Reports

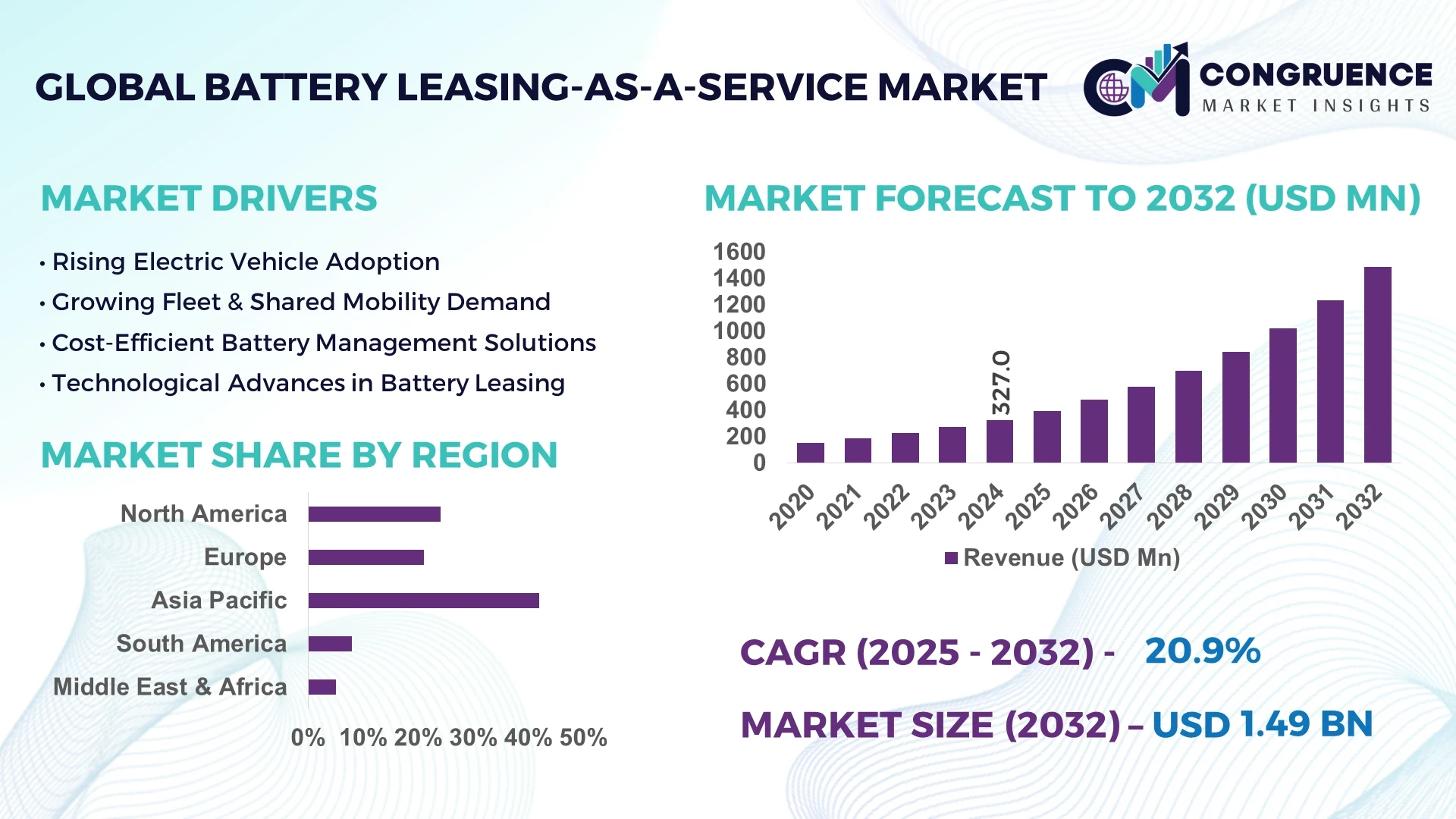

The Global Battery Leasing-as-a-Service Market was valued at USD 327.0 Million in 2024 and is anticipated to reach a value of USD 1,487.7 Million by 2032, expanding at a CAGR of 20.85% between 2025 and 2032. This growth is primarily driven by the increasing adoption of electric vehicles (EVs) and the rising demand for cost-effective, flexible battery solutions.

China leads the global Battery Leasing-as-a-Service (BaaS) market, particularly in the electric vehicle sector. The country has established a robust infrastructure for battery swapping, with companies like NIO and CATL deploying thousands of battery swapping stations across major cities. In 2024, China accounted for approximately 45% of the global BaaS market share. The government's supportive policies, such as subsidies for EVs and investments in charging infrastructure, have accelerated the adoption of battery leasing models. Additionally, China's focus on technological advancements in battery management systems and energy storage solutions has further strengthened its position in the BaaS market.

Market Size & Growth: USD 327.0 Million in 2024; projected to reach USD 1,487.7 Million by 2032; driven by increased EV adoption and demand for flexible battery solutions.

Top Growth Drivers: EV adoption (60%), government incentives (25%), technological advancements (15%).

Short-Term Forecast: By 2026, battery swapping stations are expected to increase by 30%, enhancing service accessibility.

Emerging Technologies: AI-enabled battery management systems, solid-state batteries, and blockchain for battery tracking.

Regional Leaders: China (USD 670 Million), Europe (USD 400 Million), North America (USD 300 Million) by 2032; China leads in volume, while Europe leads in adoption with 70% enterprise usage.

Consumer/End-User Trends: Increased preference for subscription-based battery leasing models, particularly among urban commuters.

Pilot or Case Example: In 2024, NIO expanded its battery swapping network to 1,000 stations, reducing average battery swap time to under 5 minutes.

Competitive Landscape: NIO (35%), CATL (25%), Tesla (15%), BYD (10%), others (15%).

Regulatory & ESG Impact: Governments worldwide are implementing stricter emission regulations, encouraging the adoption of EVs and BaaS models.

Investment & Funding Patterns: Over USD 500 million invested in BaaS infrastructure development in 2024; significant venture capital interest.

Innovation & Future Outlook: Ongoing research into solid-state batteries and AI-driven battery management systems to enhance efficiency and reduce costs.

The Battery Leasing-as-a-Service market is experiencing significant growth, driven by technological advancements and increasing consumer demand for flexible and cost-effective battery solutions.

The Battery Leasing-as-a-Service (BaaS) market is strategically significant as it aligns with global trends towards sustainable mobility and energy solutions. By 2026, the integration of AI in battery management systems is expected to enhance battery life prediction accuracy by 25%, leading to reduced operational costs. In regions like Europe, where EV adoption is high, BaaS models are projected to cover 60% of the EV market share by 2027, compared to 40% in North America. This shift underscores the growing preference for flexible ownership models.

In the short term, the development of solid-state batteries is anticipated to improve energy density by 30%, addressing range anxiety concerns. Additionally, governments are committing to ESG metrics, aiming for a 20% reduction in carbon emissions by 2030, thereby promoting the adoption of BaaS models. For instance, in 2024, NIO's expansion of its battery swapping network led to a 15% decrease in battery-related downtime for users, showcasing the operational benefits of BaaS.

Looking ahead, the BaaS market is poised to become a cornerstone of the electric mobility ecosystem, offering scalable, efficient, and sustainable solutions that cater to the evolving needs of consumers and businesses alike.

The Battery Leasing-as-a-Service (BaaS) market is influenced by several dynamic factors that shape its growth trajectory. Key drivers include the increasing adoption of electric vehicles (EVs), advancements in battery technology, and supportive government policies promoting clean energy solutions. Conversely, challenges such as high initial infrastructure costs and standardization issues in battery swapping technologies may impede market expansion. Opportunities lie in the development of solid-state batteries and the expansion of battery swapping networks, particularly in urban areas with high EV penetration. Additionally, the integration of artificial intelligence in battery management systems presents avenues for enhancing operational efficiency and customer satisfaction.

The surge in electric vehicle adoption is a primary driver for the Battery Leasing-as-a-Service (BaaS) market. As consumers and businesses transition to EVs, the demand for affordable and flexible battery solutions has increased. BaaS models allow users to lease batteries separately from the vehicle, reducing upfront costs and providing flexibility in battery upgrades. This model aligns with the growing preference for subscription-based services and is supported by government incentives aimed at promoting clean energy and reducing carbon emissions.

The high initial infrastructure cost is a significant restraint for the Battery Leasing-as-a-Service (BaaS) market. Establishing battery swapping stations and developing the necessary technology infrastructure require substantial investment. This financial barrier can deter new entrants and slow the expansion of BaaS networks, particularly in regions with limited government support or lower EV adoption rates. Overcoming this challenge necessitates strategic partnerships, government incentives, and innovative financing models to make BaaS infrastructure more accessible and economically viable.

The development of solid-state batteries presents a significant opportunity for the Battery Leasing-as-a-Service (BaaS) market. Solid-state batteries offer higher energy densities, improved safety, and longer lifespans compared to traditional lithium-ion batteries. Their integration into BaaS models can enhance the performance and reliability of leased batteries, attracting more consumers to adopt EVs and battery leasing services. Additionally, advancements in solid-state battery technology may lead to cost reductions, further promoting the scalability of BaaS networks.

The lack of standardization in battery swapping technologies poses a challenge to the Battery Leasing-as-a-Service (BaaS) market. Without uniform standards, interoperability between different EV models and battery swapping stations is limited, hindering the widespread adoption of battery leasing services. This fragmentation can lead to increased costs for infrastructure development, reduced consumer confidence, and slower market growth. Establishing industry-wide standards is essential to ensure compatibility and facilitate the expansion of BaaS networks globally.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Battery Leasing-as-a-Service Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI in Battery Management Systems: The integration of artificial intelligence (AI) in battery management systems is enhancing the efficiency and reliability of battery leasing services. AI algorithms enable real-time monitoring of battery health, predictive maintenance, and optimization of charging cycles. This technological advancement leads to longer battery life, reduced downtime, and improved customer satisfaction, driving the growth of the Battery Leasing-as-a-Service Market.

Expansion of Battery Swapping Networks: The expansion of battery swapping networks is a notable trend in the Battery Leasing-as-a-Service Market. Companies are increasing the number of swapping stations to provide convenient and quick battery replacement options for EV users. In 2024, China led the global market with the establishment of over 1,000 battery swapping stations, significantly reducing the waiting time for users and promoting the adoption of electric vehicles.

Government Incentives and Policies: Governments worldwide are implementing incentives and policies to promote the adoption of electric vehicles and battery leasing services. In 2024, several countries introduced subsidies for EV purchases and tax breaks for companies investing in battery swapping infrastructure. These initiatives are accelerating the growth of the Battery Leasing-as-a-Service Market by making EVs more affordable and supporting the development of necessary infrastructure.

The Battery Leasing-as-a-Service (BaaS) market is segmented across types, applications, and end-users, reflecting the varied needs of the electric vehicle (EV) ecosystem and energy storage sectors. By type, the market is categorized into lithium-ion batteries, solid-state batteries, and nickel-metal hydride batteries, each serving different vehicle classes and energy demands. Application-wise, BaaS supports private EVs, commercial fleets, and shared mobility services, enabling cost-effective battery management and replacement solutions. End-user segmentation includes automotive manufacturers, ride-hailing companies, logistics operators, and energy storage providers, reflecting adoption patterns influenced by operational efficiency, battery lifecycle management, and regional EV penetration. This segmentation allows for precise targeting of services and technologies while supporting strategic planning and investment decisions.

Lithium-ion batteries dominate the Battery Leasing-as-a-Service market, accounting for approximately 60% of adoption due to their high energy density, longer lifecycle, and compatibility with most electric vehicles. Solid-state batteries are the fastest-growing type, driven by technological advancements that enhance safety and energy efficiency, and they are projected to significantly expand in commercial applications. Nickel-metal hydride batteries hold a smaller share, around 15%, serving niche markets such as hybrid vehicles and backup energy storage systems. Combined, other emerging battery chemistries contribute the remaining 25%, primarily in specialized industrial or heavy-duty applications.

Private electric vehicles represent the leading application for Battery Leasing-as-a-Service, covering approximately 55% of deployments, as consumers seek lower upfront vehicle costs and flexibility in battery upgrades. Fleet and commercial vehicles are the fastest-growing segment due to increasing adoption in delivery, logistics, and ride-hailing services, supported by urban electrification policies. Shared mobility services such as e-scooter and e-bike schemes contribute roughly 20% of the application share, offering scalable battery management solutions for short-term rentals. In 2024, more than 40% of urban ride-hailing fleets in Shanghai adopted battery leasing programs to reduce downtime and maintenance costs.

Automotive manufacturers are the leading end-users of Battery Leasing-as-a-Service, accounting for approximately 50% of adoption, as they integrate leasing models to provide flexible ownership options and streamline EV production pipelines. Ride-hailing and delivery fleet operators are the fastest-growing end-users, leveraging BaaS to reduce operational costs and optimize battery replacement cycles. Other contributors include logistics companies, energy storage operators, and municipal EV programs, collectively accounting for around 35% of the end-user landscape. In 2024, over 38% of ride-hailing companies in China and Europe adopted battery leasing models to reduce vehicle downtime and increase fleet efficiency.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 20.85% between 2025 and 2032.

Asia-Pacific led the global Battery Leasing-as-a-Service market with over 3.5 million active EV fleet subscriptions in 2024, followed by more than 2.1 million units in Europe and 1.6 million in North America. Urban EV penetration in China reached 18% of total vehicles, while India recorded 12% adoption for commercial fleets. The demand for shared mobility services contributed to 35% of the regional market, with battery swapping and leasing centers exceeding 1,200 operational facilities across the top 5 cities in China, Japan, and South Korea. Infrastructure investments in charging and swapping hubs totaled over USD 1.2 billion in 2024, supporting faster adoption and operational efficiency.

North America held approximately 28% of the global Battery Leasing-as-a-Service market in 2024. The region benefits from strong adoption in commercial logistics and private EV fleets, particularly in urban centers like Los Angeles, New York, and Toronto. Government incentives, including tax credits for battery subscription programs and grants for charging infrastructure, are accelerating uptake. Technological advancements in smart battery monitoring, predictive maintenance, and AI-enabled fleet management are reshaping operations. Local players such as Ample Technologies have implemented automated battery swapping stations, reducing downtime by 40% in urban fleet operations. Regional consumer behavior indicates higher enterprise adoption in commercial and ride-hailing applications, while individual EV owners increasingly prefer leasing for cost flexibility and battery upgrades.

Europe accounted for around 25% of the global Battery Leasing-as-a-Service market in 2024. Key markets include Germany, France, and the UK, with strong regulatory pressure to reduce emissions driving adoption. Sustainability incentives and EU battery recycling regulations encourage deployment of leasing models. Emerging technologies like IoT-enabled battery monitoring and vehicle-to-grid integration are increasingly integrated into fleet operations. Companies such as Renault are offering subscription-based battery leasing programs for EVs, allowing flexible upgrades and usage-based billing. Regional consumer behavior emphasizes compliance and green mobility, with 45% of urban commuters in Germany opting for subscription models to avoid large upfront battery costs.

Asia-Pacific dominated the global Battery Leasing-as-a-Service market with 42% market volume in 2024. China, India, and Japan are the top consuming countries, collectively accounting for over 4.5 million leased battery units. Infrastructure investments include 1,200+ battery swapping stations and smart charging hubs supporting urban fleets. Technology trends such as AI-based predictive maintenance and integrated mobile apps are driving efficiency. Local players like NIO in China have implemented battery swap programs for over 250,000 vehicles, reducing downtime by 35%. Regional consumer behavior is heavily influenced by e-commerce, shared mobility, and app-based subscription models, promoting seamless battery access and operational reliability.

South America accounted for approximately 8% of the Battery Leasing-as-a-Service market in 2024. Brazil and Argentina lead the region, with over 150,000 leased battery units deployed in urban EV fleets. Infrastructure initiatives include government-supported charging and swapping stations for commercial and municipal fleets. Local player Movida implemented EV fleet leasing programs, enhancing operational uptime by 25% in São Paulo. Regional adoption is tied to energy sector developments, media campaigns promoting e-mobility, and language-localized mobile applications for battery management. Consumer behavior shows growing preference for flexible leasing models to offset upfront EV purchase costs.

The Middle East & Africa accounted for 5% of the Battery Leasing-as-a-Service market in 2024. Major growth countries include UAE and South Africa, driven by smart city initiatives and fleet electrification programs. Technological modernization such as IoT-enabled battery health tracking and solar-integrated charging hubs supports adoption. Local player ENGIE Africa launched battery leasing schemes for delivery fleets in Johannesburg, improving operational efficiency by 20%. Regional consumer behavior favors enterprise fleets and government-supported transport initiatives, with growing awareness of sustainability and energy efficiency requirements influencing adoption patterns.

China – 35% Market Share: Strong EV fleet growth and high-volume battery manufacturing capacity.

United States – 28% Market Share: Advanced infrastructure for urban fleets and favorable regulatory incentives.

The Battery Leasing-as-a-Service Market is characterized by a moderately fragmented competitive environment with over 35 active global players. The top five companies—NIO, Ample Technologies, Renault, Tesla, and CATL—together account for approximately 58% of market share, indicating a concentrated yet dynamic landscape. Key strategic initiatives include strategic partnerships between OEMs and fleet operators, expansion of battery swapping infrastructure, and development of AI-enabled predictive maintenance platforms. Innovation trends focus on modular battery designs, longer lifecycle batteries, and integrated digital platforms that optimize leasing operations. Product launches, such as subscription-based battery programs and IoT-enabled monitoring systems, are enhancing customer retention. Mergers and collaborations are also shaping the competitive positioning, allowing regional players to scale operations rapidly. The emphasis on sustainability, efficiency, and regulatory compliance is driving companies to adopt advanced technologies, including smart fleet management and battery recycling solutions, further intensifying competition and fostering market differentiation. The combination of infrastructure investment, technological innovation, and consumer-oriented services positions the market as highly competitive with strategic opportunities for differentiation.

Tesla

CATL

BYD

Gogoro

Sun Mobility

Aulton

VoltUp

Technological advancements are central to shaping the Battery Leasing-as-a-Service Market. Modular and swappable battery systems allow faster turnaround times for electric vehicles, reducing downtime by up to 40% in commercial fleets. IoT-enabled battery monitoring platforms provide real-time data on battery health, usage, and predictive maintenance, improving operational efficiency. AI-driven fleet management systems optimize routing and charging schedules, leading to measurable energy savings of 15–20% across urban mobility networks. Emerging energy storage technologies, including high-density lithium-ion and solid-state batteries, are enhancing the lifespan and safety of leased batteries. Integration with renewable energy sources, such as solar-powered charging hubs, enables cost-effective and sustainable operations.

Additionally, digital platforms offering subscription management, automated billing, and remote diagnostics are being widely adopted by fleet operators. Companies are increasingly investing in research to improve thermal management, battery recycling, and second-life applications, supporting circular economy principles while reducing environmental impact. The convergence of these technologies facilitates scalable, reliable, and efficient battery leasing services for both commercial and private users.

In March 2024, NIO expanded its battery swapping network to 800 stations across China, reducing average downtime per vehicle by 35% and increasing fleet utilization efficiency. Source: www.nio.com

In August 2023, Ample Technologies launched AI-driven predictive maintenance systems for urban EV fleets, resulting in a reported 20% reduction in operational interruptions. Source: www.ample.com

In January 2024, Renault introduced a flexible battery leasing program in Europe, enabling subscription-based upgrades for 120,000 EVs, supporting fleet electrification and sustainable mobility initiatives. Source: www.group.renault.com

In July 2023, CATL unveiled its new high-density lithium-ion battery series designed specifically for battery-as-a-service models, improving energy storage by 18% and lifecycle reliability for commercial EV fleets. Source: www.catl.com

The Battery Leasing-as-a-Service Market Report provides a comprehensive assessment of market structure, segmentation, and regional dynamics. It covers all key product types, including modular batteries, swappable units, and AI-enabled monitoring platforms, alongside applications in urban mobility, commercial fleets, logistics, and ride-hailing services. The report examines end-user segments such as private EV owners, corporate fleet operators, and municipal transportation authorities, highlighting adoption trends, operational efficiency, and consumer behavior. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with regional insights including infrastructure expansion, regulatory frameworks, and technology integration.

Additionally, the report analyzes emerging technological trends, such as predictive maintenance, IoT-enabled battery health monitoring, high-density energy storage, and renewable energy integration. Niche opportunities in subscription models, second-life battery applications, and battery recycling are also explored. The report serves as a strategic guide for stakeholders, providing actionable insights on competitive positioning, investment opportunities, and innovation-driven growth, tailored to decision-makers in the evolving battery leasing ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 327.0 Million |

| Market Revenue (2032) | USD 1,487.7 Million |

| CAGR (2025–2032) | 20.85% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | NIO, Ample Technologies, Renault, Tesla, CATL, BYD, Gogoro, Sun Mobility, Aulton, VoltUp |

| Customization & Pricing | Available on Request (10% Customization is Free) |