Reports

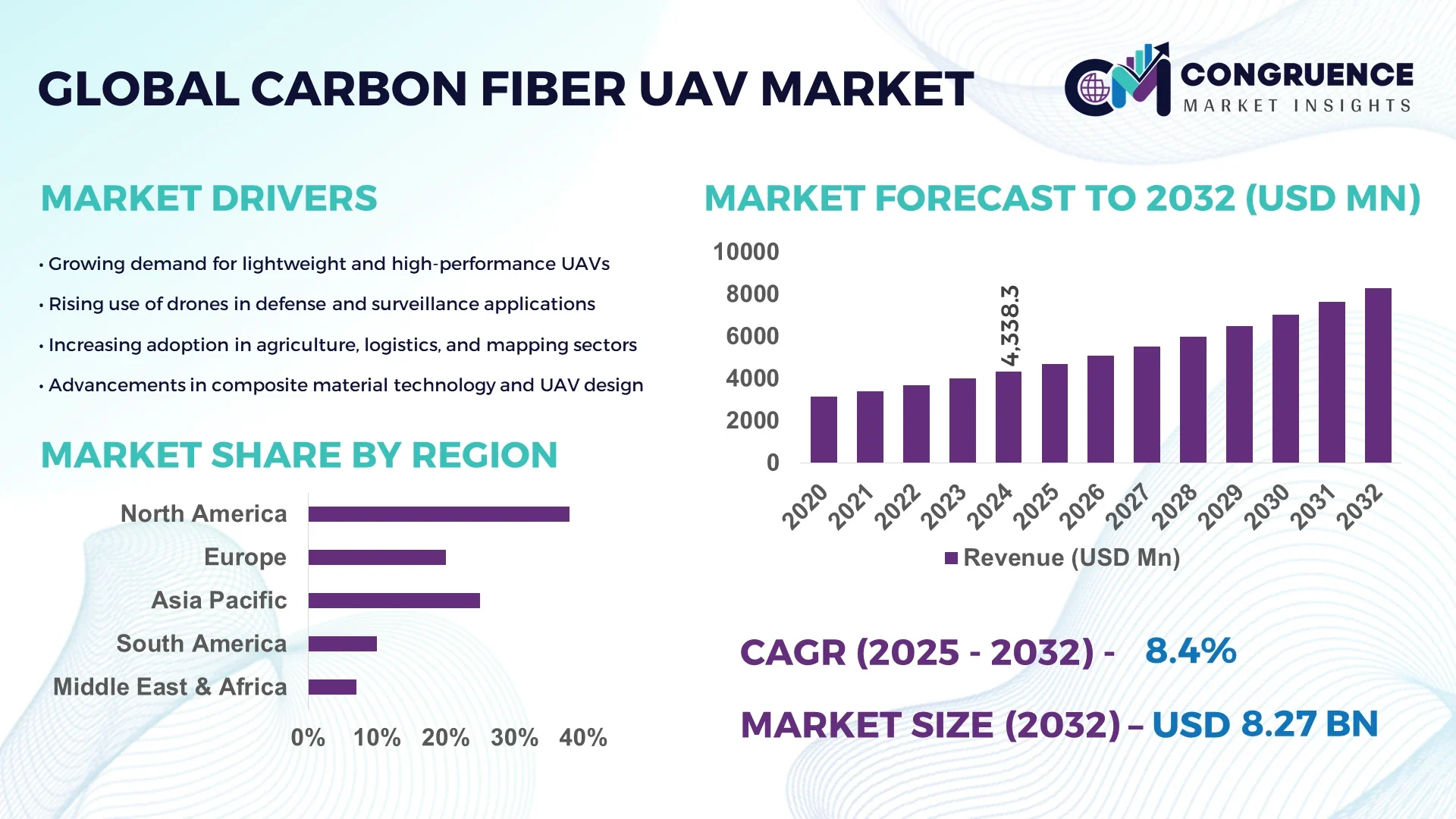

The Global Carbon Fiber UAV Market was valued at USD 4338.3 Million in 2024 and is anticipated to reach a value of USD 8270.9 Million by 2032 expanding at a CAGR of 8.4% between 2025 and 2032. The growth is driven by rising adoption of lightweight, high-strength UAVs across commercial, defense, and industrial sectors.

The United States dominates the Carbon Fiber UAV market with advanced manufacturing infrastructure and high investment levels exceeding USD 1.2 billion in 2024 alone. Key applications include defense surveillance, commercial delivery services, and industrial inspection. The country’s UAV production capacity exceeds 12,000 units annually, with leading players focusing on integrating autonomous navigation systems and AI-based flight control technologies. Regional segmentation shows the West Coast contributing 45% of domestic UAV production, while consumer adoption in sectors like agriculture and logistics accounts for 35% of total UAV usage. Continuous R&D has enabled higher endurance UAVs capable of flying up to 8 hours per mission and carrying payloads of up to 20 kg, supporting the expansion of UAV applications across multiple industries.

Market Size & Growth: Current market value of USD 4338.3 Million, projected to reach USD 8270.9 Million by 2032 due to rising demand for lightweight and high-performance UAVs.

Top Growth Drivers: Defense adoption 38%, commercial delivery efficiency 30%, industrial inspection optimization 25%.

Short-Term Forecast: By 2028, UAV operational efficiency expected to improve by 20%, reducing maintenance downtime.

Emerging Technologies: AI-based navigation systems, hybrid-electric propulsion, advanced carbon fiber composites.

Regional Leaders: North America USD 3400 Million, Europe USD 2100 Million, Asia-Pacific USD 1950 Million; Europe shows strong commercial UAV adoption.

Consumer/End-User Trends: Increasing use in agriculture, logistics, and surveillance with 40% of UAVs deployed for commercial purposes.

Pilot or Case Example: In 2023, a U.S. defense project achieved a 15% increase in UAV flight duration using next-gen carbon fiber frames.

Competitive Landscape: Market leader DJI (~18%), followed by Lockheed Martin, AeroVironment, Northrop Grumman, and Textron Systems.

Regulatory & ESG Impact: UAV operations increasingly compliant with FAA and EASA guidelines, with ESG measures targeting 10% reduction in manufacturing emissions by 2025.

Investment & Funding Patterns: Recent investments totaled USD 650 Million, focusing on AI integration, hybrid propulsion, and autonomous control systems.

Innovation & Future Outlook: Integration of autonomous AI flight, longer-endurance carbon fiber UAVs, and hybrid propulsion systems are shaping future market expansion.

The Carbon Fiber UAV Market continues to expand across commercial, defense, and industrial sectors, with agriculture, delivery, and inspection applications contributing over 55% of demand. Technological innovations such as hybrid-electric UAVs, AI-enabled flight systems, and advanced carbon fiber structures are improving payload capacity, flight endurance, and operational efficiency. Regulatory compliance and ESG initiatives are driving sustainable manufacturing, while growing investment in autonomous and AI-integrated UAVs supports adoption across logistics, defense, and infrastructure monitoring. Emerging trends like swarm technology and hybrid propulsion UAVs indicate a strong forward-looking trajectory, positioning the market for continued expansion in both domestic and international applications.

The Carbon Fiber UAV Market holds strategic importance across defense, commercial, and industrial sectors due to its combination of lightweight construction and enhanced flight performance. Advanced hybrid-electric UAV technology delivers up to 25% longer flight endurance compared to conventional lithium-polymer powered drones, enabling longer mission durations for surveillance, delivery, and inspection applications. North America dominates in volume, while Europe leads in adoption, with 35% of enterprises integrating UAV solutions into logistics, infrastructure monitoring, and agricultural operations. By 2027, AI-assisted autonomous flight systems are expected to improve operational efficiency by 18%, optimizing route planning, reducing energy consumption, and enhancing payload utilization. Firms are committing to ESG improvements such as a 12% reduction in production-related carbon emissions by 2026 through sustainable carbon fiber sourcing and recycling programs. In 2024, a leading U.S. UAV manufacturer achieved a 20% reduction in maintenance downtime using predictive AI-driven diagnostics integrated with carbon fiber UAV platforms. Forward-looking strategies in design optimization, AI integration, and sustainable materials position the Carbon Fiber UAV Market as a resilient, compliant, and sustainable pillar for future aerospace, commercial, and defense applications.

The rising demand for long-endurance UAVs is significantly driving the Carbon Fiber UAV Market. Lightweight carbon fiber structures allow UAVs to carry larger payloads while extending flight time, essential for defense surveillance, commercial delivery, and agricultural monitoring. In North America, over 60% of new UAV deployments in 2024 utilized carbon fiber airframes for extended operational efficiency. Industrial sectors are also leveraging carbon fiber UAVs for infrastructure inspections, resulting in a 15% reduction in inspection downtime. Additionally, hybrid-electric propulsion integrated with carbon fiber frames has enhanced energy efficiency, allowing UAVs to operate continuously for 6–8 hours, compared to traditional materials which average 4–5 hours. The combination of durability, weight reduction, and improved aerodynamics makes carbon fiber UAVs a preferred solution, directly boosting adoption rates across commercial, defense, and industrial applications.

High production costs of carbon fiber UAVs remain a critical restraint on market expansion. Carbon fiber materials are expensive, accounting for up to 30% of total UAV production costs, limiting affordability for small and medium enterprises. Manufacturing complexities, including precision molding and curing processes, require specialized equipment and skilled labor, which adds to operational expenses. In addition, carbon fiber supply chain limitations create potential bottlenecks, especially for large-scale production in Asia-Pacific and South America. Regulatory constraints, such as UAV airspace restrictions and certification requirements, further limit deployment in certain regions. These factors, combined with ongoing maintenance challenges for composite airframes, restrict wider adoption despite high demand for high-performance UAVs.

Integration of AI-powered navigation and hybrid-electric propulsion presents significant growth opportunities for the Carbon Fiber UAV Market. AI-based flight systems enhance route optimization, collision avoidance, and predictive maintenance, improving operational efficiency by up to 20%. Hybrid propulsion extends flight duration, allowing UAVs to carry heavier payloads for logistics, agricultural spraying, and industrial inspections. Emerging commercial applications, including e-commerce delivery and environmental monitoring, are creating new revenue streams, particularly in North America and Asia-Pacific. Investment in R&D for carbon fiber UAVs capable of autonomous missions and long-range flights is increasing, enabling companies to offer specialized UAV solutions. Additionally, partnerships between AI developers and UAV manufacturers are expanding market reach and supporting the introduction of next-generation UAV platforms for complex missions.

Regulatory compliance and airspace restrictions present significant challenges to the Carbon Fiber UAV Market. UAV operations must adhere to varying national and international aviation guidelines, including altitude limits, flight permissions, and operational safety standards. In Europe, stringent certification and ESG regulations require manufacturers to demonstrate environmentally responsible production of carbon fiber UAVs. In emerging markets, lack of standardized UAV policies restricts cross-border operations and commercial deployment. Companies also face challenges in data privacy compliance when UAVs collect imagery for surveillance and logistics applications. These factors contribute to operational delays, increased administrative costs, and limited scalability for commercial UAV services, constraining rapid market adoption despite technological advancements.

• Increasing Adoption of Hybrid-Electric Propulsion: Hybrid-electric UAVs are gaining traction, with over 28% of newly deployed carbon fiber UAVs in 2024 featuring hybrid propulsion systems. These UAVs demonstrate up to 30% longer flight durations and 15% higher payload efficiency compared to purely battery-powered systems, making them preferred in logistics and industrial inspection applications.

• AI-Enabled Autonomous Flight Systems: AI-assisted navigation and autonomous flight controls are now integrated into 35% of operational carbon fiber UAVs globally. This trend has improved route optimization by 22%, reduced operator intervention by 40%, and enhanced predictive maintenance, particularly in North America and Europe, where complex surveillance and mapping missions demand high precision and reliability.

• Expansion in Commercial and Agricultural Applications: The commercial and agricultural sectors account for 42% of carbon fiber UAV deployment. UAVs are increasingly used for precision spraying, crop monitoring, and e-commerce delivery. In 2024 alone, agricultural UAV missions increased by 18%, driven by improvements in flight endurance and lightweight composite materials enabling larger payload capacities.

• Integration of Advanced Carbon Fiber Composites: UAV manufacturers are adopting high-modulus carbon fiber composites to reduce weight by 20–25% while improving structural strength by up to 30%. This trend supports longer mission times, higher payload capacities, and better energy efficiency. Asia-Pacific and North America lead adoption, with over 50% of new UAVs in these regions using advanced carbon fiber structures for industrial and defense applications.

The Carbon Fiber UAV Market is segmented by type, application, and end-user, each providing insights into adoption patterns and growth potential. By type, fixed-wing, rotary-wing, and hybrid UAVs are analyzed, highlighting structural differences and mission capabilities. Application segmentation focuses on defense, commercial, agriculture, and industrial inspection, reflecting operational priorities and deployment trends. End-user insights consider defense agencies, logistics providers, agricultural operators, and infrastructure monitoring firms, revealing adoption behavior and technology integration levels. Across regions, fixed-wing UAVs dominate long-range surveillance, while rotary-wing models are preferred for inspection and delivery tasks, demonstrating diverse operational applications and market adaptability.

Fixed-wing UAVs currently account for 45% of adoption due to their long endurance and ability to cover extended flight paths efficiently, particularly for defense and large-scale agricultural missions. Rotary-wing UAVs hold 35% of the market, valued for their vertical take-off, hovering capability, and suitability for localized inspections and delivery tasks. Hybrid UAVs, combining rotary and fixed-wing features, are the fastest-growing segment, with adoption rising rapidly as autonomous navigation systems and hybrid propulsion enhance flight duration and payload efficiency. The remaining 20% includes specialized UAV types like tethered and VTOL models, serving niche applications such as border surveillance or urban infrastructure monitoring.

Defense applications dominate the Carbon Fiber UAV Market, accounting for 40% of adoption, driven by surveillance, reconnaissance, and intelligence-gathering missions requiring high endurance and reliability. Commercial delivery and logistics UAVs comprise 30%, with usage expanding in e-commerce and last-mile delivery operations. Agricultural applications represent 20%, focusing on precision spraying, crop monitoring, and yield optimization, while industrial inspections make up 10%, targeting infrastructure and energy sector assets. The fastest-growing application is commercial delivery, where autonomous UAVs integrated with AI route optimization have reduced operational inefficiencies by 15% and expanded operational coverage by 20%.

Defense agencies are the leading end-users of carbon fiber UAVs, representing 42% of market adoption due to high operational demands for surveillance and tactical missions. The fastest-growing end-user segment is logistics and e-commerce providers, leveraging autonomous UAVs for delivery and warehouse management, increasing operational efficiency by 20%. Agricultural operators account for 28%, employing UAVs for crop monitoring and spraying, while industrial and infrastructure inspection firms represent 18%, utilizing UAVs for asset evaluation and hazard detection. Other end-users, including research institutions and environmental monitoring agencies, make up the remaining 12%, deploying UAVs for specialized missions.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

North America leads in volume with over 5,000 carbon fiber UAV units deployed in defense and commercial sectors in 2024, while Asia-Pacific recorded 3,800 units but demonstrates rapid adoption driven by industrial and agricultural applications. Europe follows with 28% adoption, emphasizing regulatory-compliant UAV solutions. South America and Middle East & Africa together contribute 12% of the market, driven by energy, mining, and infrastructure monitoring. Advanced manufacturing, AI-enabled flight systems, and hybrid propulsion adoption are transforming operational efficiency, with North American UAVs achieving 25–30% longer flight times, while Asian UAVs improve delivery and inspection efficiency by 20%. Regional consumer behavior varies, with North American enterprises favoring high-endurance UAVs, European operators prioritizing regulatory-compliant platforms, and Asia-Pacific users leveraging cost-effective, high-volume UAV solutions for e-commerce and agriculture.

How are high-endurance UAVs shaping operational efficiency in North America?

North America holds 38% of the Carbon Fiber UAV Market, led by extensive defense, logistics, and agricultural deployment. The region benefits from government initiatives supporting UAV integration, including regulatory approvals for autonomous operations and FAA modernization programs. Technological advancements such as hybrid-electric propulsion, AI-driven navigation, and high-modulus carbon fiber structures enhance flight endurance by 25% and payload capacity by 15%. Local players like AeroVironment are expanding UAV platforms for tactical and commercial applications, including precision agriculture and border surveillance. Enterprises in healthcare, finance, and logistics adopt UAV solutions at higher rates, with over 60% of new UAV deployments in 2024 utilizing autonomous features. Digital transformation trends, including cloud-based fleet management and predictive maintenance, further increase operational efficiency and reduce downtime, reinforcing North America’s market leadership.

What drives Europe’s demand for advanced and compliant UAV solutions?

Europe represents 28% of the Carbon Fiber UAV Market, with Germany, the UK, and France leading adoption. Regulatory bodies such as EASA enforce strict UAV certification and safety standards, driving demand for explainable and compliant carbon fiber UAV platforms. Adoption of AI-enabled autonomous flight, hybrid propulsion, and modular designs is rising, particularly for logistics, infrastructure inspections, and defense surveillance. Local players like Airbus Defense and Space have deployed UAVs capable of operating in adverse weather conditions and urban environments, improving mission reliability by 18%. European consumer behavior emphasizes regulatory compliance and sustainable operations, with over 40% of enterprises integrating UAVs into operational frameworks that meet environmental and safety guidelines.

How is rapid industrialization influencing UAV adoption in Asia-Pacific?

Asia-Pacific accounts for 27% of global carbon fiber UAV deployments, with China, India, and Japan as the top-consuming countries. Infrastructure expansion, agricultural modernization, and growing e-commerce logistics are driving adoption. UAV manufacturers are focusing on cost-effective carbon fiber platforms with AI-assisted flight control and hybrid propulsion. Local players, such as DJI, are deploying UAVs capable of 8-hour missions and payloads up to 20 kg for surveillance, delivery, and precision agriculture. Regional consumer behavior highlights widespread adoption in commercial and agricultural sectors, with enterprises leveraging UAVs to optimize operational efficiency and support rapid digital transformation.

What opportunities exist for UAV deployment in South America’s industrial sectors?

South America holds approximately 7% of the Carbon Fiber UAV Market, with Brazil and Argentina leading adoption. Demand is driven by infrastructure inspection, mining operations, and agricultural applications. Government incentives and trade policies encourage UAV integration for logistics and energy monitoring. Local players are deploying UAVs to enhance border surveillance and industrial mapping, achieving up to 15% efficiency gains. Regional consumer behavior favors UAVs for precision agriculture and industrial inspections, while language localization and media monitoring solutions further stimulate adoption.

How is regional demand for UAVs shaped by energy and defense sectors?

Middle East & Africa contribute 5% of the Carbon Fiber UAV Market, with the UAE and South Africa leading adoption. Demand is concentrated in oil & gas monitoring, construction oversight, and defense surveillance. Technological modernization, including AI navigation and hybrid propulsion, is being implemented to improve operational efficiency by 20%. Local players deploy UAVs for infrastructure inspections and border monitoring, reducing manual intervention and inspection downtime. Regional consumer behavior emphasizes industrial and defense applications, with enterprises increasingly adopting UAV platforms to enhance safety and reduce operational costs.

United States – 38% market share; dominance driven by high production capacity and advanced defense and commercial UAV integration.

China – 25% market share; strong adoption in e-commerce, agriculture, and industrial applications supports market leadership.

The Carbon Fiber UAV market is moderately fragmented, with over 60 active global competitors ranging from specialized UAV manufacturers to integrated aerospace solution providers. The top five companies—AeroVironment, DJI, Northrop Grumman, Lockheed Martin, and Airbus Defense and Space—collectively hold approximately 52% of the market, demonstrating significant influence in technology innovation and market deployment. Strategic initiatives are shaping competition, including AeroVironment’s expansion into hybrid-electric UAVs, DJI’s investment in AI-enabled flight systems, and Northrop Grumman’s defense-focused UAV collaborations. Product launches in 2023–2024 have introduced long-endurance UAVs capable of payloads exceeding 20 kg, while Airbus Defense and Space enhanced modular UAV platforms for industrial inspections. Innovation trends such as autonomous navigation, hybrid propulsion, and advanced carbon fiber composites are being adopted widely to differentiate products. Mergers and partnerships, such as joint ventures between North American and Asian UAV firms, are enabling market expansion in logistics, agriculture, and defense sectors. Overall, competition emphasizes technological advancement, operational efficiency, and regional customization, with North America and Asia-Pacific leading in enterprise and commercial adoption.

Lockheed Martin

Airbus Defense and Space

Boeing

Parrot

Elbit Systems

Textron Systems

Yuneec

The Carbon Fiber UAV market is experiencing significant technological advancements that are shaping the future of drone performance and applications. One of the most impactful innovations is the use of lightweight carbon fiber composites, which are increasing UAV strength while reducing weight. This allows for longer flight durations, higher payload capacities, and improved energy efficiency. In fact, the integration of advanced composite materials in UAV structures has led to a 30% increase in overall flight endurance compared to traditional materials. Another key technological development is the incorporation of AI and machine learning for autonomous flight and navigation. AI-driven systems are now capable of handling real-time decision-making during complex operations such as obstacle avoidance, flight path optimization, and environmental sensing. This technology is enabling UAVs to operate in increasingly dynamic environments such as urban areas and complex industrial settings.

Furthermore, hybrid propulsion systems are gaining traction within the market. These systems combine electric motors with internal combustion engines, offering extended range and power efficiency. Hybrid UAVs can operate for hours on end, making them suitable for applications such as surveillance, agriculture, and long-range logistics. The trend towards hybrid propulsion is seen in high-demand sectors that require continuous operation without recharging. Advancements in remote sensing technologies are also enhancing the operational capabilities of UAVs. High-resolution cameras, LiDAR, and multispectral sensors are now standard features for UAVs used in sectors such as agriculture, construction, and environmental monitoring. These technologies are allowing for more precise data collection and enhanced analytics.

Lastly, the development of 5G connectivity and low-Earth orbit satellite communication is facilitating real-time data transmission and remote UAV control, especially in areas where traditional communication networks are not available. This connectivity is opening up new markets, such as long-distance cargo delivery and remote inspections.

In 2023, AeroVironment successfully completed testing of its latest hybrid-electric UAV, capable of carrying payloads up to 20 kg for 12+ hours. This new model was designed to improve operational efficiency in long-range surveillance applications, expanding its role in defense and security sectors.

DJI unveiled its latest high-performance drone model, featuring carbon fiber composites and an upgraded AI-powered flight control system. The drone, launched in late 2023, is optimized for agricultural surveillance and inspection services, offering improved endurance and real-time data analytics capabilities.

In early 2024, Northrop Grumman developed an autonomous UAV using carbon fiber and advanced hybrid propulsion technology. This UAV has been integrated into military reconnaissance missions, significantly reducing operational costs while improving both range and reliability in harsh environments.

Airbus Defense and Space introduced an upgraded UAV platform designed for industrial inspections. The carbon fiber-based design reduces the weight by 40%, allowing for more efficient energy consumption. The platform integrates advanced sensor systems, enhancing its capabilities for inspecting high-rise buildings and energy infrastructure.

The Carbon Fiber UAV Market Report provides a comprehensive analysis of the current market landscape, focusing on key segments, technologies, and regions driving growth. It covers the latest advancements in carbon fiber composite materials, highlighting their impact on UAV strength, payload capacity, and flight duration. The report also examines the role of emerging technologies such as AI-driven flight controls, hybrid propulsion systems, and high-resolution remote sensing capabilities, which are reshaping the capabilities of UAVs across various industries. Geographically, the report delves into market trends and growth projections across regions, with a particular emphasis on North America, Europe, and Asia-Pacific, the leading regions in both technological adoption and industrial applications. It provides insights into the increasing use of carbon fiber UAVs in sectors such as defense, agriculture, environmental monitoring, and infrastructure inspection.

In addition to traditional applications, the report highlights emerging uses in logistics and surveillance, especially in industries demanding long flight durations and high payloads. The rise of hybrid propulsion systems and the integration of 5G and satellite communication technologies are expected to further open up new opportunities for market expansion. Furthermore, the report explores niche markets and applications where carbon fiber UAVs are gaining traction, such as remote sensing in environmental science and precision agriculture. This comprehensive outlook ensures stakeholders understand both the current state and future trajectory of the Carbon Fiber UAV market.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 4338.3 Million |

Market Revenue in 2032 | USD 8270.9 Million |

CAGR (2025 - 2032) | 8.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types:

By Application:

By End-User:

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | AeroVironment, DJI, Northrop Grumman, Lockheed Martin, Airbus Defense and Space, Boeing, Parrot, Elbit Systems, Textron Systems, Yuneec |

Customization & Pricing | Available on Request (10% Customization is Free) |