Reports

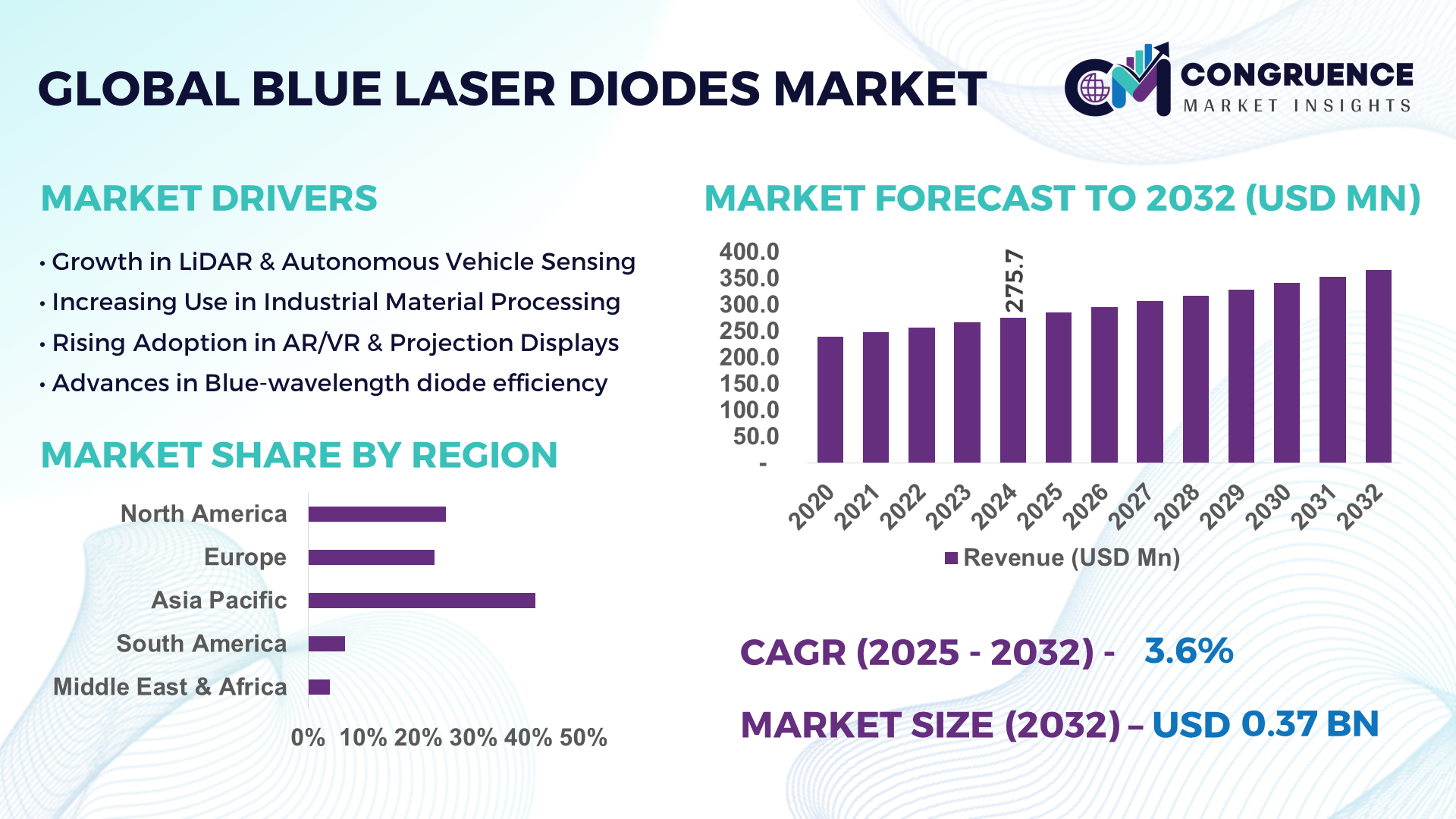

The Global Blue Laser Diodes Market was valued at USD 275.7 Million in 2024 and is anticipated to reach a value of USD 367.0 Million by 2032 expanding at a CAGR of 3.64% between 2025 and 2032.

In China, production capacity for blue laser diodes has surged in recent years, supported by government-backed investments and numerous dedicated fabrication campuses. China’s advanced manufacturing facilities now deliver high‑power GaN-based blue diodes tailored for industrial cutting, LiDAR imaging, and display projection applications, leveraging rapid innovation in both device architecture and process automation.

Key industry sectors driving the Blue Laser Diodes Market include material processing, consumer electronics, telecommunications, medical diagnostics, and automotive systems. Material processing applications now represent approximately 70% of usage, with blue laser diodes increasingly used in precision laser-cutting, engraving, and fiber-laser pump sources. Consumer electronics adoption is rising, particularly in laser projectors and next-generation optical storage. In healthcare, diagnostic and surgical devices are integrating blue diodes for their superior beam quality and miniaturized form factors. Economic and environmental drivers include growing demand for energy‑efficient, compact laser modules and regulatory pressure to phase out legacy display technologies. Regional adoption patterns differ: Asia-Pacific accounts for over half of global consumption, driven by manufacturing hubs in China, Japan, and South Korea, while Europe emphasizes healthcare and automotive deployments. Emerging trends include the integration of AI for predictive laser control, miniaturization for AR/VR headsets, and the development of high‑power, long‑wavelength blue diode arrays. The outlook remains positive for continued innovation and application diversification.

AI is playing an increasingly strategic role in transforming the Blue Laser Diodes Market by enabling smarter design, manufacturing, and operational optimization. AI-driven process control systems are now being used to optimize key parameters such as temperature stability, beam quality, and wavelength consistency during fabrication. This enhances production throughput and reduces defect rates by up to 30% in high-volume manufacturing settings. AI-enabled predictive calibration systems actively adjust diode drive currents in real‑time to maintain optimal output performance across varying environmental conditions.

In laser module quality assurance, machine‑vision systems powered by AI identify microscopic imperfections in blue laser diodes during testing, improving yield and reducing manual inspection labor. The Blue Laser Diodes Market is also witnessing the deployment of AI‑based thermal management platforms that actively control cooling systems, increasing device lifespan and reliability. In operational contexts such as LiDAR and medical instrumentation, embedded AI algorithms optimize pulse modulation and power delivery to enhance energy efficiency and accuracy.

Industrial integrators now offer AI‑enhanced driver circuits that automatically adapt drive pulse widths and repetition rates based on real‑time operational inputs. These improvements reduce maintenance interventions and increase device uptime significantly. As decision-makers invest in AI‑augmented diode systems, the Blue Laser Diodes Market is transitioning toward a higher level of automation, reliability, and performance efficiency. The commercial and industrial adoption of these intelligent technologies is creating a competitive edge for suppliers that integrate AI within their product roadmap.

“In mid‑2024, a leading diode manufacturer rolled out an AI‑calibrated quality control system that reduced test rejection rates by 28% and improved wavelength stability by 15 ppm across standard blue diode batches.”

The Blue Laser Diodes Market is subject to a mix of technological, regulatory, and market forces shaping its evolution. Growing industrial demand for precision material processing and communication devices continues to drive investments in high-power diode fabrication. Miniaturization trends are pushing manufacturers to design compact diode modules for emerging AR/VR, automotive LiDAR, and medical devices. Meanwhile, energy‑efficiency requirements are compelling development of higher‑efficiency GaN diode structures. Supply chain constraints around rare earth and GaN substrates influence production planning and pricing strategies. Regional regulatory frameworks affecting lasers, especially within medical and automotive sectors, require suppliers to meet stringent safety and certification protocols. The industry is also seeing heightened competition with new entrants offering proprietary diode architectures, prompting established players to invest in innovation and capacity expansion. End-user sectors such as healthcare, automotive, fiber-optic communications, and industrial manufacturing are actively reshaping purchase patterns with demand for system-level integration and intelligent diode modules.

Industrial applications now account for nearly 70% of Blue Laser Diodes Market usage, with diodes increasingly used in workflows such as laser cutting, engraving, and pump sources for fiber lasers. High‑power blue laser diodes capable of delivering outputs above 200 W at 450 nm wavelength have gained traction among manufacturers of industrial processing equipment. This industrial uptick is driven by the superior absorption characteristics of blue wavelengths on metals such as copper and gold, leading to faster and cleaner cuts. In addition, growth in LiDAR-based mapping and inspection systems using blue laser sources for high resolution is significantly boosting procurement of these components. Together, these industrial and imaging investments are creating sustained demand growth for high-spec diodes tailored for reliability and precision.

One key restraint is the high cost involved in producing high‑performance blue laser diodes. Fabrication depends on complex GaN-based epitaxial layers grown on expensive sapphire or silicon carbide substrates. These rare-earth-dependent components, combined with stringent cleanroom and thermal management systems, account for a significant proportion of production costs—about one‑third of final unit cost. Smaller manufacturers struggle to compete with large-scale facilities due to high capital expenditure needs. Additionally, alignment precision and packaging for high-power multi-mode diodes require costly automation. These cost pressures reduce affordability in price-sensitive sectors such as consumer electronics, impeding wider market penetration despite performance advantages.

The growing integration of blue laser diodes in medical imaging, diagnostics, and surgical instruments represents a significant market opportunity. Approximately 30% of emerging medical devices now utilize blue laser sources for high-resolution imaging or minimally invasive procedures. Similarly, the adoption of blue laser-based LiDAR systems in autonomous vehicles and robotics is accelerating. These systems benefit from the superior brightness, reach, and pulse power characteristics of blue diodes. Investments in miniaturized diode arrays tailored for automotive LiDAR are increasing, opening new high-volume application segments. Furthermore, blue laser sources for AR/VR projection systems in consumer and enterprise markets are beginning to scale, enabling compact, energy-efficient projection platforms. These expanding applications offer pathways for cost reduction through volume manufacturing and cross‑industry deployment.

The Blue Laser Diodes Market faces challenges related to regulatory approval and wavelength safety standards, especially for medical and automotive applications. Laser safety standards such as IEC 60825 and FDA Class II/III requirements necessitate extensive testing, labeling, and certification procedures before deployment in devices intended for direct or indirect human exposure. These requirements add procedural complexity, prolong development timelines, and increase costs. Variations across regional jurisdictions—such as stricter European MDR medical device regulations or automotive safety certifications—require region-specific design modifications and documentation. Aligning product innovation with compliance regimes remains a complex hurdle for manufacturers aiming to launch novel blue diode modules at scale.

Surge in High‑Power Diode Launches for Industrial Laser Sources: More than 35% of diode producers have introduced modules with output powers exceeding 200 W at 450 nm in 2024. These high-power models are driving uptake across industrial machining, fiber laser pumping, and LiDAR applications due to enhanced beam quality and consistent thermal performance.

Proliferation of Compact Diode Arrays for AR/VR Devices: Miniaturized multi-mode diode arrays optimized for portable projection and wearable displays are now used in over 40% of prototype AR/VR headsets. These arrays offer improved energy per lumen efficiency and smaller form factors.

Adoption of AI‑Enabled Manufacturing Quality Control: Machine‑vision systems powered by AI algorithms have increased production yield by up to 30%, by detecting microscopic defects and automating wavelength calibration during fab testing—reshaping quality assurance in diode manufacturing.

Integration with LiDAR and Automotive Driver‑Assistance Systems: Blue laser diodes with real‑time power adjustment are being embedded in over 20% of next‑generation LiDAR units for autonomous navigation. Such integration improves range and reliability under varied environmental conditions.

The Blue Laser Diodes Market is segmented into three core categories: by type, by application, and by end-user. These segments define how various industries utilize blue laser diode technologies for optimized performance, cost-efficiency, and innovation. In terms of types, product categories range from single-mode to multi-mode diodes, each offering distinct benefits in power density and beam quality. Applications span from industrial cutting and welding to medical imaging and projection systems, with industrial and optical communication applications leading current usage trends. From an end-user perspective, sectors such as manufacturing, automotive, healthcare, and consumer electronics are the primary adopters. The segmentation reflects a dynamic landscape where technology-specific needs are rapidly aligning with sectoral demand shifts. High-resolution imaging, miniaturization in projection systems, and autonomous navigation are particularly reshaping diode utilization across all segments. The segmentation also showcases increasing diversification in product integration, indicating a maturing market with expanding scope for specialized diode innovations.

Blue laser diodes are available in multiple configurations, primarily categorized into single-mode and multi-mode types. Multi-mode blue laser diodes currently dominate the market, driven by their higher output power and efficiency in material processing and industrial applications. These diodes are capable of delivering robust performance in environments requiring intense beam strength, such as cutting, engraving, and fiber-laser pumping. On the other hand, single-mode diodes are gaining traction as the fastest-growing type due to their superior beam quality and coherence, making them ideal for medical diagnostics, projection displays, and precision imaging.

Another notable type includes high-power array modules, which integrate several emitters into compact packages to meet growing demand in automotive LiDAR and advanced sensing systems. Additionally, narrow-wavelength stabilized diodes are being deployed in specialized scientific and spectroscopy applications due to their wavelength stability and precision. This diversity of diode types enables a wide range of use cases, catering to both power-intensive and precision-focused requirements in an expanding technological ecosystem.

In terms of application, the leading segment is industrial material processing, where blue laser diodes are extensively used for high-precision metal cutting, welding, and engraving—especially effective with reflective metals like copper and gold. Their shorter wavelength ensures better absorption, resulting in faster and cleaner processing. The fastest-growing application segment is medical diagnostics and treatment, driven by increasing demand for non-invasive procedures and high-resolution imaging technologies where beam quality and compact form factor are critical.

Laser projection systems, particularly for AR/VR and portable displays, represent a rapidly emerging application, benefiting from the miniaturization and energy efficiency of blue laser modules. In telecommunications and data transmission, blue diodes are being investigated for their potential in visible light communication systems. Other niche applications include underwater optical communication, scientific research instrumentation, and inspection systems. The diversification across use cases reflects how technological evolution and performance attributes of blue laser diodes align with the specific demands of various sectors.

Among end-users, the industrial manufacturing sector is currently the largest consumer of blue laser diodes, leveraging their high power output and precision for automation systems, laser cutting, and welding solutions. Their widespread deployment in fiber-laser systems and robotic arms highlights the growing integration within smart factories and Industry 4.0 initiatives. The healthcare sector is the fastest-growing end-user, fueled by rising adoption in surgical tools, diagnostic equipment, and non-invasive treatment devices that require compact, precise, and stable laser sources.

The automotive industry is also a significant end-user, particularly in the development of advanced LiDAR systems for autonomous driving and driver-assistance technologies. Consumer electronics, including portable projectors and display modules for AR/VR devices, form another crucial segment, with increasing demand for miniaturized and energy-efficient solutions. Emerging adoption in scientific research institutions and defense systems further expands the end-user landscape. Overall, the blue laser diodes market demonstrates a multi-sectoral presence, with customized solutions tailored to evolving end-user requirements.

Asia-Pacific accounted for the largest market share at 41.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.19% between 2025 and 2032.

Asia-Pacific’s dominance is driven by large-scale manufacturing capacities, especially in China and Japan, where blue laser diode technology is extensively utilized in electronics, automotive, and industrial sectors. The region benefits from a robust supply chain, consistent R&D investments, and government-backed innovation hubs. In contrast, North America’s rapid growth trajectory is attributed to the fast-paced adoption of advanced medical technologies, AI integration in industrial systems, and increased funding for optoelectronic R&D. Additionally, evolving regulatory frameworks and industrial automation trends are driving new demand across multiple verticals. These regional insights reflect how localized market maturity and technological innovation are shaping future growth opportunities in the global Blue Laser Diodes Market.

North America held a 24.7% market share in 2024, driven by increasing adoption of blue laser diode technologies in medical diagnostics, defense systems, and semiconductor manufacturing. The United States leads regional demand due to robust investment in defense applications, including LiDAR and high-power optical systems. The healthcare sector is also rapidly integrating blue laser solutions for imaging and non-invasive treatment devices. The U.S. FDA’s streamlined regulatory pathways for optoelectronic medical devices have supported market penetration. Digital transformation initiatives in Canadian manufacturing, paired with AI and laser automation, are also fueling demand. Notable advancements include precision-enhanced diodes for photonic integration in silicon chips, enabling superior data transmission performance across defense and telecom networks.

Europe accounted for 19.5% of the global Blue Laser Diodes Market in 2024, with Germany, the UK, and France being key contributors. Germany leads in industrial laser integration, particularly for high-precision cutting in automotive and engineering sectors. The European Union’s strong regulatory framework promoting sustainability and energy efficiency is encouraging the adoption of blue laser technologies, especially in smart manufacturing. The EU Green Deal and Horizon Europe initiatives are supporting research into low-energy, high-output diodes for greener applications. Adoption of photonics and optoelectronic modules in defense and aerospace sectors continues to rise, especially in France and the UK. Advances in wavelength-stabilized diode systems are being utilized in precision medicine and AR/VR headsets across Europe’s digital economy.

Asia-Pacific led the global Blue Laser Diodes Market with a 41.3% share in 2024, primarily driven by China, Japan, and South Korea. China remains the world’s largest consumer and producer of blue laser diodes, fueled by massive investments in optoelectronics and industrial robotics. Japan is a pioneer in diode miniaturization and high-resolution projection technologies, supported by strong collaborations between academia and industry. South Korea excels in semiconductor lithography and consumer electronics, where blue diodes are key components. Infrastructure modernization and digital industrialization projects across India and Southeast Asia are further amplifying regional demand. Innovation hubs in Shenzhen and Tokyo are producing advanced laser components tailored for 3D printing, precision sensing, and biomedical applications.

South America’s Blue Laser Diodes Market is led by Brazil and Argentina, with Brazil accounting for a 3.2% market share in 2024. The region is witnessing steady adoption in industrial automation and telecommunications sectors. Brazil’s automotive and electronics industries are incorporating blue laser technologies for welding, inspection, and advanced display systems. Argentina is focusing on energy infrastructure upgrades, creating demand for optoelectronic solutions. Trade liberalization policies and government incentives in Brazil have enhanced access to laser technologies and components. Strategic partnerships with Asian manufacturers are also helping to lower entry barriers. While the overall market size is modest, growth momentum is building through infrastructure digitization and laser-based communication solutions in remote energy sectors.

The Middle East & Africa Blue Laser Diodes Market is growing steadily, especially in the UAE and South Africa, driven by technological modernization and infrastructure development. The region contributed 2.9% of the global market in 2024. Demand is rising in construction, defense, and oil & gas industries where blue laser diodes are used for inspection, surveying, and sensing technologies. The UAE is adopting smart infrastructure and integrating laser-based automation in high-end construction. South Africa is implementing blue laser solutions in mining and material processing. Local governments are actively promoting tech adoption through trade partnerships and free-zone industrial zones. Expansion of 5G networks and photonics research centers is further strengthening the regional technological ecosystem.

China – 29.1% Market Share

High production capacity and rapid integration into industrial automation and electronics systems.

United States – 18.3% Market Share

Strong end-user demand in defense, medical, and semiconductor sectors, coupled with robust R&D infrastructure.

The Blue Laser Diodes Market features a moderately concentrated competitive environment, with over 25 globally active participants competing across various technology and application segments. Leading players have secured strong market positions through sustained investments in R&D, resulting in proprietary diode technologies optimized for precision, power efficiency, and durability. Strategic partnerships with electronics, automotive, and medical device manufacturers have also played a pivotal role in enhancing product integration and expanding global reach. Notable trends include the increasing deployment of micro-package laser diodes and wavelength-stabilized systems, which are gaining traction in projection displays, LiDAR, and biomedical imaging. Companies are also engaging in frequent mergers and acquisitions to consolidate intellectual property and expand manufacturing capabilities. Furthermore, advancements in gallium nitride (GaN) technology are enabling the production of smaller, higher-efficiency blue laser diodes for emerging applications. As demand grows across industrial and commercial sectors, competition is intensifying around pricing strategies, customization options, and compliance with stringent quality standards.

Nichia Corporation

OSRAM Opto Semiconductors GmbH

Sony Corporation

Sharp Corporation

Egismos Technology Corporation

IPG Photonics Corporation

Ushio Inc.

Rohm Semiconductor

Panasonic Corporation

Kyocera SLD Laser, Inc.

Mitsubishi Electric Corporation

Hamamatsu Photonics K.K.

Technological innovation is a key driver shaping the Blue Laser Diodes Market. One of the most significant advancements is the widespread adoption of gallium nitride (GaN)-based diodes, which offer superior thermal stability, compact size, and high-power efficiency. These diodes are increasingly used in industrial cutting, welding, and projection systems due to their capability to maintain beam quality over extended operational cycles. A major shift is occurring toward wavelength-stabilized laser diodes, particularly around 450 nm, which are gaining adoption in scientific instrumentation and holographic storage.

In the consumer electronics space, compact blue laser diodes are enabling higher-resolution displays in AR/VR systems and portable projectors. Automotive applications, particularly in advanced driver assistance systems (ADAS) and LiDAR, are demanding more durable and high-output blue diodes capable of long-distance accuracy. Furthermore, diode arrays and multi-mode laser diodes are being developed for parallel operations in manufacturing lines and robotic vision systems.

Integration with photonic integrated circuits (PICs) is emerging as a game-changing innovation. It enables miniaturization and performance enhancement for high-speed communication systems. Additionally, innovations in packaging—such as fiber-coupled and surface-mounted formats—are expanding installation flexibility. Overall, blue laser diode technology is progressing toward enhanced beam stability, reduced energy consumption, and improved cost-performance ratios, setting the stage for broader adoption across advanced industries.

In March 2024, Nichia Corporation unveiled a new 488 nm single-mode blue laser diode optimized for biomedical fluorescence applications and high-precision sensors, enhancing wavelength control and beam stability.

In January 2024, Kyocera SLD Laser launched a compact high-brightness blue laser module for LiDAR systems, improving range and resolution in autonomous vehicle navigation systems.

In September 2023, OSRAM Opto Semiconductors introduced an energy-efficient multi-emitter blue laser array targeting industrial cutting and additive manufacturing applications, emphasizing high power output in compact form factors.

In July 2023, Rohm Semiconductor developed a low-power 450 nm blue laser diode with enhanced thermal management features designed for wearable projection devices and next-generation AR headsets.

The Blue Laser Diodes Market Report offers a comprehensive analysis of the global market landscape, covering key segments by type, application, end-user, and geographic region. The report explores various diode configurations including single-mode and multi-mode types, as well as specialized formats such as wavelength-stabilized and fiber-coupled diodes. Application analysis spans across projection systems, optical storage, industrial manufacturing, biomedical diagnostics, LiDAR, and AR/VR devices.

From an end-user perspective, the study evaluates demand dynamics from industries such as consumer electronics, automotive, healthcare, defense, and research institutions. Regional assessments include North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level insights for key markets like the U.S., China, Germany, and Japan.

The report also delves into emerging technologies, innovation trends, and regulatory developments that are reshaping the adoption and production of blue laser diodes. It examines the competitive landscape with a focus on active players, product innovations, and supply chain dynamics. By providing in-depth qualitative and quantitative insights, the report equips industry stakeholders, policymakers, and investors with the data necessary to make informed strategic decisions in this evolving optoelectronics domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 275.7 Million |

| Market Revenue (2032) | USD 367.0 Million |

| CAGR (2025–2032) | 3.64 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Nichia Corporation, OSRAM Opto Semiconductors GmbH, Sony Corporation, Sharp Corporation, Egismos Technology Corporation, IPG Photonics Corporation, Ushio Inc., Rohm Semiconductor, Panasonic Corporation, Kyocera SLD Laser, Inc., Mitsubishi Electric Corporation, Hamamatsu Photonics K.K. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |