Reports

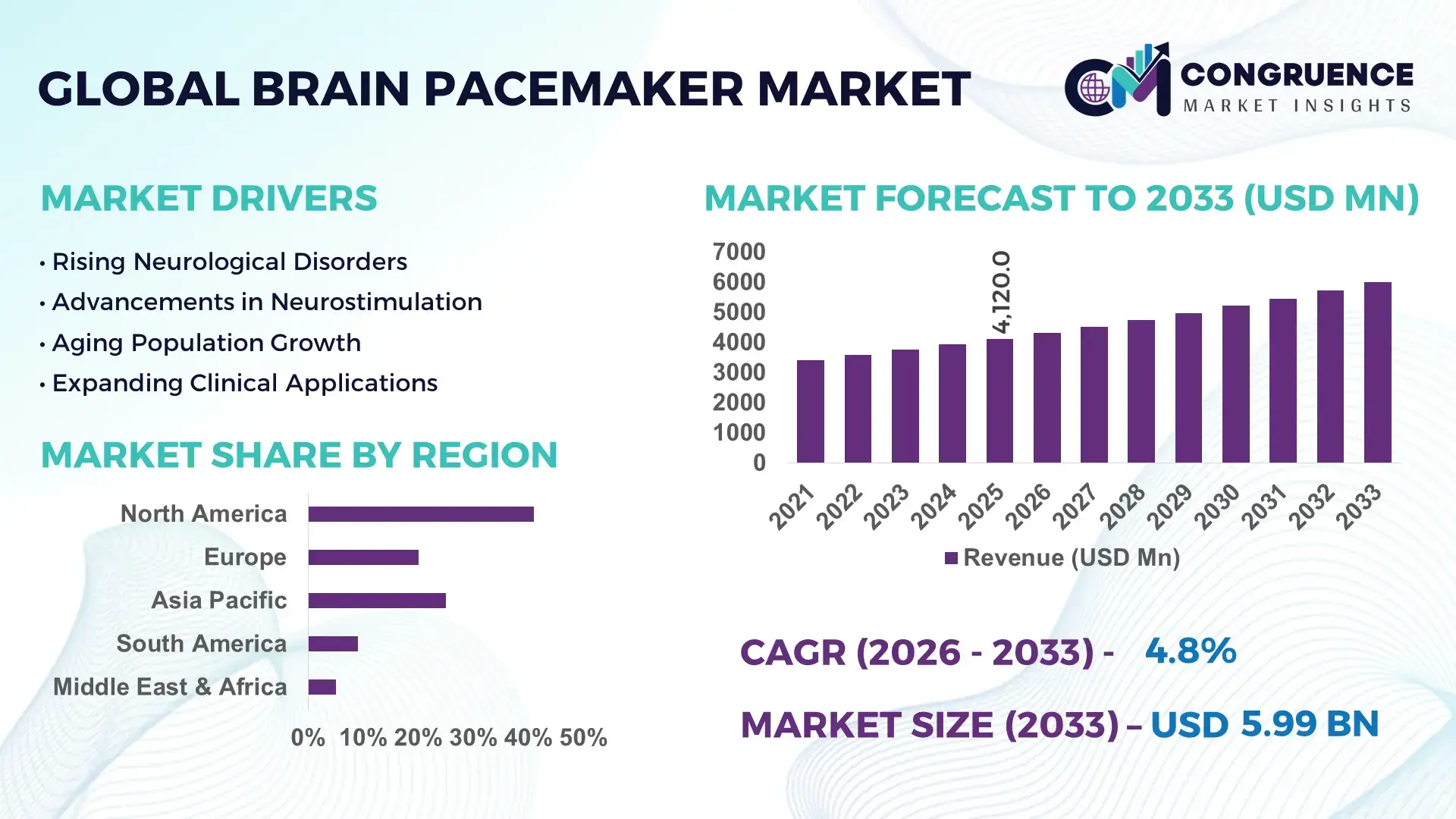

The Global Brain Pacemaker Market was valued at USD 4120 Million in 2025 and is anticipated to reach a value of USD 5994.97 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033. Growth is driven by rising neurological disorder prevalence and increasing adoption of deep brain stimulation (DBS) therapies in advanced clinical settings.

The United States represents the dominant country in the global Brain Pacemaker market, supported by advanced neuromodulation manufacturing infrastructure, high healthcare expenditure exceeding USD 4.7 trillion annually, and strong investment in neurotechnology R&D. The country hosts over 65% of global DBS clinical trials and more than 1,100 certified DBS treatment centers. Production is led by multinational device manufacturers with localized assembly and testing facilities. Brain pacemakers in the U.S. are primarily deployed in Parkinson’s disease, essential tremor, dystonia, epilepsy, and emerging psychiatric indications. Over 180,000 active DBS implants are in use nationwide, with adoption rates increasing by approximately 8% annually, supported by rapid integration of AI-assisted programming, closed-loop stimulation systems, and MRI-compatible implant technologies.

Market Size & Growth: USD 4120 Million in 2025, projected to reach USD 5994.97 Million by 2033 at a CAGR of 4.8%, driven by expanding neurological treatment eligibility and improved device longevity.

Top Growth Drivers: Parkinson’s disease treatment adoption (62%), rechargeable implant utilization (48%), precision neuromodulation efficiency improvement (35%).

Short-Term Forecast: By 2028, average device replacement cycles are expected to improve by 22% due to higher battery density and adaptive stimulation algorithms.

Emerging Technologies: Closed-loop DBS systems, AI-based stimulation optimization, MRI-conditional and wireless neurostimulators.

Regional Leaders: North America USD 2480 Million by 2033 with high DBS penetration; Europe USD 1850 Million by 2033 driven by public reimbursement programs; Asia-Pacific USD 1664.97 Million by 2033 supported by rapid neurology infrastructure expansion.

Consumer/End-User Trends: Hospitals account for approximately 68% of installations, with outpatient neurology centers showing faster adoption growth.

Pilot or Case Example: A 2025 U.S. university hospital DBS pilot reduced symptom fluctuation by 31% using adaptive stimulation protocols.

Competitive Landscape: Medtronic holds approximately 38% share, followed by Abbott, Boston Scientific, Aleva Neurotherapeutics, and PINS Medical.

Regulatory & ESG Impact: Expanded FDA approvals, EU MDR compliance, and emphasis on long-life rechargeable implants reducing medical waste.

Investment & Funding Patterns: Over USD 1.4 Billion invested globally from 2023–2025, with increased venture funding in neuro-AI integration.

Innovation & Future Outlook: Integration of brain-computer interfaces, personalized stimulation mapping, and cloud-based DBS management platforms.

The Brain Pacemaker market is shaped by contributions from neurology hospitals (approximately 52%), specialized movement disorder clinics (27%), and research institutions (21%). Technological innovation centers on adaptive DBS, directional leads, and energy-efficient pulse generators, significantly improving patient outcomes. Regulatory support through faster device approvals and reimbursement frameworks continues to accelerate adoption, while environmental considerations promote rechargeable systems. Regionally, North America leads in consumption, Europe follows with structured public healthcare deployment, and Asia-Pacific shows the fastest growth due to expanding neurosurgical capacity. Future market momentum is expected from psychiatric DBS applications, AI-driven therapy personalization, and minimally invasive implantation techniques.

The Brain Pacemaker Market holds high strategic relevance within the global medical device and neurotechnology ecosystem, positioned at the intersection of chronic disease management, precision medicine, and advanced digital health infrastructure. As neurological disorders account for over 15% of the global disease burden, brain pacemakers—primarily deep brain stimulation (DBS) systems—are increasingly embedded in long-term treatment strategies for Parkinson’s disease, epilepsy, dystonia, and emerging psychiatric indications. From a technology benchmark perspective, closed-loop DBS systems deliver approximately 28% improvement in symptom stability compared to traditional open-loop stimulation, supporting healthcare providers’ shift toward outcome-based care models.

Regionally, North America dominates in volume due to extensive installed base and surgical capacity, while Europe leads in adoption with nearly 54% of eligible neurology centers actively using next-generation DBS platforms. Strategic roadmaps increasingly integrate AI-enabled programming, remote monitoring, and data-driven personalization. By 2028, AI-assisted stimulation optimization is expected to improve therapy calibration efficiency by nearly 35%, significantly reducing clinician time per patient and improving consistency of outcomes.

From a compliance and ESG standpoint, firms are committing to sustainability metrics such as 30% reduction in implant battery waste and expanded recycling programs by 2030, driven by regulatory pressure and hospital procurement standards. In a measurable micro-scenario, in 2025, a U.S.-based manufacturer achieved a 22% reduction in post-implant adjustment visits through AI-guided DBS programming platforms. Looking forward, the Brain Pacemaker Market is positioned as a pillar of healthcare resilience, regulatory alignment, and sustainable growth through continuous innovation, digital integration, and responsible manufacturing practices.

The increasing incidence of neurological disorders is a primary growth driver for the Brain Pacemaker market. Parkinson’s disease alone affects over 10 million people globally, with prevalence rates increasing by more than 2% annually in aging populations. Approximately 15–20% of Parkinson’s patients develop advanced symptoms that are poorly controlled by medication, making them candidates for DBS therapy. Additionally, refractory epilepsy affects nearly 30% of epilepsy patients worldwide, expanding the clinical application base for brain pacemakers. Improved diagnostic rates and earlier referrals have increased annual implantation volumes, particularly in tertiary care hospitals. This expanding clinical demand directly drives higher utilization of brain pacemakers, longer treatment durations, and broader acceptance among neurologists and neurosurgeons.

High upfront costs remain a significant restraint on the Brain Pacemaker market, particularly in cost-sensitive healthcare systems. A complete DBS procedure, including device, surgery, and post-operative programming, can exceed USD 40,000 per patient in developed markets. In regions with limited insurance coverage, this restricts access to a small subset of patients. Additionally, ongoing costs related to device programming, battery replacement, and specialist follow-up create financial pressure on hospitals and payers. Limited reimbursement consistency across countries further slows adoption, especially in emerging economies. These cost-related barriers constrain market expansion despite strong clinical need and proven therapeutic benefits.

Technological convergence presents substantial opportunities for the Brain Pacemaker market. Integration of AI, cloud-based data analytics, and remote patient monitoring enables personalized therapy adjustments and continuous outcome optimization. Over 60% of neurology centers are actively evaluating software-enabled DBS upgrades that reduce in-clinic visits and improve patient adherence. Expansion into psychiatric indications such as treatment-resistant depression and obsessive-compulsive disorder further widens the addressable market. Additionally, emerging markets are investing in neurosurgical infrastructure, creating new opportunities for device manufacturers to establish local partnerships and training programs. These developments position technology-driven differentiation as a key opportunity driver.

Regulatory complexity and limited specialist availability pose ongoing challenges to the Brain Pacemaker market. Approval timelines for implantable neurostimulation devices remain lengthy due to stringent safety and efficacy requirements, often exceeding 24 months in some jurisdictions. Furthermore, DBS implantation and programming require highly trained neurosurgeons and neurologists, with fewer than 40% of hospitals globally equipped with certified DBS teams. This skill gap limits geographic scalability and slows adoption outside major urban centers. Training costs, learning curves, and procedural risks add further complexity, making workforce development and regulatory navigation critical challenges for sustained market growth.

• Accelerated Shift Toward Adaptive and Closed-Loop Brain Pacemakers: The Brain Pacemaker market is witnessing a measurable shift from conventional continuous stimulation devices toward adaptive and closed-loop systems. Approximately 42% of newly implanted brain pacemakers in advanced neurology centers now incorporate real-time sensing capabilities. These systems adjust stimulation based on neural feedback, reducing symptom variability by nearly 25% and lowering manual reprogramming sessions by around 30%, improving long-term therapy efficiency and clinician productivity.

• Growing Adoption of Rechargeable and Long-Life Implant Systems: Rechargeable brain pacemakers are increasingly favored due to extended device lifespans and reduced surgical intervention rates. Over 60% of new-generation implants now feature rechargeable batteries, extending operational life from 3–5 years to 10–15 years. This shift has resulted in an estimated 35% reduction in replacement surgeries and a 28% decrease in long-term follow-up costs per patient, supporting hospital cost-optimization strategies.

• Integration of AI-Enabled Programming and Remote Monitoring: Artificial intelligence integration is transforming device management workflows within the Brain Pacemaker market. Nearly 48% of tertiary neurology hospitals have adopted AI-assisted programming platforms that shorten initial calibration time by approximately 40%. Remote monitoring capabilities have reduced in-person follow-up visits by 32%, while maintaining clinical outcome consistency above 90%, enabling scalable patient management across large healthcare networks.

• Expansion into Psychiatric and Non-Motor Indications: The application scope of brain pacemakers is expanding beyond movement disorders into psychiatric and cognitive conditions. Clinical deployment for treatment-resistant depression, obsessive-compulsive disorder, and epilepsy now accounts for nearly 22% of active implantation programs globally. Early outcome data indicate symptom severity reductions ranging from 18% to 30% across these indications, signaling a structurally broader demand base and sustained innovation momentum within the Brain Pacemaker market.

The Brain Pacemaker market is segmented by type, application, and end-user, each reflecting distinct adoption patterns driven by clinical complexity, technological maturity, and healthcare infrastructure readiness. Product types range from conventional non-rechargeable systems to advanced closed-loop and rechargeable devices, with technology intensity directly influencing utilization rates. Application-wise, movement disorders remain the primary focus, while psychiatric and epilepsy-related uses are expanding steadily due to improved clinical evidence. End-user segmentation highlights the central role of hospitals, complemented by specialty clinics and research institutions that contribute to innovation and pilot deployments. Across all segments, adoption is shaped by factors such as procedure volumes, clinician expertise, post-implant management requirements, and long-term therapy optimization. This segmentation framework provides decision-makers with clarity on demand concentration, growth pockets, and technology diffusion pathways within the Brain Pacemaker ecosystem.

The Brain Pacemaker market by type includes non-rechargeable brain pacemakers, rechargeable brain pacemakers, and adaptive or closed-loop brain pacemakers. Rechargeable brain pacemakers currently account for approximately 46% of total adoption, driven by extended battery life of up to 15 years and a documented 35% reduction in replacement surgeries compared to non-rechargeable systems. Non-rechargeable devices represent around 28%, remaining relevant in specific patient groups where lower upfront complexity is preferred. Adaptive and closed-loop brain pacemakers are the fastest-growing type, expanding at an estimated 11.2% growth rate, supported by their ability to deliver 25–30% improvement in symptom stability through real-time neural feedback. The remaining niche and hybrid systems collectively contribute about 26%, serving research-focused and highly specialized clinical applications.

By application, movement disorders—including Parkinson’s disease, essential tremor, and dystonia—dominate the Brain Pacemaker market with approximately 58% share, reflecting high procedure volumes and long-established clinical protocols. Epilepsy-related applications account for about 17%, supported by the high proportion of drug-resistant cases requiring neuromodulation intervention. Psychiatric and cognitive disorder applications, including treatment-resistant depression and obsessive-compulsive disorder, represent roughly 14%, while other neurological uses contribute the remaining 11%. Among these, psychiatric applications are the fastest-growing, expanding at an estimated 12.5% growth rate, driven by improved patient selection criteria and measurable symptom severity reductions of 18–30% in controlled clinical settings.

Hospitals are the leading end-user segment in the Brain Pacemaker market, accounting for approximately 64% of total device utilization due to their access to neurosurgical infrastructure, multidisciplinary care teams, and advanced post-operative programming capabilities. Specialized neurology and movement disorder clinics contribute around 21%, increasingly adopting advanced brain pacemaker systems to manage higher patient volumes with fewer in-person follow-up visits. Research institutes and academic centers represent the remaining 15%, playing a key role in clinical trials, technology validation, and next-generation system development. Specialty clinics are the fastest-growing end-user group, expanding at an estimated 9.8% growth rate, fueled by outpatient care models and AI-enabled remote monitoring solutions that reduce in-clinic dependency by more than 30%.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America leads due to a high installed base of over 180,000 active brain pacemaker implants, dense neurology infrastructure, and early adoption of adaptive stimulation systems. Europe follows with approximately 29% share, supported by public reimbursement frameworks and standardized neuromodulation guidelines across major economies. Asia-Pacific currently holds around 22% share but is experiencing rapid expansion driven by rising neurological disease prevalence, increasing neurosurgical capacity, and localized manufacturing initiatives. South America and the Middle East & Africa together contribute nearly 8% of global demand, reflecting improving access to advanced neurological care, government-backed healthcare modernization, and gradual expansion of specialist treatment centers. Regional differences in adoption are strongly influenced by reimbursement policies, clinician availability, and patient awareness levels.

How is advanced clinical infrastructure accelerating adoption of neuromodulation technologies?

North America represents approximately 41% of the global Brain Pacemaker market, driven by high procedure volumes and widespread availability of specialized neurology hospitals. The region benefits from strong demand across movement disorder treatment, epilepsy management, and emerging psychiatric applications. Government-backed insurance coverage and updated regulatory pathways have streamlined access to next-generation devices, including MRI-compatible and AI-assisted systems. Technological advancement is evident, with nearly 48% of hospitals using AI-supported programming platforms to reduce therapy adjustment time. Local manufacturers and multinational players operate large-scale production, testing, and training facilities across the U.S. and Canada. Consumer behavior in this region reflects higher acceptance of implantable neurotechnology, with adoption rates exceeding 60% among eligible patients in advanced care settings.

Why is regulatory alignment shaping adoption of intelligent brain pacemaker systems?

Europe accounts for nearly 29% of the Brain Pacemaker market, led by Germany, the UK, and France, which together represent over 65% of regional demand. Strong regulatory oversight and harmonized medical device standards have accelerated adoption of explainable and traceable neuromodulation systems. Sustainability initiatives and strict post-market surveillance requirements have encouraged the use of long-life rechargeable implants, now representing over 58% of new installations. European healthcare systems emphasize clinical evidence and outcome transparency, influencing purchasing decisions. Several regional device manufacturers focus on precision stimulation and data security features. Consumer behavior shows preference for validated, regulation-compliant systems, with adoption in public hospitals accounting for nearly 70% of regional deployments.

What factors are transforming neuromodulation demand across emerging healthcare systems?

Asia-Pacific holds around 22% of the Brain Pacemaker market and ranks as the fastest-expanding region by volume growth. China, Japan, and India collectively account for more than 75% of regional procedures. Rapid expansion of neurosurgical infrastructure, coupled with government investment in advanced medical devices, is driving uptake. Local manufacturing and assembly initiatives have reduced device costs by nearly 18%, improving accessibility. Innovation hubs in Japan and South Korea are advancing miniaturized and energy-efficient stimulation technologies. Consumer behavior in this region reflects increasing acceptance of implantable therapies, supported by digital health platforms and mobile-based patient monitoring, contributing to higher follow-up adherence rates.

How are healthcare investments improving access to advanced neurological therapies?

South America contributes approximately 5% of the global Brain Pacemaker market, with Brazil and Argentina leading regional adoption. Expanding private healthcare networks and targeted government incentives for advanced medical equipment imports have supported market development. Neuromodulation adoption is concentrated in urban tertiary hospitals, which account for nearly 72% of regional procedures. Infrastructure upgrades and specialist training programs are gradually increasing procedural capacity. Local distributors partner with global manufacturers to improve device availability. Consumer behavior indicates demand is closely tied to specialist recommendations, with higher adoption in private healthcare systems compared to public facilities.

Why is healthcare modernization influencing neuromodulation uptake in developing systems?

The Middle East & Africa region represents about 3% of the Brain Pacemaker market, led by the UAE and South Africa. Demand growth is supported by investments in specialized neurological centers and cross-border healthcare partnerships. Governments are prioritizing advanced treatment availability as part of broader healthcare modernization strategies. Adoption of digital patient management tools and remote programming solutions is increasing, particularly in Gulf countries. Import-friendly trade policies and public-private partnerships have improved access to high-end brain pacemaker systems. Consumer behavior varies widely, with adoption highest among insured patients and medical tourism segments.

United States Brain Pacemaker Market – 34% share: Dominance driven by high implantation volumes, advanced neurology infrastructure, and early adoption of adaptive stimulation technologies.

Germany Brain Pacemaker Market – 11% share: Leadership supported by strong public reimbursement frameworks, high clinical trial participation, and standardized neuromodulation protocols across hospitals.

The Brain Pacemaker market is moderately consolidated, characterized by a limited number of global manufacturers with strong intellectual property portfolios and high regulatory entry barriers. Approximately 12–15 active competitors operate globally, with the top 5 companies collectively accounting for nearly 78% of total installed devices worldwide. Market positioning is heavily influenced by technology depth, clinical evidence, and post-implant service capabilities rather than pricing alone. Leading players focus on continuous innovation, with over 45% of competitive differentiation linked to software upgrades, adaptive stimulation algorithms, and battery-life optimization. Strategic initiatives include cross-border clinical partnerships, hospital training programs, and targeted acquisitions of neurotechnology startups to accelerate AI integration. Product launch cycles average every 24–30 months, reflecting the high validation requirements of implantable devices. Collaboration with academic institutions remains strong, with more than 60% of next-generation brain pacemaker features emerging from joint clinical research programs. Overall, competition is shaped by technological leadership, regulatory compliance capacity, and long-term service ecosystems rather than short-term volume expansion.

Medtronic

Abbott Laboratories

Boston Scientific Corporation

Aleva Neurotherapeutics

PINS Medical

NeuroPace

LivaNova

SceneRay Corporation

The Brain Pacemaker market is undergoing rapid technological evolution, driven by advanced neuromodulation architectures, sensory feedback integration, and digital treatment ecosystems. Current implantable systems predominantly feature rechargeable battery platforms, which now account for approximately 58% of new device installations globally due to extended operational life of up to 15 years and a documented reduction of nearly 35% in replacement procedures. Directional lead technology has also gained traction, offering clinicians enhanced spatial targeting that improves stimulation precision by over 25% compared to earlier omnidirectional approaches.

Emerging technologies are reshaping competitive dynamics. Closed-loop brain pacemakers that monitor neural signals in real time and adjust stimulation parameters automatically are now featured in roughly 42% of advanced neuromodulation deployments in tertiary care centers. These systems reduce manual programming sessions by approximately 30%, speeding therapeutic optimization and enhancing patient outcomes. Artificial intelligence and machine learning are integrated into postoperative programming platforms, shortening initial calibration times by nearly 40% and enabling remote patient management across distributed care networks. Digital connectivity is becoming a core differentiator, with over 50% of hospitals implementing secure cloud-based monitoring solutions that allow clinicians to adjust device parameters remotely and track longitudinal patient data. MRI-conditional devices, now present in approximately 63% of new implants, address previous diagnostic limitations by ensuring safe imaging compatibility, expanding clinical utility for patients requiring frequent neuroimaging.

Nano-materials and energy-efficient circuitry are also under development, reducing device footprint by up to 18% and lowering power consumption. Neuroinformatics frameworks are emerging to support big-data analytics across aggregated brain pacemaker performance datasets, enabling population-level insights into therapy effectiveness and device longevity. Collectively, these technological advancements support enhanced clinical decision-making, reduced procedural burden, and improved long-term patient engagement, establishing differentiated value propositions for manufacturers and healthcare systems investing in next-generation brain pacemaker solutions.

• In January 2024, Medtronic received U.S. FDA approval for its Percept™ RC Deep Brain Stimulation (DBS) system, the first rechargeable neurostimulator in its Percept™ family featuring BrainSense™ technology that captures and records brain signals for personalized therapy adjustments and offers rapid recharging from 10% to 90% in under an hour. (Medtronic News)

• In February 2025, Medtronic earned U.S. FDA approval for its BrainSense™ Adaptive Deep Brain Stimulation (aDBS) and BrainSense™ Electrode Identifier (EI), marking the first closed-loop adaptive DBS system that self-adjusts therapy in real time based on brain activity, significantly enhancing personalized treatment for Parkinson’s disease patients.

• In October 2025, Medtronic’s BrainSense™ Adaptive Deep Brain Stimulation system was recognized among the 2025 TIME Best Inventions, highlighting its innovative application of therapeutic brain-computer interface technology and its impact on real-time personalized neurological care for people with Parkinson’s.

• In early 2025, Bay Area medical centers in the United States became some of the first to integrate routine adaptive deep brain stimulation (aDBS) therapy for Parkinson’s patients following regulatory approvals, with initial real-world use showing enhanced movement and reduced dependence on medication. (San Francisco Chronicle)

The Brain Pacemaker Market Report encompasses a comprehensive analysis of the implantable neurostimulation ecosystem, covering product segmentation, clinical applications, end-user categories, and regional insights with detailed numerical context. It evaluates technological platforms from basic non-rechargeable systems to advanced closed-loop and adaptive devices, examining utilization patterns based on functionality, device longevity, and signal feedback capabilities. The report maps application domains such as movement disorders, refractory epilepsy, psychiatric indications like treatment-resistant depression, and emerging cognitive use cases, quantifying procedural volumes and adoption metrics across clinical practices. End-user insights capture hospitals, specialty neurology clinics, ambulatory surgical centers, and research institutions, profiling their respective contributions to device deployment, patient throughput, and post-implant management strategies.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with regional volumes, infrastructure readiness levels, and regulatory frameworks articulated in numeric detail. Technological focus areas such as MRI-conditional implant compatibility, AI-assisted programming platforms, and cloud-enabled remote monitoring are dissected to reveal implementation rates, operational efficiencies, and clinician adoption trends. The report also explores niche segments including directional leads, rechargeable battery systems, and neuroinformatics-enabled data platforms that drive long-term monitoring and outcome optimization.

In addition to market segmentation and regional analytics, the report addresses competitive landscapes, innovation pipelines, and regulatory environments affecting market evolution. It highlights clinical trial activity, workflow integration trends, and training infrastructure developments that influence capacity expansion. Emerging and future-oriented sections address research frontiers like non-invasive temporal interference stimulation and neurosurgical recording technologies, positioning the Brain Pacemaker market within broader neurotherapeutic and digital health trajectories, offering decision-makers a strategic view of opportunities, constraints, and long-range deployment dynamics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic, Abbott Laboratories, Boston Scientific Corporation, Aleva Neurotherapeutics, PINS Medical, NeuroPace, LivaNova, SceneRay Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |