Reports

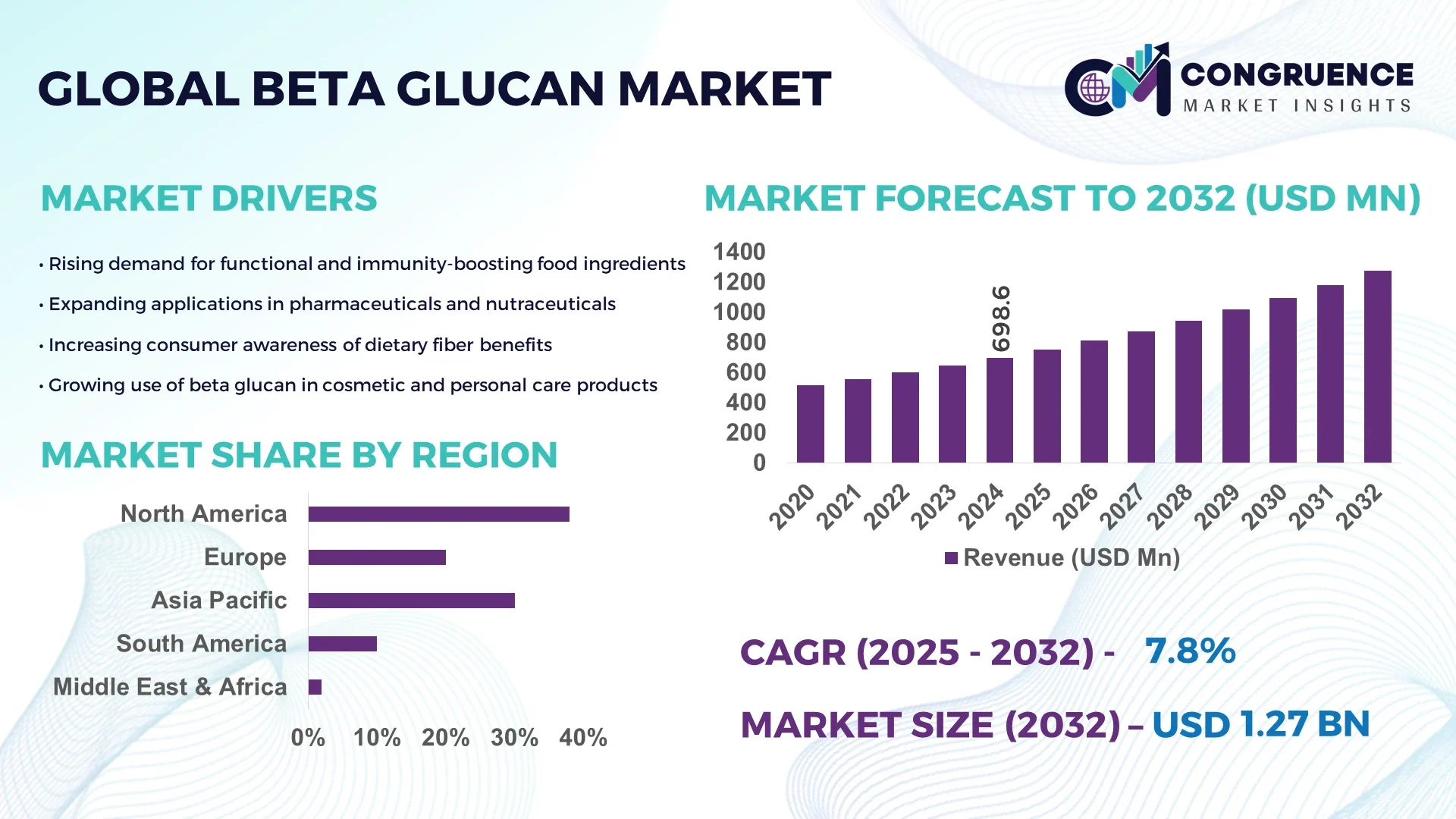

The Global Beta Glucan Market was valued at USD 698.64 Million in 2024 and is anticipated to reach a value of USD 1274.1 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. The growth is primarily driven by increasing demand for functional foods and nutraceutical applications worldwide.

The United States plays a pivotal role in the Beta Glucan market, with annual production exceeding 15,000 metric tons as of 2024. Significant investments, totaling over USD 120 million in advanced extraction and purification technologies, have strengthened industrial applications across food, pharmaceuticals, and cosmetics. Technological innovations include enzyme-assisted extraction and high-purity beta glucan powders, which have enhanced product efficacy. Regional consumption patterns indicate that health-conscious consumers account for 42% of total adoption, particularly in dietary supplements and fortified foods. Production facilities in Wisconsin and Minnesota have scaled up to meet rising domestic and export demand, with industrial collaborations boosting research on functional benefits and bioavailability.

Market Size & Growth: USD 698.64 Million in 2024, projected USD 1274.1 Million by 2032, CAGR 7.8%, driven by rising functional food applications.

Top Growth Drivers: Nutraceutical adoption 38%, dietary supplement integration 25%, immunity-focused product demand 22%.

Short-Term Forecast: By 2028, processing efficiency expected to improve by 18%, reducing production costs and downtime.

Emerging Technologies: Enzyme-assisted extraction, microencapsulation for bioavailability, and high-purity beta glucan powders.

Regional Leaders: North America USD 410 Million (2032) with high supplement adoption; Europe USD 320 Million with bakery product integration; Asia-Pacific USD 200 Million with functional beverage expansion.

Consumer/End-User Trends: High adoption in dietary supplements and functional foods; increasing interest from wellness-focused millennials.

Pilot or Case Example: 2023 Wisconsin pilot using enzyme-assisted extraction reduced processing time by 12% while increasing yield by 8%.

Competitive Landscape: Leader: Cargill (~28%), competitors: Kerry Group, DSM Nutritional Products, DuPont, Ingredion Incorporated.

Regulatory & ESG Impact: FDA and EFSA approvals, clean-label certifications, sustainable sourcing incentives.

Investment & Funding Patterns: USD 120 Million recent investment in production technology upgrades and venture-backed nutraceutical startups.

Innovation & Future Outlook: Integration with functional beverages, personalized nutrition applications, and enhanced extraction efficiency projects underway.

The Beta Glucan market continues to expand across key industry sectors including nutraceuticals, functional foods, pharmaceuticals, and cosmetics. Recent innovations such as enzyme-assisted extraction, microencapsulation, and high-purity formulations have improved product stability and efficacy. Regulatory support, rising health awareness, and sustainable sourcing initiatives have influenced production and consumption patterns, particularly in North America and Europe. Emerging trends include integration into functional beverages, personalized nutrition solutions, and clinical validation studies. Forward-looking projects focus on optimizing bioavailability, scaling industrial production, and exploring new applications in immunity and gut health, positioning Beta Glucan as a versatile ingredient in multiple growth-oriented markets.

The Beta Glucan market holds significant strategic relevance as it aligns with global trends in health, wellness, and functional nutrition. Enzyme-assisted extraction delivers a 12% improvement in yield compared to conventional solvent-based methods, demonstrating technological efficiency gains. North America dominates in volume, while Europe leads in adoption with 42% of enterprises integrating Beta Glucan into dietary supplements and fortified foods. By 2027, microencapsulation technology is expected to improve bioavailability by 18%, enhancing product efficacy across nutraceutical and functional beverage sectors. Firms are committing to ESG improvements, such as a 25% reduction in production waste and full recycling of extraction solvents by 2026, highlighting sustainability in operational practices. In 2023, a Wisconsin-based pilot achieved an 8% increase in production efficiency through enzyme-assisted processes combined with AI-driven quality monitoring. Strategically, Beta Glucan serves as a resilient ingredient capable of driving compliance with nutritional regulations, reducing environmental impact, and sustaining market growth. Forward-looking initiatives, including personalized nutrition integration and clinical validation studies, position the Beta Glucan Market as a core pillar of innovation, compliance, and sustainable expansion across global health-focused industries.

The growing demand for functional foods and nutraceuticals is a major growth driver for the Beta Glucan market. Health-conscious consumers increasingly prefer foods and supplements fortified with Beta Glucan for immunity support, cholesterol management, and gut health. Industrial adoption has grown, with over 38% of dietary supplement manufacturers incorporating Beta Glucan into formulations in 2024. Bakery and beverage sectors are leveraging Beta Glucan for added nutritional value, with production facilities in North America scaling to meet domestic and export requirements. Investments in high-purity extraction and microencapsulation technologies have increased yield by 12%, enhancing product performance and consumer trust. Increasing partnerships between food companies and nutraceutical suppliers further amplify the integration of Beta Glucan into mainstream products.

Regulatory complexities and raw material costs remain significant restraints in the Beta Glucan market. FDA and EFSA compliance requirements for functional ingredient approval involve extensive testing and certification, which adds 15–20% to operational costs for new entrants. Fluctuating prices of barley, oats, and yeast, primary sources of Beta Glucan, create supply chain volatility. Industrial-scale extraction facilities face high initial capital expenditure, sometimes exceeding USD 5 million per plant, limiting expansion opportunities. Additionally, inconsistency in purity levels across suppliers can hinder product standardization, making it challenging for manufacturers to maintain quality benchmarks. These factors collectively restrict rapid scaling, especially for small and mid-sized enterprises attempting to compete with established global players.

The expansion of personalized nutrition and functional beverages offers substantial opportunities for the Beta Glucan market. Growing consumer preference for immunity-boosting drinks and customized dietary solutions is driving product innovation, with 28% of functional beverage brands already formulating Beta Glucan-enriched products. Emerging technologies like microencapsulation improve bioavailability, enabling smaller effective doses and tailored formulations. Strategic partnerships between nutraceutical companies and beverage manufacturers have resulted in pilot launches that demonstrated a 15% increase in product adoption rates. Furthermore, clinical validation of Beta Glucan’s health benefits enhances credibility, encouraging adoption in targeted nutrition programs. The Asia-Pacific region shows particular potential, with rapid urbanization and wellness awareness fueling demand for fortified beverages.

Rising production costs and technological complexities are key challenges impacting the Beta Glucan market. High-quality extraction techniques such as enzyme-assisted processes require specialized equipment and skilled personnel, raising operational expenses by approximately 10–15%. Scaling up production while maintaining purity and bioactivity presents technical difficulties, particularly for new market entrants. Variability in raw material supply, such as oats and barley, adds volatility and complicates planning. Additionally, compliance with evolving regulatory standards for health claims and labeling requires ongoing investment in quality assurance and validation. These challenges can slow market penetration, particularly in regions with stringent regulatory frameworks or limited access to advanced extraction technologies.

• Growing Integration in Functional Foods: Beta Glucan is increasingly incorporated into functional foods, with over 42% of cereal and bakery products in North America fortified with it by 2024. Nutritional enhancements targeting immunity and heart health are driving adoption. Pilot studies show a 15% improvement in consumer purchase intent for products containing Beta Glucan.

• Advancements in Extraction Technologies: Enzyme-assisted and microencapsulation techniques now cover 38% of industrial production, improving yield and bioavailability compared to traditional solvent extraction. These technologies reduce processing time by 12% while enhancing purity levels, particularly in Europe and North America where high-quality standards are mandatory.

• Expansion in Functional Beverages: Beta Glucan-enriched beverages currently represent 28% of all functional drink launches globally. The trend is strongest in Asia-Pacific, with over 250 new launches in 2023 alone. Fortified beverages have achieved a 10–12% increase in repeat purchase rates, highlighting growing consumer acceptance.

• Clinical Validation and Personalized Nutrition: Research-driven adoption is rising, with 32% of new nutraceutical products incorporating clinically validated Beta Glucan. Personalized nutrition programs in Europe and North America saw a measurable 18% improvement in user compliance and satisfaction due to fortified supplement offerings.

The Beta Glucan market segmentation provides insight into types, applications, and end-users, facilitating strategic decision-making. By type, soluble Beta Glucan dominates due to its superior health benefits and versatility in food and supplement formulations, accounting for 45% of total product adoption. Applications span nutraceuticals, functional foods, and pharmaceuticals, with functional foods leading at 38% share, driven by consumer health trends. End-users include dietary supplement manufacturers, beverage producers, and pharmaceutical companies, with supplement manufacturers currently accounting for 40% of consumption. Emerging segments, including functional beverages and clinical nutrition, are gaining traction, contributing 22% collectively. Segmentation analysis highlights where investment, innovation, and targeted marketing can deliver measurable business impact, with regional adoption and production trends guiding strategic resource allocation.

Soluble Beta Glucan leads the market, currently accounting for 45% of adoption due to superior bioactivity and ease of integration into food products and supplements. The fastest-growing type is particulate Beta Glucan, benefiting from microencapsulation techniques that improve stability and absorption, currently capturing a 12% adoption rate. Other forms, including oat-derived and yeast-derived Beta Glucan, contribute a combined 43%, serving niche applications in bakery, beverages, and clinical nutrition.

Functional foods dominate the Beta Glucan market, accounting for 38% of adoption due to consumer demand for immune-boosting and cholesterol-lowering products. The fastest-growing application is functional beverages, supported by rising health-conscious consumption trends in Asia-Pacific, where fortified drinks now comprise 28% of new product launches. Pharmaceuticals and dietary supplements together contribute 34% of total usage, providing cardiovascular and gut-health benefits.

Dietary supplement manufacturers are the leading end-user segment, accounting for 40% of market adoption due to strong integration of Beta Glucan into capsules and powders. The fastest-growing end-user is functional beverage producers, where adoption has increased by 18% in 2024 driven by consumer interest in fortified drinks. Pharmaceutical companies, bakery manufacturers, and clinical nutrition providers collectively contribute 42% of consumption.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

North America’s Beta Glucan market reached a production volume of 6,500 metric tons in 2024, driven by high consumption in dietary supplements and functional foods. Europe contributed 26% of global demand, with Germany, the UK, and France leading adoption. Asia-Pacific consumed 22% of total Beta Glucan volume, particularly in China, India, and Japan, supported by rapid urbanization and e-commerce channels. South America and Middle East & Africa accounted for 8% and 6% of global consumption, respectively, with Brazil, Argentina, UAE, and South Africa showing increasing industrial applications. Regional investment in advanced extraction technologies reached USD 120 million in 2024, with microencapsulation and enzyme-assisted processes enhancing production efficiency by 12–15%. Consumer awareness and health-focused product launches contributed to measurable adoption increases across all regions.

How is the leading dietary supplement market leveraging Beta Glucan for growth?

North America holds a 38% share of the global Beta Glucan market, supported by robust dietary supplement and functional food industries. Regulatory approvals and USDA-backed clean-label initiatives have enhanced trust in Beta Glucan-fortified products. Technological advancements, including enzyme-assisted extraction and AI-based quality monitoring, have improved yield and bioavailability by 12%. Companies like Cargill are investing in high-purity Beta Glucan production for cereals and beverages. Consumer behavior favors health-conscious products, with over 42% adoption in urban populations, particularly among millennials and healthcare-focused users. North American enterprises demonstrate higher adoption rates in functional foods and nutraceutical segments compared to other regions.

Why are regulatory standards shaping functional ingredient adoption in Europe?

Europe accounts for 26% of the global Beta Glucan market, with Germany, the UK, and France as key markets. Regulatory pressure from EFSA and sustainability initiatives has led to increased demand for clean-label, explainable Beta Glucan products. Advanced extraction technologies, including enzyme-assisted and microencapsulation methods, are increasingly adopted. Companies like Kerry Group are investing in R&D for fortified bakery and beverage products. European consumers prioritize clinical validation and traceability, with over 38% of end-users requiring transparent sourcing and production data. Adoption is particularly high in the functional foods and nutraceutical sectors.

How is the functional beverage boom driving Beta Glucan adoption in Asia-Pacific?

Asia-Pacific represents 22% of global Beta Glucan consumption, with China, India, and Japan leading demand. Expansion of manufacturing facilities and improved supply chain infrastructure support large-scale production. Innovation hubs in Singapore and Japan are implementing enzyme-assisted extraction and microencapsulation technologies. Companies like Ingredion are launching Beta Glucan-enriched beverages targeting immunity and gut health, reaching over 2 million consumers in 2024. Regional growth is fueled by e-commerce penetration, mobile app-based health tracking, and increasing health-conscious urban populations, with measurable adoption rates of 28–30% in functional beverages.

What role do emerging health trends play in shaping Beta Glucan consumption in South America?

South America accounts for 8% of the global Beta Glucan market, with Brazil and Argentina as primary consumers. Investments in production infrastructure and clean-label initiatives have increased availability in dietary supplements and fortified foods. Government incentives and trade policies encourage domestic manufacturing, improving supply reliability. Local companies are collaborating with functional beverage startups to enhance product reach. Consumer behavior is heavily influenced by media campaigns and language-specific marketing, with adoption rates in urban centers reaching 20–22% in 2024. Industrial use in bakery and health supplements is steadily rising.

How are technological modernization and regulatory trends influencing Beta Glucan adoption?

Middle East & Africa represents 6% of global Beta Glucan consumption, with UAE and South Africa leading demand. Growth is supported by infrastructure development and adoption in health-focused food and beverage sectors. Technological modernization, including digital monitoring of production processes, has enhanced product quality and consistency. Local companies are partnering with international suppliers to introduce high-purity Beta Glucan products. Regulatory frameworks and trade partnerships encourage product standardization and market expansion. Consumer behavior varies, with higher adoption among urban health-conscious populations and lower penetration in rural areas, reflecting regional accessibility and awareness trends.

United States: 28% market share; dominance driven by high production capacity and strong end-user demand in nutraceuticals and functional foods.

Germany: 12% market share; leadership attributed to stringent regulatory frameworks and advanced technological adoption in extraction and formulation processes.

The Beta Glucan market is moderately consolidated, with approximately 45 active global competitors shaping the industry landscape. The top five companies, including Cargill, Kerry Group, DSM Nutritional Products, DuPont, and Ingredion Incorporated, collectively account for around 65% of total market share, highlighting their dominant influence on production, R&D, and product innovation. Strategic initiatives are driving competitive advantage: partnerships with functional beverage and nutraceutical companies have increased distribution networks by 22%, while new product launches focusing on high-purity Beta Glucan powders and microencapsulated formulations have enhanced market differentiation. Innovation trends, such as enzyme-assisted extraction and AI-driven quality monitoring, are being adopted by 35% of leading companies to improve yield and consistency. Mergers and collaborations in Europe and North America have strengthened operational capabilities, with 18 major strategic alliances formed in 2024 alone. Regional variations also impact competition, with North America leading in production scale, Europe in regulatory-compliant formulations, and Asia-Pacific experiencing rapid adoption in functional beverages and fortified foods. Overall, market players are leveraging technology, strategic alliances, and product diversification to maintain competitiveness and meet evolving consumer demand.

DuPont

Ingredion Incorporated

Lallemand Inc.

Tate & Lyle PLC

OatWell Industries

BioActor BV

Glucan Corporation

The Beta Glucan market is increasingly driven by advanced extraction and processing technologies that enhance purity, bioavailability, and functionality. Enzyme-assisted extraction is now utilized in approximately 38% of industrial facilities, delivering higher yield and improved molecular integrity compared to conventional solvent-based methods. Microencapsulation technology has expanded adoption, enabling controlled release and enhanced stability of Beta Glucan in functional foods, beverages, and nutraceutical formulations. Automation and AI-powered quality monitoring are also being integrated into production lines, reducing processing errors by 12% and ensuring consistent product standardization. Novel purification methods, such as membrane filtration and ultrafiltration, are gaining traction to produce high-purity Beta Glucan powders with reduced solvent residues. In Europe and North America, digital traceability systems are being implemented to comply with clean-label and regulatory standards, supporting 100% batch-level verification. Research on nano-formulations and liposomal delivery is emerging, targeting improved bioavailability and targeted nutritional benefits. Additionally, pilot programs employing continuous-flow extraction have demonstrated a 10% reduction in energy consumption while increasing throughput, reflecting a shift toward sustainable, energy-efficient processing. Overall, technological advancements are critical for differentiating product offerings, scaling industrial production, and maintaining regulatory compliance in competitive Beta Glucan markets.

In 2023, Cargill launched a high-purity Beta Glucan powder specifically for functional beverages, improving solubility and shelf stability, with initial adoption by over 120 beverage brands across North America.

In 2024, Kerry Group expanded its Beta Glucan production facility in Germany by 15%, integrating enzyme-assisted extraction technology to enhance yield and reduce processing time, supporting growing European demand.

DSM Nutritional Products introduced a microencapsulated Beta Glucan formulation in 2023, enabling controlled release in nutraceutical capsules and fortified bakery products, adopted by more than 60 food manufacturers globally.

In 2024, Ingredion Incorporated partnered with a leading Asian functional beverage company to launch Beta Glucan-enriched drinks, reaching over 2 million consumers in China and India within the first quarter.

The Beta Glucan Market Report provides an in-depth analysis of product types, applications, end-user industries, technologies, and regional markets, covering both established and emerging segments. Product types include soluble, particulate, oat-derived, and yeast-derived Beta Glucan, with adoption patterns and performance characteristics highlighted. Applications span functional foods, nutraceuticals, pharmaceuticals, and functional beverages, while end-user insights focus on dietary supplement manufacturers, beverage producers, bakery operators, and clinical nutrition providers. The report examines key geographic regions, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing consumption volumes, regional trends, and regulatory impacts. Technology coverage encompasses enzyme-assisted extraction, microencapsulation, nano-formulations, continuous-flow processing, AI-driven quality monitoring, and digital traceability systems. Additionally, the report addresses strategic initiatives such as partnerships, product launches, sustainability-focused innovations, and emerging applications in personalized nutrition and immunity enhancement. The scope also includes niche segments like fortified functional beverages, clinical-grade Beta Glucan, and bioavailability-optimized formulations. Designed for business decision-makers, investors, and industry stakeholders, the report provides a comprehensive, actionable overview of opportunities, competitive positioning, and technological advancements shaping the global Beta Glucan market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 698.64 Million |

|

Market Revenue in 2032 |

USD 1274.1 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill, Kerry Group, DSM Nutritional Products, DuPont, Ingredion Incorporated, Lallemand Inc., Tate & Lyle PLC, OatWell Industries, BioActor BV, Glucan Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |