Reports

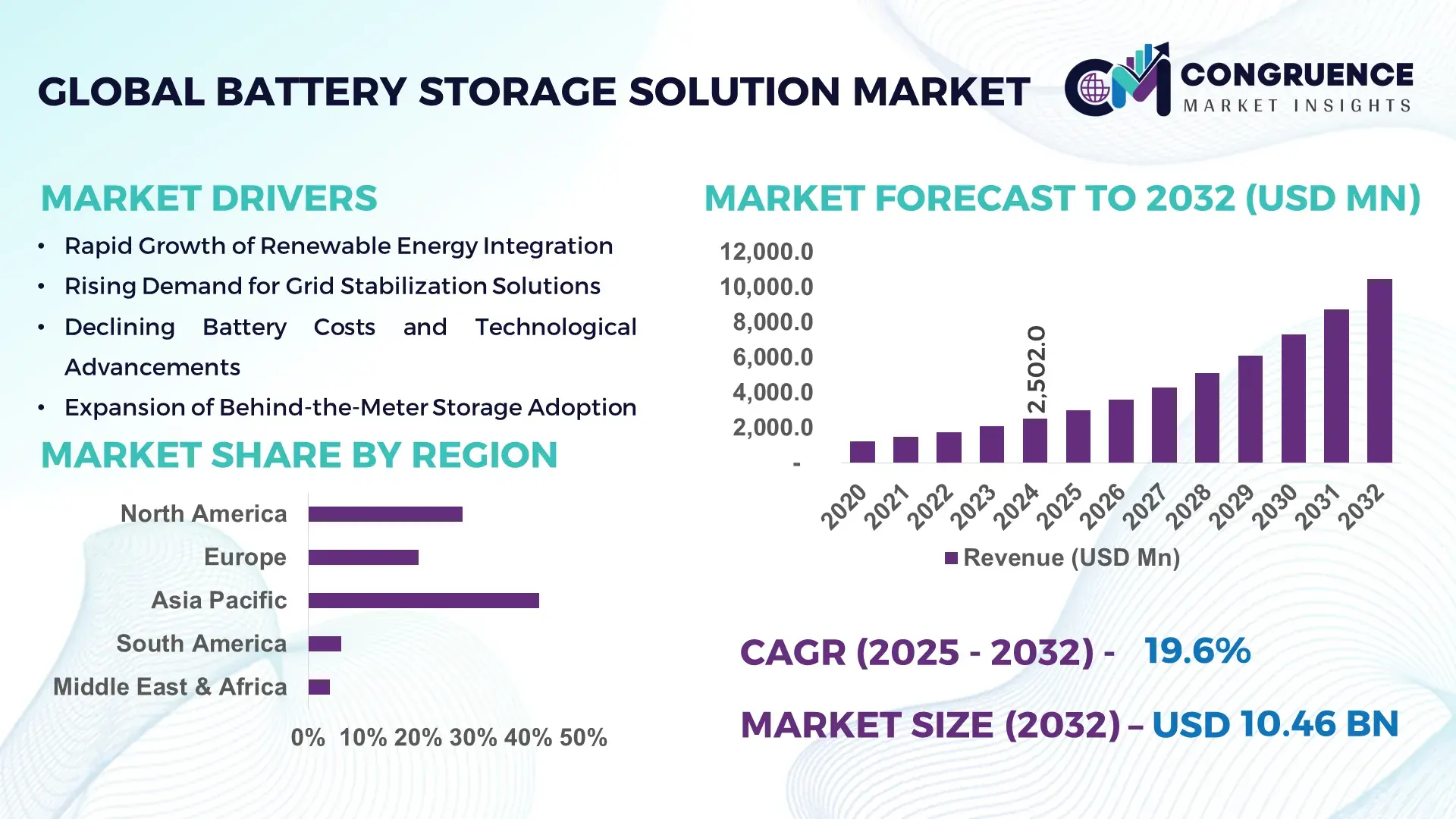

The Global Battery Storage Solution Market was valued at USD 2,502.0 Million in 2024 and is anticipated to reach a value of USD 10,460.6 Million by 2032, expanding at a CAGR of 19.58% between 2025 and 2032, according to an analysis by Congruence Market Insights. This surge is primarily driven by growing renewable energy integration and the need for grid stability.

China leads the global battery storage solution market with over 28 GW of annual utility-scale deployments in 2024 and more than USD 14 billion in investment into domestic BESS manufacturing capacity. The country’s rapid urbanization and heavy investments in modular containerised BESS systems contributed to more than 45% of new grid-scale projects using such systems. In addition, behind-the-meter storage growth in Chinese cities reached nearly 18% of new residential units in 2024.

Market Size & Growth: Valued at USD 2,502 M in 2024, projected to reach USD 10,460.6 M by 2032, at a CAGR of 19.58%, driven by renewable energy adoption and energy‑market flexibility.

Top Growth Drivers: Renewable integration (≈ 45%), grid modernization (≈ 38%), and decreasing battery cell costs (≈ 32%).

Short-Term Forecast: By 2028, system-level round-trip efficiency is expected to improve by ~ 10% due to next‑gen power electronics.

Emerging Technologies: Sodium-ion batteries, AI-based energy-management systems, and modular containerised BESS architectures.

Regional Leaders: Asia-Pacific (~USD 4,200 M by 2032, due to industrial and grid-scale demand), North America (~USD 3,000 M with strong utility-scale adoption), Europe (~USD 2,800 M powered by energy storage mandates).

Consumer/End‑User Trends: Utilities, C&I (commercial & industrial) firms, and residential users are increasingly deploying behind-the-meter storage for self-consumption and demand-charge management.

Pilot or Case Example: In 2023, a utility-scale pilot in China installed a 300 MWh BESS container, reducing curtailment of solar generation by 25%.

Competitive Landscape: Major players include CATL (~25% of global module capacity), BYD, LG Energy Solution, Tesla, and Fluence.

Regulatory & ESG Impact: Governments across Europe, U.S., and China are incentivizing BESS through capacity auctions, tax credits, and long-term procurement to meet net-zero targets.

Investment & Funding Patterns: Over USD 14 billion of BESS manufacturing investments announced in China alone in 2024, along with growing utility-scale project financing in Europe and North America.

Innovation & Future Outlook: Integration of AI-driven energy management, hybrid BESS (sodium-ion/lithium-ion), and containerised systems is positioning on‑site storage as a backbone for future grid resilience.

In recent years, commercial and industrial (C&I) sectors have increasingly adopted behind‑the‑meter battery storage to manage peak power costs and enhance grid resilience. Modular BESS units and intelligent energy-management software are accelerating deployments, while policy-driven storage tenders and declining cell costs are making large-scale storage economically viable.

The Battery Storage Solution Market is strategically vital as it provides resilience, flexibility, and dispatchability in an increasingly renewable-powered energy system. With wind and solar generation penetrating grids, storage solutions bridge supply‑demand mismatches by enabling load shifting, frequency regulation, and ancillary services. For example, sodium-ion battery systems deliver up to 15% cost savings compared to conventional lithium-ion, making them increasingly attractive for large-scale deployments.

Regionally, Asia-Pacific dominates in deployment volume, fueled by China and India’s massive utility-scale BESS buildout, while North America leads in third-party owned storage adoption, especially through capacity markets and renewables-plus-storage projects. In the short term, by 2027, AI-enabled energy‑management systems are expected to improve BESS round-trip efficiency by ~12%, driving broader uptake in commercial and industrial (C&I) sites.

Aligning with ESG goals, firms are committing to 30% reductions in battery production emissions and increasing recycling rates of battery modules by 2030. A micro‑scenario: in 2024, a major U.S. developer deployed AI-based BESS controls across its portfolio and achieved 18% lower cycling costs compared to conventional BESS management strategies.

Looking ahead, the Battery Storage Solution Market will serve as a cornerstone of the clean energy economy, enabling not just grid stability but also providing revenue streams through market participation, virtual power plant (VPP) models, and behind-the-meter value stacking.

The Battery Storage Solution Market is being shaped by the accelerating integration of renewables, ambitious decarbonization targets, and evolving power market designs. As grids across regions modernize, storage is no longer a niche backup asset — it becomes a core infrastructure component for balancing intermittency, providing fast frequency response, and enabling flexible dispatch. Falling battery system costs are making behind-the-meter (residential and commercial) installations more viable, while utility-scale storage is being increasingly bundled with solar and wind projects. Meanwhile, technological innovation is creating more modular, scalable, and managed solutions, reducing both upfront CAPEX and OPEX. Policy support, including auctions, tax incentives, and energy‑storage procurement mechanisms, further underpins sustained investment flow.

Rapid growth in wind and solar capacity globally is the strongest driver. As intermittent renewable energy sources come online, grid operators and utilities need flexible storage to absorb excess generation and stabilize supply. In many markets, new solar projects are being paired with BESS installations, enabling developers to bid into capacity markets, deliver firm power, and capture additional revenue streams. The declining cost of battery storage — especially lithium-ion and emerging sodium-ion chemistries — is making such paired deployment economically attractive. Industrial and commercial consumers are also adopting storage to manage peak power demand and reduce grid charges.

Despite significant cost declines, the capital cost associated with battery storage systems remains substantial — especially for utility-scale deployments. For many projects, CAPEX can still account for 40–60% of total project cost. In addition, technical complexity in integrating BESS with grid infrastructure (inverters, control systems) raises engineering and installation costs. There is also operational risk: battery degradation over time, thermal management, and efficiency losses require specialized maintenance. These factors can limit adoption in regions where financing is constrained or tariff incentives are limited.

Behind‑the‑meter (BTM) and commercial & industrial (C&I) energy storage segments are emerging as highly attractive opportunities. These systems allow businesses to reduce demand charges, participate in demand response programs, and optimize self-consumption of on-site solar. In many markets, C&I users are negotiating “storage as a service” contracts, reducing upfront capital burden. As energy tariffs vary and time-of-use pricing becomes more common, BTM BESS becomes a strategic hedge against peak prices. Additionally, virtual power plant (VPP) aggregation of multiple small-scale BESS units is unlocking new revenue streams in capacity and ancillary markets.

Regulatory frameworks for energy storage remain inconsistent across regions, creating uncertainty for developers and investors. In many markets, storage is not yet fully classified — sometimes treated as generation, sometimes as demand, which complicates permitting, interconnection, and revenue modeling. Lack of clear market rules for storage services (frequency regulation, capacity markets) can disincentivize investment. Furthermore, in certain jurisdictions, storage faces double charging (i.e., being charged grid fees both when importing and exporting), reducing economic appeal. This regulatory risk slows deployment and can limit financing options.

Modular and Containerised Deployment: A growing share of new utility-scale BESS projects use modular containerised systems — around 45% of new grid-scale installations in 2024 — allowing flexible capacity scaling and reducing installation timelines by over 20%.

Emergence of Sodium‑Ion Cells: Sodium-ion batteries are gaining traction, especially for grid-scale applications, thanks to lower raw-material costs and stable performance; recent factory announcements target more than 24 GW of capacity.

AI-Driven Energy Management: Over 30% of new commercial BESS deployments now include AI-based control systems, enabling predictive maintenance and optimizing charge/discharge cycles, lowering operational costs by an estimated 15%.

Declining System Costs: Average system-level costs for BESS have dropped by nearly 35% between 2022 and 2024, driven by reductions in cell prices and improvements in pack integration and power electronics.

The Battery Storage Solution Market is structured across multiple segments, including types, applications, and end-user groups, each reflecting unique deployment strategies and value propositions. By type, the market encompasses lithium-ion batteries, lead-acid batteries, sodium-ion batteries, and flow batteries, with lithium-ion systems dominating due to their energy density, modular scalability, and suitability for both utility-scale and behind-the-meter applications. Application-wise, the market spans utility-scale storage, commercial & industrial (C&I) projects, and residential energy storage, with utility-scale installations currently accounting for the largest portion owing to large solar and wind integration projects. End-user segmentation includes utilities, commercial & industrial operators, and residential consumers, reflecting diverse adoption drivers such as demand-charge management, grid stability, and renewable self-consumption. Together, these segments enable tailored deployment strategies and allow stakeholders to address both efficiency and cost-effectiveness, while ongoing technological advances are reshaping adoption patterns globally.

Lithium-ion batteries currently account for approximately 62% of adoption, owing to high energy density, long cycle life, and modular deployment capability. Sodium-ion batteries are emerging rapidly, capturing attention due to lower raw material costs and environmental advantages, with adoption expected to accelerate in grid-scale projects. Lead-acid batteries maintain relevance in cost-sensitive small-scale applications, representing about 18% of the market, while flow batteries contribute around 10% in niche utility-scale and long-duration storage scenarios. Collectively, these remaining types make up approximately 28% of total installations, serving specialized operational or economic needs.

Utility-scale storage dominates the market with roughly 55% of total deployment, driven by the integration of large solar and wind farms, providing grid stabilization and ancillary services. Behind-the-meter solutions for commercial and industrial (C&I) applications currently account for 30%, facilitating demand-charge reduction, renewable self-consumption, and participation in demand response programs. Residential energy storage makes up the remaining 15%, serving rooftop solar users and microgrid applications. Adoption of C&I storage is rising fastest, fueled by cost savings, tariff arbitrage opportunities, and corporate sustainability initiatives.

Utilities are the leading end-user segment, accounting for approximately 60% of total installations, primarily to stabilize the grid and manage renewable energy intermittency. Commercial and industrial (C&I) operators represent 28% of installations, experiencing rapid growth due to energy cost optimization and participation in grid service markets. Residential users constitute the remaining 12%, largely adopting battery storage for solar self-consumption and resilience during outages. Among C&I adopters, sectors such as data centers, manufacturing, and healthcare have adoption rates exceeding 35–40%, reflecting targeted efficiency and reliability benefits.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 21.5% between 2025 and 2032.

Asia-Pacific leads due to massive adoption in China, India, and Japan, with over 1,200 MW of utility-scale projects and 450,000 residential storage units deployed in 2024. North America follows closely with approx. 28% of global installations, driven by energy storage mandates and integration with large-scale solar farms. Europe holds 20% market share, led by Germany, UK, and France, where over 60% of new renewable projects include storage solutions. South America and MEA together account for 10%, with Brazil and UAE leading regional adoption. Strong government incentives, grid modernization projects, and increasing renewable energy capacity are key drivers shaping these regional deployment patterns.

North America holds 28% of global battery storage installations, with significant demand from utilities, healthcare, and finance sectors. Federal and state incentives, such as investment tax credits and grid modernization programs, have facilitated deployment of over 500 MW of new storage capacity in 2024 alone. Technological advancements include AI-driven energy management and integration of lithium-ion and flow batteries in large commercial projects. AES Energy Storage deployed a 100 MW/400 MWh battery project in Texas, enhancing grid resilience and peak shaving. North American consumers exhibit higher adoption of behind-the-meter solutions, particularly in commercial and residential sectors, supporting sustainability goals and operational reliability.

Europe represents 20% of the global battery storage market, with Germany, the UK, and France as leading adopters. The EU Green Deal and national renewable mandates are accelerating deployments, with over 300 MW of utility-scale and 120,000 residential systems installed in 2024. Companies are integrating smart grid technology, vehicle-to-grid systems, and AI-based energy management platforms. Siemens Energy implemented a 50 MWh storage solution in Germany, optimizing grid balancing for industrial zones. Consumer behavior shows strong preference for environmentally compliant and modular storage solutions, influenced by regulatory pressures and sustainability incentives.

Asia-Pacific leads globally with 42% market share, primarily fueled by China, India, and Japan. The region deployed over 1,200 MW of utility-scale storage and 450,000 residential units in 2024, integrating with solar and wind infrastructure. Technological innovation hubs in Shenzhen and Tokyo focus on high-capacity lithium-ion and sodium-ion battery production. BYD installed a 200 MWh storage system in China, supporting grid stability for a metropolitan solar project. Consumer behavior trends show rapid adoption in e-commerce, mobile energy apps, and renewable self-consumption solutions.

South America accounts for 6% of the global battery storage market, with Brazil and Argentina leading deployments. The region installed over 150 MW of new storage capacity in 2024, focused on supporting renewable energy integration and industrial electrification. Government incentives, including renewable energy credits and trade policies, have accelerated adoption. Engie Brasil launched a 50 MWh solar-coupled storage project, enhancing grid flexibility. Regional consumer trends indicate high adoption in urban commercial centers, with interest in media and language-specific energy management solutions.

MEA represents 4% of the global market, driven by oil & gas, construction, and industrial sectors. Major contributors include UAE and South Africa, deploying over 80 MW of grid-scale battery systems in 2024. Technological modernization includes integration of hybrid solar-storage plants and smart energy management systems. ACWA Power installed a 25 MWh battery system in Saudi Arabia, supporting peak demand management. Consumers increasingly adopt storage solutions for commercial and industrial resilience, with growing interest in renewable integration and energy cost optimization.

China – 34% Market Share: High production capacity and integration with national renewable energy projects.

United States – 28% Market Share: Strong adoption in utility-scale and C&I sectors with robust government incentives.

The Global Battery Storage Solution Market is moderately consolidated, with around 20–25 major active competitors offering cell manufacturing, system integration, and energy‑management solutions. The top 5 firms—CATL, BYD, LG Energy Solution, Tesla, and Fluence—collectively account for approximately 55–60% of global BESS capacity. Players are differentiating through strategic partnerships, mergers, and product innovation: CATL is accelerating its sodium-ion grid-battery production; BYD is scaling up its “Cube” containerised systems globally; LG Energy Solution is expanding its LFP cell capacity with new gigafactories; Tesla continues to push its Megapack systems; and Fluence is enhancing its software platform for AI-enabled dispatch optimization.

Innovation trends are reshaping the competitive landscape. Many firms are launching hybrid BESS systems, combining lithium-ion with flow or sodium-ion chemistries to win long-duration applications. Others are integrating AI-driven energy-management software that can boost dispatch revenues by 15–25%. System integrators are investing in modular container designs, enabling flexibility and scalability. Meanwhile, companies are increasingly competing on lifecycle guarantees, remote diagnostics, and performance-as-a-service models, rather than just hardware. Strategic alliances are also deepening: major cell manufacturers partner with utilities or EPC firms, while developers offer fully integrated turnkey storage-plus-solar solutions. This mix of manufacturing scale, software sophistication, and strategic collaboration is solidifying the market’s structure and driving competitive intensity.

BYD Co., Ltd.

Fluence (Siemens / AES JV)

Samsung SDI

Panasonic Corporation

Technological innovation in battery storage is accelerating across both hardware and software domains. On the hardware side, sodium‑ion batteries are gaining traction, offering a lower-cost alternative to lithium-ion while still providing competitive cycle life and thermal stability, especially for utility-scale storage. Meanwhile, hybrid BESS systems—which combine lithium-ion with flow or solid-state technologies—are being piloted to provide both high power and long-duration storage, meeting diverse application needs from frequency regulation to peak shifting.

Battery management systems (BMS) have become more intelligent and predictive. Advanced BMS now use machine learning to optimize charge and discharge cycles dynamically, prolonging battery life and minimizing degradation. These systems also support real-time state-of-health (SoH) monitoring and thermal management, significantly improving safety and performance. Round-trip efficiency has improved due to innovations in power conversion electronics, with many systems now achieving above 90% efficiency under typical operating conditions.

Another important trend is the increasing adoption of modular, containerised storage. These systems allow energy providers to scale capacity more flexibly, deploy rapidly, and manage maintenance more easily—an advantage in both grid-scale and commercial settings. The modular BESS comes with plug-and-play power modules, making expansion or maintenance more cost-effective.

On the software side, AI-driven energy‑management platforms are being integrated into BESS operations. These platforms can forecast demand, optimize dispatch based on market signals, and align with utility needs, increasing utilization and earnings potential. Some system providers are offering “storage as a service”, where they manage performance and revenue on behalf of customers, reducing the technical burden on end-users.

Looking ahead, research into next-generation chemistries—such as solid-state and metal-air batteries—is underway, promising higher energy densities and improved safety. Simultaneously, grid architecture is evolving to leverage virtual power plants (VPPs), where distributed BESS units are aggregated to provide grid services, enabling storage to play a fundamental role in future power systems. These technological trajectories position the battery storage solution market for continued innovation, operational flexibility, and strategic differentiation.

In Q4 2023, Fluence Energy reported order intake of ~$1.1 billion, lifting its total order backlog to $3.7 billion. Source: www.fluenceenergy.com

By September 30, 2024, Fluence’s backlog further expanded to ~$4.5 billion, alongside a quarterly order intake of $1.2 billion and first full‑year profit. Source: www.fluenceenergy.com

In Q2 2024, Tesla Energy deployed 9.4 GWh of battery storage systems, its highest-ever quarterly storage deployment, more than doubling its prior record. Source: www.tesla.com

For full-year 2024, Tesla reported 31.4 GWh of energy storage deployments, a 114% year-over-year increase, boosted in part by US tax credits. Source: www.tesla.com

The Battery Storage Solution Market Report offers a comprehensive analysis across a broad spectrum of segments, geographies, and technology domains. The study breaks down the market by battery chemistry (lithium-ion, sodium-ion, flow, hybrid), system deployment formats (containerised, modular units, utility-scale, residential), and service models (turnkey systems, managed storage-as-a-service).

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level deep dives for top markets such as China, the U.S., Germany, and India. Application analysis spans utility-scale grid storage, commercial & industrial (C&I) behind-the-meter solutions, and residential storage, with insights into demand drivers, revenue models, and the role of hybrid systems in each use case.

The report further explores emerging technology trends, including AI-driven energy management, advanced BMS architectures, next-generation battery chemistries, and the deployment of virtual power plants (VPPs). It evaluates key industry use cases—such as frequency regulation, demand response, microgrids, and energy arbitrage—and assesses regulatory influences, ESG drivers, and investment flows.

Strategic insights include competitive benchmarking of leading players, partnerships and mergers, project pipeline analysis, financing trends, and market entry strategies. By combining technical, commercial, and policy perspectives, the report equips decision-makers with actionable intelligence to evaluate storage deployment, capitalize on growth opportunities, and plan long-term investments in the evolving BESS landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,502.0 Million |

| Market Revenue (2032) | USD 10,460.6 Million |

| CAGR (2025–2032) | 19.58% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Contemporary Amperex Technology Co., Limited (CATL), LG Energy Solution, Tesla, Inc., BYD Co., Ltd., Fluence (Siemens / AES JV), Samsung SDI, Panasonic Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |