Reports

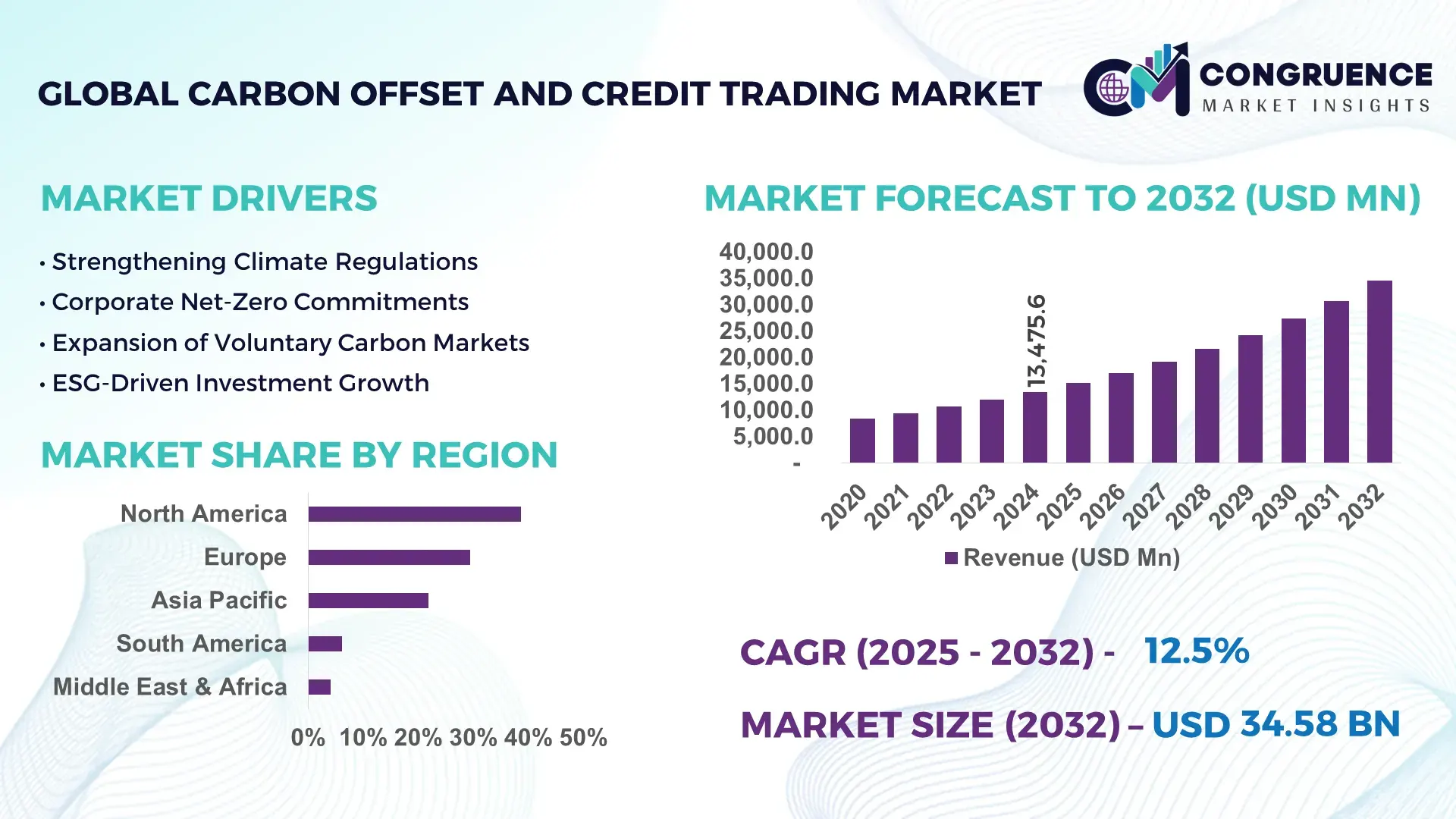

The Global Carbon Offset and Credit Trading Market was valued at USD 13,475.6 Million in 2024 and is anticipated to reach a value of USD 34,575.5 Million by 2032 expanding at a CAGR of 12.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily supported by the formalization of voluntary carbon markets, rising corporate net-zero commitments, and increasing integration of carbon pricing mechanisms into enterprise risk and compliance strategies.

The United States dominates the Carbon Offset and Credit Trading Market in terms of institutional depth and transactional scale. The country hosts more than 40% of global voluntary carbon market project developers, with annual offset issuance exceeding 200 million metric tons of CO₂e. Corporate procurement is led by energy, technology, and aviation sectors, accounting for nearly 62% of domestic credit demand. Investment activity remains strong, with over USD 6 billion deployed into carbon trading platforms, registries, and MRV technologies between 2021 and 2024. Advanced digital registries, blockchain-based credit traceability, and AI-driven verification tools are widely deployed, reducing verification cycle times by nearly 30% across U.S.-based trading platforms.

Market Size & Growth: Valued at USD 13.48 billion in 2024 and projected to reach USD 34.58 billion by 2032, driven by expanding corporate net-zero adoption and compliance-driven offset demand.

Top Growth Drivers: Corporate net-zero adoption (68%), ESG-linked procurement mandates (54%), digital MRV efficiency gains (41%).

Short-Term Forecast: By 2028, digital trading platforms are expected to reduce transaction costs by approximately 22%.

Emerging Technologies: Blockchain-based registries, AI-powered MRV systems, and satellite-enabled carbon verification tools.

Regional Leaders: North America (USD 13.9 billion by 2032; enterprise-led demand), Europe (USD 10.4 billion; regulatory-driven adoption), Asia Pacific (USD 7.6 billion; project supply expansion).

Consumer/End-User Trends: Energy, aviation, and technology firms represent over 60% of total credit purchases, with multi-year offtake agreements increasing.

Pilot or Case Example: In 2023, a U.S.-based airline offset pilot reduced lifecycle emissions intensity by 18% through verified nature-based credits.

Competitive Landscape: Market leader holds ~18% share, followed by Verra, Gold Standard, Climate Impact X, and South Pole.

Regulatory & ESG Impact: Expansion of mandatory climate disclosures and Scope 3 reporting requirements accelerating offset procurement.

Investment & Funding Patterns: Over USD 9 billion invested globally in trading platforms, registries, and carbon finance vehicles since 2021.

Innovation & Future Outlook: Integration of real-time MRV, automated settlement, and cross-border credit interoperability shaping future market structure.

The Carbon Offset and Credit Trading Market is driven primarily by energy (32%), transportation (21%), manufacturing (18%), and technology services (15%). Digital MRV platforms and tokenized credits are improving transparency, while stricter ESG disclosure norms and regional compliance schemes are shaping demand patterns. Asia Pacific leads in project origination, whereas North America and Europe drive consumption, with long-term corporate offtake agreements defining future growth trajectories.

The Carbon Offset and Credit Trading Market has become a strategic instrument for corporations aligning operational performance with climate compliance and long-term ESG objectives. Organizations increasingly embed carbon credit procurement into enterprise risk management, supply-chain optimization, and capital allocation strategies. Digitally verified credits supported by AI-driven MRV systems deliver up to 35% faster validation cycles compared to manual verification standards, significantly improving liquidity and confidence across trading platforms.

From a regional perspective, North America dominates in transaction volume, supported by advanced exchanges and institutional buyers, while Europe leads in enterprise adoption, with approximately 58% of large enterprises integrating offsets into formal decarbonization roadmaps. In Asia Pacific, supply-side expansion is accelerating, with afforestation and renewable-linked projects accounting for over 60% of new credit issuances.

In the short term, by 2027, AI-enabled monitoring and satellite-based verification are expected to improve credit accuracy and permanence scoring by nearly 28%, directly reducing reputational and compliance risks for buyers. ESG commitments are also intensifying, with firms committing to 40–50% Scope 3 emission reductions by 2030, using high-integrity offsets as interim instruments.

A measurable micro-scenario emerged in 2024, when a U.S.-based technology firm achieved a 22% reduction in net operational emissions through automated credit procurement integrated with real-time emissions tracking. Looking ahead, the Carbon Offset and Credit Trading Market is positioned as a core pillar supporting regulatory compliance, enterprise resilience, and scalable pathways toward global decarbonization.

The Carbon Offset and Credit Trading Market is shaped by evolving climate regulations, corporate decarbonization strategies, and advancements in verification technologies. Market dynamics reflect a transition from fragmented, project-based transactions toward standardized, platform-driven trading ecosystems. Demand-side activity is increasingly governed by internal carbon pricing mechanisms, while supply-side dynamics are influenced by land availability, renewable project pipelines, and verification capacity. Digital registries, enhanced transparency, and growing buyer scrutiny are reshaping credit quality benchmarks. At the same time, geopolitical climate policies and cross-border interoperability requirements continue to influence transaction flows, contract structures, and credit eligibility criteria across regions.

Corporate net-zero commitments have become a primary catalyst for market expansion. Over 75% of Fortune 500 companies have announced carbon neutrality or net-zero targets, many requiring offsets to address residual emissions. Internal carbon pricing mechanisms, averaging USD 50–100 per metric ton, are accelerating structured credit procurement. Long-term offtake agreements now cover nearly 45% of traded credits, improving market stability and predictability. Sectors such as aviation and heavy manufacturing increasingly rely on offsets to bridge technological gaps, directly stimulating trading activity and platform adoption.

Market growth faces restraint from concerns related to credit additionality, permanence, and double counting. Independent assessments indicate that nearly 30% of legacy credits face heightened scrutiny due to outdated methodologies. This has increased due diligence costs by approximately 20% for buyers and slowed transaction timelines. Fragmented standards across registries further complicate cross-border trading, limiting liquidity and creating hesitancy among institutional participants seeking long-term compliance certainty.

Digital MRV systems offer significant untapped opportunity by improving transparency and reducing verification delays. AI-powered monitoring tools can cut manual audit requirements by 35%, while satellite-based analytics improve accuracy for nature-based projects by over 25%. These technologies enable fractional ownership, real-time reporting, and automated settlement, expanding participation among mid-sized enterprises and financial institutions. As interoperability improves, digital infrastructure is expected to unlock new cross-border trading corridors.

Divergent regulatory frameworks across regions pose operational and compliance challenges. Over 20 distinct carbon standards are currently in use globally, increasing legal complexity and limiting fungibility. Companies operating across multiple jurisdictions face higher administrative overheads and inconsistent eligibility criteria. Additionally, evolving disclosure rules increase reporting burdens, requiring continuous system upgrades and legal oversight, which can disproportionately affect smaller market participants.

Expansion of Digital MRV Platforms: Over 65% of newly issued credits in 2024 incorporated some form of digital monitoring, reducing verification timelines by 30% and improving audit accuracy across forestry and renewable projects.

Growth in Long-Term Offtake Agreements: Multi-year offtake contracts now account for nearly 50% of corporate credit procurement, providing price stability and supporting large-scale project financing, particularly in Asia Pacific and Latin America.

Increased Use of Blockchain Registries: Blockchain-based registries are being used in over 40% of high-volume trades, improving traceability and reducing double-counting risks by approximately 25% compared to legacy systems.

Integration with Enterprise Carbon Accounting: More than 55% of large enterprises now integrate trading platforms directly with carbon accounting software, enabling real-time emissions balancing and improving internal reporting efficiency by 20%.

The Carbon Offset and Credit Trading Market is segmented based on type, application, and end-user, reflecting the structural evolution of global carbon markets and differentiated demand drivers. By type, the market spans compliance-based credits and voluntary carbon offsets, each aligned with distinct regulatory and corporate strategies. Applications range from regulatory compliance to corporate ESG optimization and supply-chain decarbonization, with usage intensity varying by sector maturity and disclosure requirements. End-user segmentation highlights strong participation from energy, aviation, and manufacturing enterprises, alongside growing adoption by financial institutions and technology firms. Across all segments, digitalization, enhanced verification standards, and long-term decarbonization commitments are influencing procurement behavior, contract structures, and credit preferences. This segmentation framework provides decision-makers with clarity on where demand concentration exists, how usage patterns differ across industries, and which segments are shaping future trading volumes.

The Carbon Offset and Credit Trading Market by type is primarily divided into Compliance Carbon Credits and Voluntary Carbon Offsets, along with smaller niche categories such as hybrid or jurisdictional credits. Compliance carbon credits currently lead the segment, accounting for approximately 58% of total adoption, driven by mandatory emission caps, regulated trading schemes, and legally binding reduction targets. These credits are widely used in energy, utilities, and heavy industry, where regulatory obligations require consistent annual procurement. Voluntary carbon offsets represent around 32% of adoption, primarily purchased by corporates pursuing net-zero or carbon-neutral commitments beyond regulatory requirements. Adoption of voluntary offsets is expanding rapidly, with this segment recording the fastest growth at an estimated 14.8% CAGR, supported by corporate ESG integration, consumer-facing sustainability pledges, and Scope 3 emission management. Other types, including jurisdictional REDD+ credits and emerging technology-based removals, collectively contribute roughly 10% of total activity. These segments play a niche but strategic role, particularly for buyers seeking high-integrity or long-duration carbon removal solutions.

By application, Regulatory Compliance remains the leading segment, representing approximately 46% of market usage, as industries operating under emissions trading systems must procure credits to meet legally enforced caps. This application is especially prominent in power generation, refining, and cement manufacturing, where annual emissions monitoring is mandatory. Corporate Net-Zero and ESG Reporting follows closely with around 38% adoption, as enterprises increasingly integrate offsets into sustainability disclosures, supply-chain emissions strategies, and investor reporting frameworks. This application is also the fastest growing, expanding at an estimated 15.2% CAGR, driven by mandatory climate disclosures, rising stakeholder scrutiny, and board-level accountability for emissions performance. Other applications, including carbon-neutral product labeling, supply-chain offsetting, and event-based offsetting, together account for roughly 16% of total usage. Consumer adoption trends reinforce this shift: in 2024, over 41% of global enterprises reported using offsets as part of ESG or sustainability reporting frameworks, while 57% of consumers indicated higher trust in brands that disclose third-party verified carbon offset usage.

End-user analysis shows that Energy and Utilities companies lead the Carbon Offset and Credit Trading Market, accounting for approximately 34% of total demand, due to high baseline emissions and continuous compliance obligations. These organizations typically engage in structured, long-term credit procurement aligned with regulatory cycles. Transportation and Aviation represent about 22% of adoption, using credits to balance hard-to-abate emissions and comply with international emissions frameworks. The fastest-growing end-user segment is Technology and Digital Services, expanding at an estimated 16.1% CAGR, as data centers, cloud providers, and digital platforms offset electricity and infrastructure-related emissions to meet aggressive carbon-neutral targets. Other end-users—including manufacturing, financial services, and consumer goods companies—collectively contribute around 44% of market participation. Adoption depth varies, with over 48% of large manufacturers integrating offsets into supply-chain emissions programs, while 37% of financial institutions apply credits to meet portfolio-level climate commitments.

North America accounted for the largest market share at 38.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.9% between 2025 and 2032.

North America’s leadership is supported by mature carbon trading infrastructure, high corporate ESG participation, and strong institutional buyer activity, with over 65% of Fortune 500 companies actively procuring carbon offsets or credits. Europe follows closely with approximately 29.4% share, driven by mandatory compliance frameworks and standardized emissions reporting. Asia-Pacific, holding around 21.8% share, is witnessing rapid expansion due to large-scale project origination, increasing cross-border credit issuance, and growing participation from manufacturing-heavy economies. South America and the Middle East & Africa together account for roughly 10.2%, supported by nature-based projects, renewable energy expansion, and international offset demand. Regional differences in regulation, technology adoption, and corporate climate commitments continue to shape transaction volumes and buyer behavior.

The Carbon Offset and Credit Trading Market in this region represents approximately 38.6% of global activity, making it the largest regional contributor. Demand is primarily driven by energy, aviation, technology, and financial services, which together account for nearly 68% of total credit purchases. Regulatory frameworks such as state-level cap-and-trade systems and federal climate disclosure requirements are accelerating structured offset procurement. Digital transformation is advanced, with over 55% of trades executed via online platforms using automated verification and settlement tools. Local players are investing heavily in blockchain registries and AI-driven MRV solutions to improve transparency and reduce transaction friction. Consumer behavior shows higher enterprise adoption in sectors such as healthcare and finance, where sustainability-linked reporting and emissions accountability are increasingly tied to investor and stakeholder expectations.

Europe accounts for approximately 29.4% of the Carbon Offset and Credit Trading Market, supported by strong participation from Germany, the United Kingdom, and France, which together represent over 60% of regional demand. Regulatory bodies enforcing emissions trading schemes and sustainability disclosure standards are central to market development. Adoption of emerging technologies such as digital MRV platforms and centralized registries is widespread, with nearly 48% of credits linked to digitally verified projects. Regional players are focusing on high-integrity credits aligned with strict methodological standards. Consumer and enterprise behavior reflects regulatory pressure, with compliance-driven buyers prioritizing transparent, auditable credits that meet cross-border reporting requirements.

Asia-Pacific ranks third in market share at approximately 21.8%, but leads globally in project origination volume. China, India, and Japan collectively contribute over 70% of regional credit supply, supported by large-scale renewable energy, forestry, and industrial decarbonization initiatives. Infrastructure expansion and manufacturing intensity are major demand drivers, particularly among export-oriented industries. Innovation hubs across East and Southeast Asia are accelerating adoption of satellite monitoring and mobile-based verification tools. Regional players are increasingly integrating carbon trading platforms with digital payment and settlement systems. Consumer behavior trends indicate growth driven by e-commerce, digital platforms, and multinational supply-chain decarbonization requirements.

South America represents roughly 6.1% of global market activity, with Brazil and Argentina as key contributors. The region benefits from extensive forestry and land-use projects, accounting for over 65% of locally generated credits. Energy transition initiatives and renewable deployment are supporting demand, while government incentives encourage international offset partnerships. Local market participants are focusing on large-scale afforestation and conservation-linked credits. Consumer behavior in the region shows demand tied closely to international buyers, media exposure, and localization of sustainability narratives for global brands.

The Middle East & Africa region holds approximately 4.1% of the Carbon Offset and Credit Trading Market, with demand driven by oil & gas, construction, and infrastructure sectors. The UAE and South Africa are leading contributors, together accounting for over 55% of regional transactions. Technological modernization, including digital registries and remote monitoring, is gaining traction as governments align carbon strategies with diversification goals. Local regulations and cross-border trade partnerships are supporting pilot trading initiatives. Consumer behavior reflects a growing emphasis on national sustainability goals and international collaboration, particularly among large industrial players.

United States – 34.2% Market Share: Strong enterprise demand, advanced trading infrastructure, and large-scale institutional participation drive dominance in the Carbon Offset and Credit Trading Market.

China – 18.6% Market Share: High project origination capacity, extensive renewable deployment, and strong industrial participation position China as a leading contributor to the Carbon Offset and Credit Trading Market.

The Market Competition Landscape in the Carbon Offset and Credit Trading Market is defined by a moderately fragmented environment where 35+ active competitors operate across compliance and voluntary segments. Market positioning varies from integrated full-service platforms to specialized firms focusing solely on project origination, digital verification tools, or secondary trading services. The combined share of the top 5 companies accounts for approximately 41% of total voluntary transactions, indicating a concentrated core of influential players operating amid a broad base of regional and niche providers. Established firms maintain competitive edges through strategic alliances, technology adoption, and expanded service portfolios. For example, some leaders have formed partnerships with tech providers to integrate advanced digital MRV systems and blockchain-based registries, improving traceability and reducing verification timelines on large project sets. Other market participants have pursued mergers or acquisitions of climate software specialists to bolster carbon accounting and issuance capabilities, enhancing end-to-end service offerings. Innovation trends shaping competition include AI-powered monitoring tools, blockchain-enabled credit tracking, and decentralized trading platforms that attract both enterprise and SME engagement. Despite growth pressures, competitive dynamics also reflect operational challenges such as verification integrity standards, variable pricing mechanisms, and diverse global regulatory frameworks that influence how firms differentiate offerings and capture market segments.

Allcot Group

WayCarbon

Biofílica

Carbon Clear

GreenTrees

Renewable Choice

Aera Group

Forest Carbon

NativeEnergy

Bioassets

ClimatePartner GmbH

EcoAct

Emerging and established technologies are fundamentally reshaping the Carbon Offset and Credit Trading Market, enhancing verification accuracy, transaction transparency, and market accessibility for both institutional and decentralized participants. Digital MRV (Monitoring, Reporting, Verification) systems are central to this evolution, with approximately 38% of new offset projects in 2025 deploying automated or semi-automated MRV tools such as satellite imagery, IoT sensors, and AI-based emission modeling. These systems reduce verification time by nearly 30% and improve data integrity for forestry, renewable energy, and soil carbon projects, helping buyers and sellers trust credit quality.

Blockchain and smart contract integration are facilitating more secure and transparent trading ecosystems. Around 21% of carbon credits in recent market activity are represented as tokenized assets on decentralized ledgers, removing double-counting risks and enabling programmable retirement of credits upon transaction completion. This technological shift also lowers barriers for small and medium enterprises to participate in trading platforms previously dominated by larger firms. Hybrid platforms are emerging that combine credit origination, digital MRV, and marketplace capabilities in a unified interface, improving user experience and lowering operational costs.

AI-driven analytics tools are also being adopted, with roughly 19% of energy efficiency and emissions-related offset programs employing machine learning to predict project performance, optimize credit portfolios, and model future decarbonization pathways. Such analytics support real-time carbon accounting across complex supply chains. In parallel, direct air capture, biochar, and enhanced weathering technologies are being integrated with digital tracking systems to expand the types of tradable carbon removal credits, reflecting a broader technological diversification. This convergence of digital and carbon removal technologies is positioning the market for deeper integration with global climate reporting frameworks and enterprise carbon strategies.

In June 2024, 3Degrees launched a new Carbon Removal Suite to streamline corporate access to carbon dioxide removal (CDR) markets, enabling simplified procurement pathways and market entry for corporates seeking removals-based credits and tailored procurement structures. Source: www.3degreesinc.com

In 2023, Terrapass reported that its customers supported approximately 287,656 metric tonnes of CO₂ offsets—equivalent to planting over 4.5 million trees—highlighting the company’s expanded project portfolio and verified offset delivery for individual and corporate buyers. Source: www.terrapass.com

In December 2023, Verra published a major organizational update outlining operational reforms and stakeholder engagement measures aimed at improving program scalability and governance for REDD+ and other project types, signaling institutional changes to enhance registry oversight and project management. Source: www.verra.org

In May 2024, Gold Standard launched an online resource to track methodologies under development, improving transparency around methodological updates and enabling project developers and buyers to monitor progress on new standards and criteria for certifying mitigation and removal activities. Source: www.goldstandard.org

The scope of the Carbon Offset and Credit Trading Market Report covers the comprehensive landscape of carbon trading mechanisms, spanning compliance and voluntary markets across global regions. The report examines detailed segmentation by type, including compliance carbon credits, voluntary offsets, and emerging hybrid or high-integrity credit types such as removal-based and nature-based solutions. It analyzes application areas such as regulatory compliance, corporate ESG strategies, supply-chain decarbonization, and specialized use cases like carbon-neutral product labeling, offering insights into how different sectors utilize credits for distinct decarbonization objectives. The geographic scope encompasses regional markets in North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with data on regional adoption patterns, transaction volumes, infrastructure trends, regulatory influences, and consumer behavior variations. Technology focus areas include digital MRV systems, blockchain and tokenization platforms, AI-driven analytics for emissions modeling, and integrated trading platforms that combine origination, verification, and settlement. The report also highlights industry focus areas such as energy & utilities, transportation, manufacturing, technology services, and financial institutions to illustrate end-user demand drivers and adoption behavior. With an emphasis on strategic insights and market dynamics—including competitive analysis, innovation trends, segmentation breakdowns, and regulatory frameworks—the report supports decision-makers in understanding market structure, identifying growth levers, and evaluating future pathways in the evolving carbon credit and offset ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 13,475.6 Million |

| Market Revenue (2032) | USD 34,575.5 Million |

| CAGR (2025–2032) | 12.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | South Pole Group, 3Degrees, Terrapass, Allcot Group, WayCarbon, Biofílica, Carbon Clear, GreenTrees, Renewable Choice, Aera Group, Forest Carbon, NativeEnergy, Bioassets, ClimatePartner GmbH, EcoAct |

| Customization & Pricing | Available on Request (10% Customization Free) |