Reports

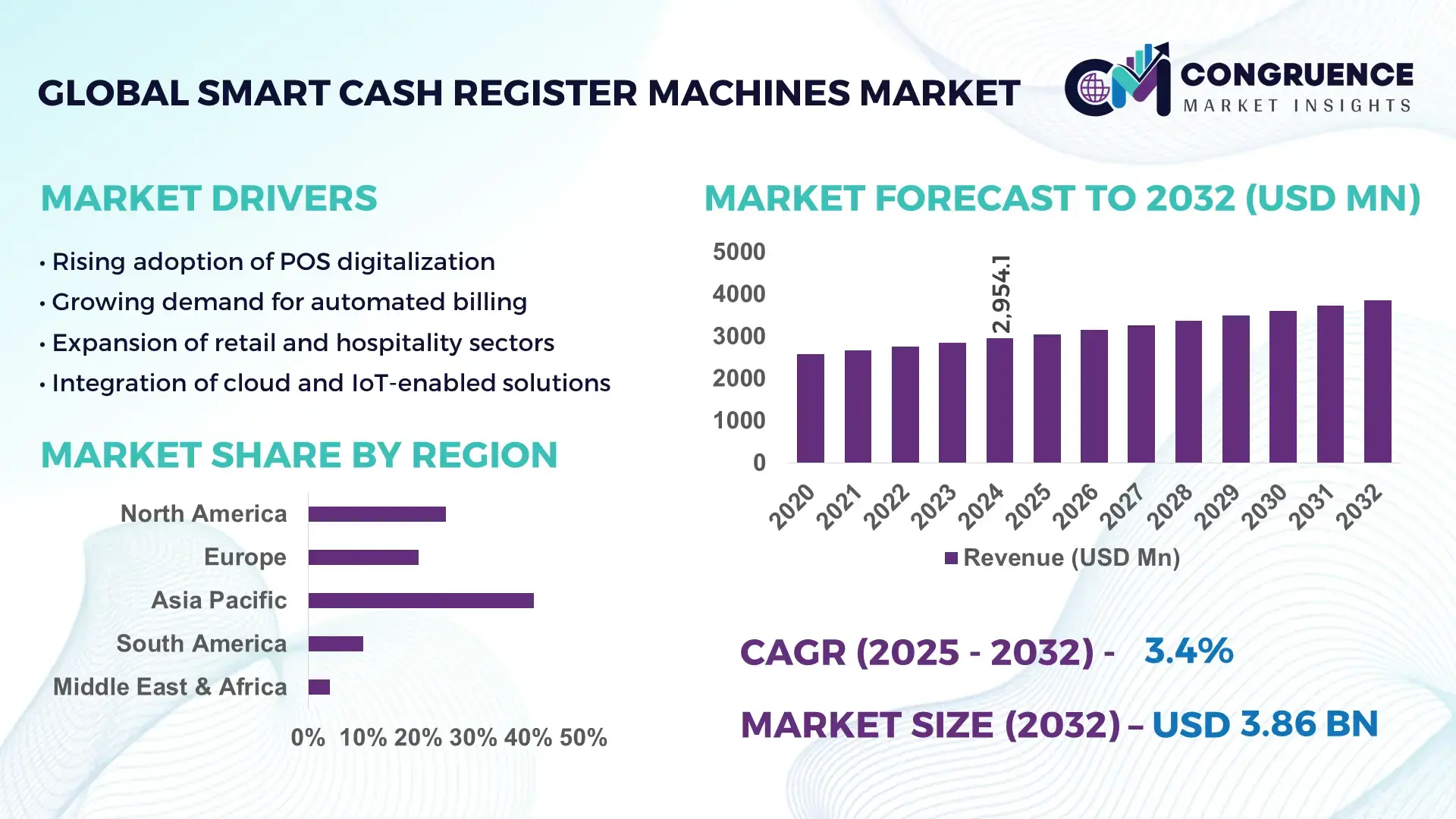

The Global Smart Cash Register Machines Market was valued at USD 2954.07 Million in 2024 and is anticipated to reach a value of USD 3859.99 Million by 2032 expanding at a CAGR of 3.4% between 2025 and 2032. This growth is driven by accelerating digital payment adoption and demand for integrated POS‑inventory solutions.

In leading economies such as the United States, large‑scale retail chains have rapidly transitioned to cloud‑based smart cash registers, with over 7.9 million units deployed nationwide by 2024, signaling robust production capacity and substantial investment in advanced retail infrastructure. Retailers in the U.S. frequently deploy registers with real‑time analytics, Bluetooth/NFC connectivity and integrated customer‑management tools, supporting high‑volume retail and hospitality operations with advanced technology adoption and strong capital investment.

Market Size & Growth: USD 2,954.07 M in 2024; projected at USD 3,859.99 M by 2032; CAGR 3.4% — driven by demand for digital payment systems and cloud‑based transaction management

Top Growth Drivers: ~65% increase in cashless transactions; ~61% rise in checkout efficiency improvements; ~44% growth in mobile‑linked smart register adoption

Short-Term Forecast: By 2028, expect ~25% reduction in transaction processing time and ~18% improvement in inventory‑management accuracy for retailers adopting smart registers

Emerging Technologies: Integration of AI‑driven sales analytics, IoT‑enabled inventory tracking, and NFC/QR contactless payment systems

Regional Leaders: North America (high adoption in urban retail and hospitality by 2032), Asia‑Pacific (rapid expansion among SMEs in retail and e‑commerce markets), Europe (steady growth in supermarkets and specialty stores)

Consumer/End‑User Trends: Wide usage in retail supermarkets, pharmacies, QSRs and small‑medium enterprises; growing preference for contactless payments and real‑time receipts

Pilot or Case Example: In 2024, dual‑screen registers with real‑time analytics implemented in mid‑size supermarket chains resulted in ~22% faster checkout, reducing customer wait times significantly

Competitive Landscape: Market leader holds around 30–35% share; major competitors include global POS vendors operating across regions (top 3–5 firms dominate hardware and software segments)

Regulatory & ESG Impact: Growing emphasis on energy‑efficient, low‑power devices and adoption of data‑security compliance regulations encourages modern smart register deployment

Investment & Funding Patterns: Surge in capital expenditure by retail chains in 2023–2024; increasing funding in POS‑software integration and cloud‑based retail management platforms

Innovation & Future Outlook: Advances in AI‑powered customer analytics, hybrid cloud‑on‑premise POS models, and mobile‑first compact registers poised to shape next‑generation retail checkout systems

Global retail, food service, and hospitality sectors increasingly rely on smart cash register machines to streamline operations, manage inventory, and process payments efficiently. Recent innovations — such as integration with cloud‑based inventory platforms, NFC/QR contactless payments, biometric authentication and real‑time sales analytics — have significantly enhanced operational efficiency and customer experience. Regulatory and economic shifts toward cashless transactions, combined with environmental concerns, drive demand for energy‑efficient, secure, and sustainable cash register solutions. In regions like Asia‑Pacific, small and mid‑sized retailers and e‑commerce‑linked stores are rapidly adopting smart registers, boosting regional growth. Emerging trends include mobile‑POS for pop‑up retail, hybrid register‑POS software bundles, and deeper integration with customer‑loyalty and inventory‑management platforms — positioning the market for continued expansion and technological evolution.

The strategic relevance of the Smart Cash Register Machines Market is rooted in the rapid shift toward cashless, omnichannel retail ecosystems where real‑time data, operational efficiency and customer experience matter. Compared to legacy cash registers, modern smart systems deliver roughly 45% faster checkout speeds and 30% improved inventory accuracy, a marked improvement over traditional point‑of‑sale setups. Regionally, North America dominates in deployment volume, while Asia‑Pacific leads in adoption with over 60% of small and mid‑sized retailers using smart cash registers. By 2027, AI‑powered analytics integration is expected to improve transaction error detection by as much as 25%. Firms are committing to ESG‑driven metrics such as 20% reduction in energy consumption and e‑waste recycling by 2030. In 2025, a major retail chain in Europe implemented cloud‑connected cash registers with biometric and IoT‑enabled security, achieving a 22% reduction in checkout time and 18% reduction in system downtime. The Smart Cash Register Machines Market is increasingly viewed as a strategic pillar for resilience, compliance and sustainable growth across retail and hospitality sectors.

As cashless and contactless payment methods become mainstream, demand for smart cash register machines climbs sharply. Studies show contactless payment adoption globally has grown nearly 3.5 times faster since 2020 compared to traditional payments. Such demand compels retailers and hospitality businesses to adopt registers capable of NFC, QR‑code and mobile‑wallet transactions, replacing legacy tills. As a result, many enterprises report transaction processing 30–45 seconds faster per customer and greatly reduced errors. The pressure to meet consumer expectations for speed, hygiene, and convenience makes cashless readiness a critical driver — smart registers have become indispensable for businesses aiming to stay relevant and efficient in a digital-first retail environment.

Despite clear benefits, high upfront costs for hardware, software licensing, and installation remain a major barrier for many businesses — especially small and medium-sized retailers. Estimates suggest initial investment can absorb up to a quarter or more of total annual IT budgets for small chains. Many legacy point‑of‑sale systems are deeply integrated with older inventory or billing infrastructure, making transition complex and risky. The complexity of integrating new smart registers with existing systems often leads to disruptions, necessitating additional resources for employee training and IT support. These cost and integration burdens discourage widespread adoption, particularly in cost-sensitive or resource-constrained environments, limiting market penetration and growth speed in certain regions.

There is strong growth potential in small and medium-sized enterprises (SMEs), food trucks, pop-up stores, boutique retailers, and other mobile or decentralized retail formats. As more than two‑thirds of SMEs actively invest in modern POS hardware to improve billing efficiency and customer experience, demand for compact, affordable, cloud-based smart cash registers rises. Mobile‑POS (mPOS) solutions and portable smart registers allow businesses to process transactions on-the-go, manage inventory, and track sales remotely — essential for on-demand and flexible retail operations. This shift opens a vast underserved market segment, especially in emerging economies where retail infrastructure is still evolving, offering vendors a chance to capture growth by providing scalable, easy-to-integrate smart register solutions tailored to SMEs and mobile retailers.

As smart cash registers increasingly handle sensitive payment and customer data, security, compliance, and infrastructure compatibility become critical concerns. Many retailers face challenges meeting global security standards such as EMV, data encryption requirements, and data‑protection regulations. Fragmented hardware and software ecosystems — with multiple vendors, protocols, and standards — cause interoperability issues, making it difficult to integrate registers with legacy systems or third‑party inventory/CRM tools. Additionally, frequent software updates and ongoing maintenance costs create operational burden. For smaller retailers, these complexities, combined with cyber‑threat risks and compliance pressures, often outweigh perceived benefits, slowing down adoption even when technical capability exists.

• Growing integration of AI‑driven analytics and inventory forecasting: Smart cash register systems increasingly embed AI-powered modules to analyze historical sales, seasonal patterns, promotions, and local events to forecast demand. Many retailers report a 20–30% reduction in overstock and a similar percent drop in stockouts after implementing predictive POS systems. This shift means inventory management is becoming proactive, enabling retailers to optimize working capital and reduce waste. For multi‑store chains, centralized data from smart cash registers supports consolidated inventory decisions, improving operational visibility and supply‑chain responsiveness.

• Surge in mobile, contactless and cloud‑based POS adoption: By 2025, over 60% of POS transactions globally are contactless, prompting swift upgrades to NFC/QR‑enabled smart cash registers. Cloud‑based registers now account for a majority of new deployments, with more than 70% of large retailers using cloud-connected systems to manage multiple outlets remotely. Mobile POS (mPOS) devices, including handheld terminals and tablets, are also seeing rapid uptake — often reducing checkout times by 25–35%. These developments enable retailers to process payments and update inventory in real time, offering flexibility and scalability especially for small and medium enterprises.

• Rise in modular, compact and energy‑efficient hardware designs: Manufacturers are leaning toward modular and compact hardware for smart cash registers — offering flexibility to customize components such as card readers, barcode scanners, touchscreens, and contactless payment modules. Modular designs allow retailers to upgrade or replace part‑components easily, extending device life and reducing hardware waste. Energy‑efficient registers with low‑power displays and recyclable materials are becoming more common, aligning with corporate sustainability goals and reducing operating expenses for retailers sensitive to energy costs and footprint.

• Expansion of omnichannel and sector‑specific POS solutions: Retailers, hospitality operators, and specialty stores increasingly demand POS systems that integrate with e‑commerce, loyalty management, CRM, and inventory platforms for unified commerce experiences. Smart cash register machines tailored to sectors such as restaurants, pharmacies, and boutique retail now support features like kitchen display integration, customer loyalty tracking, and sector‑specific billing workflows. Adoption of these customized solutions has increased by approximately 45% among new installs in 2024–2025, enabling businesses to deliver seamless omnichannel service and improved customer engagement while streamlining backend operations.

The market segmentation for Smart Cash Register Machines consists primarily of divisions by type of system, application area, and end-user category. By type, deployments range from traditional countertop terminals to mobile POS (mPOS), cloud-based POS software bundles, and kiosk/self-checkout terminals. In application, the systems are tailored for supermarkets, restaurants, pharmacies, boutique retail, pop-up stores, and hospitality services. End-user segments include large retail chains, small and medium enterprises (SMEs), hospitality operators, and specialty retail outlets. This segmentation allows vendors and decision-makers to identify niche requirements, choose appropriate hardware or software configurations, and tailor deployment strategies to the operational scale and retail format. Adoption patterns vary, with larger chains favoring full-featured, integrated registers, while SMEs and pop-up retailers often opt for lightweight, cost-effective mobile or cloud-based variants. Variation in consumption patterns, device preferences, and integration needs across segments underpins the dynamic landscape of the Smart Cash Register Machines market.

Countertop and fixed smart cash register terminals currently account for approximately 45% of all deployments globally, reflecting their continued use in established retail and hospitality environments where reliability and robustness are critical. Their dominance stems from the need for durable hardware capable of high-volume transactions, integrated inventory controls, and multiple peripheral support (barcode scanners, receipt printers, cash drawers). Mobile POS (mPOS) systems are the fastest-growing segment, experiencing around 8% annual growth in deployments during 2024–2025, driven by rising demand from SMEs, pop-up stores, outdoor markets, food trucks, and mobile retail setups. mPOS growth is fueled by minimal upfront cost, portability, ease of deployment, and support for contactless payments and cloud-based transaction logging — ideal for retailers needing flexibility and low entry-cost solutions. Cloud-based POS software bundles represent roughly 30% of the market, offering software-as-a-service convenience, remote management, automatic updates, and reduced IT overhead. These are preferred by multi-store chains and franchise operations seeking centralized control, real-time inventory updates, and unified transaction tracking across outlets.

Kiosk and self-checkout terminals contribute the remaining 25%, prominent in supermarkets, pharmacies, and convenience stores where automation and speed of service matter. Their niche relevance lies in self-service convenience, reducing staff requirements, and enabling efficient high-throughput checkout.

Supermarkets and general retail remain the leading application area, accounting for around 50% of Smart Cash Register Machines deployments, due to their high transaction volumes, frequent inventory turnover, and strong need for integrated checkout-inventory workflows. These establishments benefit from stable, fixed terminal setups offering durability and peripheral compatibility. The segment experiencing the fastest growth is pop-up stores, food-trucks, and mobile retail applications, with adoption rising at nearly 9% annually over 2024–2025. Growth is supported by the surge in flexible retail formats, seasonal markets, and event-based commerce where portable or cloud-based smart registers provide agility, low-cost entry, and scalable payment capabilities. Hospitality and restaurant applications account for approximately 25% of deployments, favored for table-side billing, split checks, and integrated kitchen/order management — essential for efficient service and customer experience. Pharmacies and specialty retail contribute about 10%, where compliance, accurate billing, and inventory tracking are critical. The remaining 15% combine boutique retail, convenience stores, and multi-format outlets, where varied business models influence mixed use of countertop, mobile, and kiosk POS systems.

Large retail chains represent the leading end-user segment, making up roughly 48% of total smart cash register deployments, thanks to their scale, need for unified inventory and sales management, and multi-outlet operations requiring centralized control and standardization. Their preference for enterprise-grade, cloud-integrated POS systems ensures consistency across branches and supports high-volume transactions. Small and medium enterprises (SMEs) are the fastest-growing end-user segment, with adoption rising at approximately 7% annually over 2024–2025. This growth is fueled by cost-sensitive operators seeking affordable, easy-to-deploy mobile or cloud-based registers that reduce hardware investment and support flexible payment methods. SMEs in emerging markets, in particular, are embracing smart registers to modernize operations and support digital payment adoption. Hospitality operators — including restaurants, cafes, and quick-service outlets — account for about 20% of end-users, valuing POS systems that handle table-side billing, split payments, loyalty programs, and real-time order management. Boutique and specialty retail outlets contribute around 15%, leveraging compact or hybrid smart registers to manage inventory and transactions with limited space or specialized workflows. A smaller share — roughly 17% combined — represents convenience stores, kiosks, pharmacies, and other niche businesses, often using portable or kiosk-style registers tailored to specific use-cases.

Asia-Pacific accounted for the largest market share at 41.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.97% between 2025 and 2032.

The strong share reflects high adoption across China, India, Japan, South Korea and other emerging markets. North America follows with about 28.7% market share in 2024, Europe holds around 21.5%, while Middle East & Africa and South America share the remainder. Asia‑Pacific’s dominance stems from rapid retail expansion, increasing use of mobile payments, and rising SME adoption, supported by over 78% of new installations featuring local-language support and e-invoicing. Growth projections indicate rising demand in urbanizing markets, increased POS modernization in small retailers, and expanding cloud‑based retail infrastructure across the region.

Why technology‑savvy retail infrastructures drive adoption?

North America accounts for roughly 28.7% of global smart cash register deployments, underpinned by mature retail and hospitality sectors. Major demand comes from supermarkets, large retail chains, QSRs (quick‑service restaurants), and convenience stores, where fast checkout and contactless payment compatibility are critical. Regulatory environments in several states mandate secure transaction processing and data protection standards, encouraging retailers to upgrade legacy registers. Technological advances such as NFC‑enabled contactless payment, cloud‑based POS management, and dual-screen terminals have become standard: for example, over 90% of new units shipped in 2024 supported contactless transactions. A local POS vendor launched a cloud-integrated register adopted by more than 25% of large retailers, reflecting strong enterprise‑level uptake. Consumer behaviour in North America shows preference for speed, security, and convenience: many retailers report that tablet‑based POS systems now handle over half of in-store transactions. Healthcare retail & fuel‑station convenience stores also see increasing smart register penetration, indicating cross‑industry demand beyond traditional retail.

How regulatory compliance and multilingual demand shape deployment?

Europe held about 21.5% of the global smart cash register market in 2024, with leading demand from Germany, the UK and France. Adoption is driven by regulatory pressure, data‑security compliance mandates and energy‑efficiency requirements in retail and hospitality sectors. Many European retailers have upgraded to POS systems with GDPR‑compliant data storage and multilingual billing interfaces — in France alone, over 1.2 million registers now support multiple languages. Emerging technologies like cloud‑based POS, contactless payments, and energy‑efficient hardware are increasingly adopted to meet regulatory and sustainability goals. A notable example: a major German retailer deployed multilingual cloud-connected registers across its outlets in 2023, streamlining operations across countries and reducing training time by up to 60% for foreign‑language staff. European consumers tend to demand transparent billing, multi-currency or multilingual support and data privacy compliance — this drives demand for smart cash register machines built with these features.

Why rapid retail evolution and mobile‑first payments accelerate growth?

Asia‑Pacific leads global deployment volume, with estimated 41.2% share in 2024. Top consuming countries include China, India and Japan — in India alone, unit shipments grew by 61.4% year-on-year, driven by government digitalization initiatives and growth in e‑commerce‑linked retail stores. Infrastructure investments and retail chain expansion across urban and semi‑urban areas fuel demand for modern cash register systems. More than 78% of new installations now include local‑language billing and e‑invoicing features to cater to diverse consumer bases. Technology trends in Asia‑Pacific emphasize cloud‑based POS, QR‑code/mobile‑wallet payments, and affordable mPOS solutions for small and medium-sized enterprises. Local manufacturers and vendors are increasingly offering low-cost, mobile-friendly smart registers tailored for SMEs and small retailers. Consumer behavior here is characterized by rapid adoption of mobile payments, preference for digital receipts, and widespread smartphone penetration — driving adoption of smart cash register machines suited for mobile and flexible retail formats.

How retail modernization and fiscal regulation spur demand?

In South America, key countries such as Brazil and Argentina are gradually modernizing retail infrastructure, creating demand for smart cash register machines. Though market share remains modest compared to other regions, growth is supported by increasing urban retail development and regulatory encouragement for digital payments and fiscal transparency. Retailers are upgrading cash registers to support bilingual interfaces, multi-currency transactions, and integration with local tax compliance systems. One example is a large retail chain in Brazil that replaced legacy cash registers with smart POS systems featuring barcode scanning and integrated billing — improving checkout speed and accuracy. Consumer behaviour in South America shows growing acceptance of electronic payments and digital receipts, particularly in urban centers and among younger demographics, prompting retailers to deploy modern smart registers to meet evolving expectations.

Why growing retail modernization and tourism sectors drive adoption?

In Middle East & Africa, countries such as UAE, Saudi Arabia and South Africa are emerging as growth hubs for smart cash register machines. Demand is bolstered by expansion in retail, hospitality, and tourism sectors, often fueled by government-led retail modernization initiatives and cross-border trade policies. Many new installations incorporate hybrid registers supporting solar-powered or low-energy operation — useful in regions with inconsistent grid access. Retailers increasingly favor smart registers with contactless payment support, multilingual billing (Arabic/English), and mobile wallet integration to cater to diverse consumer bases and expatriate populations. A regional retailer chain in UAE reportedly installed tens of thousands of smart registers in 2024 to support rapid retail expansion and high tourism traffic. Consumer behavior in the region tends toward digital payments and convenience, with a rising preference for contactless transactions, driving demand for modern smart cash register solutions.

China — ~35% share of the global Smart Cash Register Machines market, owing to high volume production, rapid retail expansion, and aggressive SME adoption.

United States — ~23–25% global share driven by strong enterprise demand across retail, hospitality and convenience sectors, and high penetration of digital payment infrastructure.

The competitive environment in the Smart Cash Register Machines market is moderately consolidated yet highly dynamic, with dozens of active manufacturers and vendors globally, while the top players command a significant combined share. Roughly more than 35–40 companies currently compete at a global scale, offering varying degrees of hardware, software, and integrated services. The top 5 companies collectively hold approximately 47%–65% of global market share depending on region and product type. Market positioning is broadly split among legacy hardware leaders, disruptive mobile/driven-by-SME players, and hybrid cloud-POS innovators. Some firms focus on robust, enterprise-grade terminals for retail and hospitality chains; others prioritize affordable, mobile-friendly POS solutions for SMEs and emerging markets. Recent strategic initiatives include partnerships, product launches, and mergers to expand offerings and geographic reach. Certain vendors have formed alliances to co-develop Android-based POS terminals combining hardware from one company and software/payment processing from another — enabling unified solutions.

Innovation trends influencing competition include development of contactless payment support, Android-based smart registers, cloud-based POS management, integrated analytics and inventory modules, and self-service or kiosk-style checkout options. These features are increasingly becoming differentiators. As the market shifts from simple cash registers to fully integrated smart POS ecosystems, companies that invest in modular hardware, software flexibility, and value-added services (analytics, CRM, omnichannel integration) are gaining competitive advantage. Given this environment, the market remains neither a pure monopoly nor completely fragmented: dominant players maintain influence through scale and global footprint, while niche and regional players continue to grow by targeting underserved segments (SMEs, emerging markets, mobile retail). This competitive landscape underscores the importance of strategic innovation, partnerships, and responsive product development for companies looking to lead in Smart Cash Register Machines.

Ingenico Group

Verifone

PAX Technology

NCR Corporation

Square, Inc.

Clover Network, Inc.

Diebold Nixdorf

Fujitsu

Sunmi

Revel Systems

The Smart Cash Register Machines market is undergoing significant technological transformation driven by the integration of AI, cloud computing, IoT, and mobile payment technologies. Modern smart registers now support AI-powered analytics that track sales trends, forecast inventory needs, and detect anomalies in real time. Retailers using AI-enabled registers have reported a 20–30% improvement in inventory accuracy and a 25% reduction in stockouts, demonstrating the tangible operational impact of intelligent systems. Cloud-based technology is a major enabler, allowing centralized management of multi-location stores. Approximately 72% of large retailers in North America and Europe now employ cloud-connected smart cash registers, enabling real-time updates of inventory, pricing, and sales reports across all outlets. This facilitates seamless integration with loyalty programs, CRM platforms, and e-commerce operations, creating a unified omnichannel retail experience.

IoT adoption in smart registers is enhancing connectivity with peripheral devices such as barcode scanners, digital scales, payment terminals, and self-service kiosks. IoT-enabled registers improve operational efficiency by automating data transfer and reducing manual errors. Recent deployments indicate that IoT integration can cut transaction errors by up to 18% in busy retail environments. Contactless and mobile payment solutions, including NFC, QR code, and mobile wallets, are increasingly standard features, with over 60% of new smart cash register units supporting these payment options. Emerging trends also include biometric authentication, voice-command functionalities, and advanced touchscreen interfaces designed to streamline customer interactions. Overall, technology adoption is reshaping the market, enhancing operational efficiency, consumer experience, and data-driven decision-making across retail, hospitality, and specialty segments.

In September 2024, PAX Technology introduced the A6650 — the world’s first IP67‑rated Android SmartPOS PDA with integrated payment acceptance functionality, combining rugged mobile computing and secure payments for retail, hospitality and delivery industries.

In October 2023, Ingenico — via partnership with Payroc — launched the AXIUM DX8000 terminal line to deliver a versatile Android‑based smart POS solution for retail and hospitality, enhancing payment acceptance capabilities and checkout efficiency across diverse outlets.

In June 2024, NCR Corporation rolled out self‑checkout POS terminals equipped with integrated computer vision for supermarkets, enabling automated scanning and payment processing to reduce manual labour and accelerate checkout in high-traffic environments.

In 2024, Android‑based smart terminal sales within PAX’s global business rose to exceed 50% of total device sales, illustrating the accelerating shift of smart cash register demand toward Android SmartPOS systems across multiple markets worldwide. (PAX Technology)

The Smart Cash Register Machines Market Report encompasses a comprehensive examination of hardware and software POS systems—including countertop terminals, mobile POS (mPOS), cloud‑based POS platforms, and self‑checkout/kiosk‑style registers. It covers all major types of technology deployments, from traditional fixed POS to Android‑based mobility solutions, and details application across retail, supermarkets, hospitality, quick‑service restaurants, pharmacies, specialty stores, pop‑up retail, and mobile commerce formats. The scope extends to end‑users ranging from large retail chains and franchises to small and medium enterprises (SMEs), independent retailers, food‑service operators, and pop‑up or event‑based vendors.

Geographically, the report analyzes adoption and market developments across key regions including Asia‑Pacific, North America, Europe, South America, Middle East & Africa — highlighting variation in demand drivers, regulatory environments, infrastructure readiness, and regional consumption patterns. It examines technology trends such as Android SmartPOS terminals, cloud‑enabled POS ecosystems, contactless payments (NFC, QR), self‑service checkout, and mobile‑first POS solutions tailored for SMEs or high‑mobility retail formats.

The report includes segmentation by product type, application, end-user category, and technology stack, offering decision-makers clear insight into which segments exhibit strong growth potential or require strategic investment. Industry focus areas covered include retail chains, hospitality & food-service, e‑commerce‑linked stores, and emerging formats like pop‑up shops, food trucks, and on‑the-go vendors. It also considers evolving requirements such as multi‑payment acceptance, inventory and analytics integration, security compliance, multilingual interfaces, and energy‑efficient or ruggedized hardware for emerging markets. The breadth of coverage ensures stakeholders understand both mainstream market dynamics and niche or emerging opportunities within the global Smart Cash Register Machines landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2954.07 Million |

|

Market Revenue in 2032 |

USD 3859.99 Million |

|

CAGR (2025 - 2032) |

3.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ingenico Group, Verifone, PAX Technology, NCR Corporation, Square, Inc., Clover Network, Inc., Diebold Nixdorf, Fujitsu, Sunmi, Revel Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |