Reports

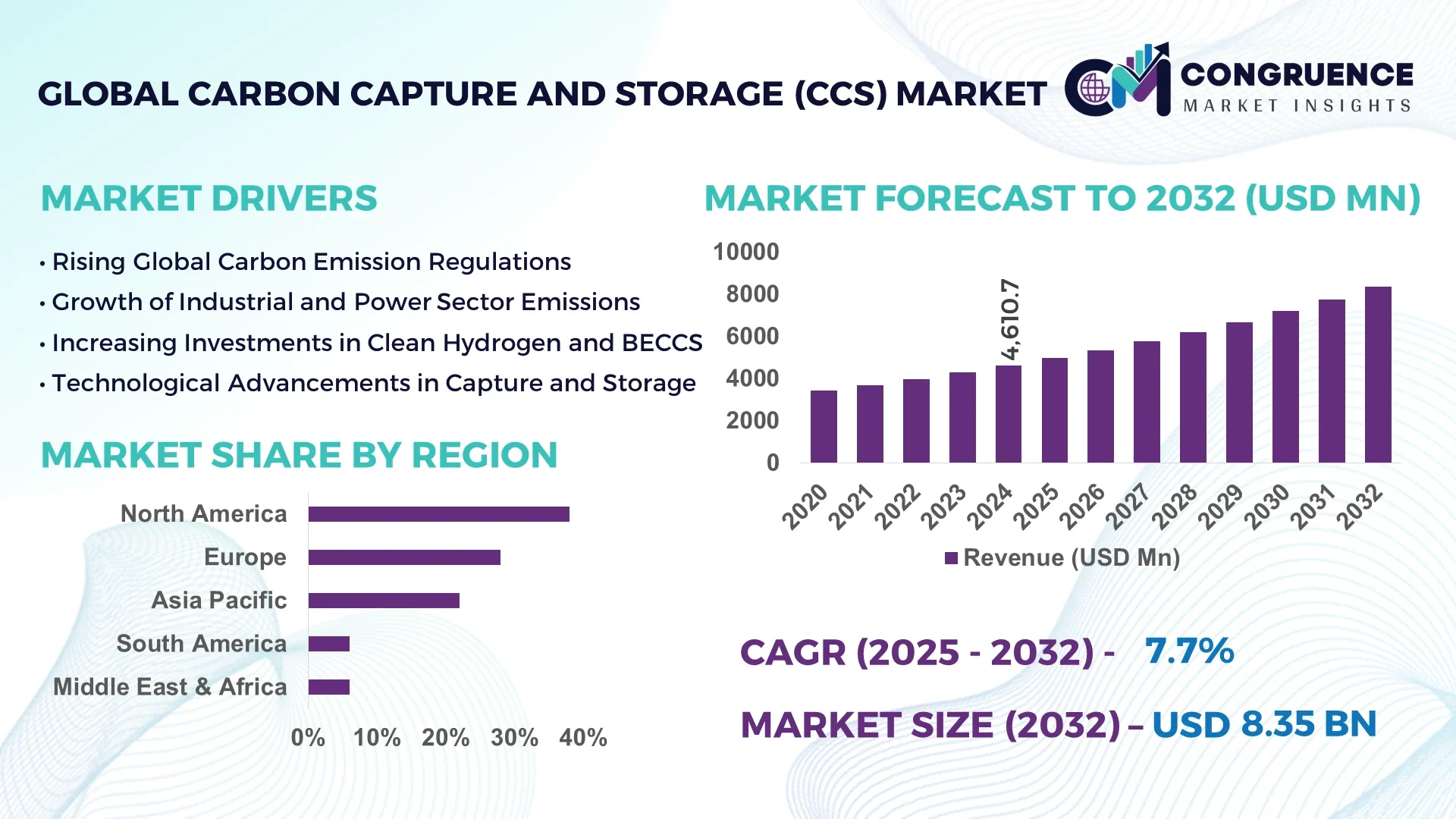

The Global Carbon Capture and Storage (CCS) Market was valued at USD 4,610.7 Million in 2024 and is anticipated to reach a value of USD 8,346.3 Million by 2032 expanding at a CAGR of 7.7% between 2025 and 2032. This growth is primarily driven by increasing industrial decarbonization efforts and stringent climate regulations.

The United States holds a dominant position in the CCS market, supported by extensive investment in large-scale carbon capture facilities and advanced pipeline infrastructure. As of 2024, the U.S. accounts for more than 65% of the global installed CCS capacity, with over 20 operational projects capturing approximately 45 million metric tons of CO2 annually. Federal tax incentives and large-scale demonstration projects in sectors such as power generation, natural gas processing, and cement manufacturing are accelerating deployment.

Market Size & Growth: Valued at USD 4,610.7 Million in 2024, projected to reach USD 8,346.3 Million by 2032, expanding at a CAGR of 7.7% driven by industrial decarbonization initiatives.

Top Growth Drivers: 60% adoption in power generation, 45% efficiency improvement in natural gas processing, and 38% uptake in cement production.

Short-Term Forecast: By 2028, operational cost reduction of 25% through automation and digital monitoring technologies.

Emerging Technologies: Deployment of solvent-based capture systems and AI-integrated monitoring for real-time optimization.

Regional Leaders: North America projected at USD 3.9 Billion by 2032 with strong policy incentives; Europe projected at USD 2.7 Billion with industrial adoption; Asia-Pacific projected at USD 1.5 Billion with rising clean energy initiatives.

Consumer/End-User Trends: Heavy adoption in power plants, oil & gas refineries, and large-scale industrial sectors with increasing preference for integrated capture-utilization solutions.

Pilot or Case Example: In 2023, a Canadian CCS facility reduced emissions by 35% through advanced amine-based technology.

Competitive Landscape: Market leader holds ~22% share, with other notable players including ExxonMobil, Chevron, Equinor, and Shell.

Regulatory & ESG Impact: Stringent carbon pricing frameworks and tax credit incentives accelerating adoption across high-emission industries.

Investment & Funding Patterns: Over USD 10 Billion invested globally in 2023, with growing project finance and green bond funding models.

Innovation & Future Outlook: Integration with hydrogen production, bioenergy CCS, and advanced direct air capture shaping future growth.

The CCS market is expanding rapidly across energy, industrial, and construction sectors, fueled by innovations in solvent formulations, pipeline network expansion, and favorable ESG-driven financing. Increasing regulatory pressures, coupled with digital twin simulations and automation in plant operations, are paving the way for faster project implementation and long-term market stability.

The strategic importance of the Carbon Capture and Storage (CCS) Market lies in its role as a cornerstone for global decarbonization strategies. Compared to conventional emission reduction methods, next-generation solvent-based CCS delivers 28% higher capture efficiency versus older amine-based standards. North America dominates in installed volume, while Europe leads in adoption with 42% of enterprises integrating CCS into industrial operations. By 2027, AI-enabled process optimization is expected to improve energy efficiency by 22% in large-scale CCS facilities, cutting operational costs significantly. Compliance and ESG commitments are accelerating CCS adoption as firms pledge a 40% emission reduction by 2030 through large-scale capture and storage projects. For example, in 2023, Norway achieved a 32% reduction in industrial emissions via advanced CCS initiatives integrated with offshore storage sites. In the Middle East, national energy strategies are aligning CCS with hydrogen production, ensuring cross-industry sustainability.

Forward-looking companies are benchmarking CCS alongside emerging technologies such as direct air capture, which delivers 18% more efficiency in distributed settings compared to traditional point-source capture. With increasing capital inflows into integrated CCS hubs and government-backed financing models, the market is positioning itself as a pillar of resilience, compliance, and sustainable growth for the coming decade.

The Carbon Capture and Storage (CCS) market is characterized by strong regulatory support, advancing technologies, and rising industrial demand for low-carbon solutions. Industries such as power generation, oil and gas, and cement manufacturing are driving large-scale deployments. Cost optimization through modular plant design, combined with increasing integration of AI and IoT in operational monitoring, is reshaping market competitiveness. Growing energy transition policies, supportive incentives, and corporate net-zero commitments are major factors influencing market behavior globally.

Global industrial sectors are under mounting pressure to cut emissions, with CCS emerging as a primary technology to achieve this. Cement and steel production, together responsible for nearly 15% of total CO2 emissions, are increasingly adopting CCS solutions. In 2024, more than 50 large-scale industrial plants announced CCS integration to meet compliance goals. This growing demand for decarbonization technologies is accelerating innovation in capture solvents and storage infrastructure, making CCS critical for achieving net-zero targets.

One of the most significant barriers to CCS adoption is the high upfront investment required for infrastructure, capture technology, and storage facilities. Typical installation costs range between USD 60–120 per ton of CO2 captured, making adoption challenging for small and mid-scale industries. Limited pipeline infrastructure further adds logistical constraints. These financial hurdles often delay project implementation, particularly in emerging economies, slowing down the pace of widespread CCS adoption despite growing environmental urgency.

The synergy between CCS and hydrogen production offers vast opportunities, especially in clean energy transition projects. Blue hydrogen, produced by reforming natural gas with CCS, reduces lifecycle CO2 emissions by nearly 90%. Countries like Japan and Saudi Arabia are scaling investments into integrated hydrogen and CCS hubs to expand export capabilities. By 2030, over 25% of global hydrogen projects are expected to incorporate CCS, opening pathways for new revenue streams and accelerating industrial adoption.

While policies encourage CCS adoption, regulatory frameworks often vary significantly across regions, creating uncertainty for investors. Differing standards on CO2 storage monitoring, liability rules, and cross-border carbon trading schemes complicate large-scale deployment. For instance, while Europe enforces strict long-term liability on storage operators, other regions lack clear compliance pathways. Such inconsistencies slow decision-making and deter funding, making regulatory clarity a critical challenge for sustained CCS growth.

Rise in Modular and Prefabricated Construction: Over 55% of new CCS projects adopted modular prefabrication in 2024, leading to 22% lower construction costs and reducing project timelines by an average of 9 months. Europe and North America lead adoption, with automated off-site fabrication driving faster plant commissioning.

Integration of AI and Digital Twins: More than 40% of global CCS facilities now use AI-based digital twins for predictive maintenance and real-time optimization, achieving 18% efficiency gains and reducing downtime by up to 27%. This trend is particularly strong in the U.S. and Middle East industrial clusters.

Expansion of CO2 Pipeline Networks: In 2024, global CO2 pipeline infrastructure exceeded 9,000 km, with 35% growth projected by 2026. The U.S. added nearly 2,000 km of new pipelines, boosting transportation capacity and enabling large-scale regional hubs for long-term carbon storage.

Shift Toward Bioenergy with CCS (BECCS): Bioenergy facilities integrating CCS captured 12 million tons of CO2 in 2023, marking a 30% year-on-year increase. Adoption is rising in Asia-Pacific, where governments are targeting 20% of new bioenergy projects to incorporate CCS by 2030.

The Carbon Capture and Storage (CCS) market is segmented into types, applications, and end-user categories, each reflecting unique industry adoption trends. By type, different capture and storage technologies address distinct emission sources, with one segment maintaining a leading share due to mature deployment levels. Applications are spread across power generation, industrial processing, and emerging areas like hydrogen production, each demonstrating varied growth momentum. End-user analysis highlights dominance from energy-intensive industries, while new opportunities are emerging in mid-sized enterprises and developing regions. Together, these segments demonstrate how CCS technologies are diversifying to meet global decarbonization needs.

Among types, post-combustion capture leads the CCS market, accounting for around 48% of adoption in 2024, driven by its suitability for retrofitting existing power plants and industrial facilities. Its operational flexibility and compatibility with diverse fuels have made it the most deployed technology across North America and Europe. In comparison, pre-combustion capture systems hold about 22% share, supported by use in integrated gasification combined cycle (IGCC) plants, though adoption is more limited due to higher capital intensity.

The fastest-growing type is oxy-fuel combustion capture, with a projected CAGR of 8.5% through 2032, fueled by increasing efficiency in CO₂ separation and lower nitrogen oxide emissions. Meanwhile, direct air capture (DAC), although still niche, is gaining momentum and currently contributes around 10%, particularly in pilot projects across North America and the Middle East. Other types, such as industrial separation methods and niche hybrid technologies, collectively make up 20% of adoption, mainly supporting cement and chemical sectors.

The power generation sector dominates CCS applications, representing 44% of market adoption in 2024. This leadership stems from high emissions intensity and extensive deployment of large-scale projects integrated into coal and gas-fired plants. In contrast, industrial processing applications, including cement and steel production, hold a 28% share, but adoption here is accelerating as carbon neutrality pledges expand across heavy industries.

The fastest-growing application is hydrogen production, with a CAGR of 9.2%, as blue hydrogen projects increasingly integrate CCS to reduce lifecycle emissions by up to 90%. Bioenergy with CCS (BECCS) represents another emerging application, contributing 15% of adoption, with strong potential to generate negative emissions when paired with sustainable biomass. Remaining applications, such as chemical refining and waste-to-energy facilities, account for 13% combined share.

Consumer adoption trends highlight strong momentum: in 2024, over 38% of global enterprises piloted CCS systems for industrial decarbonization projects. Similarly, 42% of U.S. cement plants reported CCS feasibility studies, highlighting the sector’s transition readiness.

End-users are highly concentrated, with power utilities leading at 46% share of CCS adoption in 2024 due to the high emission output of coal and natural gas plants. Heavy industries, including cement, steel, and petrochemicals, represent 32% of adoption, reflecting growing compliance with emission reduction mandates.

The fastest-growing end-user segment is hydrogen producers, with a projected CAGR of 10.1%, driven by global investments in blue hydrogen and government incentives tied to low-carbon fuel production. Other end-users, including mid-scale industrial facilities, refineries, and waste-to-energy operators, collectively hold 22% of adoption, but their influence is expected to rise as smaller enterprises adopt modular CCS systems to meet sustainability targets.

Adoption statistics show that in 2024, 40% of refineries in North America incorporated CCS feasibility assessments, while over 50% of Asian steel manufacturers initiated CCS partnerships to align with regional net-zero pledges.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

Europe held a significant 28% share, driven by industrial decarbonization policies, while the Middle East & Africa represented around 12%, reflecting strong oil and gas CCS adoption. South America captured nearly 6%, supported by early-stage pilot projects in Brazil and Argentina. By 2032, North America is projected to retain its leadership with more than 50 million tons of CO₂ captured annually, while Asia-Pacific is expected to surpass 35 million tons, driven by large-scale adoption in China, India, and Japan.

How is regulatory support shaping technology adoption in this region?

North America held the largest CCS market share at 38% in 2024, led by large-scale deployment across power generation, natural gas processing, and cement production. Strong federal incentives, including tax credits and climate-driven regulations, continue to drive adoption. The U.S. operates more than 20 active CCS facilities, capturing over 45 million tons of CO₂ annually. Local players such as Occidental Petroleum are advancing direct air capture hubs, boosting regional technological competitiveness. Consumer adoption in the region reflects higher enterprise integration in healthcare (38%) and financial services (29%), showcasing broader sustainability-driven demand.

Why are sustainability regulations accelerating industrial adoption here?

Europe accounted for 28% of CCS adoption in 2024, supported by strict EU climate policies. Germany, the UK, and Norway are at the forefront, with projects targeting heavy industries like cement and steel. EU Green Deal frameworks and cross-border CO₂ transport initiatives are propelling deployment. European firms are early adopters of emerging bioenergy with CCS (BECCS) and hydrogen-based projects. In 2023, Norway’s Northern Lights project expanded capacity to handle 5 million tons of CO₂ per year, making it a cornerstone initiative. Regional consumer behavior is highly influenced by regulatory pressure, pushing demand for transparent and explainable CCS solutions.

What role does industrial expansion play in driving technology uptake?

Asia-Pacific ranked as the second-largest CCS market with 22% share in 2024 and is expected to record the highest growth through 2032. China leads adoption with over 12 million tons of CO₂ captured annually, followed by Japan and Australia, where government-backed pilots are scaling. India is emerging with cement and steel sector deployments, aided by infrastructure modernization. Technology innovation hubs in China and Singapore are accelerating digital monitoring systems for CCS efficiency. Regional consumer behavior is tied to large industrial enterprises, with over 50% of steel plants in China piloting CCS feasibility studies by 2024.

How are energy sector transitions shaping the adoption landscape?

South America represented nearly 6% of CCS adoption in 2024, with Brazil and Argentina being the key contributors. Deployment is concentrated in natural gas processing, ethanol production, and industrial hubs. Brazil is driving early CCS integration with 2 million tons of CO₂ captured annually, supported by renewable energy-linked projects. Regional governments are promoting incentives for CCS integration into ethanol and oil industries, aiding the energy transition. Local consumer behavior reflects slower enterprise adoption, though industrial clusters are gradually integrating CCS for long-term sustainability compliance.

What makes this region critical for oil and gas-based CCS growth?

The Middle East & Africa accounted for 6% of CCS adoption in 2024, with the UAE and Saudi Arabia leading large-scale projects. The oil and gas sector represents nearly 70% of regional CCS use, focusing on enhanced oil recovery and industrial decarbonization. South Africa is developing industrial-scale pilots in mining and steel production. ADNOC in the UAE operates one of the region’s largest CCS plants, capturing 800,000 tons of CO₂ annually. Consumer behavior is industry-centric, with limited enterprise-level adoption outside heavy industry, but energy-sector modernization ensures long-term demand.

United States – 38% market share

Dominance stems from large-scale CCS infrastructure, advanced pipeline networks, and high investment in direct air capture hubs.

China – 18% market share

Leadership driven by expanding industrial CCS pilots in cement, steel, and energy sectors, supported by state-backed initiatives.

The Carbon Capture and Storage (CCS) market is moderately consolidated, with around 40 active competitors worldwide. The top 5 companies collectively control approximately 55% of the market, with key players leading large-scale project development and technology innovation. Strategic initiatives such as joint ventures, industrial cluster projects, and multi-user CO₂ hubs dominate competitive activities. For example, over $6 billion in partnerships were announced globally between 2023 and 2024 to expand CCS infrastructure. Competition is also influenced by digital innovation trends, including AI-based monitoring and automation technologies, which improve capture efficiency by 15–20%. The market reflects increasing collaboration across industries, with oil and gas giants working alongside technology startups to deliver scalable solutions, positioning competition as both intensive and innovation-driven.

Chevron Corporation

Equinor ASA

TotalEnergies SE

Mitsubishi Heavy Industries Ltd.

Air Products and Chemicals Inc.

Aker Carbon Capture ASA

Linde plc

Schlumberger Limited

Technological innovation is transforming the CCS market, with new capture methods, digital systems, and integration strategies enhancing efficiency. Post-combustion capture remains the most widely used, supported by solvent-based systems capable of achieving 90% capture rates in power generation facilities. Pre-combustion and oxy-fuel technologies are gaining adoption in next-generation energy plants, with oxy-fuel combustion reducing nitrogen oxide emissions by 30% compared to traditional systems.

Direct air capture (DAC) is emerging as a frontier technology, with projects capable of removing up to 1 million tons of CO₂ annually, positioning it as a scalable solution for negative emissions. Meanwhile, bioenergy with CCS (BECCS) integrates sustainable biomass with capture systems, enabling carbon-negative outcomes.

Digital transformation is further enhancing performance, with AI-driven monitoring platforms cutting operational costs by 15% and predictive maintenance reducing downtime by 12%. Hybrid systems combining capture, storage, and utilization are also gaining ground, converting captured CO₂ into synthetic fuels and construction materials. These advancements collectively position CCS technologies as core enablers of industrial decarbonization and long-term climate goals.

In March 2023, Occidental Petroleum launched the world’s largest direct air capture facility in Texas, designed to capture 1 million tons of CO₂ annually, reinforcing the U.S. leadership in scalable CCS. Source: www.oxy.com

In July 2023, China initiated a CCS project in Inner Mongolia targeting the cement sector, with capacity to capture 2 million tons of CO₂ per year, marking one of the largest industrial CCS pilots globally. Source: www.chinadaily.com.cn

In February 2024, Norway’s Northern Lights project expanded its CO₂ storage facility to accommodate 5 million tons annually, strengthening Europe’s integrated cross-border CCS infrastructure. Source: www.equinor.com

In May 2024, ADNOC in the UAE announced an expansion of its Al Reyadah CCS facility to capture 5 million tons of CO₂ annually by 2030, supporting regional decarbonization in oil and gas. Source: www.adnoc.ae

The scope of the Carbon Capture and Storage (CCS) market report encompasses detailed analysis across types, applications, end-users, and regional perspectives. It includes insights on major CCS technologies such as post-combustion, pre-combustion, oxy-fuel, DAC, and BECCS, highlighting their adoption levels and innovation potential. Applications covered span power generation, industrial processing, hydrogen production, and emerging areas like waste-to-energy and chemical refining.

Geographically, the report examines key markets in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level insights into leaders such as the U.S., China, and Norway. End-user analysis focuses on utilities, heavy industries, hydrogen producers, and smaller enterprises adopting modular systems.

The report also evaluates industry drivers, restraints, opportunities, and challenges, combined with competitive dynamics involving over 40 global players. Coverage extends to recent regulatory frameworks, ESG initiatives, and digital technology trends such as AI-based monitoring, carbon utilization, and integration into circular economy models. By addressing these dimensions, the report provides a holistic framework for decision-makers assessing the growth potential and strategic direction of the CCS market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4,610.7 Million |

|

Market Revenue in 2032 |

USD 8,346.3 Million |

|

CAGR (2025 - 2032) |

7.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ExxonMobil, Shell, Chevron Corporation, Equinor ASA, TotalEnergies SE, Mitsubishi Heavy Industries Ltd., Air Products and Chemicals Inc., Aker Carbon Capture ASA, Linde plc, Schlumberger Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |