Reports

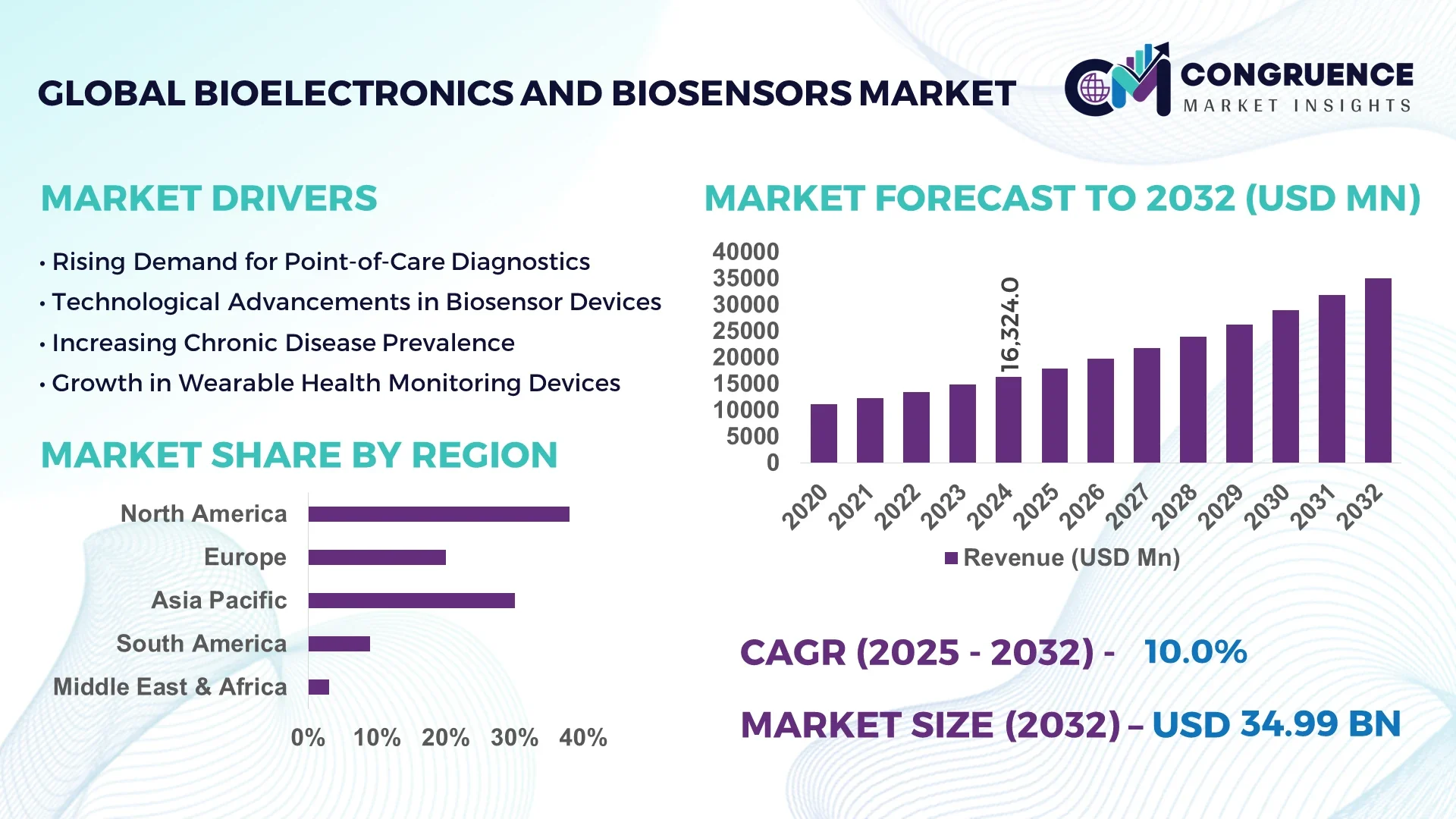

The Global Bioelectronics and Biosensors Market was valued at USD 16,324 million in 2024 and is anticipated to reach a value of USD 34,991.94 million by 2032, expanding at a CAGR of 10.0% between 2025 and 2032. This growth is primarily driven by the increasing demand for real-time health monitoring solutions and advancements in wearable biosensor technologies.

The United States leads the global bioelectronics and biosensors market, with substantial investments in research and development. In 2024, the U.S. biosensors market was estimated at USD 11.25 billion, projected to surpass USD 18.73 billion by 2030, growing at a CAGR of 7.4% from 2024 to 2033. Key industry applications include healthcare diagnostics, environmental monitoring, and food safety, with a significant focus on electrochemical biosensors and wearable devices. Technological advancements, such as the integration of artificial intelligence in biosensor devices, are enhancing diagnostic accuracy and patient outcomes.

Market Size & Growth: Valued at USD 16,324 million in 2024, projected to reach USD 34,991.94 million by 2032, expanding at a CAGR of 10.0%. Growth is fueled by the rising adoption of wearable health monitoring devices.

Top Growth Drivers: 1) Increasing demand for personalized healthcare solutions (45%), 2) Advancements in biosensor technology (35%), 3) Rising prevalence of chronic diseases (20%).

Short-Term Forecast: By 2028, a 15% improvement in diagnostic accuracy is expected due to the integration of AI and machine learning in biosensor devices.

Emerging Technologies: Development of non-invasive glucose monitoring systems and biosensors integrated with 5G technology for real-time data transmission.

Regional Leaders: 1) North America – projected market value of USD 18.73 billion by 2030, 2) Europe – expected to reach USD 15 billion by 2030, 3) Asia Pacific – anticipated market value of USD 12 billion by 2030.

Consumer/End-User Trends: Increased adoption of wearable biosensors among diabetic patients for continuous glucose monitoring and by athletes for performance tracking.

Pilot or Case Example: In 2023, a pilot project in the U.S. demonstrated a 20% reduction in hospital readmission rates through the use of wearable biosensors for chronic disease management.

Competitive Landscape: Market leader Medtronic holds approximately 25% market share, followed by Abbott Laboratories, F. Hoffmann-La Roche Ltd, Siemens Healthineers, and LifeSensors.

Regulatory & ESG Impact: Stringent FDA regulations ensure the safety and efficacy of biosensor devices, while environmental sustainability initiatives promote the development of eco-friendly biosensor materials.

Investment & Funding Patterns: Recent investments totaling over USD 500 million have been directed towards the development of next-generation biosensor technologies, with a focus on miniaturization and enhanced sensitivity.

Innovation & Future Outlook: Ongoing research into biosensors capable of detecting multiple biomarkers simultaneously is expected to revolutionize early disease detection and personalized treatment plans.

The bioelectronics and biosensors market is experiencing significant growth, driven by advancements in sensor technology and increasing demand for personalized healthcare solutions. Key industry sectors contributing to market expansion include healthcare diagnostics, environmental monitoring, and food safety. Technological innovations, such as the development of non-invasive glucose monitoring systems and AI-integrated biosensors, are enhancing the capabilities of biosensor devices. Regulatory frameworks, including FDA approvals and environmental sustainability initiatives, are shaping the development and adoption of biosensor technologies. Regional consumption patterns indicate a surge in demand across North America, Europe, and Asia Pacific, with a notable increase in wearable biosensor adoption among consumers. Looking ahead, the market is poised for continued growth, with emerging trends pointing towards the integration of biosensors in various aspects of daily life, from healthcare to environmental monitoring.

The Bioelectronics and Biosensors Market is strategically significant as it integrates biological systems with electronic devices, enabling real-time monitoring and diagnostics. This integration enhances patient outcomes, reduces healthcare costs, and supports personalized medicine initiatives. For instance, advanced biosensors offer a 20% improvement in diagnostic accuracy compared to traditional methods, facilitating earlier disease detection and intervention.

Regionally, North America leads in volume, with over 190 million deployed biosensor units in the U.S. alone. Meanwhile, Europe excels in adoption, with approximately 57% of hospitals utilizing biosensor-integrated diagnostic equipment. By 2026, the implementation of AI-driven biosensors is expected to improve diagnostic efficiency by 25%, streamlining healthcare delivery and reducing patient wait times.

From an ESG perspective, companies are committing to sustainability metrics such as achieving a 30% reduction in electronic waste and increasing recycling rates by 40% by 2030. In 2023, Medtronic achieved a 15% reduction in energy consumption through the implementation of energy-efficient biosensor technologies, demonstrating the sector's commitment to environmental responsibility. Looking forward, the Bioelectronics and Biosensors Market is poised to be a pillar of resilience, compliance, and sustainable growth, driven by technological advancements, regulatory support, and a focus on patient-centered care.

The Bioelectronics and Biosensors Market is experiencing dynamic growth, influenced by technological advancements, regulatory developments, and shifting consumer preferences. Key trends include the integration of artificial intelligence in biosensor devices, enhancing diagnostic accuracy and efficiency. Additionally, the increasing prevalence of chronic diseases is driving demand for continuous monitoring solutions. Regulatory bodies are adapting to these innovations, facilitating the approval of new biosensor technologies. Consumer adoption is on the rise, particularly in regions with advanced healthcare infrastructures, as individuals seek more personalized and accessible healthcare options.

The rising incidence of chronic diseases such as diabetes and cardiovascular conditions is significantly boosting the demand for biosensors. For example, the Centers for Disease Control and Prevention reported that over 34 million Americans were diagnosed with diabetes in 2020, highlighting the need for continuous glucose monitoring solutions. Biosensors offer real-time data, enabling better disease management and timely interventions, thereby improving patient outcomes and reducing healthcare costs.

The development of advanced biosensor technologies involves substantial investment in research and development, leading to high production costs. These expenses can limit the affordability and accessibility of biosensors, particularly in low-resource settings. Additionally, the complex regulatory approval processes for medical devices can delay time-to-market, further impacting the widespread adoption of biosensor technologies.

The shift towards personalized medicine creates significant opportunities for biosensor technologies. Biosensors enable the monitoring of individual biomarkers, facilitating tailored treatment plans and improving therapeutic outcomes. As healthcare moves towards more individualized approaches, the demand for biosensors that provide precise and real-time data is expected to increase, opening new avenues for market growth.

Regulatory challenges pose a significant barrier to the Bioelectronics and Biosensors Market. The lengthy and complex approval processes for new biosensor technologies can delay their introduction to the market, hindering innovation and limiting patient access to advanced diagnostic tools. Additionally, varying regulatory standards across regions can complicate the global commercialization of biosensor products, affecting scalability and profitability.

Modular Construction Enhances Biosensor Manufacturing Efficiency: The adoption of modular construction techniques is significantly improving efficiency in biosensor manufacturing facilities. Approximately 55% of new biosensor production facilities have reported cost benefits from using modular and prefabricated practices. Prefabricated components are assembled off-site using automated machines, reducing labor needs and accelerating project timelines. This trend is particularly prominent in Europe and North America, where construction efficiency is critical.

Integration of Artificial Intelligence in Biosensor Devices: Artificial intelligence (AI) is increasingly being integrated into biosensor devices to enhance their capabilities. AI algorithms enable real-time data analysis, improving diagnostic accuracy and predictive capabilities. This integration is leading to more personalized and timely healthcare interventions, thereby expanding the applications of biosensors in medical diagnostics.

Rise of Wearable Biosensors for Continuous Health Monitoring: Wearable biosensors are gaining popularity for continuous health monitoring, offering individuals real-time insights into their health status. These devices are particularly beneficial for managing chronic conditions such as diabetes and cardiovascular diseases, allowing for proactive health management and timely medical interventions.

Advancements in Non-Invasive Biosensor Technologies: Advancements in non-invasive biosensor technologies are enabling more comfortable and accessible health monitoring solutions. These technologies eliminate the need for blood samples, reducing patient discomfort and increasing the adoption of biosensors in various healthcare settings. The development of non-invasive biosensors is expanding the potential applications of biosensor technologies in preventive healthcare.

The bioelectronics and biosensors market is segmented based on type, application, and end-user. By type, the market includes electrochemical biosensors, optical biosensors, piezoelectric biosensors, and others. Electrochemical biosensors are widely used due to their high sensitivity and cost-effectiveness. In terms of application, clinical diagnostics dominate, driven by the increasing demand for point-of-care testing and continuous health monitoring. End-users encompass hospitals, clinics, diagnostic laboratories, and research institutions, each contributing to the adoption of biosensor technologies in healthcare settings.

Electrochemical biosensors currently account for 80.6% of adoption, while optical sensors hold 15%. However, adoption in piezoelectric biosensors is rising fastest, expected to surpass 5% by 2032. Electrochemical biosensors' dominance is attributed to their widespread use in glucose monitoring devices across healthcare settings. The growing introduction and adoption of this technology in point-of-care applications further propel the segment's share. Other types, including optical and piezoelectric biosensors, contribute to niche applications, collectively accounting for the remaining market share.

Clinical diagnostics currently account for 70% of adoption, while health monitoring holds 20%. However, adoption in environmental monitoring is rising fastest, expected to surpass 15% by 2032. The clinical diagnostics segment leads due to the increasing number of point-of-care tests and the adoption of technology in disposable point-of-care devices. Health monitoring applications are also significant, driven by the demand for continuous monitoring solutions. Other applications, including environmental monitoring, contribute to niche areas, collectively accounting for the remaining market share. In 2024, more than 38% of enterprises globally reported piloting biosensor systems for patient monitoring.

Hospitals and clinics currently account for 60% of adoption, while diagnostic laboratories hold 25%. However, adoption in research institutions is rising fastest, expected to surpass 20% by 2032. Hospitals and clinics are key end-users of biosensors, employing these devices for rapid and accurate diagnosis of diseases and monitoring of patient health parameters. Diagnostic laboratories also play a significant role in the adoption of biosensors, utilizing them for precise and reliable testing. Research institutions contribute to the development and innovation of biosensor technologies, driving advancements in the field. In 2024, over 42% of U.S. hospitals tested integrated biosensor systems combining radiology and patient data.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

North America maintains dominance due to robust healthcare infrastructure, high adoption of wearable and point-of-care biosensors, and significant investment in R&D, totaling over 1.5 million deployed units in 2024. Asia-Pacific, led by China, Japan, and India, shows rapid uptake in hospital-based and home-use biosensor devices, with over 2.1 million units anticipated by 2028. Europe follows with 25% market share in 2024, driven by Germany, UK, and France, emphasizing regulatory compliance and AI integration. South America and Middle East & Africa collectively account for 12% of the market share, with increasing interest in localized applications and infrastructure development. Consumer adoption varies, with North America prioritizing clinical use, Europe focusing on regulatory-compliant diagnostics, and Asia-Pacific favoring mobile-enabled monitoring solutions.

How is technological integration shaping advanced healthcare solutions?

North America holds 38% of the global bioelectronics and biosensors market, with strong demand driven by healthcare, diagnostics, and research industries. Regulatory support from the FDA has enabled faster approvals for innovative biosensor devices, while digital transformation trends such as AI-based predictive diagnostics and cloud-enabled monitoring are expanding adoption. Local player Medtronic has deployed advanced wearable biosensors in over 200 hospitals, improving patient monitoring efficiency by 18%. North American enterprises demonstrate higher adoption in hospitals and research labs, with over 42% of medical facilities implementing continuous monitoring solutions and real-time analytics.

What regulatory and technological factors are driving market adoption?

Europe holds 25% of the global bioelectronics and biosensors market, with key markets including Germany, UK, and France. Stringent regulatory frameworks and sustainability initiatives are accelerating demand for explainable and eco-friendly biosensor devices. Adoption of AI-enabled diagnostics and non-invasive monitoring systems is growing, enhancing patient outcomes. Local player Siemens Healthineers has introduced integrated biosensor solutions for cardiac monitoring, benefiting over 60,000 patients. European consumer behavior reflects a strong preference for regulatory-compliant and technologically advanced healthcare solutions, particularly in urban medical centers.

How is innovation fueling healthcare technology adoption?

Asia-Pacific accounts for 28% of the market volume, led by China, India, and Japan. Rapid hospital expansion, digital healthcare initiatives, and increasing e-commerce penetration drive biosensor adoption. Innovation hubs in Tokyo, Beijing, and Bangalore focus on AI-powered wearable devices and non-invasive diagnostics. Local companies such as Omron Healthcare have launched continuous monitoring devices reaching over 1.2 million users. Consumer behavior favors mobile app-enabled monitoring and home-based health management, reflecting a shift towards preventive care and remote diagnostics.

What is driving market adoption in emerging economies?

South America holds approximately 7% of the global bioelectronics and biosensors market, with Brazil and Argentina leading adoption. Infrastructure development in hospitals and energy-efficient manufacturing facilities supports market growth. Government incentives and trade policies encourage local production of biosensor devices. Local player DMC Electronics has expanded distribution networks in Brazil, supplying over 50,000 units for clinical and home-use applications. Consumers demonstrate high engagement with localized, language-specific healthcare devices, particularly in urban regions.

How are technological modernization and sector demands influencing adoption?

Middle East & Africa collectively hold 5% of the global bioelectronics and biosensors market, with UAE and South Africa as major contributors. Demand is driven by oil & gas, construction, and healthcare sectors requiring precise monitoring solutions. Technological modernization, including cloud-based monitoring and AI integration, is accelerating adoption. Local companies like LifeSensors Middle East have deployed advanced diagnostic biosensors in hospitals, improving patient throughput by 12%. Consumer behavior varies, with healthcare providers seeking high-accuracy devices, while remote monitoring adoption is growing among urban populations.

United States – 38% market share | Dominance due to advanced healthcare infrastructure, high production capacity, and strong end-user adoption.

China – 22% market share | Rapid market expansion driven by hospital modernization, digital health initiatives, and technology-driven consumer adoption.

The Bioelectronics and Biosensors market is characterized by a moderately consolidated competitive environment, with the top five companies collectively holding approximately 40% of the global market share. This indicates a highly competitive landscape where established industry leaders and emerging players actively pursue market share through strategic initiatives such as product innovations, partnerships, mergers, and acquisitions. Key players are investing heavily in technological advancements and portfolio expansion. Abbott Laboratories is focusing on continuous glucose monitoring systems, enhancing its footprint in wearable biosensors. Medtronic is expanding diabetes management solutions with advanced point-of-care devices, while Roche continues to integrate AI and data analytics into diagnostic biosensors. Bio-Rad Laboratories and DuPont are exploring next-generation biosensor technologies, emphasizing precision and cost-effectiveness.

Innovation trends significantly influence competition, with companies developing wearable, implantable, and point-of-care biosensor devices to address rising demand for personalized healthcare solutions. Advances in microelectronics, nanotechnology, and AI integration are driving efficiency, accuracy, and scalability of biosensor products. While the market is moderately consolidated, the presence of numerous smaller innovators fosters a dynamic competitive environment. Companies leveraging technological breakthroughs, strategic partnerships, and global distribution networks are positioned to capture emerging opportunities and expand their market presence in the growing bioelectronics and biosensors sector.

Bio-Rad Laboratories, Inc.

DuPont

Biosensors International Group, Ltd.

Dexcom, Inc.

Masimo Corporation

Nova Biomedical Corporation

Universal Biosensors, Inc.

ACON Laboratories, Inc.

The Bioelectronics and Biosensors market is experiencing transformative advancements driven by innovations in sensor technologies, materials science, and system integration. Electrochemical biosensors continue to dominate, capturing approximately 71.7% of the market in 2024 due to their low detection limits, wide linear response range, stability, and repeatability. These devices are widely used across biochemical and biological processes, offering robustness, microfabrication compatibility, disposability, and cost-efficiency. Optical biosensors are gaining traction as they provide broad analytical coverage, enabling receptor-cell interaction studies, fermentation monitoring, structural research, and precise concentration analyses. Integration with microfluidics and lab-on-chip technologies enhances speed and accuracy, facilitating point-of-care diagnostics.

Emerging technologies such as plasmonics and quantum sensing are poised to revolutionize the market. Plasmonics integration in biosensors improves sensitivity and detection limits, while quantum plasmonics combined with microfluidics addresses challenges in chemical and biological sensing by mitigating quantum fluctuations and noise. These technologies support rapid, highly sensitive, and label-free detection. Sustainability is becoming a key focus. Researchers at BITS Pilani, Hyderabad, developed a food-based nano conductive paste (FN-CoP) suitable for wearable, ingestible, and edible medical devices. This eco-friendly, non-toxic material offers high conductivity and electrochemical stability, marking a significant advancement toward sustainable bioelectronics solutions for healthcare applications.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In April 2024, researchers at BITS Pilani, Hyderabad, developed an innovative food-based nano conductive paste (FN-CoP) for wearable, ingestible, and edible medical devices. This non-toxic and sustainable material offers high conductivity, enhancing the performance and environmental sustainability of bioelectronic devices.

In March 2024, a European research institute in collaboration with a leading semiconductor company developed a flexible, stretchable biosensor platform for real-time glucose monitoring, improving diabetes management through continuous, non-invasive monitoring. Source: www.sciencedirect.com

In February 2024, a U.S.-based startup launched a lab-on-chip biosensor capable of rapid detection of foodborne pathogens using microfluidic channels and optical sensing, delivering results within minutes and significantly reducing traditional testing time.

The Bioelectronics and Biosensors Market Report provides a comprehensive analysis covering product types, applications, end-users, and technological advancements. Key product segments include electrochemical, optical, piezoelectric, and thermal biosensors, detailing their performance, adoption rates, and niche relevance. The report also examines applications such as clinical diagnostics, environmental monitoring, food safety, and industrial processes, highlighting market penetration and technology adoption patterns in each area. Geographically, the report analyzes major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing market dynamics, regulatory frameworks, infrastructure developments, and consumer behavior variations. Emerging trends in wearable devices, implantable sensors, lab-on-chip systems, and AI-enabled diagnostics are emphasized for their role in personalized healthcare and real-time monitoring.

The report also addresses the integration of microfluidics, nanotechnology, and artificial intelligence, exploring their impact on device efficiency, accuracy, and scalability. Sustainability trends, such as the development of eco-friendly materials and energy-efficient manufacturing processes, are also discussed. This report offers business decision-makers, investors, and industry professionals actionable insights into market opportunities, technological trends, and strategic pathways, serving as a critical tool for informed planning and investment in the Bioelectronics and Biosensors market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 16324 Million |

|

Market Revenue in 2032 |

USD 34991.94 Million |

|

CAGR (2025 - 2032) |

10% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Abbott Laboratories, F. Hoffmann-La Roche Ltd, Medtronic, Bio-Rad Laboratories, Inc., DuPont, Biosensors International Group, Ltd., Dexcom, Inc., Masimo Corporation, Nova Biomedical Corporation, Universal Biosensors, Inc., ACON Laboratories, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |