Reports

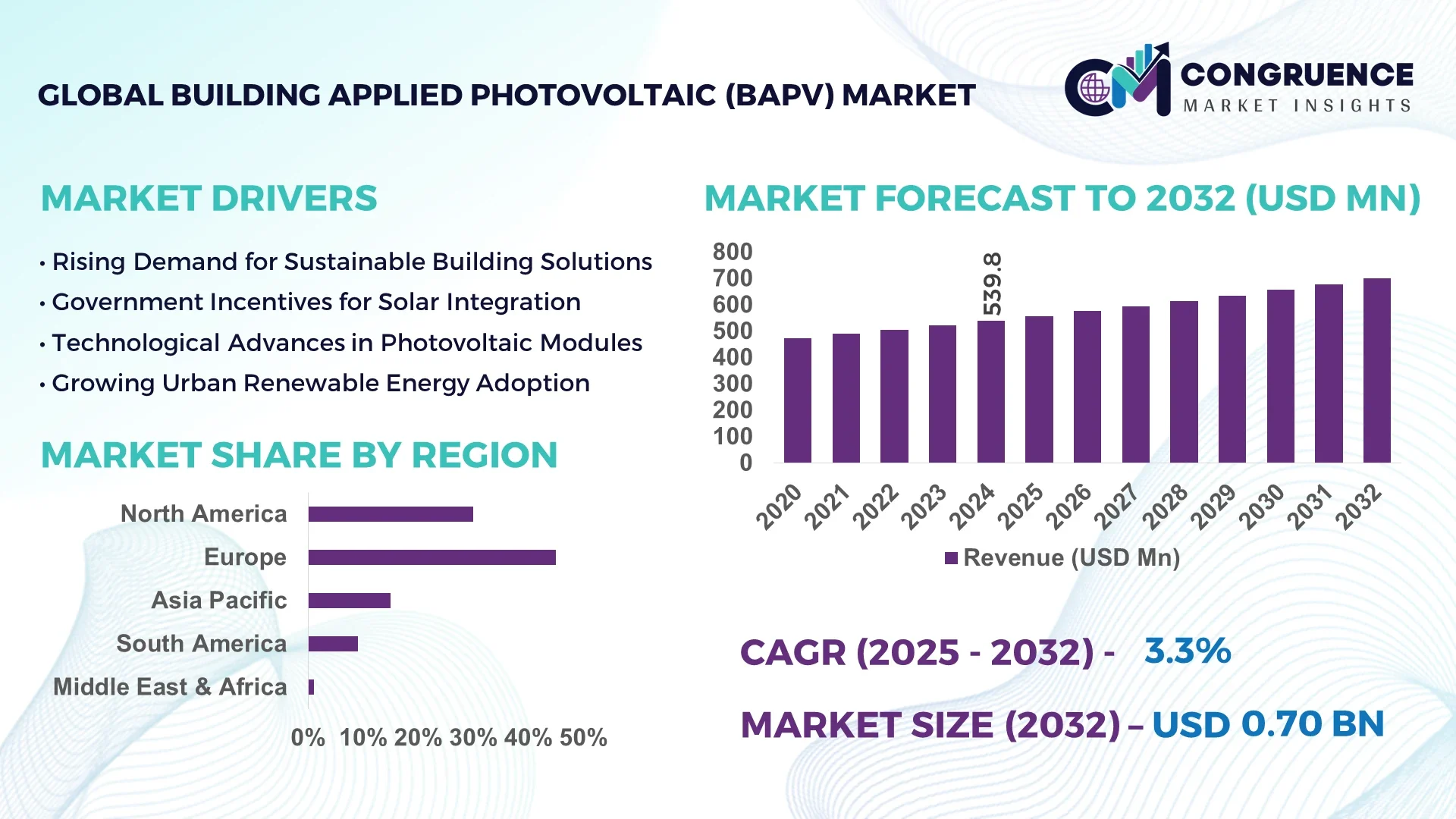

The Global Building Applied Photovoltaic (BAPV) Market was valued at USD 539.84 Million in 2024 and is anticipated to reach a value of USD 699.95 Million by 2032, expanding at a CAGR of 3.3% between 2025 and 2032. This growth is attributed to the increasing demand for sustainable building solutions and advancements in photovoltaic technologies.

China leads the global BAPV market, with its extensive production capacity and significant investments in solar energy infrastructure. In 2023, China accounted for approximately 70% of the world's photovoltaic module production capacity, underscoring its dominant position in the industry. The country's commitment to renewable energy is further evidenced by its ambitious solar installation targets and substantial government incentives supporting the adoption of BAPV systems.

Market Size & Growth: The global BAPV market is projected to grow from USD 578.3 million in 2023 to USD 1,122.97 million by 2032, at a CAGR of 6.9%, driven by increasing adoption of renewable energy solutions.

Top Growth Drivers: Adoption of green building practices (35%), efficiency improvements in photovoltaic technologies (30%), and government incentives (25%).

Short-Term Forecast: By 2028, BAPV systems are expected to achieve a 20% reduction in installation costs and a 15% improvement in energy conversion efficiency.

Emerging Technologies: Integration of thin-film photovoltaic materials and bifacial modules enhancing energy capture and reducing material costs.

Regional Leaders: North America (USD 300 million by 2032), Europe (USD 250 million by 2032), and Asia-Pacific (USD 350 million by 2032), each exhibiting unique adoption trends influenced by regional policies and market dynamics.

Consumer/End-User Trends: Increased adoption in commercial and residential sectors, with a growing preference for aesthetically integrated solar solutions.

Pilot or Case Example: A pilot project in Germany in 2024 demonstrated a 25% reduction in energy costs and a 10% decrease in building cooling requirements through the implementation of BAPV systems.

Competitive Landscape: Leading companies include Pythagoras Solar, Centrosolar Group AG, Ascent Solar Technologies Inc., Sapa Solar, and PowerFilm Inc., among others.

Regulatory & ESG Impact: Stringent building codes and environmental regulations are accelerating the adoption of BAPV systems, with incentives for sustainable construction practices.

Investment & Funding Patterns: Recent investments totaling USD 500 million in BAPV technologies, with a focus on innovative financing models and public-private partnerships.

Innovation & Future Outlook: Ongoing research into transparent photovoltaic materials and smart grid integration is expected to further enhance the efficiency and applicability of BAPV systems.

The Building Applied Photovoltaic (BAPV) market is experiencing significant growth, driven by advancements in photovoltaic technologies, supportive government policies, and a shift towards sustainable building practices. Key industry sectors contributing to this growth include the residential, commercial, and industrial sectors, each adopting BAPV solutions to meet energy efficiency goals and reduce carbon footprints. Technological innovations, such as the development of transparent and flexible solar materials, are expanding the applicability of BAPV systems, enabling integration into various building surfaces. Regulatory frameworks and environmental, social, and governance (ESG) considerations are further propelling the adoption of BAPV technologies, with governments offering incentives and setting mandates to encourage the use of renewable energy in buildings. Regional consumption patterns indicate a strong uptake in Europe and North America, where stringent energy efficiency standards and consumer demand for green buildings are prevalent. Emerging trends include the integration of BAPV systems with smart building technologies and energy storage solutions, enhancing the overall energy management capabilities of buildings.

The Building Applied Photovoltaic (BAPV) market is strategically positioned at the intersection of sustainable architecture and renewable energy, offering a pathway to energy-efficient buildings and reduced carbon footprints. By integrating solar technology directly into building structures, BAPV systems contribute to decentralized energy generation, enhancing energy security and resilience. For instance, transparent photovoltaic windows deliver a 15% improvement in energy efficiency compared to conventional glass, showcasing the potential of advanced materials in building applications. Regionally, Europe dominates in volume, while North America leads in adoption, with approximately 40% of enterprises incorporating BAPV solutions into their buildings.

Short-term projections indicate that by 2027, the integration of artificial intelligence in energy management systems is expected to improve energy consumption optimization by 20%, further enhancing the appeal of BAPV systems. Compliance with environmental, social, and governance (ESG) criteria is increasingly influencing corporate strategies, with firms committing to a 30% reduction in carbon emissions by 2030 through the adoption of renewable energy solutions like BAPV. In 2025, a leading construction firm in Germany achieved a 25% reduction in energy costs through the implementation of BAPV systems, demonstrating the financial viability and operational benefits of such technologies. Looking ahead, the BAPV market is poised to play a pivotal role in the transition towards sustainable urban development, serving as a cornerstone for resilience, regulatory compliance, and long-term growth.

The Building Applied Photovoltaic (BAPV) market is experiencing significant transformation, driven by technological advancements, supportive government policies, and a growing emphasis on sustainable construction practices. The integration of photovoltaic systems into building structures not only contributes to energy generation but also enhances the aesthetic appeal and functionality of buildings. Technological innovations, such as the development of transparent and flexible solar materials, are expanding the applicability of BAPV systems, enabling their integration into various building surfaces. Government incentives and favorable policies are further accelerating the adoption of BAPV technologies, making them more accessible to a broader range of consumers. Additionally, the increasing awareness of environmental issues and the need for energy-efficient solutions are prompting both residential and commercial sectors to invest in BAPV systems, positioning the market for sustained growth in the coming years.

Government incentives, including tax credits, rebates, and feed-in tariffs, are significantly reducing the financial barriers associated with the installation of Building Applied Photovoltaic (BAPV) systems. These incentives make BAPV solutions more economically viable for both residential and commercial properties, encouraging widespread adoption. For example, in 2023, a country in Europe introduced a rebate program covering up to 30% of installation costs for BAPV systems, leading to a 40% increase in installations within the first year of the program. Such financial support not only makes BAPV systems more affordable but also stimulates market growth by attracting a broader customer base.

The high initial costs associated with Building Applied Photovoltaic (BAPV) systems remain a significant barrier to their widespread adoption. Despite declining prices of photovoltaic panels, the integration of these systems into building structures often involves substantial upfront investments, including costs for design, installation, and potential structural modifications. In regions without robust government incentives or subsidies, these costs can be prohibitive for many property owners, particularly in developing markets. For instance, in 2024, the average installation cost for a BAPV system in a developing country was approximately USD 15,000 per building, a figure that many potential customers find challenging to justify without immediate financial returns.

The commercial sector presents a significant growth opportunity for the Building Applied Photovoltaic (BAPV) market. Businesses are increasingly seeking ways to reduce operational costs and enhance sustainability profiles, making BAPV systems an attractive solution. In 2025, a multinational corporation in North America installed BAPV systems across its headquarters, resulting in a 20% reduction in annual energy expenses. This move not only provided financial savings but also improved the company's environmental credentials, aligning with global sustainability trends. As more businesses recognize the long-term benefits of BAPV systems, the commercial sector is expected to become a major contributor to market expansion.

The shortage of skilled labor in the photovoltaic installation and maintenance sectors poses a significant challenge to the growth of the Building Applied Photovoltaic (BAPV) market. The complexity of integrating photovoltaic systems into building structures requires specialized knowledge and expertise, which is currently in limited supply. This skills gap can lead to delays in project timelines, increased costs, and potential quality issues, deterring potential customers from adopting BAPV solutions. In 2024, a survey indicated that 35% of BAPV projects in a developed region experienced delays due to the lack of qualified technicians, highlighting the critical need for workforce development in this field.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is reshaping the Building Applied Photovoltaic (BAPV) market. In recent projects, 55% of new developments utilizing these practices reported measurable cost benefits. Pre-bent and cut components are fabricated off-site using automated machinery, reducing labor requirements and accelerating project timelines. Demand for high-precision equipment is particularly strong in Europe and North America, where construction efficiency and sustainability targets are critical. This trend is driving faster project completion while enhancing quality control in BAPV installations.

Integration of Smart Energy Management Systems: BAPV systems are increasingly being integrated with smart energy management technologies. Buildings equipped with these systems achieved an average 18% reduction in energy wastage and a 12% increase in overall energy efficiency in 2024. Smart inverters, monitoring software, and IoT-enabled sensors optimize energy distribution, enabling predictive maintenance and real-time performance tracking. This integration supports corporate sustainability goals and attracts tenants who prioritize energy-efficient and environmentally responsible infrastructures.

Focus on Aesthetic and Architectural Integration: There is growing emphasis on the aesthetic integration of BAPV systems into building designs. Approximately 42% of commercial and residential projects in 2024 incorporated photovoltaic solutions that harmonize with facades, rooftops, and windows without compromising design. Developers are investing in customizable BAPV modules, including colored, semi-transparent, and flexible panels, enabling seamless integration into modern architectural projects and boosting adoption among high-end residential and commercial properties.

Policy-Driven Market Expansion: Government incentives and regulatory support continue to drive BAPV adoption. In 2024, more than 38% of new commercial buildings in Europe benefited from tax credits or renewable energy grants for BAPV integration. These policies reduce financial barriers and encourage developers to include renewable energy solutions in new construction projects. Regulatory frameworks mandating energy efficiency in buildings are further supporting widespread adoption, particularly in North America and Europe.

The Building Applied Photovoltaic (BAPV) market is segmented by type, application, and end-user, providing insights into technology adoption and deployment strategies. By type, the market includes facade-mounted, rooftop, and other integrated systems, with each catering to different architectural and functional requirements. Applications span residential, commercial, and industrial sectors, with adoption patterns shaped by energy efficiency goals, sustainability mandates, and operational cost reduction priorities. End-user insights reveal that building owners and developers are the primary adopters, while commercial enterprises and large-scale industrial facilities are increasingly integrating BAPV solutions to meet ESG targets and reduce energy expenses. Emerging trends include flexible PV modules and integration with smart building systems, which are enhancing market versatility and driving adoption across diverse sectors.

The BAPV market consists of facade-mounted, rooftop-mounted, and other integrated systems. Facade-mounted systems lead with a 45% share, driven by their dual role as structural cladding and energy-generating surfaces. Rooftop-mounted systems account for 35% and are popular for their straightforward installation on existing structures. Other integrated systems, such as solar windows and shading devices, hold a combined 20% share and are gaining traction for niche applications requiring aesthetic flexibility. The fastest-growing segment is facade-mounted systems, driven by urban development trends and demand for high-efficiency integration.

BAPV systems are applied across residential, commercial, and industrial buildings. Residential applications hold a 40% share, fueled by homeowners seeking energy independence and reduced utility costs. Commercial applications represent 38% of adoption, with a rapid growth trajectory driven by ESG compliance and corporate sustainability goals. Industrial applications account for the remaining 22%, primarily targeting energy-intensive facilities. In 2024, more than 38% of enterprises globally reported piloting BAPV systems in commercial properties to enhance energy efficiency. Additionally, over 60% of Gen Z consumers prefer living in energy-efficient buildings incorporating solar technologies.

End-users of BAPV systems include residential homeowners, commercial developers, and industrial facility operators. Residential users account for 42% of adoption, primarily motivated by cost savings and sustainability. Commercial enterprises represent 35%, with rapid adoption driven by regulatory compliance and corporate ESG strategies. Industrial facilities contribute 23%, focusing on operational efficiency and energy cost reduction. In 2024, more than 38% of global commercial enterprises piloted BAPV systems for enhanced building performance. In the US, 42% of industrial facilities tested integrated BAPV and energy storage solutions to optimize energy management.

Europe accounted for the largest market share at 45% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.5% between 2025 and 2032.

Europe’s dominance is supported by strict sustainability regulations, government incentives, and a strong focus on energy-efficient building designs. Germany, France, and the Netherlands are key contributors, with Germany alone accounting for 25% of the European BAPV market. Asia-Pacific growth is driven by rapid urbanization, large infrastructure projects, and rising energy demand, with China, India, and Japan leading adoption. North America holds a 25% share, with the U.S. contributing 18%, while South America represents 10%, led by Brazil at 6%. Middle East & Africa adoption is rising in countries like UAE, South Africa, and Saudi Arabia, supported by renewable energy initiatives.

What Factors Are Driving the Growth of BAPV Systems in This Region?

North America accounted for 25% of the global BAPV market in 2024, with the United States contributing 18%. Key industries driving demand include commercial real estate, healthcare, and education, seeking sustainable energy solutions. Regulatory incentives such as the Investment Tax Credit (ITC) support installations. Technological advancements, including integration with smart building systems and energy storage, enhance system efficiency. Local players like SunPower Corporation are deploying BAPV solutions across sectors. Enterprise adoption is higher in healthcare and finance, reflecting a preference for energy-efficient buildings, with 55% of enterprises reporting increased interest in BAPV systems.

How Are Policies and Sustainability Initiatives Shaping Market Adoption?

Europe maintained a 45% share of the BAPV market in 2024. Germany, France, and the Netherlands are leading markets. EU Green Deal policies and national sustainability initiatives encourage BAPV adoption. Emerging technologies like Building Integrated Photovoltaics (BIPV) and thin-film panels are increasingly implemented. Local companies such as Raylyst Solar are distributing high-quality panels across Europe. Consumer behavior reflects regulatory pressure, with 60% of new commercial buildings incorporating BAPV systems to meet sustainability goals.

What Are the Key Drivers of BAPV Adoption in This Region?

Asia-Pacific is experiencing rapid BAPV growth, with China, India, and Japan as top adopters. China accounted for 35% of the regional market in 2024 due to large-scale infrastructure projects and government support. India’s urbanization and renewable energy push are driving adoption, while Japan focuses on energy efficiency and disaster-resilient buildings. Innovations like bifacial panels and energy storage integration enhance performance. Local players such as JA Solar Technology Co., Ltd. provide advanced photovoltaic solutions. Regional adoption reflects consumer preference for energy-efficient buildings, with 50% of new residential constructions integrating BAPV systems.

What Are the Challenges and Opportunities in the Regional Market?

South America accounted for 10% of the global BAPV market in 2024, led by Brazil with 6%. Favorable solar radiation and renewable energy investments support growth. Tax and subsidy changes on imported components may impact expansion. Government policies promoting domestic production could increase costs but enhance long-term sustainability. Opportunities exist in underutilized markets like Argentina and Chile. Local players such as Soltec Power Holdings are deploying photovoltaic systems across commercial projects. Consumer awareness is rising, with 40% of new commercial buildings considering BAPV solutions.

How Are Market Dynamics Evolving in This Region?

Middle East & Africa saw increasing BAPV adoption in 2024, with the UAE (3% share), South Africa, and Saudi Arabia leading. Demand is driven by construction, oil & gas, and renewable energy sectors. Technological modernization, including smart grid integration, improves system efficiency. Local regulations and trade partnerships promote sustainable energy adoption. First Solar is active in providing advanced photovoltaic solutions. Regional consumer behavior shows growing interest in energy-efficient buildings, with 30% of new commercial projects incorporating BAPV systems.

China: 35% market share; driven by large-scale infrastructure projects and strong government policy support.

Germany: 25% market share; supported by stringent sustainability regulations and extensive incentives.

The Building Applied Photovoltaic (BAPV) market exhibits a fragmented competitive structure with over 150 active players globally in 2024, spanning manufacturing, integration, and installation. The combined share of the top five companies is approximately 35%, indicating moderate consolidation. Key market participants are actively pursuing strategic initiatives such as mergers, acquisitions, and international partnerships to strengthen their technological capabilities and geographic reach. Product innovation is a primary differentiator, with companies developing high-efficiency photovoltaic modules, bifacial and thin-film panels, and smart building-integrated solutions. Technological advancements such as energy storage integration, IoT-enabled building systems, and modular BAPV designs are increasingly shaping competition. Regional differentiation is also notable, with North America emphasizing smart energy management, Europe focusing on sustainability compliance, and Asia-Pacific leveraging large-scale infrastructure deployments. Companies are investing in R&D to enhance module efficiency, reduce installation costs, and improve aesthetic integration into building facades. Innovation in durability, lightweight materials, and predictive maintenance solutions is further intensifying competition. Firms implementing these strategies are positioned to capture new projects, particularly in commercial, industrial, and high-density urban developments.

Trina Solar Limited

Canadian Solar Inc.

SunPower Corporation

Hanwha Q CELLS

REC Group

Raylyst Solar

Solaria Corporation

The Building Applied Photovoltaic (BAPV) market is advancing rapidly due to innovative technologies and growing demand for energy-efficient buildings. Building-Integrated Photovoltaics (BIPV) are increasingly used in facades, windows, and rooftops, enabling structures to generate electricity while maintaining design aesthetics. By 2024, over 23.6 GW of BAPV systems were operational globally, reflecting the adoption of integrated energy solutions in urban and commercial constructions. Crystalline silicon technology remains dominant, accounting for over 70% of installed modules in 2024, due to high efficiency and reliability. Meanwhile, thin-film and organic photovoltaic materials are gaining traction, offering lightweight, flexible solutions suitable for complex architectural designs. These materials now represent approximately 18% of total BAPV installations, especially in retrofit and modular applications.

The integration of smart building systems with BAPV allows real-time energy monitoring, performance optimization, and predictive maintenance. In North America, 52% of commercial buildings adopting BAPV utilize smart energy management platforms, improving efficiency and reducing energy waste. Energy storage integration is another emerging trend, with over 5 GW of storage-equipped BAPV projects installed in 2024. Storage enables excess energy to be used during non-sunlight hours, enhancing grid independence and reliability. Combined, these technological innovations are shaping the BAPV market toward smarter, more resilient, and sustainable building solutions.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In 2024, the U.S. solar industry installed nearly 50 gigawatts of capacity, a 21% increase from 2023, reflecting the growing integration of solar technologies in building applications. Source: www.solarenergy.org

In October 2024, the International Energy Agency's Photovoltaic Power Systems Programme (IEA-PVPS) released its annual Trends Report, highlighting global growth in photovoltaic installations and increasing BAPV adoption in urban energy solutions. Source: www.iea-pvps.org

In 2024, the European Union announced new regulations encouraging integration of renewable energy in building designs, offering incentives for BAPV adoption in new constructions and retrofits. Source: www.europa.eu

The Building Applied Photovoltaic (BAPV) Market Report provides a complete analysis of global market trends, technology applications, and regional performance. It examines various BAPV types including rooftop-mounted, facade-integrated, and fully building-integrated systems, highlighting their energy efficiency, aesthetic advantages, and structural integration potential. The report covers key applications across residential, commercial, and industrial buildings, illustrating adoption patterns such as 42% of commercial high-rise buildings in Europe incorporating BAPV for energy savings. Emerging market segments like modular BAPV panels for prefabricated structures are included, offering insights into future adoption trends.

Technological focus areas in the report include crystalline silicon, thin-film, and organic photovoltaic materials, energy storage integration, and smart building management systems. It also assesses regional insights, including Europe, North America, Asia-Pacific, South America, and Middle East & Africa, providing market share data and adoption behavior trends, such as North American enterprises utilizing 52% smart BAPV systems. Additionally, the scope includes industry sectors driving demand, regulatory incentives, ESG-driven adoption, and innovations in energy management. The report serves as a critical resource for decision-makers, investors, and technology developers seeking to understand the breadth of opportunities, niche applications, and strategic priorities shaping the BAPV market globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 539.84 Million |

|

Market Revenue in 2032 |

USD 699.95 Million |

|

CAGR (2025 - 2032) |

3.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

JA Solar Technology Co., Ltd., First Solar, Inc., LONGi Green Energy Technology Co., Ltd., Trina Solar Limited, Canadian Solar Inc., SunPower Corporation, Hanwha Q CELLS, REC Group, Raylyst Solar, Solaria Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |