Reports

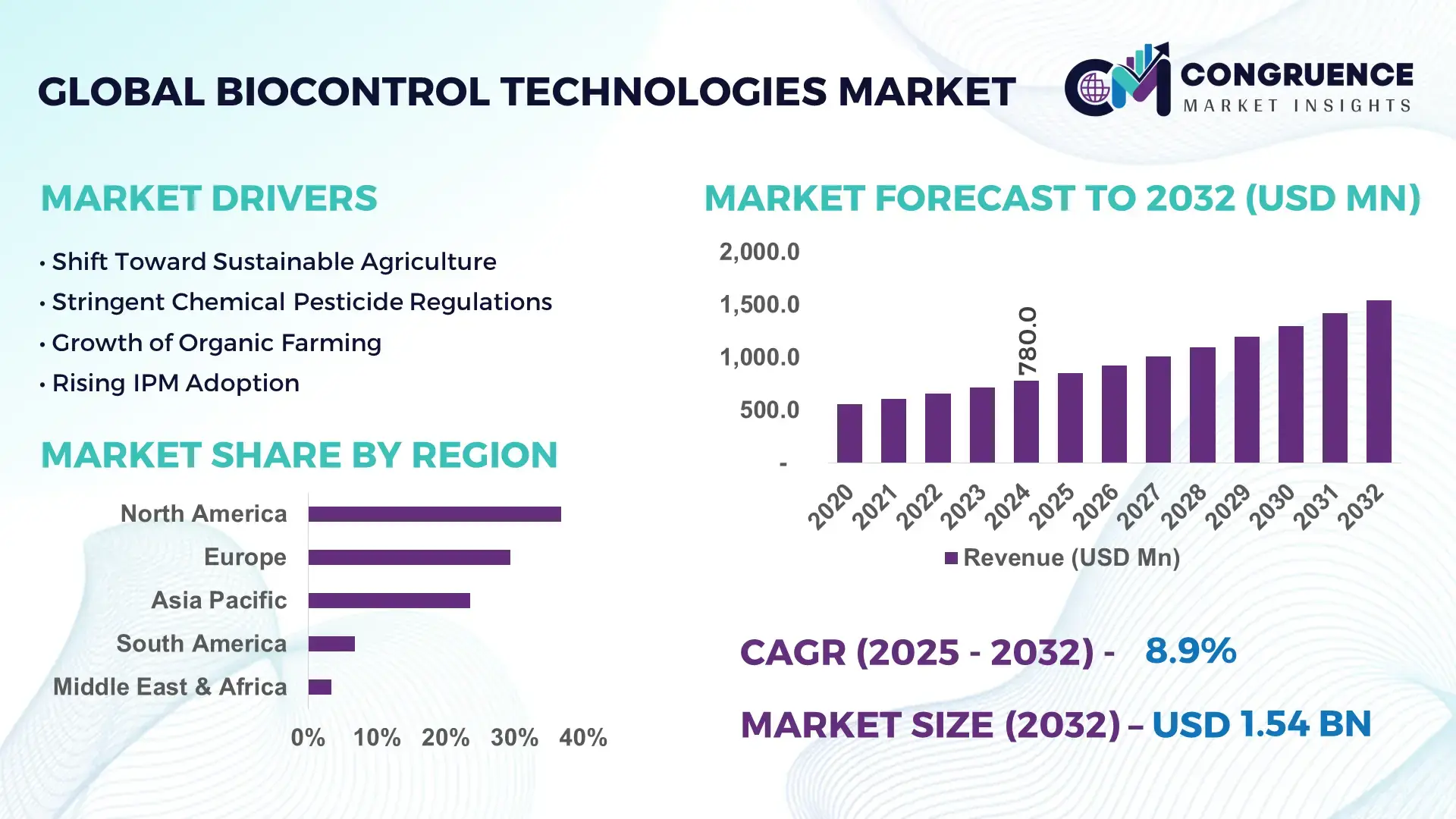

The Global Biocontrol Technologies Market was valued at USD 780.0 Million in 2024 and is anticipated to reach a value of USD 1,542.8 Million by 2032 expanding at a CAGR of 8.9% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily supported by rising regulatory restrictions on chemical pesticides and the accelerating adoption of sustainable agricultural inputs across commercial farming systems.

The United States represents the most influential country within the global Biocontrol Technologies Market in terms of industrial depth and deployment scale. The country hosts more than 400 registered biopesticide manufacturing facilities, with annual production capacity exceeding 120,000 metric tons of microbial and biochemical control agents. Public and private investments in biological crop protection surpassed USD 1.1 billion between 2021 and 2024, directed toward fermentation infrastructure, strain optimization, and field-level formulation technologies. Biocontrol products are actively applied across over 38% of U.S. row crop acreage, particularly in corn, soybean, and specialty fruit cultivation. Technological advancements include AI-assisted strain selection, controlled-release formulations, and precision spray integration, enabling improved efficacy consistency and scalable commercial deployment across large-scale agricultural operations.

Market Size & Growth: Valued at USD 780.0 Million in 2024, projected to reach USD 1,542.8 Million by 2032, expanding at a CAGR of 8.9%, driven by increasing bans on synthetic agrochemicals and sustainability-focused farming practices.

Top Growth Drivers: Adoption of integrated pest management increased by 42%, biological efficacy improvement reached 31%, and residue-free crop demand rose by 47%.

Short-Term Forecast: By 2028, biocontrol adoption is expected to reduce chemical pesticide dependency by 28% across commercial farms.

Emerging Technologies: AI-based microbial strain screening, nano-encapsulation delivery systems, and precision drone-based biocontrol application.

Regional Leaders: North America projected at USD 520 Million by 2032 with high mechanized adoption; Europe at USD 460 Million with regulatory-driven uptake; Asia Pacific at USD 390 Million supported by horticulture expansion.

Consumer/End-User Trends: Commercial agriculture accounts for 61% usage, followed by greenhouse cultivation and organic farming systems.

Pilot or Case Example: In 2023, a California vineyard project reduced fungal infestation by 36% using microbial biocontrol sprays.

Competitive Landscape: Bayer holds approximately 18% share, followed by Syngenta, BASF, Koppert, and Marrone Bio Innovations.

Regulatory & ESG Impact: Over 70 countries now provide fast-track approvals for biological pest control products.

Investment & Funding Patterns: Global investments exceeded USD 2.4 Billion during 2021–2024, focused on fermentation and formulation scaling.

Innovation & Future Outlook: Integration with precision agriculture platforms and climate-adaptive biocontrol solutions is reshaping product pipelines.

Biocontrol Technologies are widely applied across cereals, fruits, vegetables, and plantation crops, with cereals contributing nearly 34% of total demand. Recent innovations include multi-strain microbial blends, shelf-stable formulations, and compatibility with digital farm management tools. Regulatory emphasis on environmental safety, combined with rising organic food consumption in Europe and Asia Pacific, is accelerating adoption. Future growth is shaped by climate-resilient crop protection needs and cross-sector integration with precision agriculture.

The Biocontrol Technologies Market holds growing strategic relevance as agriculture, food security, and environmental compliance converge. Governments and agribusinesses are increasingly positioning biological crop protection as a core pillar of sustainable food systems. Compared to conventional synthetic pesticides, microbial biocontrol formulations deliver up to 35% improvement in target-specific pest suppression while reducing soil toxicity accumulation by over 40%. Fermentation-based microbial production delivers 28% higher scalability efficiency compared to older chemical synthesis standards.

Regionally, North America dominates in volume due to large-scale commercial farming, while Europe leads in adoption intensity, with over 52% of farms integrating at least one biological control product into pest management programs. Asia Pacific is emerging rapidly, supported by rising horticulture output and government-backed bio-input subsidy programs.

In the short term, by 2027, AI-driven strain optimization is expected to cut product development timelines by 22% and improve field efficacy consistency by 18%. From an ESG perspective, agribusiness firms are committing to reducing chemical pesticide runoff by 30% by 2030 through biological substitution strategies. In 2024, Brazil achieved a 26% reduction in chemical pesticide usage across soybean farms through nationwide microbial biocontrol deployment programs. Looking ahead, the Biocontrol Technologies Market is positioned as a critical enabler of agricultural resilience, regulatory compliance, and long-term sustainable productivity.

The Biocontrol Technologies Market is shaped by the intersection of regulatory pressure, technological advancement, and shifting agricultural practices. Increasing restrictions on chemical pesticides across North America and Europe are accelerating biological alternatives. Advances in microbial fermentation, formulation stability, and precision application are improving product reliability at scale. Climate variability is also driving demand, as biological agents demonstrate higher adaptability across temperature and humidity fluctuations. Additionally, alignment with organic certification standards and integrated pest management frameworks is expanding commercial viability. Market dynamics further reflect increasing collaboration between agri-tech firms, biotech startups, and research institutions to commercialize next-generation biological solutions.

Sustainability mandates across more than 70 agricultural economies are reshaping pest management strategies. Regulatory frameworks increasingly restrict residue limits, pushing growers toward biological alternatives. Over 48% of newly approved crop protection products between 2021 and 2024 were biologically derived. Large retailers now require residue-free certifications for premium produce categories, influencing supplier practices. Biocontrol technologies align with soil health preservation, reducing microbial degradation by nearly 33% compared to synthetic inputs. These mandates are creating structural demand across large-scale farming, greenhouse operations, and export-oriented agriculture.

Despite progress, formulation stability remains a critical limitation. Many microbial products exhibit shelf lives 40–50% shorter than chemical pesticides, increasing cold-chain dependency and logistics costs. Temperature sensitivity during storage and transport affects product efficacy consistency, particularly in tropical regions. Inadequate farmer training on handling biological inputs further reduces effectiveness, with misapplication rates reported above 18% in developing markets. These constraints limit adoption among cost-sensitive and infrastructure-constrained agricultural regions.

Precision agriculture integration presents a high-impact opportunity for biocontrol technologies. GPS-guided sprayers and drone-based delivery systems improve application accuracy by over 27%, reducing biological input wastage. Integration with farm management software enables real-time pest monitoring and targeted biocontrol deployment. Digital agriculture platforms are expanding across more than 45 million hectares globally, creating scalable deployment channels. This convergence enhances efficacy reliability, reduces operational costs, and supports data-driven pest management strategies.

Regulatory inconsistency across regions presents a significant challenge. Approval timelines for biological products vary from 6 months in some EU states to over 36 months in certain emerging economies. Differences in strain classification, residue testing protocols, and labeling requirements increase compliance costs. Smaller manufacturers face delays in cross-border commercialization, limiting global scalability. These regulatory complexities slow innovation diffusion and restrict market penetration despite strong underlying demand.

Expansion of AI-Enabled Microbial Discovery: AI-driven screening platforms have reduced microbial strain discovery cycles by 29% while increasing efficacy hit rates by 21%. Over 60 biotech firms globally now deploy machine-learning tools to identify pest-specific biological agents faster than traditional laboratory methods.

Growth in Precision Application Technologies: Drone-based biocontrol application expanded by 41% between 2022 and 2024. Precision spraying reduces input waste by 24% and improves field-level pest suppression consistency by 19%, particularly in horticulture and plantation crops.

Shift Toward Multi-Strain Formulations: Multi-strain microbial products now account for 37% of new product launches. These formulations enhance resistance management and increase pest control durability by up to 32% under variable climatic conditions.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Biocontrol Technologies Market. Research suggests that 55% of new production facilities achieved cost efficiencies through prefabricated fermentation units, reducing setup timelines by 34% and improving production scalability across North America and Europe.

The Biocontrol Technologies Market is segmented based on type, application, and end-user groups, reflecting the diversity of biological solutions and their deployment across agricultural and non-agricultural systems. By type, the market spans microbial agents, biochemical agents, and macro-organisms, each addressing specific pest and disease challenges. Applications range from crop protection and soil health management to post-harvest treatment and forestry use, with varying adoption intensity depending on crop type and regulatory frameworks. From an end-user perspective, commercial agriculture dominates, followed by greenhouse operators, organic farms, and public-sector land management bodies. Segmentation trends indicate a gradual shift toward integrated solutions combining multiple biocontrol types, driven by resistance management needs, environmental compliance, and the push for sustainable productivity. Decision-makers increasingly evaluate segmentation not only by efficacy, but also by compatibility with precision agriculture systems and regulatory acceptance across regions.

The market by type includes microbial biocontrol agents, biochemical biocontrol agents, and macro-organisms. Microbial biocontrol agents—including bacteria, fungi, and viruses—represent the leading segment, accounting for approximately 46% of total adoption, supported by their broad-spectrum applicability across cereals, fruits, and vegetables, along with scalability through fermentation-based production. In comparison, biochemical agents such as pheromones and plant extracts hold around 29% of adoption, primarily used in targeted pest monitoring and mating disruption strategies. However, macro-organisms, including predatory insects and parasitoids, are witnessing the fastest growth, expanding at an estimated 11.2% CAGR, driven by increasing use in greenhouse and high-value horticulture systems where chemical inputs are restricted. The remaining niche biological formulations, including nematodes and botanicals, collectively account for nearly 25% of the market, serving specialized crop and regional needs.

By application, crop protection remains the dominant segment, accounting for nearly 58% of total usage, as biocontrol products are increasingly integrated into pest and disease management programs for cereals, oilseeds, fruits, and vegetables. Soil health and yield enhancement applications represent about 24% of adoption, leveraging microbial agents to improve nutrient uptake and suppress soil-borne pathogens. However, post-harvest protection and storage pest control is the fastest-growing application area, expanding at an estimated 10.6% CAGR, supported by rising demand for residue-free storage solutions and export-quality produce. Forestry, turf management, and landscape applications together contribute the remaining 18%, largely driven by public-sector and municipal initiatives. In 2024, more than 41% of large commercial farms globally reported piloting biological crop protection solutions as part of integrated pest management programs.

From an end-user perspective, commercial agriculture enterprises lead the Biocontrol Technologies Market, accounting for approximately 62% of total adoption, reflecting large-scale deployment across row crops, plantations, and export-oriented farming operations. Greenhouse and controlled-environment agriculture operators hold around 21%, benefiting from predictable conditions that enhance biocontrol effectiveness. However, organic farming operations represent the fastest-growing end-user segment, expanding at an estimated 12.4% CAGR, fueled by rising organic food demand and stricter certification requirements limiting synthetic inputs. Public land management agencies, landscaping services, and smallholder cooperatives together contribute the remaining 17%, often supported by subsidy and sustainability programs. In 2024, over 39% of greenhouse operators globally reported increasing biological input usage to manage resistance issues.

North America accounted for the largest market share at 36.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.9% between 2025 and 2032.

Regional performance is shaped by differences in regulatory maturity, agricultural practices, and technology adoption. North America and Europe lead in large-scale commercial deployment, supported by strict pesticide regulations and advanced farming infrastructure. Asia-Pacific shows accelerating momentum due to rising food demand, government-backed bio-input programs, and expanding horticulture acreage. South America benefits from export-oriented agriculture and tropical crop cultivation, while the Middle East & Africa market is emerging, driven by food security initiatives and arid-climate pest management needs. Collectively, the top three regions account for over 78% of global biocontrol adoption, underscoring the concentration of technological capacity and end-user readiness.

North America represents approximately 36.8% of global biocontrol adoption, supported by extensive commercial farming and early regulatory acceptance of biological inputs. The United States and Canada together deploy biocontrol solutions across more than 45 million hectares of cropland. Key demand-driving industries include row crop agriculture, specialty fruits, vegetables, and greenhouse cultivation. Government support includes expedited approvals for biological products and sustainability-linked farm incentive programs. Technological advancements include AI-enabled strain optimization, precision sprayers, and drone-based application systems, improving field-level efficiency by over 20%. Local players such as Marrone Bio Innovations focus on microbial-based fungicides and insecticides tailored for large-acreage crops. Regional consumer behavior shows higher adoption among large agribusiness enterprises, with over 44% of commercial farms integrating at least one biological control solution into pest management programs.

Europe accounts for roughly 29.4% of the global market, driven by stringent environmental regulations and sustainability initiatives. Key markets include Germany, France, Italy, and Spain, where biological alternatives are increasingly favored over chemical pesticides. Regulatory bodies enforce strict residue limits, accelerating adoption of microbial and pheromone-based solutions. Emerging technologies such as multi-strain formulations and digital pest monitoring platforms are gaining traction. Local companies like Koppert Biological Systems actively expand greenhouse and horticulture-focused biocontrol portfolios. Consumer behavior in the region reflects regulatory-driven demand, with over 52% of protected cultivation operators prioritizing biological inputs to meet compliance and certification standards.

Asia-Pacific ranks as the fastest-growing regional market, accounting for approximately 23.6% of global adoption. China, India, and Japan are the top consuming countries, collectively covering more than 60% of regional usage. Expansion of horticulture, rice cultivation, and plantation crops supports demand. Manufacturing capacity is increasing, with over 180 regional production units dedicated to microbial fermentation and formulation. Innovation hubs in China and India focus on cost-effective biopesticides and locally adapted strains. Regional consumer behavior reflects rapid adoption among small and mid-sized farms, supported by government subsidy programs and digital advisory platforms.

South America holds around 6.8% of global adoption, with Brazil and Argentina as key contributors. The region’s demand is driven by soybean, sugarcane, coffee, and fruit exports. Infrastructure investments in bio-input production and distribution support market expansion. Government incentives promoting sustainable agriculture and reduced chemical residues enhance adoption. Brazilian firms such as biological input cooperatives focus on large-scale microbial solutions for tropical pests. Regional consumer behavior is closely tied to export compliance, with over 35% of export farms adopting biological pest control to meet international residue standards.

The Middle East & Africa region accounts for approximately 3.4% of global usage, reflecting its emerging market status. Demand is concentrated in countries such as the UAE, Saudi Arabia, South Africa, and Kenya. Applications focus on horticulture, date palms, and protected agriculture. Technological modernization includes greenhouse farming and controlled-environment agriculture. Local regulations emphasize food security and water-efficient farming. Regional players increasingly deploy microbial biocontrol solutions adapted to arid climates. Consumer behavior highlights adoption by high-value crop producers, with biological solutions used to manage pest pressure under water-scarce conditions.

United States – 28.6% Market Share: Strong dominance due to large-scale commercial agriculture, advanced production capacity, and early regulatory acceptance of biological inputs.

Germany – 11.9% Market Share: Leadership driven by strict environmental regulations, high adoption in protected cultivation, and strong innovation ecosystems for biological crop protection.

The Biocontrol Technologies Market features a moderately fragmented competitive structure, characterized by the presence of more than 80–100 active commercial participants globally, ranging from multinational agrochemical firms to specialized biological solution providers and regional innovators. The top five companies collectively account for approximately 54–58% of total market activity, reflecting increasing consolidation around firms with advanced microbial R&D capabilities, global regulatory expertise, and scalable fermentation infrastructure. Competitive positioning is shaped by continuous product innovation, portfolio expansion across microbial, biochemical, and macro-organism solutions, and geographic penetration into high-growth agricultural regions. Strategic initiatives such as partnerships with agri-tech platforms, acquisitions of niche biological startups, and investments in digital agriculture integration are intensifying competitive differentiation. More than 45% of leading players launched new biological formulations or expanded label claims between 2022 and 2024, highlighting rapid innovation cycles. Competition is also influenced by regulatory navigation strength, as firms with faster approval pipelines gain time-to-market advantages. Overall, competition is shifting from price-based rivalry toward performance reliability, formulation stability, and compatibility with precision agriculture systems.

Koppert Biological Systems

Marrone Bio Innovations

Certis Biologicals

Valent BioSciences

Biobest Group

Andermatt Group

Technology evolution is central to competitiveness in the Biocontrol Technologies Market. Microbial fermentation optimization has significantly improved production yields, with next-generation bioreactors delivering up to 32% higher output efficiency compared to conventional batch systems. Advances in strain genomics and AI-assisted screening enable faster identification of pest-specific microbes, reducing development timelines by approximately 25%. Encapsulation and controlled-release formulations enhance shelf life and field stability, extending product usability by 40–50% under variable climatic conditions. Precision application technologies, including GPS-enabled sprayers and drone-based delivery, reduce input wastage by 20–27% while improving coverage accuracy. Integration with digital farm management platforms allows real-time pest monitoring and targeted biocontrol deployment. Emerging technologies include multi-strain synergistic formulations, which improve resistance management, and RNA-based biological solutions for species-specific pest control. Additionally, advancements in cold-chain logistics and carrier materials are addressing historical storage and transport challenges. Collectively, these technologies are transforming biocontrol from niche solutions into scalable, performance-driven agricultural inputs suitable for large-acreage deployment.

In August 2024, Biotalys NV was recognized as the “Sustainable Crop Protection Company of the Year” at the AgTech Breakthrough Awards, highlighting its innovation in protein-based biocontrol solutions such as its AGROBODY™ platform and biofungicide EVOCA™, which demonstrated effective inhibition of Botrytis fruit rot and powdery mildew during field trials. Source: www.biotalys.com

In April 2024, Koppert Biological Systems expanded its field trial program globally with approximately 300 demonstration trials, showcasing beneficial insects and microbial solutions (e.g., predatory mites and nematodes) against pests such as wireworms, achieving up to ~30 percentage points reduction in damage in potato trials versus untreated controls. Source: www.koppert.com

In March 2025, Koppert announced a strategic partnership with Insect Science, naming the latter its preferred supplier of semiochemical solutions to enhance sustainable pest management tools such as monitoring lures and mating disruption products across Southern Europe and the Middle East & Africa regions. Source: www.koppert.com

In 2024, UPL launched a seed treatment biocontrol product (NIMAXXA) in Brazil that combines three Bacillus strains to control nematodes while providing root biostimulation, offering a two-year shelf life without refrigeration and six-month seed viability. Source: news.agropages.com

The Biocontrol Technologies Market Report provides a comprehensive assessment of biological crop protection solutions across global agricultural systems. The scope includes detailed evaluation of product types such as microbial agents, biochemical agents, and macro-organisms, alongside emerging biological formulations and delivery technologies. It covers application areas including crop protection, soil health enhancement, post-harvest treatment, forestry, and turf management. The report examines end-user segments spanning commercial agriculture, greenhouse operations, organic farming, and public-sector land management. Geographic coverage extends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating regional deployment patterns, regulatory frameworks, and adoption intensity. The analysis also includes technology-focused insights into fermentation systems, formulation stability solutions, precision application tools, and digital integration trends. Additionally, the report evaluates competitive dynamics, innovation pipelines, and operational strategies shaping the market landscape. Emerging niches such as RNA-based biocontrol and climate-resilient biological solutions are included to reflect evolving industry priorities. Overall, the report is designed to support strategic planning, investment analysis, and decision-making for stakeholders across the agricultural and biological input value chain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 780.0 Million |

| Market Revenue (2032) | USD 1,542.8 Million |

| CAGR (2025–2032) | 8.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bayer CropScience AG; Syngenta Group; BASF SE; Koppert Biological Systems; Marrone Bio Innovations; Certis Biologicals; Valent BioSciences; Biobest Group; Andermatt Group |

| Customization & Pricing | Available on Request (10% Customization Free) |