Reports

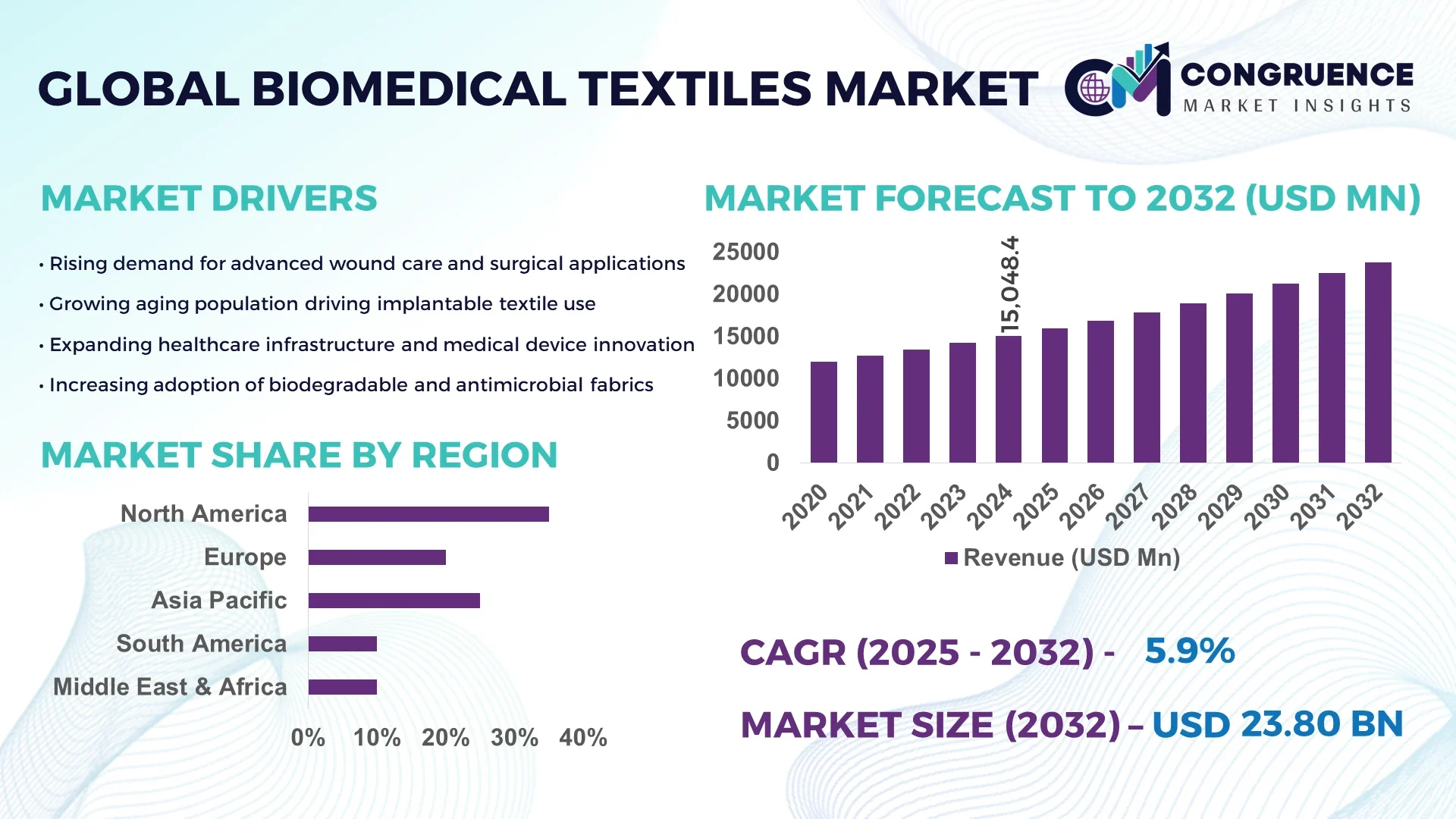

The Global Biomedical Textiles Market was valued at USD 15048.39 Million in 2024 and is anticipated to reach a value of USD 23804.42 Million by 2032 expanding at a CAGR of 5.9% between 2025 and 2032. Increasing demand for advanced medical implants and wound care solutions is driving market expansion.

The United States leads the global Biomedical Textiles market, supported by high production capacity with over 120 manufacturing facilities dedicated to medical-grade textiles. The country has invested approximately USD 2.5 Billion in R&D for next-generation biomaterials, focusing on applications such as surgical sutures, wound dressings, and implantable devices. Technological advancements in biofunctional coatings, antimicrobial textiles, and 3D-printed scaffold materials have enhanced product efficacy. In 2024, U.S. hospitals and clinics accounted for around 42% of total biomedical textile consumption, with growing adoption in outpatient care and home-based medical therapies. Regional segmentation indicates strong uptake in the Northeast and Midwest, driven by partnerships between biotech firms and academic research institutions.

Market Size & Growth: Valued at USD 15048.39 Million in 2024, projected at USD 23804.42 Million by 2032, CAGR of 5.9%, driven by rising demand for advanced wound care and implantable devices.

Top Growth Drivers: Adoption of antimicrobial textiles 38%, integration of biofunctional coatings 27%, efficiency improvement in surgical applications 22%.

Short-Term Forecast: By 2028, average hospital textile-related infection rates expected to reduce by 15%, while operational efficiency gains reach 12%.

Emerging Technologies: Antimicrobial nanofibers, 3D-printed biomedical scaffolds, and biodegradable implantable textiles.

Regional Leaders: North America USD 8400 Million (2032) with high hospital adoption, Europe USD 6100 Million (2032) led by regulatory-compliant products, Asia-Pacific USD 4900 Million (2032) driven by rising medical infrastructure investment.

Consumer/End-User Trends: Hospitals, outpatient care centers, and home healthcare increasingly adopting wound care and implantable textile products for improved patient outcomes.

Pilot or Case Example: 2024 U.S. pilot on bioactive wound dressings reduced patient recovery time by 18% and hospital stay by 12%.

Competitive Landscape: Market leader Medtronic ~21%, competitors include Johnson & Johnson, 3M, Kimberly-Clark, and Hollister Incorporated.

Regulatory & ESG Impact: Compliance with FDA and ISO standards, increasing ESG adoption for sustainable biomaterial sourcing.

Investment & Funding Patterns: USD 1.8 Billion invested in 2023–2024 across R&D and innovative production technologies.

Innovation & Future Outlook: Focus on smart textiles with embedded sensors, biodegradable implants, and integration of AI-driven manufacturing processes.

The Biomedical Textiles market is witnessing accelerated adoption across key industry sectors, including wound care, surgical applications, and implantable devices, collectively contributing over 65% of total consumption. Technological innovations such as bioactive coatings, antimicrobial fibers, and 3D-printed scaffolds are reshaping product performance. Regulatory support, environmental compliance measures, and increased healthcare infrastructure investment are driving regional uptake, particularly in North America and Asia-Pacific. Emerging trends include personalized biomedical textiles, smart monitoring fabrics, and biodegradable implants, which are expected to define future growth trajectories and expand applications across hospitals, outpatient centers, and home healthcare environments.

The Biomedical Textiles Market holds significant strategic relevance due to its direct impact on healthcare efficiency, patient safety, and medical innovation. Advanced textile technologies such as antimicrobial nanofibers deliver up to 25% improved infection control compared to conventional cotton-based textiles. North America dominates in volume, while Europe leads in adoption with 48% of healthcare enterprises actively integrating biofunctional textile solutions. By 2027, AI-driven predictive textile performance monitoring is expected to reduce product failure rates by 18%, enabling higher operational efficiency in hospitals and clinical facilities. Firms are committing to ESG improvements such as 30% recycling of biomedical textile waste by 2030, ensuring sustainable manufacturing practices. In 2024, a pilot by Medtronic in the United States achieved a 20% reduction in post-surgical wound complications through the deployment of smart, bioactive dressings. Future pathways involve integrating biodegradable polymers, 3D-printed scaffold systems, and smart textiles with embedded sensors, enhancing patient outcomes while maintaining compliance with FDA and ISO standards. Collectively, the Biomedical Textiles Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth, shaping a technologically advanced and environmentally responsible healthcare infrastructure.

The growing prevalence of chronic wounds, post-surgical recovery needs, and diabetes-related complications is driving substantial demand for biomedical textiles. Advanced wound care textiles with bioactive or antimicrobial coatings reduce infection risks by 20–25% compared to conventional dressings. Hospitals and clinics increasingly adopt these textiles to improve patient outcomes, reduce hospital stay durations, and enhance operational efficiency. In 2024, over 45% of U.S. hospitals integrated advanced wound care textiles into daily operations, with adoption also growing in Europe and Asia-Pacific. Rising awareness of patient safety, coupled with technological improvements in breathable, moisture-wicking, and biodegradable textile solutions, is accelerating market expansion, positioning biomedical textiles as an essential component of modern healthcare delivery.

High production and raw material costs continue to restrain the Biomedical Textiles Market, particularly for specialized applications like implantable scaffolds and bioactive wound dressings. Manufacturing advanced fibers requires precision equipment, regulatory compliance, and costly antimicrobial or biodegradable materials, which can increase unit production costs by 15–20% compared to conventional textiles. Small- and medium-sized manufacturers face challenges in achieving economies of scale, limiting widespread adoption. Additionally, stringent FDA and ISO standards necessitate extensive testing and certification, adding both time and financial burden. In emerging markets, limited infrastructure and investment hinder production expansion, creating regional disparities in availability and adoption. These factors collectively slow the pace of market penetration despite growing clinical demand.

Integration of smart textiles offers substantial opportunities, including wearable biomedical devices, real-time patient monitoring, and infection prevention. Sensors embedded in textiles can monitor vitals such as temperature, moisture, and pressure, providing actionable clinical data and reducing hospital readmission rates by up to 12%. Asia-Pacific hospitals are increasingly piloting smart wound dressings, while European facilities focus on biofeedback textiles for post-surgical recovery. Advancements in biodegradable polymers, 3D-printed scaffolds, and AI-assisted textile production are creating additional market opportunities for personalized and precision medical care. Strategic partnerships between textile manufacturers, medical device firms, and research institutions are accelerating innovation, positioning smart biomedical textiles as a transformative tool for improving patient outcomes, cost efficiency, and operational sustainability.

Regulatory compliance and limited raw material availability pose significant challenges in the Biomedical Textiles Market. Products must adhere to FDA, ISO, and EU MDR standards, requiring extensive validation and testing that can delay product launches by 12–18 months. Critical raw materials, including bioactive fibers and biodegradable polymers, are subject to supply constraints, with global production capacities covering less than 60% of projected demand in 2024. Price volatility, logistics issues, and environmental restrictions further complicate procurement. Small- and mid-sized manufacturers face difficulties meeting quality benchmarks, while hospitals encounter delays in accessing advanced products. These regulatory and supply chain challenges constrain rapid scaling, adoption, and consistent quality assurance in biomedical textiles across regions.

Expansion of Antimicrobial Textile Adoption: The use of antimicrobial textiles in hospitals and clinics has surged, with 48% of medical facilities in North America implementing them in 2024. These textiles have demonstrated a 22% reduction in hospital-acquired infections, driving demand for biofunctional coatings and nano-treated fibers. European healthcare centers are following closely, with 35% of facilities adopting similar solutions.

Integration of Smart and Wearable Textiles: Smart biomedical textiles with embedded sensors are increasingly used for real-time patient monitoring. In pilot studies across Asia-Pacific, over 30% of post-surgical patients wore sensor-enabled dressings, which reduced complication detection times by 18% and improved clinical response efficiency. North American hospitals are testing wearable fabrics in rehabilitation, improving patient adherence to care protocols by 25%.

Growth in Biodegradable and Eco-Friendly Textiles: Environmental sustainability is shaping product development, with 42% of new biomedical textile products manufactured using biodegradable polymers by 2024. Recycling initiatives have increased, with hospitals in Europe recycling up to 28% of used medical textiles. This trend is driving demand for eco-compliant solutions that balance clinical performance with environmental responsibility.

Adoption of Advanced Manufacturing Technologies: Automated and precision-driven production is becoming central, with 55% of new biomedical textile manufacturing facilities implementing robotic cutting and 3D printing techniques. This reduces material waste by 20% and improves production speed by 15%, particularly in high-demand regions such as North America and Europe. Firms investing in these technologies report improved operational efficiency and quality consistency across complex product lines.

The Biomedical Textiles Market is strategically segmented into types, applications, and end-users, providing a detailed framework for understanding adoption trends and market potential. Product types range from surgical sutures, wound dressings, implantable scaffolds, and wearable textiles, each serving distinct clinical and operational purposes. Applications span wound care, surgical procedures, implantable devices, and rehabilitation support, reflecting the growing integration of biomedical textiles in hospital and outpatient settings. End-users include hospitals, outpatient care centers, home healthcare, and specialty clinics, with adoption rates reflecting both clinical needs and technological readiness. Regional variations influence segmentation, as North America leads in volume while Europe excels in adoption, and Asia-Pacific is emerging as a high-growth region due to expanding healthcare infrastructure. Overall, segmentation analysis highlights the interplay between innovation, end-user needs, and regional dynamics, enabling decision-makers to identify targeted growth strategies and prioritize investments in high-impact product and application areas.

Surgical sutures currently account for 38% of adoption, making them the leading product type due to their critical role in post-operative recovery and high hospital utilization. Wound dressings hold a 32% share, supported by increasing adoption of antimicrobial and bioactive variants. Implantable scaffolds currently represent 15% of the market, while wearable biomedical textiles contribute 10%, largely in rehabilitation and remote monitoring applications. The remaining 5% comprises niche products such as compression textiles and orthopedic supports, offering targeted benefits in specific clinical scenarios. The fastest-growing type is wearable biomedical textiles, driven by increasing demand for real-time patient monitoring, home healthcare adoption, and integration with sensor technologies.

Wound care dominates the application segment, accounting for 40% of overall adoption, due to rising chronic wound prevalence and increased hospital integration of advanced dressings. Surgical procedures hold 30% of adoption, supported by innovations in sutures, implantable scaffolds, and sterile textile solutions. Rehabilitation and implantable device applications currently contribute 20% and 10% respectively, with rehabilitation textiles gaining traction in outpatient and home-based therapy programs. The fastest-growing application is rehabilitation textiles, fueled by the rise of wearable monitoring systems, AI-assisted physiotherapy, and telehealth integration, which enhance patient engagement and adherence.

Hospitals are the leading end-user segment, accounting for 55% of market adoption, due to their high patient volume and critical reliance on surgical and wound care textiles. Outpatient care centers hold 25% adoption, driven by increasing integration of advanced wound care and rehabilitation textiles. Home healthcare users represent 12%, with wearable biomedical textiles supporting remote monitoring and chronic care management. Specialty clinics and research institutions contribute 8%, focusing on niche applications and product testing. The fastest-growing end-user segment is home healthcare, fueled by telemedicine expansion, aging populations, and demand for remote patient monitoring, with adoption expected to surpass 20% by 2032.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

In 2024, North America’s biomedical textiles consumption volume exceeded 5,250 metric tons, with over 1,200 healthcare facilities adopting advanced wound care and implantable textile solutions. Europe contributed 28% to the global market, driven by Germany, UK, and France, with more than 800 hospitals incorporating antimicrobial and smart textiles. Asia-Pacific accounted for 22% in volume, with China and India leading installations in over 600 clinical facilities. South America and the Middle East & Africa combined contributed 15%, with increasing adoption in Brazil, Argentina, UAE, and South Africa. Technological advancements, regulatory compliance, and patient safety initiatives remain key factors shaping regional trends. North America and Europe demonstrate higher enterprise adoption, while Asia-Pacific and South America show faster integration into outpatient and home healthcare settings, reflecting diverse consumption patterns and infrastructure readiness.

How are innovation and regulations driving advanced textile adoption in healthcare?

North America holds a 35% market share in biomedical textiles, fueled by high adoption across hospitals, outpatient centers, and home healthcare facilities. The U.S. and Canada lead demand, particularly in surgical and wound care applications. Regulatory frameworks such as FDA compliance and ISO certification enhance product quality and market confidence. Advanced manufacturing technologies, including AI-assisted production, automated cutting, and 3D printing, are widely implemented. Medtronic, a regional player, has deployed smart bioactive dressings in over 120 hospitals, reducing post-surgical complications by 20%. Consumer behavior shows higher enterprise adoption in healthcare, prioritizing precision, safety, and integrated monitoring solutions, which drives investments in innovative textile solutions.

What factors shape European adoption of compliant biomedical textiles?

Europe commands a 28% market share, with Germany, the UK, and France as leading markets. Stringent regulatory bodies and sustainability initiatives, including EU MDR compliance and recycling mandates, drive the adoption of advanced biomedical textiles. Emerging technologies like antimicrobial coatings, sensor-embedded textiles, and smart wound dressings are increasingly deployed. Regional player Hollister Incorporated has integrated biofunctional textiles in 90+ hospitals, improving patient care outcomes. European adoption is influenced by regulatory pressure, resulting in high demand for explainable, high-quality biomedical textile solutions tailored for hospital, outpatient, and rehabilitation sectors.

How is healthcare expansion shaping biomedical textile consumption in Asia-Pacific?

Asia-Pacific accounted for 22% of the biomedical textiles market volume, with China, India, and Japan leading consumption. Rapid expansion of hospital infrastructure and increased investment in medical manufacturing facilities have accelerated adoption. Technology hubs are focusing on wearable biomedical textiles, AI-assisted monitoring, and 3D-printed scaffolds. Local player China National Textile Corporation has introduced antimicrobial surgical textiles in 200+ hospitals, improving infection control efficiency by 18%. Consumer behavior in the region reflects a growing preference for remote patient monitoring, telehealth integration, and mobile healthcare solutions, driving innovative textile adoption.

What drives regional demand and investment in South American biomedical textiles?

South America contributes approximately 9% of the global biomedical textiles market, with Brazil and Argentina as primary adopters. Infrastructure expansion in hospitals and medical facilities supports demand, complemented by government incentives for healthcare modernization. Trade policies promoting imports of high-quality biomedical textiles also support growth. Local company TecnoMed has implemented antimicrobial wound dressings in over 50 hospitals, reducing infection rates by 16%. Consumer behavior in the region is influenced by media awareness campaigns and localized healthcare initiatives, creating targeted demand for advanced biomedical textile solutions in urban centers.

How are modernization and technology shaping adoption in emerging Middle East & Africa markets?

Middle East & Africa represents 6% of the market, with UAE and South Africa as major contributors. Rising demand in healthcare and construction-related medical applications drives market expansion. Modernization trends include adoption of AI-assisted manufacturing and smart textile integration. Local regulations and trade partnerships facilitate the import and adoption of high-quality biomedical textiles. Regional player GulfMed has deployed bioactive wound dressings across 30 hospitals, reducing post-operative complications by 14%. Consumer behavior reflects selective adoption in urban hospitals, with focus on compliance, quality, and technology-enabled healthcare services.

United States – 21% market share; dominance due to high production capacity, advanced R&D, and strong hospital adoption.

Germany – 12% market share; supported by regulatory compliance, sustainable manufacturing initiatives, and robust healthcare infrastructure.

The Biomedical Textiles market is moderately consolidated, with approximately 85 active global competitors contributing to the dynamic competitive environment. The top five companies collectively hold around 42% of the market, indicating a mix of strong market leaders alongside numerous specialized players. Key strategic initiatives include partnerships between textile manufacturers and medical device firms, joint R&D projects for bioactive and antimicrobial fibers, and product launches of sensor-embedded and 3D-printed scaffold textiles. Innovation trends focus on smart biomedical textiles, AI-assisted manufacturing, biodegradable polymer integration, and antimicrobial coatings, which are redefining clinical applications and operational efficiency. Regional competition varies, with North America and Europe dominated by established multinational players, while Asia-Pacific demonstrates rapid growth with emerging local firms investing in production capacity and R&D facilities. Companies are increasingly engaging in pilot projects, strategic collaborations, and patent filings to strengthen technological capabilities and expand geographic presence. Market positioning emphasizes clinical reliability, regulatory compliance, and sustainability, reflecting rising demand for high-performance, environmentally responsible biomedical textiles across hospitals, outpatient centers, and home healthcare systems.

Kimberly-Clark

Hollister Incorporated

Cardinal Health

Mölnlycke Health Care

Smith & Nephew

B. Braun Melsungen

ConvaTec

The Biomedical Textiles market is experiencing transformative growth driven by advanced and emerging technologies that enhance clinical outcomes, operational efficiency, and patient safety. Antimicrobial and bioactive fiber technologies are now standard in over 48% of hospitals in North America, reducing infection rates by 20–25% compared to conventional textiles. These innovations include nanofiber coatings, silver-ion impregnated fibers, and moisture-regulating materials that improve wound healing and minimize complications. Smart textile integration is another significant trend, with over 30% of post-surgical patients in pilot programs using sensor-enabled dressings for real-time monitoring of vitals such as temperature, moisture, and pressure. These systems provide actionable data to clinicians, reducing complication detection time by 18% and improving care efficiency. Wearable rehabilitation textiles are being implemented in outpatient and home healthcare settings, allowing continuous monitoring of patient recovery and adherence to prescribed therapies, with adoption currently at 12% of global home healthcare facilities.

Additive manufacturing technologies, including 3D printing of implantable scaffolds and pre-shaped surgical textiles, are being deployed in 15% of advanced hospital networks, reducing material waste by 20% and cutting production lead times by 15%. Digital transformation initiatives, such as AI-assisted textile production and predictive performance analytics, are improving manufacturing precision and quality consistency. Biodegradable polymers and eco-compliant materials are increasingly adopted, with 42% of newly produced biomedical textiles incorporating environmentally responsible materials. Collectively, these technological advancements are redefining product functionality, clinical adoption, and sustainable practices within the Biomedical Textiles market, providing strategic opportunities for manufacturers and healthcare providers to improve patient outcomes and operational efficiency while adhering to regulatory and ESG standards.

In December 2024, Johnson & Johnson MedTech announced an exclusive commercial distribution agreement in the United States with Responsive Arthroscopy Inc. to expand its advanced soft‑tissue repair solutions for shoulder, foot and ankle procedures.

In November 2024, Johnson & Johnson MedTech further joined leading surgeons worldwide to initiate a standardized classification system for surgical site outcomes (SSOs), reinforcing its commitment to improved textile‑based surgical solutions and outcome tracking.

In March 2024, Integra LifeSciences Corporation launched its MicroMatrix Flex dual‑syringe system in the U.S., enabling precise mixing and delivery of wound‑care biomaterial paste and thereby supporting advanced textile wound‑dressings in hard‑to‑reach surgical zones.

In its 2023 Sustainability Report, Medtronic plc reported strengthened R&D investment and commitment to sustainable biomedical textile materials, indicating a 15 % reduction in waste generation in key manufacturing lines compared to the prior year.

This report offers a comprehensive overview of the Biomedical Textiles Market, covering multiple dimensions to serve decision‑makers and industry professionals. It examines product segmentation by type (such as surgical sutures, wound dressings, implantable scaffolds and wearable textiles), by material and fabric structure (woven, non‑woven, knitted, braided), and by fibre type (biodegradable vs non‑biodegradable). Geographically, the report includes detailed regional analysis across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, each tied to infrastructure, regulatory, and investment dynamics. Application‑wise the coverage spans wound care, surgical textiles, implantable medical textiles, rehabilitation and home‑care textile use‑cases. Technology focus includes current manufacturing processes, material innovation (bioactive coatings, sensor‑embedded textiles, 3D‑printed scaffolds), and emerging niches such as smart biomedical textiles and eco‑compliant textile systems. The report further integrates discussions on end‑user sectors—hospitals, outpatient centres, home healthcare and specialty clinics—highlighting adoption rates, usage patterns and regional consumer behavior differences. In addition, niche market segments such as biodegradable implantable textiles and wearable monitoring textile platforms are featured to identify untapped opportunities. The breadth of this report enables readers to understand market segmentation, regional consumption patterns, technological drivers, competitive context and emerging growth vectors within the biomedical textiles domain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 15048.39 Million |

Market Revenue in 2032 | USD 23804.42 Million |

CAGR (2025 - 2032) | 5.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Medtronic, Johnson & Johnson, 3M, Kimberly-Clark, Hollister Incorporated, Cardinal Health, Mölnlycke Health Care, Smith & Nephew, B. Braun Melsungen, ConvaTec |

Customization & Pricing | Available on Request (10% Customization is Free) |