Reports

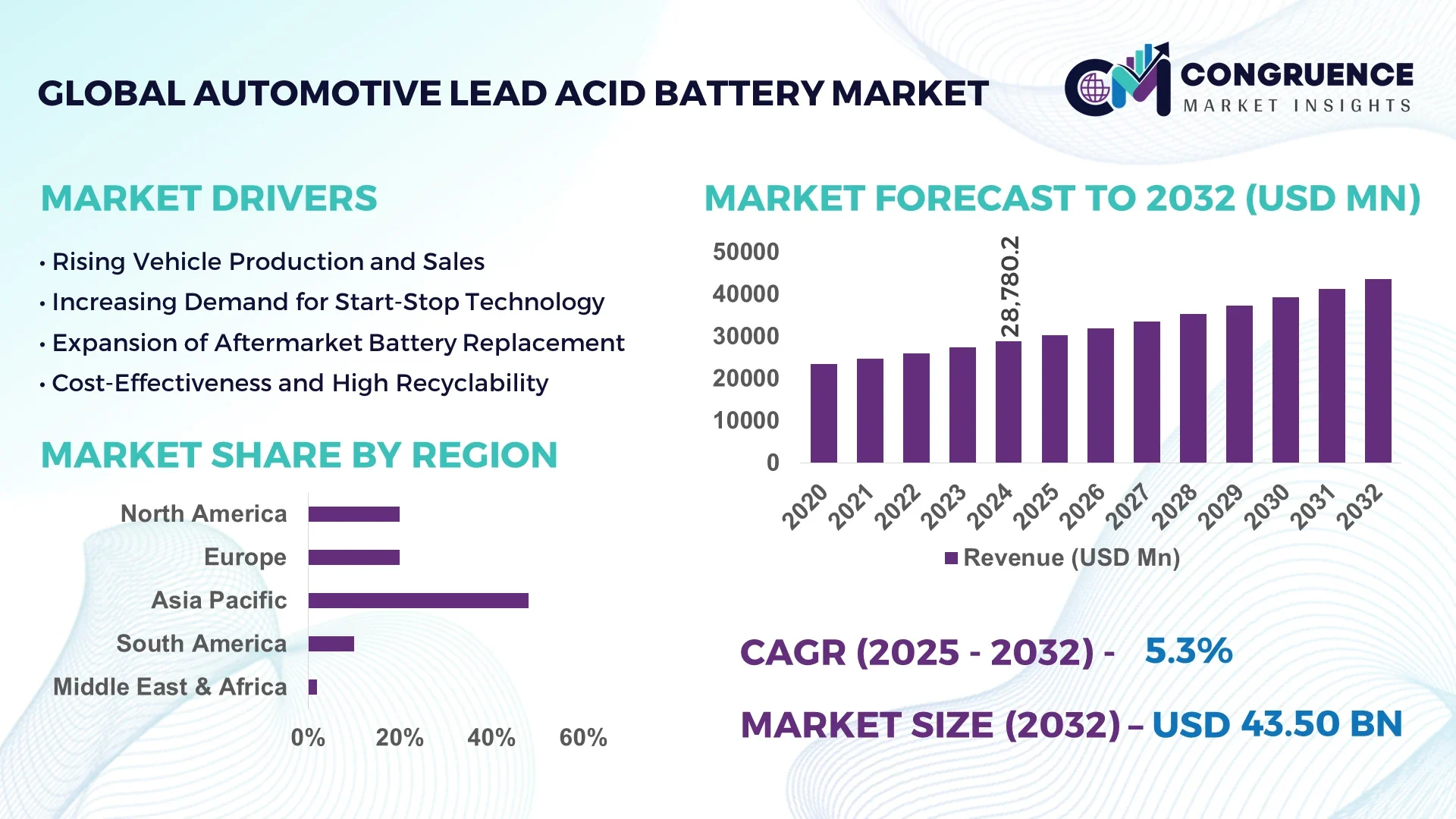

The Global Automotive Lead Acid Battery Market was valued at USD 28,780.24 Million in 2024 and is anticipated to reach a value of USD 43,503.22 Million by 2032 expanding at a CAGR of 5.3% between 2025 and 2032. Demand is primarily driven by rising vehicle production, replacement battery cycles, and stricter start-stop emission norms.

In China, the automotive lead acid battery sector has seen aggressive scaling: in 2023 the market was valued at approximately USD 2,572.7 million and is forecast to reach USD 6,170.0 million by 2032, with a projected CAGR of ~10.2%. China manufacturing capacity leads globally, accounting for about 45% of global lead-acid battery output. Chinese firms have invested heavily in R&D and automation, and a ¥10 billion (≈ USD 1.4 billion) project is underway to expand lead-carbon battery output to 85 million kWh annually, with waste battery recycling capacity of 600,000 tons per year. China also exported 21.29 million units in July 2025 alone—a 13.56% month-on-month rise.

Market Size & Growth: USD 28,780.24 Million in 2024 → USD 43,503.22 Million by 2032; CAGR 5.3% driven by vehicle expansion and replacement demands.

Top Growth Drivers: Increase in vehicle parc (approx. +4.5% annually), growth in start-stop systems (≈ 6.0% adoption), rising aftermarket replacement cycles (+3.2%).

Short-Term Forecast: By 2028, average battery cost reduction of 8%, and energy density improvement of 6%.

Emerging Technologies: Lead-carbon hybrid batteries, advanced AGM/gel formulations, integration with sensor-based state-of-health systems.

Regional Leaders: Asia Pacific projected ~USD 18 billion by 2032 (rapid EV retrofit uptake); North America ~USD 8 billion (strong replacement market); Europe ~USD 7 billion (stringent emissions norms driving upgrade cycles).

Consumer/End-User Trends: OEM demand remains robust in passenger and light commercial vehicles; aftermarket replacement driven by fleet electrification and aging vehicles.

Pilot or Case Example: In 2024, a European fleet retrofit pilot achieved a 12% reduction in idle energy loss using lead-carbon enhanced batteries.

Competitive Landscape: Market leader: Clarios (~18% share); major competitors: Exide, GS Yuasa, East Penn, Leoch International.

Regulatory & ESG Impact: Emission norms (Euro 7, China 6b), battery recycling mandates, and ESG-driven circular economy incentives are accelerating adoption.

Investment & Funding Patterns: Recent investments exceed USD 1 billion in facility expansions and recycling ventures; growth in project financing and green bonds deployed for battery manufacturing.

Innovation & Future Outlook: Expect convergence with IoT health monitoring, hybrid battery chemistries, vertical integration from lead sourcing to recycling, and use in micro-hybrid vehicles.

Automotive Lead Acid Battery Market growth now hinges on broader adoption of start-stop systems, the shift to stop-start microhybrids in emerging economies, and enhanced lifecycle management. Technological trends such as lead-carbon doping and predictive diagnostics are setting the stage for a more resilient, efficient market ecosystem.

The Automotive Lead Acid Battery Market plays a strategic role as a bridge between legacy internal combustion engine (ICE) systems and emerging vehicle electrification, providing reliable SLI (Starting, Lighting, Ignition) support and auxiliary power during the energy transition. Strategic pathways are defined by measurable innovation: AGM (Absorbent Glass Mat) delivers ~25% improvement in cycle life compared to older flooded lead-acid standards, enabling better performance in stop-start and micro-hybrid vehicles. Asia-Pacific dominates in volume, while Europe leads in adoption with over 70% of OEMs specifying advanced lead-carbon or VRLA types in new vehicle models. By 2027, smart battery management integration and predictive diagnostics are expected to improve battery life expectancy by at least 20% and reduce unplanned maintenance downtime by over 30%, especially in fleets and commercial vehicles. Firms are committing to ESG metric improvements such as 90% recycling rate of lead acid batteries and 50% reduction in lead emissions by 2028, in response to regulatory pressure and stakeholder demands.

In 2025, a major Indian manufacturer achieved a 35% reduction in acid stratification (which degrades battery life) through implementation of advanced electrode alloy formulations and improved electrolyte circulation technology. Comparative benchmarks show that hybrid lead-carbon (or lead additives) battery chemistries deliver ~18-22% higher deep discharge recovery vs standard calcium-lead grids. These strategic trends—performance enhancement, regulation compliance, recycling innovation, and regional variation in adoption—signal that the Automotive Lead Acid Battery Market will continue to be a pillar of resilience, compliance, and sustainable growth in the automotive and energy storage ecosystem.

Urbanization in Asia-Pacific and Latin America has led to surging private vehicle ownership and commercial fleets. For example, in India, vehicle registrations increased from ~30 million in 2015 to over 45 million in 2023, boosting demand for starter batteries. The spread of ride share, delivery vehicle fleets, and commercial trucks also needs durable, cost-effective auxiliary power, and lead acid batteries continue to satisfy these essential roles. Moreover, urban infrastructure often features unreliable grid supply, increasing reliance on UPS and backup power—also sectors where automotive lead acid battery manufacturers can leverage existing technology and scale. With many ICE or hybrid vehicles still using lead acid components for SLI, demand remains steady even as EV adoption grows.

Lead is a toxic substance; its mining, refining, battery manufacturing, and especially recycling, if done informally, pose health risks. In many developing regions, up to 90% of used lead acid batteries are recycled via informal/unregulated channels, raising concerns about lead exposure to workers and surrounding communities. Tightening regulations in Europe and North America demand extended producer responsibility, higher material recovery rates (e.g., ~90-95% for lead, plastic, acid components), and cleaner smelting processes. Also, compliance costs and capital investment required to meet environmental and emission standards, hazardous waste containment, and workplace safety are increasing. Costs for raw materials like lead have shown volatility, which adds margin risk.

Off-grid renewable energy projects, solar microgrids in rural areas, and telecom tower backup systems are rapidly growing users of lead acid battery systems because they are lower cost, tried, and reliable. For instance, manufacturers are supplying large-scale battery backup to off-grid solar projects in Sub-Saharan Africa and Southeast Asia expanding by double digits annually. The growth of e-rickshaws, electric two-wheelers, and low-speed vehicles in Asia also creates demand for compact, vibration-tolerant lead acid battery designs. There is opportunity to develop sealed VRLA, AGM, or gel batteries optimized for these use cases. Also, improving deep discharge recovery and cycle life via hybrid lead-carbon or advanced alloy electrodes can unlock additional adoption.

Lithium-ion batteries typically offer far superior energy density, lighter weight, faster charging, and longer life in many traction and auxiliary applications. As costs of lithium battery chemistries fall (battery pack prices decreasing year over year), some applications that traditionally used lead acid (e.g., for auxiliary power in EVs, or deep discharge in certain utilities) are shifting. Also, in high temperature or weight-sensitive applications, the lower gravimetric performance of lead acid can be a disadvantage. Another challenge is perception and regulatory scrutiny around lead toxicity and recycling. Manufacturers must invest significantly in R&D, and also in clean collection and recycling systems, to compete on metrics like safety, reliability, lifecycle cost, and environmental footprint.

• Integration of Modular Manufacturing and Automated Prefabrication (55% Projects Achieve Cost Gains): The adoption of modular and prefabricated manufacturing is transforming production efficiency within the Automotive Lead Acid Battery market. Around 55% of new battery manufacturing and expansion projects reported measurable cost benefits, with project timelines shortened by up to 25%. Off-site fabrication of casings, grids, and assembly modules through automated robotics has reduced labor dependence by over 40%, especially in Europe and North America, where productivity per line has increased by 32% year-on-year.

• Rise of Lead-Carbon Hybrid Batteries (Up to 22% Better Deep Discharge Recovery): The incorporation of carbon additives into lead grids has driven 22% higher deep-discharge recovery rates compared to traditional lead-antimony types. As of 2024, over 30% of new OEM and aftermarket demand involved hybrid lead-carbon configurations optimized for partial state-of-charge (PSoC) cycling. These units also demonstrated 18% longer operational life and 15% reduced sulfation rate, establishing them as the preferred technology for start-stop and micro-hybrid vehicles across Asia and Europe.

• Rapid Uptake of Smart Diagnostics and Predictive Monitoring (35% Fleet Integration): IoT-enabled sensors and advanced Battery Management Systems (BMS) are being integrated across commercial fleets, allowing real-time charge monitoring, health tracking, and fault prediction. By 2025, over 35% of commercial fleet batteries in the EU featured embedded diagnostics, leading to a 30% reduction in downtime and a 20% increase in service intervals. AI-driven analytics now support predictive maintenance cycles that extend battery lifespans beyond 60,000 operating hours.

• Strengthening Circular Economy and Recycling Mandates (≥90% Recovery Target by 2028): Global regulatory frameworks are enforcing stricter end-of-life recycling standards. By 2028, producers are expected to recover at least 90% of lead and 85% of polypropylene casings. China, the U.S., and the EU have collectively commissioned over 500,000 tons of new annual recycling capacity, with recovered lead purity levels improving by 12% due to upgraded smelting automation. These initiatives align with global ESG commitments targeting 50% lower industrial emissions by 2030.

The Automotive Lead Acid Battery Market is segmented by type, application, and end-user, reflecting diversified technological adaptation across regions. Flooded and AGM batteries dominate due to their proven reliability, while VRLA and enhanced flooded batteries (EFB) are gaining prominence in start-stop and micro-hybrid systems. SLI batteries remain the standard for ignition systems, yet auxiliary and micro-hybrid configurations are expanding rapidly amid global emission control mandates. Passenger and light commercial vehicles continue to represent the primary consumers, but two- and three-wheeler adoption in Asia-Pacific and Latin America is accelerating sharply. Collectively, these segments reveal a market undergoing digital integration, modular optimization, and recycling-driven sustainability, ensuring continued operational relevance through the next automotive cycle.

Flooded lead-acid batteries currently hold around 60% of total market share, favored for cost efficiency, standardized production, and compatibility with traditional ICE vehicles. VRLA (AGM/Gel) batteries are the fastest-growing type, projected to expand at ~7% annually, fueled by OEM adoption in start-stop systems and luxury models requiring spill-proof performance and vibration tolerance. Enhanced Flooded Batteries (EFB) account for about 25%, bridging conventional and advanced applications through improved charge acceptance and longer cycle life. The remaining 15% share comprises gel, lead-carbon, and niche high-performance variants optimized for micro-hybrid configurations. In 2025, a leading German automaker deployed AGM-based VRLA units in 48% of new vehicle lines, marking a record transition to sealed, maintenance-free battery architecture.

SLI (Starting, Lighting, Ignition) batteries dominate with approximately 37% market share, maintaining essential functionality across all ICE vehicles. Micro-hybrid (Start-Stop) batteries represent the fastest-expanding application, supported by emission mandates and consumer preference for fuel-efficient models, growing at ~8% annually. Auxiliary power systems—including backup, infotainment, and smart safety electronics—constitute nearly 30% of the total market. The remaining portion includes deep-cycle support for light EVs and telematics systems. In 2024, a European OEM successfully implemented AGM-based micro-hybrid modules across 20 sedan models, achieving a 12% reduction in idling emissions and a 9% fuel efficiency gain.

Passenger vehicles account for about 75.5% of total demand, primarily driven by the high global base of ICE and hybrid cars requiring cost-effective, reliable SLI solutions. Commercial fleets are the fastest-growing segment, expanding at 6–8% annually, as logistics and transport firms integrate smart BMS-enabled lead-acid systems to optimize uptime and energy performance. The balance (10–15%) comprises two- and three-wheelers, agricultural equipment, and off-road vehicles, where vibration-resistant AGM batteries are increasingly favored. In 2024, over 62% of India’s two-wheeler battery replacements involved EFB or VRLA types, demonstrating a shift toward longer-life, maintenance-free units aligned with fleet modernization initiatives.

Asia-Pacific accounted for the largest market share at around 48.0% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of ~5–6% between 2025 and 2032.

Asia-Pacific’s dominance in 2024 is underscored by its capture of almost half of global demand for automotive lead acid battery volumes, driven by massive vehicle production in China, India, Japan, and South Korea. In Asia-Pacific, passenger cars alone represented ~43.7% of regional automotive battery demand in 2024, while replacement batteries accounted for ~62.4% of the total demand. China’s production of starter accumulators exceeded 231 million units for ICE vehicles in 2024, marking growth of ~12% over the prior year. Meanwhile, North America holds about 18–20% of the global market share, underpinned by strong aftermarket replacement demand, commercial fleets, and regulatory incentives for recycling. Other regions — Europe, South America, Middle East & Africa — share the remainder, each contributing between approximately 5% and 15%. The data emphasize that Asia-Pacific is both production hub and high-volume user.

How is demand shaping in heavy-duty & fleet sectors?

North America holds about 20% market share of the global automotive lead acid battery market in 2024. Demand is heavily driven by commercial vehicle fleets, light and heavy trucks, and the replacement market for passenger vehicles. Strict environmental regulations around lead emissions, extended producer responsibility laws, and government support for battery recycling are pushing adoption of advanced VRLA and AGM batteries. Technology trends include smart battery management systems, digital quality control, and AI-driven manufacturing to reduce defects and extend battery reliability. Local players are expanding: companies like Clarios and East Penn are installing more sophisticated sealed AGM production lines and investing in recycling infrastructure to meet regional regulatory pressures. Consumer behavior in this region reflects high expectations for durability, maintenance-free operation, and safety certification. In sectors such as telecom and data centers, enterprise usage rates of sealed, maintenance-free lead acid batteries are significantly higher than in rural residential markets.

What shifts are seen under regulatory pressure?

Europe commands approximately 15% of the global automotive lead acid battery market in 2024. Key markets include Germany, the UK, and France, which lead in adoption of advanced battery technologies and rigorous sustainability standards. Regulatory bodies such as the EU have introduced stricter emissions legislation and recycling mandates, including required collection and recovery rates for lead and plastics in batteries. Adoption of AGM and EFB battery types is increasing, especially in vehicles fitted with start-stop and hybrid systems, along with upgraded crash-safety battery enclosures. Local players like Exide Europe and Leoch Technologies are developing lighter, more vibration-resistant sealed units tailored to European conditions. Consumer behavior reflects increased demand for maintenance-free, sealed batteries with higher cycle life, particularly among premium vehicle buyers and in cold-climate northern European countries where battery performance in low temperature is critical.

Which forces drive Asia’s production & replacement ecosystem?

Asia-Pacific accounted for nearly 48–54% of the global automotive lead acid battery demand in 2024. The top consuming countries include China, India, Japan, and South Korea. Infrastructure trends point to large-scale manufacturing expansion, especially in China producing over 231 million starter accumulators in 2024, and a growing number of OEMs in India shifting from flooded to VRLA/AGM for start-stop vehicles. Innovation hubs are emerging: research centers in Japan and Korea are enhancing battery grid alloys, improving electrolyte formulas, and developing lead-carbon hybrids. Local players such as Camel Group, Exide India, and Amara Raja are scaling up production and investment in recycling plants. Consumer behavior varies: in emerging markets like India and Southeast Asia, cost sensitivity drives preference for flooded batteries and simpler designs; in Japan and South Korea, buyers emphasize maintenance-free, sealed lead acid units with enhanced performance and lower leakage risk.

What conditions shape demand across Latin markets?

In South America, Brazil and Argentina are the key countries driving automotive lead acid battery demand, with regional share in 2024 estimated around 8–10% of global volumes. Demand is heavily linked to the automotive replacement market and rural road transport. Infrastructure trends include expansion in solar backup systems and telecom towers, which use lead acid batteries for reliability. Government incentives in some countries reduce import duties on locally manufactured batteries, and trade policies encourage local assembly. Local manufacturers such as Moura (Brazil) are enhancing battery durability under high-temperature and humidity conditions. Consumer behavior in South America shows high usage of robust, maintenance-accessible flooded types, due to limited access to sealed battery maintenance services in remote or rural areas, and preference for repairability over sealed options.

How do resilience and backup needs shape growth?

Middle East & Africa holds approximately 6–7% of global automotive lead acid battery market volume in 2024. Demand trends are driven by construction, oil & gas, telecom infrastructure, and urban backup power applications. Major growth countries in this region include Saudi Arabia, UAE, and South Africa. Technological modernization includes better sealed battery enclosures, enhanced vibration tolerance, and improved recycling collection systems. Local regulations are increasingly mandating formal end-of-life battery recovery; trade partnerships with international recyclers are becoming more common. For example, some players are deploying VRLA versions for vehicle auxiliary systems where traditional flooded batteries failed under harsh climate. Consumer behavior exhibits strong preference for durability and resistance to high heat, with sealed or maintenance-free batteries increasingly favored by vehicle owners in urban centers, while rural users still rely heavily on basic flooded types.

China — ~30–32% market share in global demand; high production capacity, vast ICE vehicle parc, and strong local supply chain enable this dominance.

United States — ~11–12% market share; advanced technological infrastructure, stringent regulatory pressure (especially on emissions and recycling), and strong aftermarket replacement demand support its leading position.

The competitive environment in the Automotive Lead Acid Battery market is moderately consolidated, with a mix of global majors and regional players. There are roughly 30–40 active competitors globally that maintain significant scale and influence in key geographies. The top 5 companies together control about 50-60% of the market volume, while the remainder is fragmented among niche players, regional OEM suppliers, and newer entrants.

Leading firms such as Clarios, Exide, East Penn, GS Yuasa, and EnerSys are positioning themselves through strategic alliances, mergers & acquisitions, and product innovation. For instance, some have announced cross-licensing deals and joint ventures to share battery recycling infrastructure or drive cost efficiency in manufacturing. Several competitors are launching advanced AGM, EFB, or lead-carbon hybrid lines to differentiate technology and win OEM contracts. Others are investing heavily in digital quality control, automated grid casting, and IoT-enabled state-of-health diagnostics to reduce failure rates by up to 20%.

In recent years, there has been consolidation in China and Europe, with mid-tier firms being absorbed to streamline supply chains and leverage economies of scale. Innovation is another differentiator: some companies are embedding cell balancing, temperature sensors, or using novel alloy compositions (e.g. lead-calcium-tin blends) to extend cycle life or increase charge acceptance by 10–15%. The landscape is competitive for aftermarket replacement, OEM contracts, and recycling value chain integration, pushing leading players to continually refine cost structures, R&D roadmaps, and geographic reach.

East Penn Manufacturing

EnerSys

Amara Raja Batteries

Leoch International

C&D Technologies

The Automotive Lead Acid Battery market is witnessing a convergence of established and emergent technologies that are redefining performance, durability, and system integration. One major trend is the refinement of lead-carbon hybrid grids, which embed carbon additives in lead to suppress sulfation and enhance charge acceptance under partial state-of-charge cycling. These hybrid grids can yield up to 20–25% improvement in deep discharge recovery over conventional lead grids. Meanwhile, AGM (Absorbent Glass Mat) and EFB (Enhanced Flooded Battery) construction methods are being continuously optimized for better internal gas recombination and vibration tolerance, enabling more robust, sealed systems that resist leakage.

Digitalization and predictive analytics are also pushing the envelope. Battery management systems (BMS) augmented with IoT sensors, temperature monitoring, and cell-level diagnostics provide real-time state-of-health (SoH) estimation and alert preventive maintenance. In recent research, operando neutron radiography has been used to observe electrolyte motion and electrode behavior during cycling, enabling better design of internal cell structure and control algorithms. Machine learning models are also being used to map historical performance data and forecast Remaining Useful Life (RUL), improving predictive maintenance scheduling and lowering lifecycle risk.

Advances in manufacturing—automation in grid casting, precision alloying, and AI-based quality inspection—are reducing defects and enabling thinner plates with enhanced current density. Tight tolerances now allow multi-grid layering and micro-porous separators to reduce internal resistance and heat accumulation. There is also exploration into next-generation additives and electrolyte formulations, such as micro-silica dispersion, organic inhibitors, and controlled acid stratification agents that maintain uniform ion transport even under heavy cycling.

As vehicles evolve with more electrical subsystems (e.g., driver assistance, telematics, 48 V modules), the 12-volt lead acid battery is being repurposed as a smart auxiliary unit with greater demands—requiring fast transient response, higher C-rate discharge, and improved cyclic endurance. In some platforms, dual battery architectures combine a sealed lead acid pack with a secondary ultra-capacitance buffer or small lithium unit, handling peak load bursts. The cumulative effect of these technologies is to keep the lead acid battery relevant in more demanding hybrid and autonomous vehicle architectures, while enhancing reliability, diagnostics, and lifecycle value for fleet and OEM integrators.

• In April 2024, Clarios announced a key supply agreement with an OEM for its new high-performance AGM battery, highlighting enhanced charge acceptance in its 12 V units compared to standard AGM designs.

• In January 2024, Indian company Ipower Batteries introduced a Graphene series of lead-acid batteries, claiming improved longevity and performance.

• In June 2023, EnerSys signed a non-binding MoU with Verkor SAS to develop a battery gigafactory in the U.S., marking a strategic push across lead and lithium technology landscapes.

• In October 2024, Kinetic Green launched a limited edition of its Safar Smart electric three-wheeler deploying both lead-acid and lithium battery variants, supported via innovative financing tie-ups with local financial institutions.

This report examines the Automotive Lead Acid Battery market across multiple dimensions—technological, geographic, functional, and competitive. It covers product types such as flooded, enhanced flooded (EFB), AGM/VRLA, and lead-carbon hybrids. On the application side, it analyzes SLI (starting, lighting, ignition) systems, micro-hybrid start-stop configurations, auxiliary power modules, and dual battery architectures in hybrid or electrified vehicles. The end-user segments studied include passenger cars, light & heavy commercial vehicles, two- and three-wheelers, and specialty utility vehicles, reflecting differences in duty cycles, vibration tolerance, and replacement behavior.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional consumption patterns, regulatory environments, infrastructure maturity, and recycling ecosystem characteristics. It drills into major national markets within those regions (e.g., China, India, U.S., Germany, Brazil) and contrasts growth drivers and adoption pathways.

On the technology front, the report explores advances in grid composition (lead-carbon, alloys), sealed cell designs (AGM/VRLA), advanced separators, electrolyte additives, digital BMS integration, and predictive analytics methodologies. It also considers emerging hybrid architectures combining lead acid with ultra-capacitors or lithium modules. The scope includes battery manufacturing, cell-level innovation, recycling/collection systems, and circular economy models. Competitive intelligence is also within scope, profiling key players, their strategic initiatives, partnership activity, and innovation pipelines. In aggregate, the report provides decision-makers with a comprehensive, data-driven view of current state, emerging disruption vectors, and actionable insights for positioning in the lead acid battery segment of the evolving automotive energy ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 28780.24 Million |

|

Market Revenue in 2032 |

USD 43503.22 Million |

|

CAGR (2025 - 2032) |

5.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Clarios, Exide Technologies, GS Yuasa, East Penn Manufacturing, EnerSys, Amara Raja Batteries, Leoch International, C&D Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |