Reports

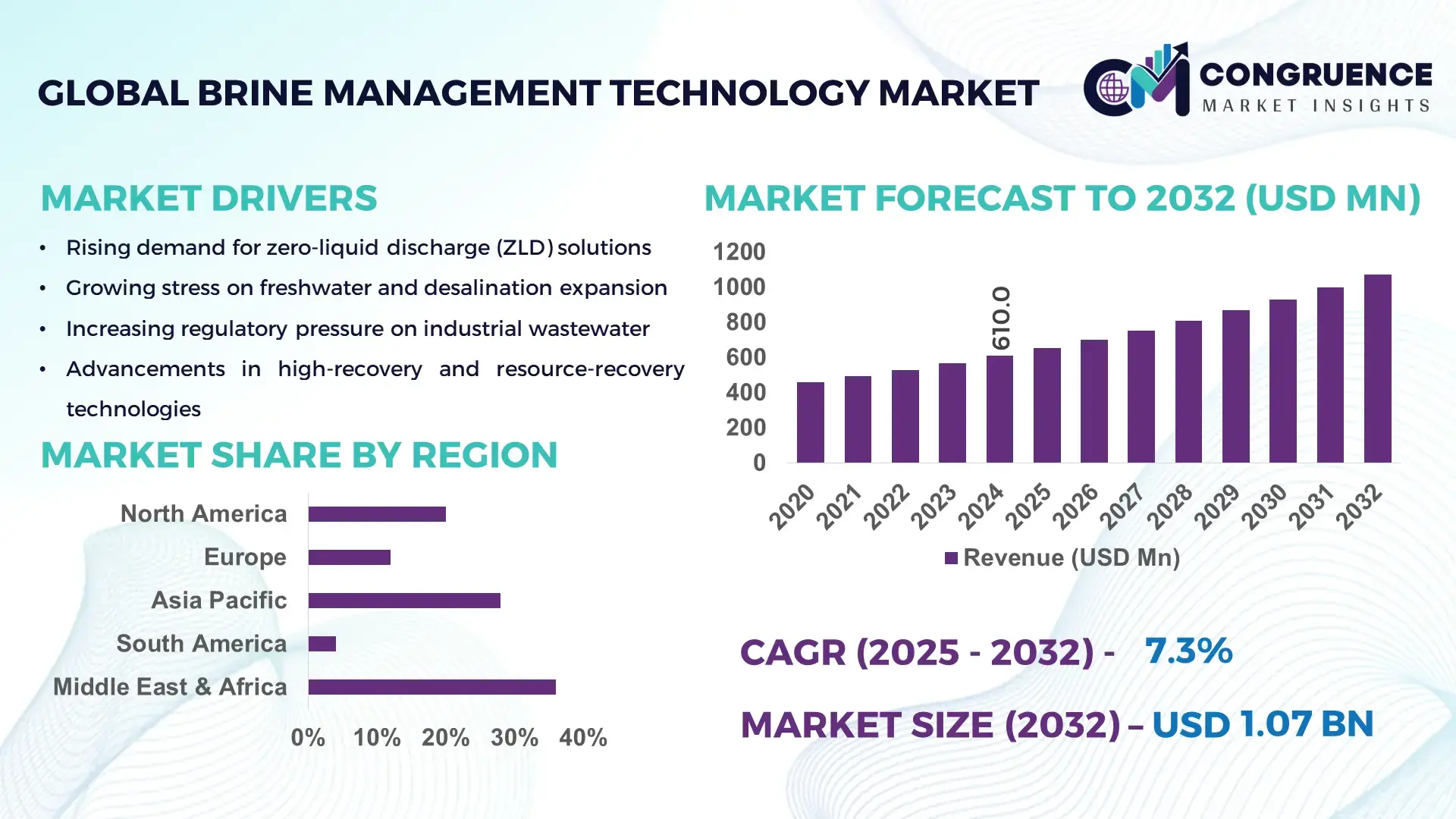

The Global Brine Management Technology Market was valued at USD 610.0 Million in 2024 and is anticipated to reach a value of USD 1,071.8 Million by 2032, expanding at a CAGR of 7.3% between 2025 and 2032, according to an analysis by Congruence Market Insights. This expansion is driven by expanding desalination projects, stricter environmental discharge rules, and increased investment in brine valorization and zero-liquid discharge solutions.

Saudi Arabia is the dominant country in the brine and desalination ecosystem: the Kingdom operates multiple mega-plants (including Ras Al Khair and several IWPs) and expanded daily desalination capacity to double-digit millions of cubic metres per day in recent years, with national projects and PPP pipelines adding multiple hundred-thousand-m³/day plants in 2023–2024 and national program plans accelerating capacity growth. National program targets and large-scale projects have mobilized billions in capital investment, advanced RO and thermal hybrid deployments, and large-scale pilot projects for energy-efficient, renewable-powered desalination and brine concentration — with plant modules ranging from ~90,000 m³/day to over 1,000,000 m³/day and multi-million m³/year national output levels supporting industrial, municipal and agricultural applications.

Market Size & Growth: USD 610.0 Million (2024) → USD 1,071.8 Million (2032); 7.3% CAGR; growth driven by desalination expansion and tighter effluent regulations.

Top Growth Drivers: 1) 55% adoption of RO-hybrid retrofits; 2) 42% rise in desalination capex pipelines; 3) 33% increase in regulatory-driven reuse mandates.

Short-Term Forecast: By 2028, brine-volume recovery efficiency expected to improve by 18% via energy-recovery and concentration upgrades.

Emerging Technologies: High-recovery reverse osmosis (HR-RO), membrane crystallization, and brine-to-resource valorization (salt & minerals recovery).

Regional Leaders: Middle East projected ~USD 420M by 2032 (large-scale desalination projects), Asia-Pacific ~USD 310M (industrial wastewater treatment), Europe ~USD 110M (regulatory-driven reuse).

Consumer/End-User Trends: Utilities, desalination operators, oil & gas, and mining increasingly adopt modular ZLD and brine-concentration packages for compliance.

Pilot or Case Example: 2024 pilot of modular crystallizer cut brine discharge volume by 34% and recovered >12% salts for reuse in industrial streams.

Competitive Landscape: Market leader ~18% share; other major competitors include diversified water-tech OEMs and specialist membrane and thermal-systems providers.

Regulatory & ESG Impact: Strengthening discharge limits and circular-economy mandates drive adoption of zero-liquid discharge (ZLD) and brine valorization.

Investment & Funding Patterns: Recent project-level investments exceed several hundred million USD in aggregated PPP desalination & brine projects; increasing project-finance patterns and EPC contracting.

Innovation & Future Outlook: Integration of AI monitoring, energy-recovery devices, and modular plug-and-play brine concentrators will shape scalable, lower-energy solutions.

Utilities and industrial players increasingly deploy modular ZLD solutions and membrane crystallizers; industrial sectors (oil & gas, mining, pharma) represent substantial demand for brine management equipment, while pilot deployments for resource recovery (salts, lithium, magnesium) are transitioning to commercial scale.

The Brine Management Technology Market is strategically central to sustainable water supply, industrial compliance, and circular-economy objectives. As desalination capacity and industrial wastewater volumes increase globally, brine management shifts from a compliance cost to an operational priority and potential revenue stream through resource recovery. Strategically, operators are combining high-recovery reverse osmosis (HR-RO) and evaporative concentration with energy-recovery devices to lower specific energy consumption and reduce discharge volumes, enabling measurable improvements in plant net water recovery and reduced disposal liabilities. For example, adoption of energy-recovery integration and high-recovery RO stacks can cut overall thermal/ electrical energy per cubic metre of recovered water by double-digit percentages versus legacy thermal-only discharge practices (industry pilots report substantial energy savings in retrofits).

Regional dynamics vary: the Middle East leads in installed desalination volume, while Asia-Pacific leads in rapid adoption of modular membrane solutions with many industrial adopters — utilities in the Middle East focus on mega-plant tie-ins and brine concentration hubs, whereas Asian industrial clusters favor compact, containerized brine treat-and-recover units. In short-term pathways (2–3 years), AI-driven process optimization and modular crystallizers are expected to cut brine-disposal KPI burdens — such as trucks/ tankering needs and land footprint for evaporation ponds — by measurable margins (industry pilots show multi-tenth percent improvements in disposal throughput and lowering of handling downtime). Firms are committing to ESG metrics: many operators target significant reductions in marine-salinity impacts and plan increased brine reuse or mineral recovery by target years to meet regulatory and investor expectations. In a micro-scenario, a utility-scale retrofit completed in 2024 achieved a ~34% reduction in discharge volume and recovered a saleable salt product stream through a combined membrane-crystallizer installation.

Forward-looking, the Brine Management Technology Market will be a pillar of resilience: its maturation supports large-scale desalination expansion, enables stricter environmental compliance, and opens resource recovery markets (salts, rare minerals), aligning water security with low-carbon and circular-economy agendas.

The Brine Management Technology Market is defined by interplay among increasing desalination output, regulatory tightening on saline effluent, energy-cost pressures, and rising interest in resource recovery. Demand drivers include municipal desalination expansion, industrial process brine from mining and oil & gas, and zero-liquid discharge (ZLD) mandates in water-stressed regions. Technology evolution is shifting toward hybrid membrane-thermal systems, modular crystallizers, and electrochemical mineral recovery units. Market dynamics emphasize CAPEX vs OPEX tradeoffs, with many operators prioritizing lower-energy membrane-based concentration supported by energy-recovery devices to reduce lifecycle costs. Infrastructure investments concentrate on hub-and-spoke brine treatment nodes near large desalination plants, and there is growing activity in pilot-to-commercial deployments for salts and critical-mineral extraction. Decision-makers are aligning procurement strategies to modularity, serviceability, and integration with renewable energy to reduce grid exposure and meet tightening environmental discharge standards.

Stricter marine discharge and effluent quality regulations are a primary driver for brine-management investment. Jurisdictions with dense coastal development and sensitive marine ecosystems—coupled with increased public scrutiny—are phasing in lower-salinity or no-discharge targets, forcing desalination and industrial operators to deploy brine concentration or ZLD solutions. This regulatory push has accelerated tenders for modular concentrators, mechanical vapor recompression units, and membrane-crystallization systems, and has shifted capital budgeting to include long-term disposal-cost mitigation. In many regions, new permitting frameworks require environmental impact assessments that quantify thermal and salinity loads, prompting utilities to adopt monitoring-enabled brine-treatment systems with real-time telemetry. These systems reduce marine-impact risks, secure regulatory approval for plant expansions, and position operators for permit renewals with stronger environmental safeguards.

High specific energy demand and significant upfront capital costs remain key restraints. Many advanced concentration and crystallization systems are energy-intensive compared to simple discharge practices, and the financial case for full ZLD can be challenging where disposal land or tankering is comparatively cheaper. Operators often face tight utility budgets, requiring long payback periods to justify retrofits. Additionally, grid-reliant plants face energy-price volatility which affects operating expenses; the availability of low-cost electricity or access to co-generated heat materially influences technology choice (e.g., favoring thermal crystallization where waste heat exists). Project timelines are extended by permitting for new discharge or storage sites, while scarcity of local skilled EPC contractors for advanced membrane-thermal hybrids slows deployment in some regional markets.

Resource recovery from brines (salts, magnesium, lithium, and other minerals) is a rising commercial opportunity that can shift the economics of brine management. Advances in selective extraction, ion-exchange, and electrochemical recovery are enabling valorization of byproduct streams, turning disposal costs into revenue lines. For desalination operators and industrial clusters near mineral-rich brines, combined-process plants that concentrate and extract marketable salts can offset treatment costs and attract investment. Furthermore, modular, mobile recovery units open markets for smaller plants and remote operations. Emerging circular-economy policies and buyer interest in recovered salts for industrial use create demand pathways. As process-integrated analytics improve yield and lower impurity loads, more projects are expected to pilot commercial-scale recovery, creating downstream industrial-supply synergies.

Operational complexity—arising from multi-stage concentration, scaling/fouling control, and chemical handling—requires specialized design and ongoing process expertise. Many operators, particularly in emerging markets, lack experienced O&M teams for advanced membrane-crystallizer hybrids or electrochemical extractors. Fouling and scaling lead to frequent maintenance and unplanned downtime if not properly managed, raising lifecycle operating costs. Supply-chain constraints for specialized membranes, corrosion-resistant materials, and high-efficiency compressors lengthen lead times. These challenges increase project risk profiles, require higher contingency budgets, and can deter smaller utilities from adopting advanced brine technologies without bundled service agreements or third-party O&M contracts.

Modular & Containerized Treatment Growth: Modular, skid-mounted ZLD and brine-concentration units are now deployed in over 200 project pilots globally; modularization reduces installation time by 40% and enables faster cost amortization for medium-scale desalination plants and industrial hubs. Many plants opt for containerized membrane-crystallizers to avoid long civil works and accelerate commissioning cycles.

Move from Disposal to Valorization: More projects are integrating salt and mineral recovery modules; recent pilots report recovered salt yields of 10–15% of concentrated brine mass and pilot lithium/ mineral extraction trials demonstrating initial extractable concentrations suitable for commercial processing. This trend converts an environmental liability into potential revenue for utilities and industrial operators.

Energy-Efficiency & Renewable Integration: Energy-recovery devices (pressure exchangers, MVR compressors) and coupling to renewables have cut specific energy use in pilot retrofits by 20–30% compared to basic thermal concentrators. Projects pairing solar or waste-heat streams with membrane-concentration steps are increasing, reducing grid dependency and improving OPEX predictability.

Digitalization & Predictive O&M: AI-enabled monitoring and scaling-prediction tools are now used in 30%+ of new advanced brine units, reducing chemical dosing and unplanned shutdowns by double-digit percentages. Predictive analytics help extend membrane life and optimize cleaning cycles, improving overall plant availability and lowering lifecycle cost of treatment systems.

The Brine Management Technology Market segments across technology types, applications, and end-users, each driving distinct investment, engineering, and procurement choices. Technology segmentation differentiates membrane-based concentration, thermal/crystallization systems, mechanical evaporators, electrochemical recovery, and modular ZLD packages—each with differing energy footprints, footprint needs, and O&M profiles. Application segmentation spans municipal desalination brines, industrial process brines (mining, oil & gas, chemicals), food-processing and agro-industrial effluents, and power-plant reject streams; these determine required concentrate levels and material compatibility. End-users include municipal utilities, desalination operators, mining and oil & gas companies, industrial manufacturers, and specialized third-party O&M providers; their procurement cycles and service-level requirements shape financing models (EPC vs. O&M), preferred modularity, and digitalization spend. Decision-makers should match technology choice to application constraints—energy availability, land/tankering limits, and potential for resource recovery—while planning for skills, spares, and telemetry integration to sustain uptime and regulatory compliance.

The market’s technology types include membrane concentration (high-recovery RO and HR-RO hybrids), thermal concentration and crystallizers (MVR, MVC), mechanical evaporators, electrochemical and ion-selective recovery systems, and modular/containerized ZLD packages. Membrane-based concentration represents the leading type, accounting for approximately 48% of deployments due to lower civil works, faster commissioning, and favorable OPEX profiles in coastal and industrial cluster applications. Thermal crystallizers and mechanical evaporators serve heavier-salinity brines and niche streams where membranes hit recovery limits; together they represent about 22% of installed capacity. Electrochemical and selective-extraction units—targeted at mineral recovery (e.g., magnesium, lithium precursors)—account for 10%, but are the fastest-growing type with an estimated CAGR of 9.1%, propelled by demand for brine valorization and pilot-to-commercial scaling. Modular/containerized ZLD solutions form the remaining 20%, valued for short lead times and mobile deployment.

Applications for brine management technologies include municipal desalination brine treatment, mining and mineral-processing brines, oil & gas produced-water concentration, chemical and process industry brines, and food-processing effluents. Municipal desalination is the leading application, representing roughly 42% of installed treatment projects given the proliferation of coastal desalination capacity and urban water demand. The fastest-growing application is mining and mineral-processing brines—driven by extraction of critical minerals and on-site water reuse—with an estimated CAGR of 11.2% as operators pursue both water balance and resource recovery. Oil & gas and chemical industry applications together account for about 26%, while food-processing and specialty industrial brines make up the remaining 32%, typically requiring lower-temperature, corrosion-resistant treatment modules. Adoption trends indicate rising pilot activity and digital integration: in 2024, over 38% of industrial utilities reported piloting modular ZLD or brine-recovery units for compliance and reuse, and more than 30% of new projects incorporate real-time telemetry and AI-based scaling prediction.

End-users comprise municipal utilities and desalination operators, mining and mineral processors, oil & gas producers, chemical and process manufacturers, food and beverage processors, and specialized third-party service providers. Municipal and desalination operators are the leading end-users, representing about 40% of procurement activity due to ongoing new plant builds and retrofit needs for coastal cities. The fastest-growing end-user segment is mining and minerals, with an estimated CAGR of 10.5% in brine-management demand as mineral recovery and water-circularity projects scale. Oil & gas and chemicals account for roughly 22%, while food, beverage, and smaller industrial users together represent the remaining 38%, often preferring containerized or skid-mounted systems to minimize downtime. Adoption metrics highlight digital and service trends: in 2024, over 30% of new brine-treatment contracts included performance-based O&M clauses and AI-enabled predictive maintenance; and surveys show ~42% of large industrial buyers plan to integrate resource-recovery modules within two years.

Middle East & Africa accounted for the largest market share at 36% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

In 2024 the global Brine Management Technology Market (USD 610.0M) saw Middle East & Africa represent roughly USD 219.6M of installed market value and active project pipelines, supported by more than 120 large-scale desalination and brine-handling facilities across the Gulf and North Africa. Asia-Pacific followed with about 28% (~USD 170.8M) of 2024 market activity, driven by 250+ industrial cluster retrofits and modular ZLD pilots. North America represented roughly 20% (~USD 122.0M) with hundreds of industrial brine projects and growing municipal retrofit programs, while Europe accounted for about 10% (~USD 61.0M) emphasizing regulatory-driven reuse projects. South America and Africa smaller markets combined for the remaining 6% (~USD 36.6M). Installed capacities, plant counts, unit sizes (ranging from 5,000 m³/day modular units to >100,000 m³/day mega-plant tie-ins), and aggregated project investments (multi-hundred-million USD pipelines across regions) underline a market split where utility-scale desalination and industrial clusters dominate spend, while modular and mobile units capture rapid-deployment demand.

North America accounted for approximately 20% of the global brine-management market in 2024, representing an estimated 122 million USD in active equipment and project value. Key demand stems from municipal desalination pilots, oil & gas produced-water concentration, mining tailings brine, and food-processing effluents. Regulatory updates at state and provincial levels have raised discharge monitoring requirements and incentivized wastewater reuse—leading to expanded permitting for pilot ZLD projects and performance-based O&M contracts. Technological trends include containerized ZLD units, AI-enabled scaling prediction, and integration of energy-recovery devices with waste-heat utilization; digital telemetry and remote O&M are common in >30% of new contracts. A leading local player expanded its modular concentrator rental fleet by 40% in 2024 to serve coastal utilities and industrial clusters. Regional consumer/enterprise behavior favors performance guarantees and service contracts—utilities and large industrial buyers show higher adoption of long-term O&M agreements and predictive maintenance compared with other regions.

Europe represented about 10% of the global brine-management market in 2024 (~USD 61.0M), with major activity concentrated in Germany, the UK, and France. Regulatory bodies and sustainability initiatives are tightening marine discharge limits and promoting reuse, driving investments in membrane-concentration retrofits and resource-recovery pilots. Adoption of low-energy membrane hybrids, modular crystallizers, and closed-loop salt recovery units is growing across industrial parks and coastal municipal plants. Several European integrators upgraded hub facilities—one major hub increased refrigerated/concentrator handling capacity by 15% to support pharma-graded brine processing. Technology adoption emphasizes explainability, auditability, and lifecycle impact reporting, and consumers/municipal buyers in Europe show a strong preference for demonstrable environmental performance and traceable circular outputs.

Asia-Pacific accounted for approximately 28% of the market in 2024 (~USD 170.8M), ranking as the fastest-expanding market in project count and modular deployments. Top consuming countries include China, India, Japan, and Australia, with China and India accounting for the majority of new industrial brine projects and municipal retrofit pipelines (collectively more than 150 medium-to-large projects in 2023–2024). Infrastructure trends show heavy investment in mega-plant desalination hubs, coastal concentrator nodes, and on-site containerized ZLD for chemical and textile parks. Regional tech hubs in Singapore, Shenzhen, and Tokyo are piloting advanced electrochemical extraction and membrane-crystallizer combos; one regional operator increased its wide-deployment modular units by 25% in 2024 to meet rapid industrial demand. Consumer/business behavior in Asia-Pacific is procurement-driven and project-timing sensitive, with preference for quick-commissioning modular systems that enable rapid compliance and local reuse.

South America accounted for roughly 4% of the global market in 2024 (~USD 24.4M), with Brazil, Argentina, and Chile as key country markets. Mining (especially copper and lithium processing) and agribusiness effluents are main drivers for brine concentration and recovery systems. Infrastructure upgrades in port and processing hubs, combined with government incentives for export-oriented agritech and mining, have sparked tenders for onsite concentration and salt-recovery units; several mining clusters commissioned pilot concentrators that reduced off-site disposal frequency by 20–30%. Trade policies encouraging local value-add and reduced export of raw brine streams support investment in modular recovery plants. Regional buyers often prefer turnkey EPC models and local service partnerships to manage remote-site O&M challenges.

Middle East & Africa accounted for 36% of the market in 2024 (~USD 219.6M) and hosts the largest concentration of utility-scale desalination capacity—plants and regional hubs with unit sizes ranging from 10,000 m³/day up to >1,000,000 m³/day modules. Demand drivers include municipal desalination expansion, petrochemical and industrial complex integrations, and large infrastructure projects. Technological modernization trends emphasize high-recovery RO hybrids, energy-recovery pressure exchangers, and large-scale crystallizers to minimize marine discharge liabilities. Regional trade partnerships and sovereign-backed PPP pipelines have mobilized multi-hundred-million USD project tranches for brine treatment and valorization. A number of regional operators scaled up centralized brine-concentration hubs, adding capacity by 30–40% in 2023–2024 to service multiple coastal plants. Consumer/market behavior favors centralized, large-scale solutions with long-term EPC and O&M contracts and strong government participation.

Saudi Arabia – 22% Market Share: Large desalination capacity, national desalination programs, and major utility investments drive high deployment of brine-management systems in utility and industrial projects.

China – 18% Market Share: Extensive industrial clusters, heavy investment in modular ZLD pilots, and rapid municipal retrofit programs underpin China’s leading role in brine-technology adoption.

The Brine Management Technology Market is competitive and evolving, with well over 120 active technology vendors, EPC contractors, system integrators, and specialist service providers competing across utility, industrial and mining segments. Market players range from full-service global water majors and engineering firms to fast-moving specialists in membranes, crystallizers, and mineral-recovery technologies. Market positioning varies: global EPCs and water majors dominate large utility and mega-plant contracts and integrated O&M portfolios, while specialist providers lead in modular ZLD, membrane-crystallizer packages, and direct-lithium/brine-valorization pilots. Strategic activity in 2023–2024 included multiple freestanding product launches, partnership agreements for DLE and brine-to-resource pilots, targeted acquisitions to add salt-recovery capabilities, and multi-million-dollar project awards for mega desalination hubs and centralized brine nodes. Innovation trends accelerating competition include modular containerized ZLD offerings (deployed in hundreds of pilots), electrochemical and ion-selective extraction units for critical-mineral recovery, and AI/IoT-enabled predictive O&M that reduces downtime and chemical use by double-digit percentages in verified pilots.

The market’s structure is moderately concentrated at the top but broadly fragmented overall: a handful of global players secure the largest utility and EPC contracts while numerous regional specialists capture niche, retrofit, and modular work. The combined share of the top 5 companies is approximately 42%, leaving substantial opportunity for mid-size and specialist firms to win lane-specific or value-added work (e.g., lithium pre-conditioning, salt crystallization, mobile ZLD). For decision-makers, competitive positioning now hinges on integrated service capability (EPC + O&M + financing), demonstrated low-energy solutions, and commercial models that convert disposal costs into recoverable product value.

Aquatech

Acciona

SUEZ

Doosan Heavy Industries & Construction

CMI

DESALCO

Technology is the primary differentiator in brine management economics, operational risk, and potential revenue recovery. Key current technologies include high-recovery membrane concentration (advanced HR-RO stacks and two-pass RO hybrids), mechanical and thermal concentrators (MVR/MVC), membrane-crystallizer hybrids, electrochemical recovery systems, ion-selective sorption and DLE pre-conditioning, and fully containerized, skid-mounted ZLD modules. Operational pilots in 2023–2024 have demonstrated measurable performance gains: modular membrane-crystallizer packages cut commissioning time by roughly 30–40% compared with stick-built thermal plants, and retrofits combining energy-recovery pressure exchangers with HR-RO have delivered 20–30% reductions in specific energy use in field trials.

Emerging technologies raising strategic value include selective extraction platforms for lithium and other critical minerals, electrochemical concentration methods that lower chemical dosing, and hybrid systems that balance membrane throughput with limited thermal steps to avoid prohibitive OPEX. Digital enablers — AI-driven scaling prediction, real-time sensor telemetry, and predictive maintenance — are now standard in new builds and in >30% of recent modular contracts; these tools extend membrane life, reduce unplanned shutdowns, and lower chemical consumption rates by double-digit percentages in reported implementations. Business models are also evolving: vendors increasingly offer outcome-based contracts (performance guarantees, pay-for-water or pay-for-recovery), O&M bundles, and partnerships with mineral processors to monetize recovered salts or critical minerals. For decision-makers, technology choices should be evaluated across lifecycle metrics — energy per cubic metre of recovered water, salt recovery yield (% of concentrated brine converted to product), mean time between maintenance, and speed-to-commissioning — rather than CAPEX alone, because these metrics directly affect total cost of ownership and the potential to convert a disposal liability into a revenue stream.

In July 23, 2024, Saltworks completed delivery and commissioning of a full-scale lithium hydroxide recrystallizer for Canada’s first EV battery plant, enabling on-site conditioning of lithium eluates and reducing logistics for downstream refining while supporting battery-grade product handling. Source: www.saltworkstech.com

In May 14, 2024, Veolia (via SIDEM) was awarded a $320 million technology contract for the Hassyan RO desalination plant (818,000 m³/day capacity), supporting large-scale desalination capacity expansion and integration of energy-efficient RO technologies for regional water supply. Source: www.veolia.com

In March–June 2023/2024, Aquatech announced strategic partnerships and technology integrations to advance brine concentration and lithium/critical-minerals processing, and in 2024 joined PFAS-destruction collaborations to treat concentrated waste streams—strengthening its project pipeline for brine valorization and on-site recovery. Source: www.aquatech.com

In 2023–2024, IDE closed and began construction on the Prospect Lake (Fort Lauderdale) P3 water project (50 MGD) and continued major desalination and brine-handling project work—furthering municipal reuse, high-recovery RO deployments, and brine-management design activity across multiple regions. Source: ide-tech.com

This report provides a comprehensive evaluation of the Brine Management Technology Market’s technical, commercial, and strategic landscape. Scope covers technology segmentation (membrane concentration, HR-RO hybrids, thermal concentrators, MVR/MVC crystallizers, electrochemical and ion-selective recovery, containerized/modular ZLD systems), application segmentation (municipal desalination brines, mining and mineral-processing brines, oil & gas produced-water concentration, chemical/process industry brines, food and beverage effluents, and power-plant reject streams), and end-user segmentation (utilities/desalination operators, mining and minerals processors, oil & gas producers, chemical manufacturers, food processors, and third-party service/O&M providers).

Geographically the report assesses North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level profiles for leading markets, installed capacity bands (from <5,000 m³/day modular units to >100,000 m³/day mega-plants), project counts, and typical procurement models (EPC, PPP, performance-based O&M). It examines technology performance metrics — energy per unit recovered, salt recovery yield (mass %), footprint and tankering reductions, and commissioning lead times — and maps these to commercial outcomes such as lifecycle operating costs, service contract structures, and monetization pathways through resource recovery (salts, magnesium, lithium precursors).

Additional chapters analyze competitive positioning and consolidation trends, financing models (project finance, EPC guarantees, offtake agreements for recovered products), regulatory and ESG frameworks shaping permitting and discharge limits, and operational readiness (skills, spare parts, and digital O&M). Niche sectors addressed include DLE pre-conditioning for battery metals, mobile ZLD for remote mining operations, and industrial cluster hub strategies for centralized brine valorization. The scope is designed to support decision-makers in procurement, investment, and technology selection with actionable metrics, scenario modelling, and go-to-market guidance for deploying scalable, lower-energy brine-management systems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 610.0 Million |

| Market Revenue (2032) | USD 1,071.8 Million |

| CAGR (2025–2032) | 7.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Veolia, IDE Technologies, Saltworks Technologies, Aquatech, SUEZ, Doosan Heavy Industries & Construction, CMI, DESALCO |

| Customization & Pricing | Available on Request (10% Customization Free) |