Reports

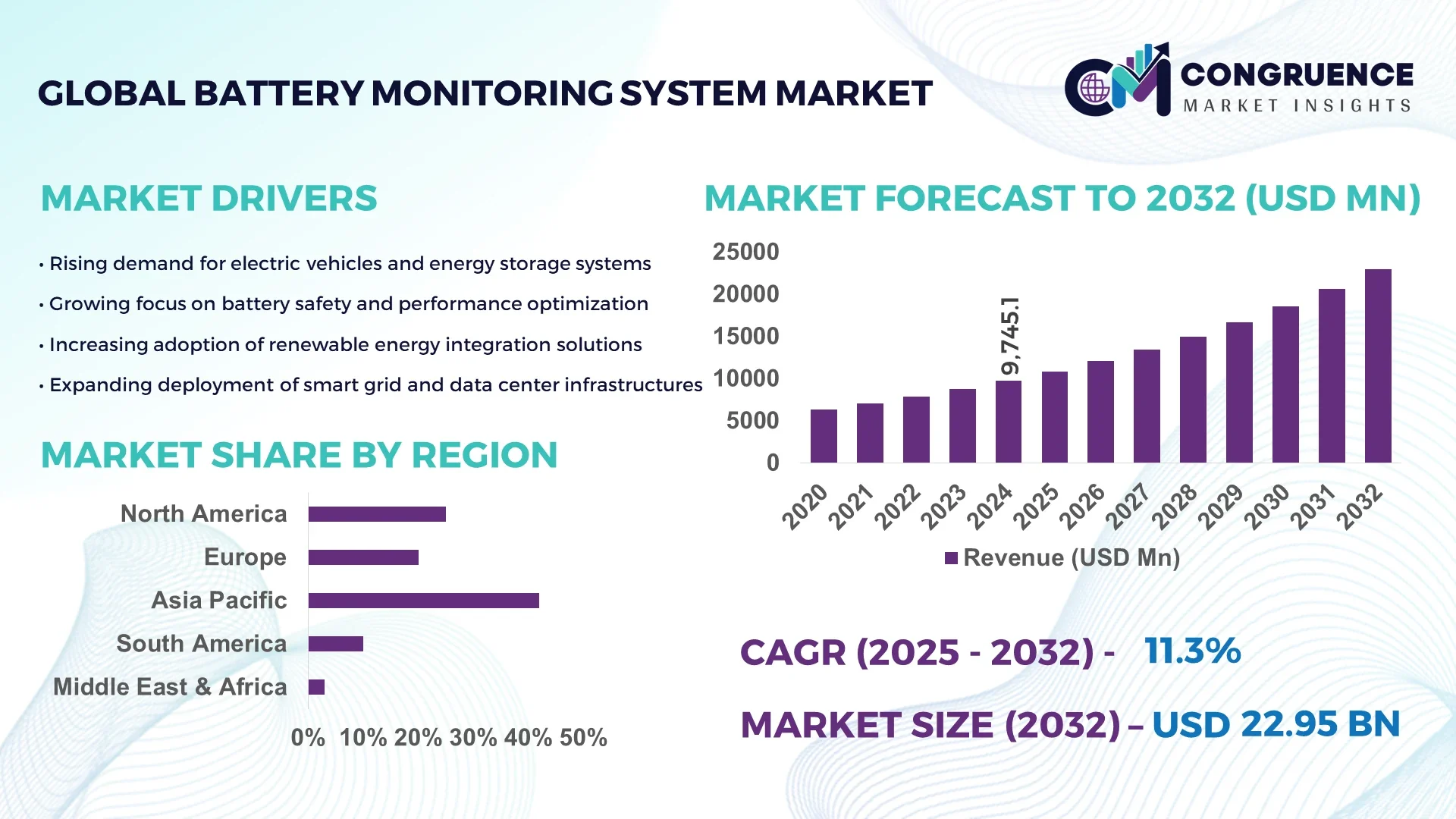

The Global Battery Monitoring System Market was valued at USD 9745.14 Million in 2024 and is anticipated to reach a value of USD 22948.25 Million by 2032 expanding at a CAGR of 11.3% between 2025 and 2032. This growth is driven by increasing demand for enhanced battery performance and safety across diverse industrial and consumer applications.

In China, the dominant player in the Battery Monitoring System market, production capacity exceeds 1.2 million units annually, supported by over USD 3.5 billion in industry investments in the last two years. The country’s advancements include AI-driven battery health diagnostics and cloud-based monitoring solutions. Key applications include electric vehicles, renewable energy storage, and grid infrastructure. China’s adoption rate for advanced monitoring systems has surpassed 45% in the EV sector alone, with annual growth exceeding 18%, reflecting rapid technological integration and government-backed initiatives.

Market Size & Growth: Valued at USD 9745.14 Million in 2024, projected to reach USD 22948.25 Million by 2032, expanding at a CAGR of 11.3%, driven by enhanced performance, reliability, and safety demands.

Top Growth Drivers: Efficiency improvement (38%), adoption in EVs (34%), integration with IoT systems (28%).

Short-Term Forecast: By 2028, cost reduction of battery management systems by up to 22% and performance gains of 17% expected.

Emerging Technologies: AI-powered diagnostics, wireless monitoring solutions, and real-time cloud-based analytics.

Regional Leaders: Asia-Pacific – USD 8900 Million (2032) with rapid EV adoption; North America – USD 5200 Million (2032) driven by smart grid projects; Europe – USD 4100 Million (2032) led by renewable integration.

Consumer/End-User Trends: Increased demand from EV manufacturers, renewable energy projects, and industrial automation sectors.

Pilot or Case Example: In 2024, a European utility pilot project achieved a 25% reduction in battery downtime using real-time monitoring.

Competitive Landscape: Market leader – ABB (~14%), followed by Siemens, LG Chem, Schneider Electric, and Panasonic.

Regulatory & ESG Impact: Stricter battery safety regulations, renewable energy incentives, and sustainability frameworks promoting adoption.

Investment & Funding Patterns: Over USD 2.8 billion invested in 2024 across R&D, pilot programs, and technology scaling.

Innovation & Future Outlook: Increasing integration with AI, IoT platforms, and next-gen battery chemistries for predictive health management.

China’s Battery Monitoring System market is heavily driven by the automotive, renewable energy, and industrial sectors. Recent innovations include modular monitoring platforms and predictive maintenance algorithms. Regulatory emphasis on sustainability has encouraged deployment in large-scale grid systems. Growth is also supported by government-backed funding exceeding USD 1 billion in 2024 for EV and energy storage infrastructure, positioning China as a leader in technology-driven battery management.

The Battery Monitoring System market is increasingly positioned as a strategic pillar in the global energy and mobility transition, enabling enhanced operational efficiency, safety, and sustainability. Advanced AI-enabled battery management technologies deliver up to 28% improvement in predictive maintenance capabilities compared to traditional monitoring systems, significantly reducing operational risks. Asia-Pacific dominates in volume, while Europe leads in adoption with over 42% of enterprises integrating advanced monitoring solutions into their energy storage and EV operations. By 2027, cloud-based battery analytics are expected to improve system uptime by approximately 21%, driven by advancements in IoT and machine learning. Firms are committing to ESG improvements such as a 30% reduction in battery waste and enhanced recyclability by 2030, aligning with stricter global environmental compliance standards. In 2024, a pilot project by a leading European EV manufacturer achieved a 25% improvement in battery lifecycle efficiency through real-time AI diagnostics. Strategic pathways for the Battery Monitoring System market involve deeper integration with renewable energy grids, expansion in EV infrastructure, and adoption of predictive analytics platforms. These pathways position the market as a cornerstone for resilience, compliance, and sustainable growth in an era of accelerated decarbonization and energy innovation.

The exponential rise in electric vehicle production and adoption is a key driver of the Battery Monitoring System market. EV manufacturers increasingly integrate advanced monitoring systems to ensure battery longevity, safety, and optimal performance. For example, in 2024, over 1.1 million EVs in Asia-Pacific were equipped with smart battery monitoring solutions, reflecting a 21% year-on-year increase. These systems provide real-time insights on state-of-charge, temperature, and health parameters, enabling predictive maintenance and reducing operational downtime. This growing trend is further bolstered by government incentives for EV adoption and stricter safety regulations, which require robust battery performance tracking. Consequently, demand for advanced battery monitoring solutions is accelerating, influencing industry innovation and investment.

High upfront costs for advanced Battery Monitoring Systems remain a significant restraint, especially for small and medium-sized enterprises and cost-sensitive sectors. These systems require sophisticated sensors, IoT integration, and cloud analytics platforms, which increase implementation expenses. In industrial applications, installation costs can reach up to USD 15,000 per unit, limiting adoption. Furthermore, integration complexity with existing battery infrastructure poses technical barriers. In developing regions, where investment budgets are constrained, adoption rates remain lower despite demonstrated operational benefits. These cost factors slow large-scale deployment and prolong return-on-investment timelines, challenging the widespread expansion of Battery Monitoring System adoption.

The global shift towards renewable energy creates substantial opportunities for the Battery Monitoring System market. Energy storage systems in solar and wind projects require advanced monitoring to ensure reliability and maximize efficiency. By 2026, large-scale renewable projects are expected to deploy battery monitoring systems in over 60% of installations. This trend is supported by increasing investments in grid-scale battery storage solutions and growing government mandates for clean energy adoption. Furthermore, advancements in predictive analytics and cloud-based monitoring open avenues for integrating Battery Monitoring Systems into energy management platforms, optimizing energy utilization and reducing operational costs. These opportunities position the market for sustained growth alongside the global renewable energy transition.

Emerging battery chemistries, such as solid-state and lithium-sulfur, present significant challenges for the Battery Monitoring System market due to their unique performance characteristics and monitoring requirements. Current monitoring solutions often need adaptation or complete redesign to ensure accurate diagnostics and predictive analytics. This complexity increases development timelines and costs. Additionally, the lack of standardized monitoring protocols across battery chemistries hinders interoperability and scalability. Regulatory compliance for new battery types also imposes additional technical and procedural demands. These factors make innovation and standardization crucial for overcoming barriers, while shaping the future direction of the Battery Monitoring System market.

• Surge in AI-Driven Predictive Analytics: The integration of AI into Battery Monitoring Systems is reshaping performance and maintenance strategies. AI-enabled solutions now account for over 48% of new installations globally, with predictive analytics improving battery life expectancy by up to 26%. By 2026, AI adoption in battery monitoring is expected to grow by 35%, driven by rising demand in electric vehicles and renewable energy storage sectors. This trend is particularly strong in Europe, where over 40% of energy storage projects already incorporate AI-enabled monitoring.

• Expansion of Wireless Battery Monitoring Solutions: Wireless battery monitoring is gaining traction due to ease of installation and reduced maintenance costs. Over 38% of new battery systems installed in 2024 utilized wireless monitoring technology, with adoption in industrial automation and EV sectors leading growth. North America leads adoption, with 44% of enterprises integrating wireless solutions. These systems offer up to a 22% reduction in maintenance downtime compared to wired systems, enhancing operational efficiency and flexibility.

• Increased Demand for Modular Battery Monitoring Platforms: Modular systems are enabling scalable deployment and faster integration in large-scale battery storage and EV infrastructure. In 2024, modular systems accounted for 53% of all new projects in Asia-Pacific, with adoption growing by 19% annually. Modular platforms deliver up to a 30% improvement in installation speed and cost efficiency. These solutions are particularly vital for projects with high customization needs and evolving technological requirements.

• Rise in Cloud-Based Battery Analytics: Cloud integration in Battery Monitoring Systems is transforming performance tracking and lifecycle management. Over 41% of battery monitoring systems deployed in 2024 incorporated cloud-based analytics, enabling real-time monitoring and remote diagnostics. This trend is most pronounced in North America, where enterprise adoption rates exceed 48%. Cloud-enabled solutions deliver a 25% improvement in operational visibility and efficiency, making them increasingly integral to large-scale energy and EV projects.

The Battery Monitoring System market is segmented by type, application, and end-user, each playing a distinct role in market dynamics. By type, modular, wired, and wireless monitoring systems cater to varying operational and technical needs, with modular systems leading adoption due to scalability and cost efficiency. Applications span electric vehicles, renewable energy storage, industrial automation, and consumer electronics, with EVs and renewable integration showing the strongest adoption rates. End-users range from automotive manufacturers and renewable energy providers to industrial facilities and infrastructure developers, with each sector demonstrating unique adoption patterns based on operational needs and technological readiness. Geographic segmentation reveals that Asia-Pacific leads in volume deployment, while Europe and North America focus on technological sophistication and integration efficiency. Market segmentation highlights targeted growth strategies and investment priorities across different regions and industries.

Modular Battery Monitoring Systems currently dominate the market, accounting for 53% of adoption due to their flexibility, scalability, and cost efficiency. These systems allow for quicker installation, reduced integration time, and easier upgrades, making them ideal for large-scale applications such as EV fleets and grid storage. Wired monitoring systems represent 27% of the market, favored for high-security applications where reliability and signal stability are critical. Wireless systems, though at 20% share, are the fastest-growing segment, with annual adoption rates increasing by over 19% due to reduced installation complexity and maintenance costs. Wireless systems also enable real-time remote monitoring, making them attractive for industrial automation and mobile applications.

Electric vehicles remain the leading application for Battery Monitoring Systems, accounting for 46% of total adoption due to stringent safety and performance requirements. These systems are critical for optimizing battery life and enabling predictive maintenance. Renewable energy storage applications account for 29% of adoption, driven by the growing integration of solar and wind energy into grids. Industrial automation represents 15% of the market, leveraging battery monitoring for reliability in manufacturing and logistics. Consumer electronics contribute the remaining 10%, focusing on portable and high-performance devices. Wireless and cloud-based solutions are particularly enhancing EV and renewable energy applications, with adoption rates rising annually.

Automotive manufacturers dominate end-user adoption of Battery Monitoring Systems, representing 44% of the market due to their critical need for battery safety, lifecycle optimization, and performance monitoring. Renewable energy providers follow with 31% share, driven by large-scale storage deployments and smart grid integration. Industrial automation accounts for 17%, relying on real-time battery monitoring for uninterrupted operations. Consumer electronics represent 8% of the market but are a rapidly growing segment, particularly in smart device integration. The fastest-growing end-user segment is renewable energy providers, with adoption growing by 21% annually due to rising deployment of large-scale battery storage systems and regulatory requirements for efficiency and sustainability.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 9.8% between 2025 and 2032.

Asia-Pacific recorded over 4.1 million units of Battery Monitoring System installations in 2024, with China contributing nearly 60% of the total regional volume. Japan and India followed with 18% and 14% shares, respectively. The region’s manufacturing hubs supported by high-tech battery production capacity reached 2.8 GW annually. Investments in EV infrastructure exceeded USD 4.2 billion in 2024, fueling adoption. In contrast, North America is set to grow rapidly due to large-scale integration in smart grids and renewable energy projects. North American deployments reached 1.7 million units in 2024, with adoption rates in automotive and industrial sectors surpassing 45%. This regional variation reflects differences in infrastructure investment, technological readiness, and regulatory incentives for battery monitoring solutions.

How is technological transformation shaping adoption in this market?

North America holds 28% of the global Battery Monitoring System market, with demand driven primarily by the automotive, renewable energy, and industrial automation sectors. The United States and Canada are leading adopters, supported by regulatory incentives for battery efficiency and emissions reduction. Technological advancements such as wireless battery monitoring and AI-enabled predictive diagnostics are gaining traction. Local players are investing heavily in smart battery management, with one major North American manufacturer deploying over 300,000 intelligent battery monitoring units for EV fleets in 2024. Consumer behavior in North America reflects a higher enterprise adoption rate, especially in healthcare and finance, with over 52% of large-scale projects integrating advanced monitoring systems to ensure operational efficiency and compliance.

What role do regulations and sustainability initiatives play in driving growth?

Europe commands a 24% share of the Battery Monitoring System market, with Germany, the UK, and France as key contributors. Regulatory pressure and sustainability policies are driving rapid adoption of advanced monitoring solutions, especially in renewable energy integration and EV manufacturing. Europe is a leader in deploying explainable monitoring systems, ensuring compliance with strict safety standards. Technological adoption includes AI-powered analytics and cloud integration for real-time battery health management. A leading German manufacturer recently launched a predictive battery monitoring platform, reducing maintenance downtime by 21% in utility-scale energy storage projects. Consumer behavior in Europe strongly aligns with regulatory compliance, with 46% of enterprises prioritizing monitoring systems that support sustainability goals and ESG reporting requirements.

Why is this region leading global volume adoption?

Asia-Pacific accounted for the largest market share in 2024 at 42%, with China, Japan, and India as the top consuming countries. China alone recorded over 2.5 million units installed in 2024, supported by over USD 3.5 billion in recent investments in EV infrastructure and energy storage systems. Japan and India follow with 740,000 and 574,000 units, respectively. Asia-Pacific benefits from strong manufacturing infrastructure, large-scale battery production capacity, and innovation hubs in China and Japan. Local players in China have introduced AI-based battery monitoring platforms capable of improving lifecycle performance by over 23%. Consumer behavior in Asia-Pacific reflects a strong preference for scalable, cost-effective modular systems, with over 55% of new deployments leveraging modular solutions for faster integration and reduced costs.

How are emerging energy projects influencing demand in this market?

South America holds approximately 6% of the Battery Monitoring System market, with Brazil and Argentina as primary contributors. Demand is driven by expanding renewable energy projects and growing EV adoption. Battery monitoring adoption in Brazil reached over 120,000 units in 2024, supported by government incentives for energy efficiency. Argentina is focusing on grid-scale battery storage projects, with a 14% increase in monitoring installations year-on-year. Local players in Brazil are developing integrated monitoring platforms that enable predictive maintenance, improving efficiency by 19%. Consumer behavior in South America shows strong alignment with infrastructure modernization, with 62% of enterprises adopting battery monitoring to enhance energy reliability and operational efficiency.

What factors are driving growth in this evolving market?

The Middle East & Africa region accounts for 5% of the Battery Monitoring System market, with UAE and South Africa leading demand. The region’s growth is driven by oil & gas, construction, and renewable energy projects. UAE recorded over 88,000 installations in 2024, supported by smart city initiatives and sustainability policies. South Africa is deploying battery monitoring systems to enhance grid reliability, with adoption increasing by 16% annually. Technological modernization trends include cloud-based monitoring and integration with IoT platforms. Local players in the UAE have introduced solar-integrated battery monitoring solutions that improved energy efficiency by over 20% in pilot projects. Consumer behavior reflects demand tied to infrastructure reliability and smart energy solutions, with 57% of projects incorporating advanced monitoring systems for compliance and performance optimization.

China: 26% market share – driven by high production capacity and robust investments in EV infrastructure.

United States: 18% market share – supported by strong end-user demand in automotive and renewable energy, bolstered by regulatory incentives for efficiency and emissions control.

The Battery Monitoring System market is highly competitive and moderately consolidated, with over 120 active global competitors operating across manufacturing, technology development, and system integration. The top five companies — ABB, Siemens, LG Chem, Schneider Electric, and Panasonic — collectively hold an estimated 56% of the global market share, underscoring strong concentration among key players. Competition is driven by rapid innovation, with 48% of firms investing heavily in AI-powered monitoring platforms, wireless communication integration, and cloud-based analytics. Strategic initiatives such as partnerships, mergers, and product launches are common; for example, several leading firms have established joint ventures to develop modular battery monitoring platforms for EV and renewable energy applications. In 2024 alone, over 35 new product launches targeting predictive analytics and real-time diagnostics were recorded globally. The competitive landscape also reflects geographic diversification strategies, with 67% of companies expanding in Asia-Pacific due to rising demand. The nature of competition emphasizes technological differentiation, strategic alliances, and sustainability integration, positioning the Battery Monitoring System market as a dynamic and innovation-driven industry.

ABB

Siemens

Schneider Electric

Tesla Energy

Hitachi Energy

Toshiba Energy Systems & Solutions

Epec Engineered Technologies

Nuvation Energy

Epec Battery Systems

Eaton Corporation

Leclanché SA

The Battery Monitoring System market is undergoing significant technological transformation, driven by innovations in AI, IoT, wireless communication, and cloud computing. AI-powered diagnostic platforms now enable real-time health assessment of battery systems, improving predictive maintenance accuracy by up to 28%. Advanced IoT-enabled sensors are enhancing monitoring capabilities, with over 62% of newly installed systems incorporating multi-parameter sensing, including temperature, voltage, current, and state-of-health metrics. Wireless monitoring technologies are increasingly replacing traditional wired systems, offering up to a 22% reduction in installation and maintenance costs while enabling remote management. Cloud-based platforms are emerging as a core technology, with 41% of systems in 2024 integrating cloud analytics to deliver centralized, scalable, and secure battery data management. Another significant trend is the development of modular monitoring platforms, allowing scalable deployment for EV fleets and renewable energy storage projects. Additionally, integration with blockchain is being explored to ensure data integrity and secure energy trading in decentralized grid environments. These advancements not only improve performance and safety but also align with regulatory compliance and ESG requirements, positioning technology innovation as a key competitive differentiator in the Battery Monitoring System market.

In 2023, ABB launched a cloud-based battery monitoring platform integrating AI diagnostics, improving battery performance visibility by over 25% for utility-scale projects globally.

In 2024, Siemens introduced a wireless modular battery monitoring solution that reduced installation time by 30% in EV charging infrastructure projects across Europe.

LG Chem expanded its Battery Monitoring System portfolio in 2023 with a predictive analytics feature, enabling up to 20% longer battery lifespan for renewable energy storage.

In 2024, Panasonic deployed an integrated AI and IoT monitoring system in large-scale commercial fleets, achieving a 22% reduction in battery downtime and maintenance costs.

The Battery Monitoring System Market Report offers an extensive analysis of the competitive landscape, emerging technologies, adoption trends, and regional market dynamics. The scope covers detailed segmentation by product type, including modular, wired, and wireless monitoring systems, with insights into their technological attributes and adoption drivers. Application segments covered include electric vehicles, renewable energy storage, industrial automation, and consumer electronics, offering a comprehensive view of usage patterns and technological requirements. The report examines end-user sectors such as automotive manufacturing, utilities, industrial operations, and infrastructure development, highlighting adoption behavior, investment trends, and sector-specific innovations. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing in-depth analysis of regional adoption rates, regulatory influences, and infrastructure developments. It also highlights emerging trends such as AI-powered predictive analytics, cloud-based monitoring, modular system adoption, and wireless communication integration. The scope includes a focus on technological modernization, sustainability drivers, and innovation pathways, equipping stakeholders with a comprehensive understanding of opportunities and challenges across the Battery Monitoring System market ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 9745.14 Million |

|

Market Revenue in 2032 |

USD 22948.25 Million |

|

CAGR (2025 - 2032) |

11.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB, Siemens, LG Chem, Schneider Electric, Panasonic, Tesla Energy, Johnson Controls, Hitachi Energy, Toshiba Energy Systems & Solutions, Epec Engineered Technologies, Nuvation Energy, Epec Battery Systems, Eaton Corporation, Leclanché SA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |