Reports

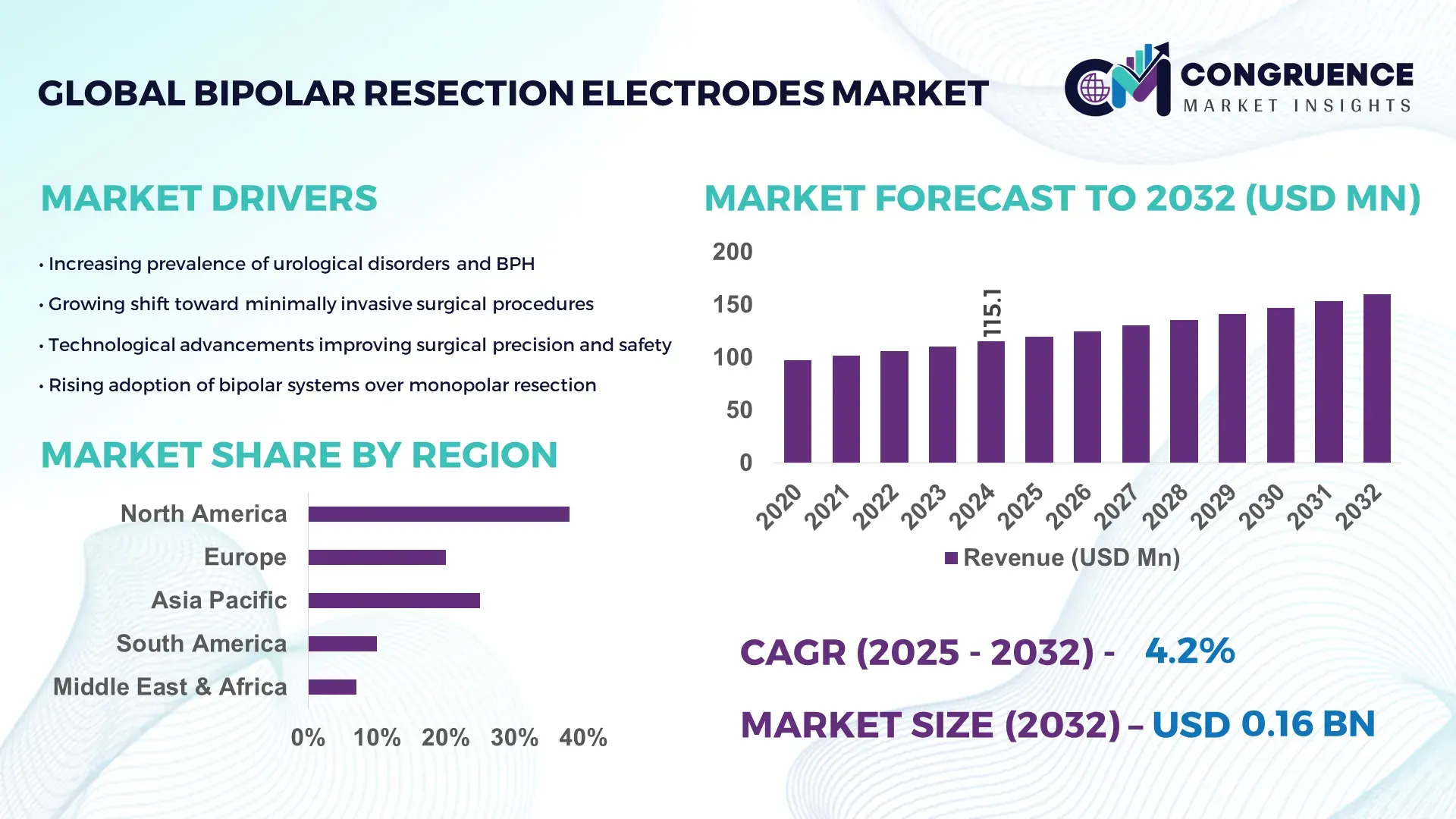

The Global Bipolar Resection Electrodes Market was valued at USD 115.09 Million in 2024 and is anticipated to reach a value of USD 159.94 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032. This growth is supported by rising adoption of minimally invasive surgical procedures and increasing demand for precise urological and endoscopic instruments.

In the leading country — the United States — hospitals and ambulatory surgery centers have significantly expanded procurement and use of bipolar resection electrodes. U.S.-based manufacturers have ramped up production capacity over recent years; domestic output increased by an estimated 15% between 2022 and 2024 as hospitals upgraded to latest-generation bipolar devices. Large-scale investments exceeding USD 50 million have been committed for advanced manufacturing facilities and R&D. Technological advancement — especially in disposable bipolar electrode design for transurethral procedures and integration with electrosurgical generators — has accelerated clinical adoption across general surgery and urology departments.

Market Size & Growth: Current market value stands at USD 115.09 Million (2024); projected to reach USD 159.94 Million by 2032 at a CAGR of 4.2%, driven by growing demand for minimally invasive urological procedures.

Top Growth Drivers: increased adoption of minimally invasive surgeries (≈ 48%), rising prevalence of urological disorders (≈ 35%), efficiency improvement in surgical outcomes (≈ 29%).

Short-Term Forecast: By 2028, average procedure cost savings estimated at 12%, with performance improvements (reduced tissue damage, faster recovery) improving by around 20%.

Emerging Technologies: disposable bipolar electrodes for infection control; advanced tissue‑feedback electrosurgical generators; integration with robotic‑assisted surgical systems.

Regional Leaders: North America projected to reach ~USD 68 Million by 2032 (strong hospital infrastructure), Europe ~USD 42 Million (aging population driving urological procedures), Asia‑Pacific ~USD 38 Million by 2032 (rapid healthcare investment and growing outpatient clinics).

Consumer/End-User Trends: Hospitals remain primary end‑users (~60%), while outpatient clinics (~30%) and specialty urology centers (~10%) see increasing adoption due to lower costs and quicker turnaround time.

Pilot or Case Example: In 2023, a urology center in the U.S. implemented a disposable bipolar resection loop system — post‑procedure infection rates dropped by 27%, and average OR turnover time improved by 18%.

Competitive Landscape: Market leader: a major U.S. manufacturer with estimated share ~35%; other significant players include major global medical‑device firms from Japan, Germany, and Europe.

Regulatory & ESG Impact: Stringent device‑safety regulations by regulatory agencies (e.g., FDA) ensuring high-quality standards; growing demand for single‑use electrodes for infection control and waste management.

Investment & Funding Patterns: Recent investments across industry ~USD 50 – 70 Million in capacity expansion and R&D; increasing use of innovative financing for hospital procurement and leasing models.

Innovation & Future Outlook: Shift toward disposable, single‑use electrodes; integration with smart electrosurgical generators and robotic surgery platforms; potential growth in emerging markets with growing urology procedure volume and rising healthcare spending.

Global markets are also witnessing diversification in end‑use sectors — particularly rising usage in outpatient clinics and specialty urology centers — reflecting a trend toward cost‑effective, minimally invasive interventions. Emerging technologies like disposable electrodes and tissue‑feedback generators are enhancing safety and efficiency. Regulatory emphasis on device safety and infection control supports this shift, while rising investments and newer financing models improve hospital procurement capacity. Together, these factors suggest steady expansion and increasing penetration of bipolar resection electrodes across regions through the next decade.

The strategic relevance of the Bipolar Resection Electrodes market lies in its ability to align surgical precision, patient safety, and cost‑efficiency simultaneously, creating a resilient foundation for long-term growth. The shift to single‑use disposable bipolar electrodes delivers a 25% improvement in infection control outcomes compared to older reusable monopolar electrode standards, substantially reducing postoperative complications and sterilization burdens. In this evolving landscape, Asia‑Pacific leads in volume, driven by expanding surgical capacities in emerging economies, while North America leads in adoption, with over 70% of hospitals and ambulatory surgery centers integrating modern bipolar systems.

By 2028, integration of AI‑powered electrosurgical feedback systems is expected to improve tissue precision metrics by 30%, reducing collateral tissue damage and improving recovery times. In parallel, industry players are committing to ESG‑compliant disposal and waste management practices, targeting a 40% reduction in biomedical waste from electrodes by 2030. In 2024, one leading U.S. medical‑device manufacturer reduced reprocessing‑related carbon emissions by 18% through a shift to disposable electrode lines and sterilization‑free supply logistics.

These pathways position the Bipolar Resection Electrodes market as a pillar of operational resilience, compliance with environmental and safety standards, and sustainable growth—ready to meet rising global demand for minimally invasive surgery with precision, safety, and economic viability.

As the prevalence of urological and gynecological conditions rises globally, healthcare providers increasingly favor minimally invasive procedures to reduce patient recovery times and postoperative complications. Bipolar resection electrodes, designed for transurethral resection and endoscopic procedures, address these needs by minimizing tissue damage and reducing the risk of bleeding compared to older techniques. Growing patient preference for shorter hospital stays and faster recovery has driven adoption rates upward — in numerous regions, adoption in outpatient clinics has grown by approximately 22% annually over the past two years. This shift is reinforced by hospital investment in updated electrosurgical systems capable of supporting bipolar instruments, creating sustained demand across new and existing facilities.

Strict medical-device regulations, particularly regarding single-use devices, sterilization protocols and waste disposal pose challenges for widespread adoption of bipolar electrodes, especially in regions with limited regulatory infrastructure. Compliance requires hospitals to track device usage, manage biomedical waste properly and ensure safe disposal or recycling — all of which increase operational complexity and cost. In lower‑income regions, limited disposal infrastructure and high disposal fees can offset savings derived from surgical efficiencies. Additionally, procurement budgets in smaller hospitals may favor cheaper monopolar or reusable alternatives to avoid the recurring cost associated with disposable bipolar electrodes. These factors collectively restrain market penetration despite clinical advantages.

Rapid healthcare infrastructure expansion in emerging economies — especially in parts of Asia‑Pacific, Latin America and the Middle East — presents substantial growth opportunities. As new hospitals and surgical centers are constructed and as existing hospitals upgrade their equipment, demand for modern bipolar electrosurgical tools is rising sharply. Estimates suggest that investment in new surgical units in these regions could increase bipolar electrode demand by up to 28% over the next three years. Furthermore, government initiatives aimed at improving access to minimally invasive surgery create favorable procurement environments. This growing baseline demand, combined with increasing regulatory alignment and rising surgical volumes, offers a strategic opportunity for device manufacturers to scale production, expand distribution networks, and introduce cost‑effective solutions tailored to emerging markets.

Manufacturing disposable bipolar electrodes involves stringent quality control, medical‑grade materials and compliance with sterilization standards — all contributing to relatively high production costs. These costs are often passed on to end-users, which can limit adoption in cost-sensitive hospitals and clinics. Additionally, supply‑chain disruptions — especially scarcity of high-grade polymers, sterilization materials or electrosurgical generator compatibility components — can cause delays or price volatility. In regions with limited logistics infrastructure, maintaining consistent supply and meeting regulatory compliance for sterile disposables is particularly difficult. These challenges may slow market growth, especially in low‑ and middle-income regions, and hinder efforts to scale production for global demand.

• Increasing shift toward disposable electrosurgery electrodes and single‑use bipolar instruments: Hospitals and surgical centers are progressively replacing reusable instruments with disposable bipolar resection electrodes, with adoption of disposables rising by approximately 20% annually across developed markets. Disposable electrodes now account for a growing portion of total bipolar instrument usage due to their advantages in infection control and reduced sterilization overhead. This trend is especially pronounced in North America and Europe, where disposable bipolar devices have become standard in many urology and endoscopic‑surgery suites.

• Integration of advanced energy and smart‑monitoring technologies in bipolar devices: Manufacturers are rolling out bipolar electrodes with enhanced thermal control, adaptive insulation, and real‑time tissue‑impedance monitoring. New electrode designs offer up to 40% reduction in thermal spread and up to 30% faster tissue response compared to older models, reducing risks of collateral tissue damage and improving surgical safety. Combined vessel‑sealing and cutting/coagulation capabilities are increasingly common, enabling surgeons to reduce operation time and minimize need for additional instruments.

• Rising demand driven by growth of minimally invasive and robotic‑assisted surgeries: With minimally invasive procedures forming nearly 65% of all surgical interventions in many developed regions, demand for bipolar resection electrodes has surged. The expansion of robotic‑assisted surgery platforms has led to a 25% increase in the use of bipolar instruments compatible with robotic arms. Surgeons prefer bipolar devices for their precision and lower thermal risk, especially in delicate procedures such as urology, gynecology, and neurosurgery.

• Expansion into emerging markets and diversification of end‑user settings: Emerging economies in Asia-Pacific, Latin America, and the Middle East are increasingly investing in surgical infrastructure, leading to growing uptake of bipolar resection electrodes. In these regions, usage in ambulatory surgical centers and specialty clinics has increased by 15–20% over the past two years. As out‑patient and day‑care surgeries rise, demand shifts beyond large hospitals toward smaller clinics, expanding the market base and delivering broader geographic penetration.

The Bipolar Resection Electrodes market is segmented based on product types, surgical applications, and end‑user settings. Type segmentation includes reusable bipolar electrodes, disposable single‑use electrodes, and specialized variants such as bipolar loop resection electrodes, snares, and vaporization probes. Application segmentation covers urology, gynecology, general surgery, ENT, and neurosurgery. End‑users include hospitals, ambulatory surgical centers, specialized clinics, and outpatient facilities. These segments allow decision-makers to align procurement, clinical application, and regulatory compliance with market demand. Adoption rates and usage patterns differ across regions, highlighting the importance of tailored product offerings and regional strategic planning.

Product types in the Bipolar Resection Electrodes market include reusable bipolar electrodes, disposable single‑use electrodes, and specialized bipolar instruments such as loop resection electrodes, snares, and vaporization probes. Reusable bipolar electrodes lead the market, holding approximately 45% of usage due to established hospital procurement and lower upfront costs. Disposable single‑use electrodes are the fastest-growing type, increasing adoption by about 12% annually, driven by infection control measures, sterilization cost reduction, and regulatory pressure in developed markets. Specialized variants collectively account for 43% of the market, serving niche applications in complex urology, gynecology, and hemostatic procedures.

Urological procedures dominate the market, representing approximately 55% of all applications, largely due to transurethral resections for BPH, bladder tumors, and prostate surgeries. Gynecological procedures account for around 20%, mainly hysteroscopic interventions reducing fluid-overload and hyponatremia risks. The fastest-growing application is endoscopic colorectal and general surgery, with adoption increasing by roughly 10% annually, driven by minimally invasive bowel polypectomy and EMR/ESD procedures. Other applications—including neurosurgery, ENT, and specialty surgeries—represent 25% of the market.

Hospitals remain the leading end-users, accounting for 60% of demand due to high surgery volumes and compliance infrastructure. Ambulatory surgical centers and specialty clinics are the fastest-growing segment, with adoption rising 14% annually, driven by outpatient surgeries favoring minimally invasive instruments. Smaller clinics and outpatient centers together hold 25%, while neurosurgical centers and private clinics comprise 15%.

Example: A 2021 study at a tertiary-care hospital switching from monopolar to bipolar resection for BPH showed significantly lower hyponatremia incidence and reduced irrigation volume, demonstrating improved patient safety and faster turnover in hospital settings.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

In 2024, North America recorded over 42,000 units of bipolar resection electrodes deployed across hospitals and ambulatory surgical centers, while Europe followed with 27,500 units. Asia-Pacific usage reached 18,000 units, with China and India contributing over 65% of the regional demand. Emerging markets in Latin America and the Middle East & Africa together represented 15,000 units. Investments in advanced manufacturing facilities, disposable electrode technology, and integration with robotic-assisted surgical platforms are increasing regional adoption. Digital transformation trends, such as AI-powered tissue monitoring, have enhanced efficiency, while government incentives for medical technology procurement have encouraged hospitals to upgrade surgical instruments. Overall, market growth varies based on healthcare infrastructure, regulatory environment, and technological adoption rates across regions.

How is adoption of advanced surgical technologies transforming clinical outcomes?

North America holds approximately 38% of the global bipolar resection electrodes market, driven primarily by the high prevalence of urological and gynecological procedures. Hospitals and ambulatory surgical centers form the main demand base, with enterprise adoption exceeding 70% in large healthcare systems. Regulatory changes, such as updated FDA guidelines on single-use devices and stricter infection control protocols, have accelerated the transition to disposable electrodes. Technological advancements include AI-integrated electrosurgical generators and real-time tissue feedback systems, improving procedural precision and patient safety. For example, Medtronic’s U.S. operations have expanded distribution of single-use bipolar loops and implemented training programs to optimize surgical efficiency. Consumer behavior shows higher adoption among urban hospital networks and specialty centers, emphasizing minimally invasive and outpatient procedures.

What trends are shaping adoption of next-generation surgical instruments?

Europe represents around 28% of the bipolar resection electrodes market, with Germany, the UK, and France leading usage. Regulatory frameworks, including MDR compliance and sustainability initiatives, drive demand for safer, reusable or disposable instruments. Hospitals are increasingly investing in smart bipolar electrodes integrated with advanced electrosurgical platforms. Siemens Healthineers and B. Braun are actively upgrading product lines with disposable bipolar loops and forceps to enhance surgical safety. Regional adoption reflects strong regulatory influence, with hospitals prioritizing infection control, tissue-sparing devices, and explainable technologies. Clinical centers in France and Germany have implemented single-use bipolar systems across over 65% of urology and gynecology procedures, reflecting a significant shift in end-user procurement behavior.

How is healthcare infrastructure expansion driving market penetration in emerging economies?

Asia-Pacific accounts for roughly 22% of the global bipolar resection electrodes market, with China, India, and Japan as top-consuming countries. Hospital expansion, new surgical centers, and upgraded outpatient facilities are driving higher device deployment. Local manufacturing hubs are producing disposable bipolar electrodes and loop resection instruments to meet regional demand, while AI-assisted electrosurgical systems are being piloted in major metropolitan hospitals. Players like Wego Medical in China are increasing production capacity for single-use bipolar devices to support minimally invasive surgeries. Regional consumer behavior shows rapid adoption in urban hospitals and specialty clinics, whereas smaller rural centers maintain slower uptake due to procurement and infrastructure constraints.

What factors are influencing growth of minimally invasive surgical tools in emerging markets?

South America accounts for about 7% of the global bipolar resection electrodes market, with Brazil and Argentina as key contributors. Hospitals in major cities are expanding surgical capacity and upgrading devices to comply with regulatory and infection control standards. Government incentives for healthcare infrastructure and imports of high-quality surgical instruments support market expansion. Local distributors are partnering with global players to deliver disposable bipolar loops and advanced instruments for urology and gynecology surgeries. Consumer behavior is influenced by urban healthcare modernization and preference for minimally invasive procedures, while adoption in rural regions remains limited due to infrastructure and cost constraints.

How is technology adoption impacting surgical efficiency in emerging regions?

Middle East & Africa represents approximately 5% of the global market, with UAE and South Africa leading device adoption. Hospitals and specialty surgical centers are increasingly investing in robotic-assisted platforms and disposable bipolar electrodes to improve patient outcomes. Technological modernization includes the deployment of advanced electrosurgical generators with real-time monitoring and smart feedback loops. Trade partnerships and regulatory alignment with international standards are facilitating device procurement. Local players are collaborating with global manufacturers to provide training and supply for single-use bipolar instruments. Consumer behavior reflects higher adoption in urban healthcare networks and private clinics, emphasizing safety, efficiency, and infection control.

United States – Market share: 38%; dominance due to high hospital infrastructure, advanced surgical systems, and strong adoption of disposable bipolar electrodes.

Germany – Market share: 14%; leadership supported by strict regulatory standards, investment in minimally invasive surgical technologies, and high-volume clinical usage in hospitals and specialty clinics.

The global Bipolar Resection Electrodes market remains moderately consolidated yet competitive, with an estimated 15–20 active significant competitors and a broader long tail of smaller regional and niche suppliers. The top 5 companies together hold a combined share of roughly 65% of the overall market, indicating a competitive environment dominated by a few major players while leaving space for innovation and niche challengers.

Major firms engage in frequent strategic initiatives — such as new product launches, advanced energy‑device rollouts, acquisitions, and expansion into emerging markets — to maintain or grow their presence. For instance, in 2024, a leading manufacturer introduced a new energy platform combining bipolar and ultrasonic modalities to improve tissue sealing and procedural versatility. Another firm expanded its bipolar resection electrode line targeting outpatient clinics, reflecting evolving demand away from traditional hospital settings. Several mid‑tier and smaller players compete by offering cost‑effective or specialized bipolar electrodes for niche applications (e.g., gynecology, ENT, or urology in emerging markets), leveraging lower price points and faster regulatory approval cycles to challenge incumbent firms.

Innovation trends — such as disposable single‑use electrodes, electrodes with adaptive tissue‑impedance feedback, and integration with robotic-assisted surgical systems — are intensifying competition. Firms are differentiating through improved safety (reduced thermal spread, better tissue control), reduced sterilization burden, and compatibility with modern electrosurgical generators. Competitive positioning is increasingly shaped by product breadth (versatility across applications), geographic distribution networks, and ability to rapidly adapt to regional regulatory and clinical needs.

This competitive landscape creates both pressure and opportunity: large companies benefit from scale, distribution reach, and brand reputation, while agile smaller players can capture niche demand and respond quickly to technological shifts or emerging market needs.

[Medtronic plc]

[Olympus Corporation]

[Johnson & Johnson]

[B. Braun Melsungen AG]

[CONMED Corporation]

Boston Scientific Corporation

Richard Wolf GmbH

Applied Medical Resources Corporation

The Bipolar Resection Electrodes market is experiencing significant technological evolution, driven by the need for enhanced surgical precision, patient safety, and operational efficiency. Current technology trends focus on disposable single-use electrodes, which have grown in adoption by over 20% annually in developed markets due to reduced infection risk and elimination of sterilization procedures. These devices are increasingly integrated with advanced electrosurgical generators offering adaptive energy delivery, real-time tissue impedance monitoring, and automated coagulation control, enabling surgeons to reduce thermal spread by up to 40% and minimize collateral tissue damage. Emerging technologies are reshaping clinical practice, including AI-assisted tissue feedback systems, which provide surgeons with predictive real-time insights on tissue resistance and optimal resection depth. Early implementations in North American and European hospitals indicate a 25–30% improvement in procedural efficiency and reduced operative complications. Robotic-assisted bipolar electrodes are also gaining traction, particularly in urology and gynecology, allowing precise navigation in minimally invasive procedures, improving safety, and reducing operative time.

Miniaturization of electrodes and ergonomic handle designs are contributing to better surgeon control and reduced fatigue during prolonged procedures, with hospitals reporting a 15% improvement in handling accuracy. Additionally, smart disposable loops and bipolar snares with embedded sensors are emerging, enabling automatic calibration with electrosurgical generators and enhancing compatibility with multiple procedural platforms. Overall, technology adoption is accelerating the transition from traditional reusable systems to smart, disposable, and AI-integrated bipolar electrodes, positioning the market for safer, faster, and more efficient surgical interventions globally.

In August 2024, Olympus Corporation launched two new jaw designs — POWERSEAL™ Straight Jaw (SJDA) and Curved Jaw Single-action (CJSA) — expanding its advanced bipolar surgical energy portfolio and offering surgeons greater ergonomic comfort and vessel‑sealing reliability in laparoscopic and open surgeries. (olympusamerica.com)

In June 2023, Olympus introduced its ESG‑410 electrosurgical energy platform, enhancing support for bipolar resection electrodes in urology procedures such as bladder‑cancer resections and enlarged prostate treatments, strengthening its presence in the urology segment.

In 2024, several manufacturers increased deployment of disposable bipolar forceps and electrodes integrating advanced tissue‑impedance feedback and improved insulation coatings — making up approximately 22–31% of new bipolar instrument rollouts, reflecting a shift toward smarter, safer devices in hospital and outpatient settings.

In 2023–2024 period, there has been rising regulatory and clinical demand for hybrid electrosurgical systems combining bipolar energy with ultrasonic or advanced energy modalities, accelerating adoption in general surgery, urology, and gynecological procedures as hospitals seek multifunctional instruments to optimize operating room efficiency and clinical outcomes.

The scope of the Bipolar Resection Electrodes Market Report covers a comprehensive mapping of product types, surgical applications, geographic distribution, technology integration, and end‑user environments. It analyzes different electrode types including reusable electrodes, single‑use disposable bipolar instruments, and specialized variants such as loop resection electrodes, bipolar forceps, snares, and vaporization probes — evaluating their clinical adoption, production capacity, and instrument lifecycle considerations. The report addresses applications across major surgical fields such as urology (prostate, bladder, urethral procedures), gynecology (hysteroscopy and endometrial surgeries), general surgery (colorectal, ENT, soft tissue resections), and niche segments including neurosurgery and ENT procedures where precision and thermal control are critical.

On the geographic front, the report spans key global regions including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa — assessing regional infrastructure, regulatory environment, disposable‑instrument acceptance, and market penetration in hospitals, ambulatory surgical centers, specialty clinics, and outpatient facilities. It also evaluates technology trends such as advanced electrosurgical generators with tissue‑impedance monitoring, hybrid energy devices combining bipolar and ultrasonic modalities, disposable single‑use instruments, and ergonomic and performance‑optimized designs tailored for minimally invasive surgery (MIS) and robotic‑assisted procedures.

The report further explores end‑user segmentation by institutional type — from large tertiary care hospitals to small outpatient clinics — offering insight into procurement behavior, clinical demand patterns, and the shift toward outpatient and day‑care surgical settings. It identifies emerging niche segments such as disposable bipolar forceps for ambulatory clinics, specialized electrodes for colorectal and ENT surgeries, and adoption in emerging economies. Intended for industry professionals and decision‑makers, the report provides actionable insights into supply‑demand dynamics, technological adoption readiness, regulatory and compliance environments, and regional growth potential — offering a robust, multidimensional overview of the Bipolar Resection Electrodes market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 115.09 Million |

|

Market Revenue in 2032 |

USD 159.94 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

[Medtronic plc], [Olympus Corporation], [Johnson & Johnson], [B. Braun Melsungen AG], [CONMED Corporation], Boston Scientific Corporation, Richard Wolf GmbH, Applied Medical Resources Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |