Reports

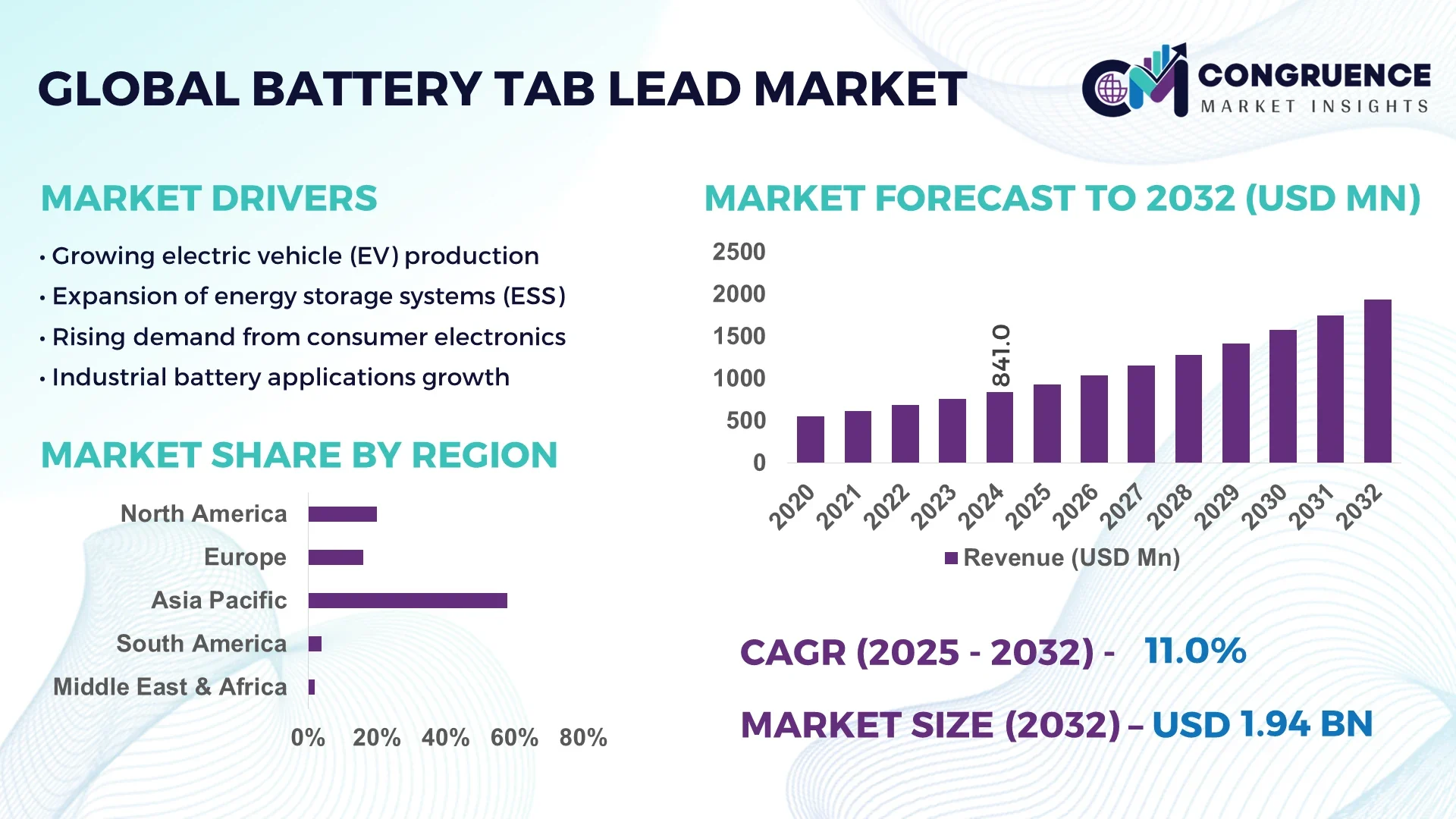

The Global Battery Tab Lead Market was valued at USD 841 Million in 2024 and is anticipated to reach a value of USD 1,938.1 Million by 2032 expanding at a CAGR of 11.0% between 2025 and 2032.

In China, which dominates the marketplace, the battery tab lead industry has ramped up production capacity significantly. Major manufacturers have invested in high-precision punching, slitting and stamping lines tailored for tab lead strips, with automated coil-feeding systems being commissioned in 2024. Industrial investment levels have increased through both state-backed funds and private capital focused on EV battery and energy storage sectors. Chinese firms are deploying battery tab lead material in applications ranging from cylindrical EV cells, prismatic power packs, and large grid storage modules. Technological advances include implementation of dry electrode processes and laser welding of tab leads to reduce connective resistance, as well as integration of in-line ultrasonic cleaning and automated optical inspection to improve product quality.

Key industry sectors for the Battery Tab Lead Market include automotive (EVs & hybrids), energy storage systems (ESS), consumer electronics (such as smartphones, laptops), and industrial backup/battery banks. Automotive applications contribute the majority due to high demand for cylindrical and prismatic cell tab leads, followed by ESS which is growing rapidly owing to grid and renewable energy storage adoption. Technological innovations are impacting the market: the shift toward dry electrode coating for improved uniformity and reduced solvent use; adoption of laser-cutting and laser welding techniques for precision tab shaping; in-line vision-based inspection systems detecting micro-defects in tab lead welds; and digital twin modelling to optimize fabrication, slitting, stamping, and forming processes. On the regulatory front, increasing environmental regulations limit solvent emissions, impose stricter lead handling and disposal rules, and demand life-cycle assessments. Economically, rising raw material (lead) and energy costs are pushing manufacturers toward efficiency improvements and waste minimization. Regionally, Asia-Pacific remains the largest consumer (especially China, South Korea, Japan), followed by North America and Europe; consumption patterns show strong uptake in EV battery tab lead demand in China, while Europe’s consumption is driven more by ESS and regulatory push toward clean energy storage. Emerging trends include materials innovation (e.g. alternatives to pure lead alloys for improved conductivity and lower corrosion), modular manufacturing lines which allow rapid changeover for different cell formats, and increasing use of automation throughout the production chain. The future outlook sees further investments in R&D, tighter environmental compliance, and more collaborative partnerships between equipment makers, material suppliers, and battery manufacturers.

Artificial Intelligence (AI) is becoming a core enabler in the Battery Tab Lead Market, fundamentally reshaping manufacturing, quality control, and operational efficiency for cell makers and equipment providers. AI-driven defect detection systems are now able to identify subsurface or microscopic weld anomalies in tab-lead joints that were previously undetectable using traditional visual inspections. This has reduced scrap rates in tab welding operations by over 25% in some Chinese production lines employing machine-vision combined with deep learning models. In the area of process optimization, AI models are being used to continuously monitor real-time data streams — for example, measuring temperature gradients, electrode lead thickness, lead strip alignment, and welding current — and adjust parameters on the fly to ensure uniformity in tab faces and weld integrity. Equipment downtime is being minimized via predictive maintenance algorithms that analyze vibration, acoustic, and current signature data to forecast failures in tab lead slitting or stamping presses before breakdowns occur. Energy consumption is also optimized with AI controlling heating and cooling cycles for dry electrode and forming operations, resulting in lower energy usage in critical tab lead processes. Additionally, supply chain optimization for raw lead alloys is being improved using AI forecasting (demand, material pricing volatility) and logistics scheduling. Overall, the Battery Tab Lead Market is becoming more data-driven, with AI enabling tighter process control, improved yield rates, lower waste, and much greater operational transparency—benefits crucial for decision-makers navigating rising input costs and environmental regulation.

“In 2025, Wuxi LEAD Intelligent Equipment implemented its AI-powered vision inspection system in its battery tab lead weld line, achieving a defect detection accuracy exceeding 99.2% and reducing weld rework by approximately 35%.”

The overall market dynamics specific to the keyword Battery Tab Lead Market reflect accelerating technological complexity, stricter environmental oversight, rising input costs, and shifting consumption patterns. Demand drivers from EVs, grid storage, consumer electronics, and industrial backup systems are combining, putting pressure on manufacturers to optimize production processes, reduce waste, and deliver consistently high quality in tab leads. Production capacity expansions are being matched by investments in automation, AI, and advanced inspection technologies. At the same time, regulatory pressure on lead use, lead emissions, workplace safety, and disposal is forcing product innovation and materials substitution. Supply-side influences include lead alloy raw material availability, energy costs (especially electricity), labor availability of skilled operators, and capital expenditures for equipment upgrades. Decision-makers must balance investments in process performance improvements (e.g. welding, stamping, slitting accuracy) with margins under pressure from input cost inflation and environmental compliance costs.

Growing adoption of electric vehicles and large-scale battery storage in grid applications is driving demand for high-quality, high-conductivity battery tab leads. In vehicle battery packs, tab leads play critical roles in interconnecting cells for current flow and thermal dissipation. As EV models proliferate, manufacturers are specifying more rigorous standards for tab lead thickness, material purity, and weld quality. In energy storage systems, longer cycle life, safety, and efficiency require better tab materials and precise welding, putting pressure on manufacturers to invest in new equipment. For example, several cell-producers have reduced internal resistance by specifying laser-welded tab leads with sub-10 micron weld seam misalignment, improving power performance and thermal management in packs. These technical requirements raise the profile of tab lead quality and drive capital investment from both OEMs and equipment suppliers.

Lead is a toxic heavy metal; regulatory regimes in Europe, North America, and parts of Asia require strict handling, emissions control, recycling, and disposal of lead and lead oxide containing components. Compliance with these environmental regulations necessitates investment in emission control systems (like fume hoods, scrubbers), worker safety systems, continuous monitoring, and recycling infrastructure. These impose increased cost burdens on Battery Tab Lead Market participants. In addition, public health concerns lead to restrictions or bans in certain jurisdictions, which increase legal risk, complicate supply chain logistics, and sometimes force redesign or substitution of materials. Furthermore, volatility in raw lead alloy supply due to geopolitical or trade-restrictions can lead to material shortages or sharp cost increases, influencing production scheduling and capital investment decisions.

There is growing opportunity in developing alternative lead alloys (or lead-composite materials) that maintain required conductivity, mechanical strength, and corrosion resistance, while using less pure lead or substituting with less toxic additives. Novel coatings and surface treatments to reduce oxidation, improve weldability, and improve contact resistance are being tested. Also, integration of dry electrode technology in the early electrode/tab lead interface offers opportunity for reduced solvent use and faster processing. Equipment manufacturers are exploring modular tab lead forming tools which can switch between formats (e.g., cylindrical, prismatic, pouch) with minimal tooling changeover time. Process innovations like laser-cut tab edges and in-line optical measurement create opportunity to reduce scrap and ensure tighter tolerances, which is especially valuable in sectors like EVs and ESS.

Manufacturing high-precision tab leads involves expensive tooling, tight tolerances, and complex welding or joining operations. Factors like laser-weld setup costs, precision stamping dies, slitting tools, and the necessity for ultra-clean environments add both capital cost and operational complexity. Achieving consistent weld integrity across large batches—especially with varying lead alloy formulations and changing humidity/temperature conditions—is technically challenging. Small misalignments can degrade electrical performance, heat management, and long-term reliability of battery packs. For many players, maintaining these precise tolerances while keeping production costs manageable is a critical hurdle. Skilled labor shortages, or securing engineers capable of implementing advanced automation and inspection systems, also constrain rapid scale-up.

Increasing Use of Vision-Based Micro-defect Detection Systems: Manufacturers in China have begun deploying AI-enhanced vision systems capable of identifying weld micro-cracks, misalignments, and microscopic burrs on tab lead welds—such systems are delivering defect detection rates above 99% and rework reductions of over 30%.

Adoption of Dry Electrode and Solvent-less Process Technologies: To meet stricter environmental regulations and reduce emissions and operational hazards, dry electrode coating processes are replacing wet solvent-based systems. These methods eliminate volatile organic solvent use and improve stability of lead-to-electrode interfaces, leading to more uniform tab lead bonding and reduced safety risk.

Modular Forming and Universal Tooling for Multiple Cell Formats: Equipment makers are designing stamping, slitting, and forming tools that can be rapidly reconfigured to produce tab leads for various battery cell formats (cylindrical, prismatic, pouch) with minimal changeover time. This allows manufacturers to serve EV, ESS, and consumer electronics clients with shared tooling, reducing capital expenditure per unit variation.

Embedded Sustainability Criteria in Production Processes: Companies are integrating energy-efficient motors, AI-controlled heating and drying stages, and on-site renewable power generation in tab lead fabrication. For example, Chinese firms are feeding 50% of operational electricity from photovoltaic systems into their battery equipment facilities; precision in drying/coating stages is reducing energy waste by over 60% in key unit operations.

The segmentation of the Global Battery Tab Lead Market provides crucial insights into the structural dynamics shaping industry development. The market is broadly divided by type, application, and end-user categories, each reflecting unique demand patterns and technological advancements. By type, the market includes aluminum tab leads, nickel tab leads, copper tab leads, and composite tab materials, each offering distinct conductivity, mechanical strength, and cost advantages. By application, the market spans electric vehicles, energy storage systems, consumer electronics, and industrial batteries, with EV adoption representing the primary growth engine. From the end-user perspective, automotive manufacturers, electronics producers, and renewable energy operators dominate consumption, with increasing demand from industrial and backup power sectors. This segmentation highlights how shifts in material innovation, regional manufacturing policies, and downstream consumption trends collectively influence both current demand and future growth directions in the Battery Tab Lead Market.

Within the Battery Tab Lead Market, aluminum tab leads dominate as the leading type, owing to their lightweight structure, corrosion resistance, and high suitability for large-format lithium-ion batteries, particularly in electric vehicles. Their role in enhancing thermal management and enabling faster charging cycles has made them the preferred choice for high-capacity energy storage applications. Nickel tab leads are recognized as the fastest-growing type due to their superior conductivity and strength, which support increasing demand in both prismatic and cylindrical battery cells. These properties make nickel tab leads critical in applications requiring durability under high current loads, such as advanced EV powertrains and industrial energy storage units. Copper tab leads, though costlier, serve niche high-performance applications where ultra-low resistance is vital, particularly in high-drain consumer electronics and specialized automotive batteries. Composite tab materials, blending performance attributes of multiple metals, are gradually emerging as alternatives for manufacturers prioritizing customized conductivity and mechanical flexibility. Collectively, this product diversity underscores the vital role of type-specific innovations in shaping the global market.

The electric vehicle (EV) sector remains the largest application area in the Battery Tab Lead Market, driven by mass adoption of lithium-ion batteries in passenger cars, commercial fleets, and hybrid vehicles. The demand for tab leads with superior durability, conductivity, and precise weldability aligns directly with the technical requirements of modern EV powertrains. The fastest-growing application is energy storage systems (ESS), supported by accelerating global investments in renewable energy integration and smart grid development. ESS applications require tab leads with enhanced cycle life and stable conductivity to ensure consistent performance over extended operational lifetimes, especially in grid-scale deployments. Consumer electronics, including smartphones, laptops, and wearables, continue to contribute significantly, although growth is comparatively moderate due to market maturity. Industrial batteries for backup power, telecommunication, and heavy machinery represent a specialized segment where reliability and safety standards drive consistent tab lead demand. Together, these applications highlight the widespread and evolving utility of battery tab leads across industries.

Among end-users, the automotive industry is the leading consumer in the Battery Tab Lead Market, supported by aggressive electrification targets and scaling production capacities of EV manufacturers. The automotive sector’s demand is amplified by large-scale gigafactory investments and the adoption of advanced welding technologies ensuring high-performance tab lead integration. The fastest-growing end-user segment is the renewable energy and grid storage sector, which increasingly requires long-lasting, high-efficiency tab leads to support large-scale energy storage projects. This demand is fueled by global energy transition strategies and government-backed programs promoting solar, wind, and hybrid energy integration. Electronics manufacturers remain steady contributors, utilizing tab leads for compact, high-density batteries in mobile devices and computing equipment. Industrial operators, particularly those in telecommunications, mining, and backup energy systems, also rely on durable tab leads to maintain uninterrupted operations. Together, these end-user dynamics emphasize the strategic importance of aligning material and process innovations with the specific needs of each consuming sector.

Asia-Pacific accounted for the largest market share at 58% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 12.5% between 2025 and 2032.

The Asia-Pacific region benefits from extensive manufacturing capacity and large-scale adoption in electric vehicles and energy storage projects, while North America is accelerating through substantial government-backed clean energy programs, advanced R&D hubs, and rapid adoption of digitalized production systems. Europe maintains strong demand driven by sustainability regulations and innovation in green mobility, while South America and the Middle East & Africa show promising growth linked to renewable infrastructure and industrial diversification initiatives.

North America held approximately 20% market share in 2024, underpinned by rapid expansion of electric vehicle infrastructure and grid-level energy storage deployments. The United States and Canada are leading demand, supported by automotive OEMs scaling production of EV batteries. Government initiatives such as subsidies for clean energy adoption and tax credits for EV manufacturing provide a robust regulatory foundation. Technological advancements include deployment of AI-based inspection systems and automation in tab lead welding, improving efficiency and reducing defect rates. Digital transformation trends such as digital twins and predictive maintenance tools are being integrated in battery production facilities, enabling consistent quality assurance and enhancing operational performance across the Battery Tab Lead Market.

Europe accounted for nearly 16% of the market share in 2024, with Germany, the United Kingdom, and France representing the largest demand hubs. The European Union’s sustainability initiatives, particularly the Green Deal and battery passport regulations, are shaping material use and recycling practices. The region’s manufacturers are heavily investing in environmentally friendly processes, including solvent-free electrode bonding and recyclable lead-alloy alternatives. Technological adoption is notable in Germany, where precision automation and Industry 4.0 practices are integrated into battery tab lead production lines. The United Kingdom and France are also strengthening research in advanced welding techniques and tab coating technologies to improve conductivity and efficiency within the Battery Tab Lead Market.

Asia-Pacific recorded the largest market volume globally in 2024, with China, Japan, and India as the top consuming countries. China leads in large-scale EV battery manufacturing capacity, while Japan maintains a strong presence in high-performance consumer electronics. India is emerging with substantial investments in localized battery production plants aligned with national clean energy targets. The region’s infrastructure growth includes mega-factories with integrated AI-enabled tab lead manufacturing lines and automated inspection systems. Innovation hubs in South Korea and Japan are advancing material research, particularly in low-resistance alloy designs. This regional ecosystem of scale, innovation, and policy support cements Asia-Pacific’s leadership in the Battery Tab Lead Market.

South America represented around 4% of global market share in 2024, with Brazil and Argentina as the most significant contributors. Brazil’s energy diversification strategy, including solar and wind integration, is fueling demand for grid-scale battery storage systems, thereby boosting the need for battery tab leads. Argentina is supporting domestic EV adoption with incentives that drive local assembly and component demand. Infrastructure development projects, particularly renewable energy installations, are reinforcing market momentum. Government trade policies encouraging technology partnerships with international players are creating favorable conditions for advancing tab lead production and application across the South American Battery Tab Lead Market.

The Middle East & Africa accounted for about 2% of global market share in 2024, with the United Arab Emirates and South Africa being the leading countries. Demand stems from diversification into clean energy, with solar and hybrid grid systems requiring advanced battery storage solutions. The UAE is investing in digitalized gigafactories with precision tab lead fabrication, while South Africa is focusing on backup power solutions for industrial and residential sectors. Technological modernization includes automation and AI-supported quality monitoring systems in regional facilities. Local regulations encouraging renewable adoption and trade partnerships with Asian equipment suppliers further support the growth of the Battery Tab Lead Market in this region.

China – 42% Market Share

High production capacity supported by large-scale EV and ESS battery manufacturing plants.

United States – 15% Market Share

Strong end-user demand driven by EV adoption and government-backed clean energy incentives.

The competitive environment in the Battery Tab Lead Market is highly dynamic, featuring over 30 active global competitors that vary in scale, specialization, and regional presence. Leading players are investing heavily in advanced manufacturing technologies, including automated welding systems, AI-powered quality inspection, and precision slitting processes to enhance product reliability and efficiency. Strategic initiatives such as partnerships with battery manufacturers, joint ventures in energy storage projects, and targeted product launches are prevalent, allowing firms to strengthen market positioning and expand geographic reach. Mergers and acquisitions are also shaping the competitive landscape, enabling companies to consolidate technological capabilities and optimize supply chains. Innovation trends include the development of low-resistance alloys, modular tab lead designs, and dry electrode-compatible tab leads, which provide operational efficiency and improved electrical performance. Regional specialization is evident, with Asia-Pacific dominating production volume while North America and Europe focus on advanced process automation, sustainability compliance, and high-performance product offerings. The combination of technological investment, strategic alliances, and process innovation is fostering a highly competitive environment that continuously elevates market standards.

Furukawa Electric Co., Ltd.

Hitachi Metals, Ltd.

JX Nippon Mining & Metals Corporation

Wuxi Lead Intelligent Equipment Co., Ltd.

Advanced Battery Technologies, Inc.

Shenzhen BAK Battery Co., Ltd.

Quallion LLC

Matsushita Battery Industrial Co., Ltd.

Ningbo Ronbay New Energy Technology Co., Ltd.

Korea Battery Materials Co., Ltd.

Technological advancement is a core driver in the Battery Tab Lead Market, focusing on enhancing conductivity, weld strength, and manufacturing precision. Laser welding technologies are increasingly employed to achieve uniform, low-resistance connections between tab leads and battery electrodes, reducing electrical losses and improving thermal stability. AI-powered vision inspection systems are integrated into production lines to detect micro-defects, misalignments, and burrs, with defect detection accuracy exceeding 99% in leading facilities. Automated slitting, stamping, and forming machines improve operational throughput while maintaining dimensional precision for multiple battery formats, including cylindrical, prismatic, and pouch cells. Emerging dry electrode-compatible tab leads minimize solvent use and streamline electrode integration, aligning with environmental regulations and energy efficiency goals. Digital twin simulations are being applied to optimize welding parameters, tab thickness, and assembly sequences, enhancing performance predictability and reducing material waste. Additionally, the market is exploring composite and coated lead alloys that combine corrosion resistance, high conductivity, and mechanical strength for long-cycle applications. Collectively, these technologies are elevating product reliability, operational efficiency, and sustainability within the Battery Tab Lead Market, making them central to competitive advantage.

In March 2023, Wuxi Lead Intelligent Equipment launched an automated tab lead laser welding line for EV batteries, achieving defect reduction of 30% and enhancing production throughput by 18% through integrated AI inspection systems.

In August 2023, Hitachi Metals introduced a high-conductivity nickel tab lead variant designed for high-power industrial storage batteries, improving current handling and thermal stability for large-format prismatic cells.

In February 2024, JX Nippon Mining & Metals commissioned a modular tab lead fabrication line capable of producing multiple battery formats with rapid tooling changeover, supporting both automotive and energy storage applications.

In November 2024, Furukawa Electric implemented AI-driven predictive maintenance on its tab lead stamping machines, reducing unplanned downtime by 25% and optimizing operational scheduling across multiple production sites.

The Battery Tab Lead Market Report covers a comprehensive analysis of product types, applications, and end-user segments across global regions. Types include aluminum, nickel, copper, and composite tab leads, addressing various performance and durability requirements. Applications span electric vehicles, energy storage systems, consumer electronics, and industrial batteries, with insights into material suitability and technological integration for each segment. The report examines end-user adoption across automotive OEMs, electronics manufacturers, renewable energy operators, and industrial battery providers, emphasizing operational needs, production scale, and application-specific standards. Geographic coverage encompasses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional consumption patterns, manufacturing trends, and infrastructure development. Technology-focused insights address laser welding, AI inspection, dry electrode integration, digital twins, and advanced alloy design. Emerging and niche market segments, including hybrid composites and modular manufacturing solutions, are explored to illustrate innovation-driven opportunities. This scope provides decision-makers with a structured understanding of production processes, material innovations, market dynamics, and strategic positioning in the Battery Tab Lead Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 841 Million |

| Market Revenue (2032) | USD 1,938.1 Million |

| CAGR (2025–2032) | 11.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Furukawa Electric Co., Ltd., Hitachi Metals, Ltd., JX Nippon Mining & Metals Corporation, Wuxi Lead Intelligent Equipment Co., Ltd., Advanced Battery Technologies, Inc., Shenzhen BAK Battery Co., Ltd., Quallion LLC, Matsushita Battery Industrial Co., Ltd., Ningbo Ronbay New Energy Technology Co., Ltd., Korea Battery Materials Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |