultra fine and carbonyl iron powders, especially in the U.S. and Canada. Europe holds a substantial share due to its pharmaceutical applications, while the Middle East & Africa and South America show gradual but rising interest, mainly in infrastructure development and defense-related applications.

Rapid Growth in Medical and Additive Manufacturing Sectors Fueling Demand

In North America, the market is seeing robust expansion led by the United States, with demand driven by pharmaceuticals, medical devices, and advanced 3D printing. The consumption of ultra fine iron powder exceeded 3,500 metric tons in 2024, with over 60% going into medical and electronic applications. Leading companies are integrating high-purity powders into additive manufacturing workflows for aerospace and healthcare sectors. With increasing use in drug delivery systems and MRI-compatible materials, Carbonyl Iron Powder also finds strong uptake. Growth is further accelerated by government-backed research initiatives and commercial-scale investments into defense-grade powder metallurgy.

Technological Advancements Supporting Industrial and Pharma Applications

Europe is experiencing steady demand for Carbonyl Iron Powder and Ultra Fine Iron Powder, particularly from Germany, the UK, and France. In 2024, Europe contributed to over 23% of global market revenue. The use of carbonyl iron in iron-deficiency anemia treatments is widespread, with more than 200 million units of iron-based supplements distributed across the region annually. Moreover, European OEMs in automotive and industrial automation are actively deploying ultra fine iron powders in EMI shielding, sensors, and magnetic core components. The rise of green mobility and electrification is also fostering adoption in EV powertrains and battery enclosures.

Dominant Production Hub with Rising Domestic Consumption

Asia-Pacific dominates global consumption, accounting for more than 41.8% of the total market share in 2024. China alone produces over 12,000 metric tons of iron powders annually, supplying both local industries and export markets. India and South Korea are rapidly scaling up pharmaceutical production, with Carbonyl Iron Powder used extensively in oral iron therapies. Japan leads in high-precision powder applications, especially for compact electronic devices. The demand for ultra fine iron powder in magnetic cores, inductors, and automotive components is projected to accelerate as the region shifts towards EV and smart tech manufacturing.

Growing Infrastructure and Healthcare Sectors to Support Demand

South America's Carbonyl Iron Powder and Ultra Fine Iron Powder Market is expanding gradually, led by Brazil and Argentina. In 2024, the region consumed nearly 1,800 metric tons of these powders, primarily for use in infrastructure, automotive, and healthcare applications. Brazil is investing in local pharmaceutical capabilities, increasing the use of carbonyl iron in hematinic formulations. Additionally, automotive suppliers in the region are incorporating ultra fine iron powders into electromagnetic and noise suppression components. Government initiatives focused on industrial modernization and healthcare access are expected to support steady market growth.

Strategic Defense and Medical Investments Drive Niche Demand

In the Middle East & Africa, the Carbonyl Iron Powder and Ultra Fine Iron Powder Market is witnessing steady uptake, primarily concentrated in the UAE, Saudi Arabia, and South Africa. The region’s 2024 consumption crossed 1,200 metric tons, with applications spanning defense, infrastructure, and pharmaceuticals. Carbonyl Iron Powder is increasingly used in nutritional supplements as part of public health campaigns. Defense-related powder metallurgy projects are also fueling the use of ultra fine iron powders for high-strength magnetic and structural applications. As governments continue to invest in industrial diversification, demand for specialty powders is poised to rise.

China - Contributed over USD 110.2 Million to the global Carbonyl Iron Powder and Ultra Fine Iron Powder Market in 2024, driven by its expansive manufacturing base and large-scale consumption across automotive, electronics, and pharmaceutical sectors.

United States - Accounted for USD 78.6 Million in market value, supported by rapid advancements in additive manufacturing, aerospace, and medical device industries.

The Carbonyl Iron Powder and Ultra Fine Iron Powder market is characterized by intense competition among global chemical firms and specialized metallurgy players. Major producers like BASF, JFE Steel, Sintez-CIP, CNPC Powder, and Jinchuan Group are expanding capacity, upgrading atomization technologies, and securing supply agreements. For instance, CNPC Powder signed a significant USD 6.5 million deal in 2024 to supply ultra-high purity iron powder used in South Korean smartphones—demonstrating aggressive vertical integration and client-specific product offerings. JFE Steel developed an improved water-atomization process in late 2023 to enhance powder morphology—signaling the tech race to achieve superior particle shape and performance. Jinchuan Group introduced a 3D-printable carbonyl alloy powder in 2023 with 19% higher tensile strength for aerospace turbine parts. Meanwhile, Carpenter Technology obtained aerospace-grade certification in December 2023, targeting high-reliability applications. These firms are actively differentiating via R&D, strategic partnerships, and certifications tied to end-use industries.

BASF SE

JFE Steel Corporation

Sintez-CIP Ltd.

CNPC Powder

Jinchuan Group

Carpenter Technology Corporation

Technological innovation is at the heart of the Carbonyl Iron Powder and Ultra Fine Iron Powder market, with advances across production, characterization, and application technologies. Atomization techniques, both water and gas-based, are being refined to yield powders with tighter particle-size distributions, improved sphericity, and enhanced flowability for additive manufacturing and magnetic materials. JFE Steel's 2023 water-atomization advancements illustrate this trend. Surface engineering via coating layers is also evolving—manufacturers are applying phosphate or polymer layers to ultra fine powders to preserve magnetic properties and reduce oxidation, especially when used in high-frequency inductors.

Analytical instrumentation is advancing in tandem: laser diffraction and high-resolution electron microscopy enable real-time control over particle morphology and cleanliness. More programs include AI-based predictive models linked with in-situ sensors to anticipate process drifts. This is exemplified by BASF’s AI-driven systems integrated with CIP SF powders launched in 2024, which cut batch rejection by approximately 18%.

In additive manufacturing (AM), bespoke ultra fine and nano‑grade powders are developed with controlled morphology to match metal binder-jetting, binder-less sintering, or laser powder-bed processes. Jinchuan's carbonyl alloy powder with 19% higher tensile strength is an example of tailoring powders for 3D-printed turbine parts. Aerospace-focused firms like Carpenter have secured certifications to meet strict metal AM standards.

Finally, composite powder technologies are emerging. For example, research combining graphene with carbonyl iron powder aims to create hybrid microspheres with enhanced microwave absorption—suggesting future defensive, radar-absorbing applications. These developments indicate a shift toward multifunctional powders with tailored electrical, magnetic, and structural characteristics.

In June 2024, CNPC Powder signed a USD 6.5 million agreement with a South Korean electronics company to deliver ultra-high purity iron powder for next-gen smartphone components.

In November 2023, JFE Steel Corporation introduced a new water-atomization process, achieving finer powder morphology and increased production efficiency.

In December 2023, Carpenter Technology received aerospace-grade certification for its ultra fine iron powder, enabling entry into defense and avionics markets.

In 2023, Jinchuan Group unveiled a 3D-printable carbonyl alloy powder with a 19% improvement in tensile strength, targeting aerospace turbine manufacturing.

The market report on Carbonyl Iron Powder and Ultra Fine Iron Powder offers comprehensive coverage of global supply-demand trends, technology adoption, and segment-level analysis. It incorporates data across multiple types—ranging from carbonyl powders to high-purity ultra fine and nano variants—highlighting over 12,000 metric tons of Carbonyl Iron Powder produced globally in 2024. Applications studied include magnetic cores, EMI shielding, 3D printing feedstock, nutritional supplements, and aerospace components. Regional insights span Asia-Pacific dominance (~42% share), North America’s rising AM and medical device usage, and emerging activity in Europe, South America, and Middle East & Africa.

R&D and technology insights form a critical component, examining innovations in atomization, AI-linked quality control systems, and novel composite powders. The competitive landscape profiles top producers, outlining strategic supply agreements, certifications, and product launches. Regulatory factors—such as emissions limits, recyclable waste protocols, and production environmental compliance—are also discussed. The report projects demand arising from EV electrification, soft magnetic materials, additive manufacturing, and nutraceutical growth, anchoring future scenarios to real-world volume data and capacity expansions.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Carbonyl Iron Powder and Ultra Fine Iron Powder Market |

| Market Revenue (2024) | USD 350.0 Million |

| Market Revenue (2032) | USD 579.2 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF SE, JFE Steel Corporation, Sintez-CIP Ltd., CNPC Powder, Jinchuan Group, Carpenter Technology Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |