Reports

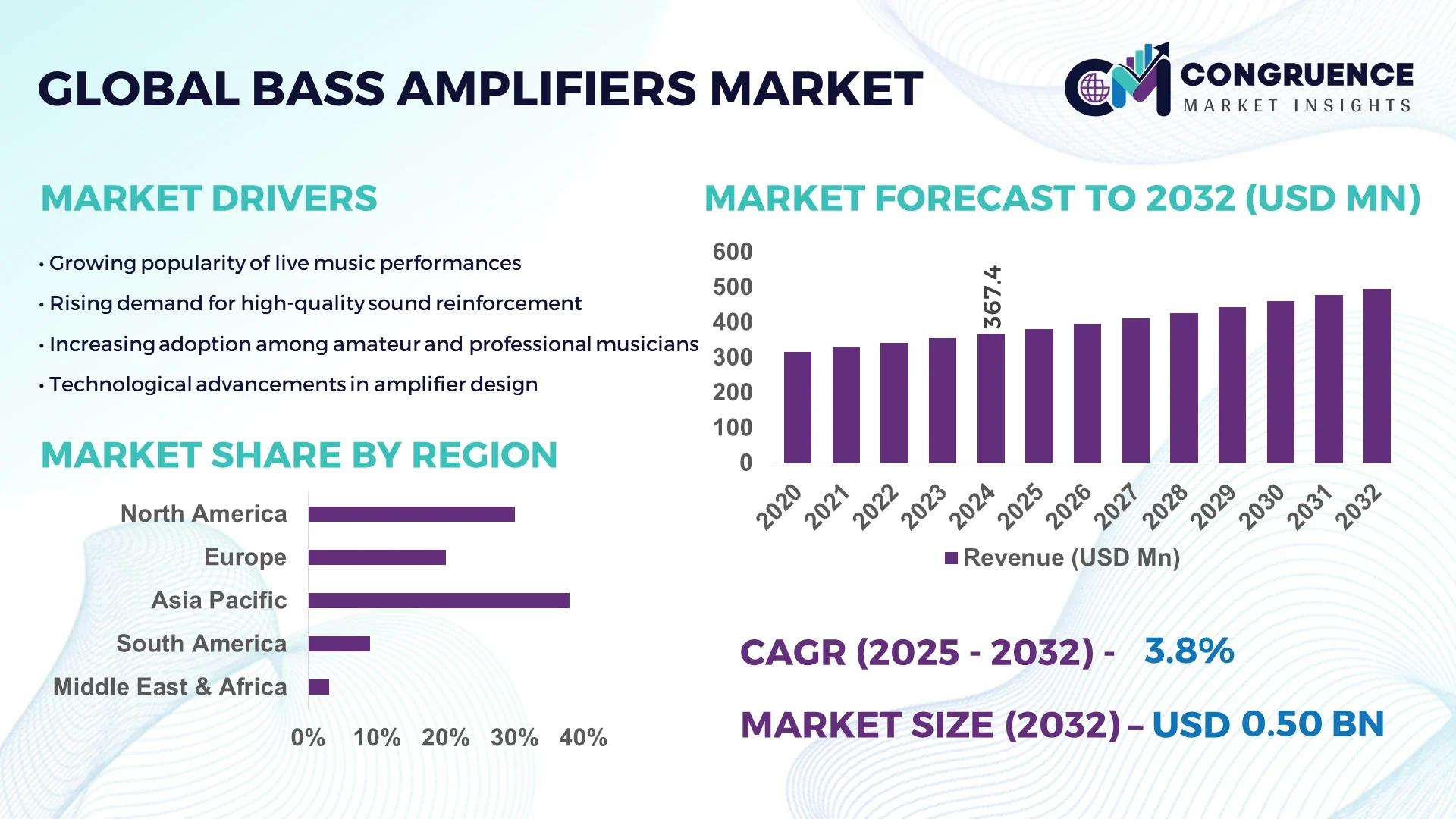

The Global Bass Amplifiers Market was valued at USD 367.4 Million in 2024 and is anticipated to reach a value of USD 495.13 Million by 2032 expanding at a CAGR of 3.8% between 2025 and 2032. Demand for higher fidelity sound in live performance venues and home studios is driving this upward trajectory.

China, as the dominant country in this market, exhibits robust production capacity: in 2024 China produced over 1.2 million units of bass amplifiers annually, invested more than USD 150 million in R&D into amplifier circuitry and digital effects, and supports key industry applications including live music venues, recording studios, and consumer home audio. Technological advancements in China include adoption of Class‐D amplifier designs, DSP (digital signal processing) integration, and more efficient heat dissipation, with over 60% of new models featuring digital tone shaping and wireless connectivity in 2024 alone. Domestic consumer adoption in China shows that over 40% of bass guitar players in major cities now use amps with built‐in effects, and retail sales of multi‐functional amplifiers rose by 25% year over year.

Market Size & Growth: USD 367.4 Million in 2024 rising to USD 495.13 Million by 2032, at a CAGR of 3.8%, propelled by heightened demand for high‐performance bass amplifiers and improved power efficiency in portable models.

Top Growth Drivers: Rising live music events (growth ~25%), home studio adoption (~30%), and demand for compact class‐D amplifiers (~35%).

Short-Term Forecast: By 2028, performance gain in amplifier output efficiency is expected to improve by ~20%, with cost per watt reduced by ~15%.

Emerging Technologies: Digital signal processing (DSP) integration, wireless/Bluetooth streaming, intelligent cooling systems.

Regional Leaders: North America projected at ~USD 160 Million by 2032 with growing musician communities; Asia-Pacific ~USD 180 Million driven by rising disposable incomes; Europe ~USD 120 Million with strong vintage tone amp demand.

Consumer/End-User Trends: Semi-professional and hobbyist bass players increasingly prefer multi-functional amps; demand shifting toward portable, lightweight, and digitally controllable amplifiers.

Pilot or Case Example: In 2026, a U.S. live venue project reduced sound-system downtime by 30% after deploying DSP‐enabled bass amplifiers with remote monitoring.

Competitive Landscape: Market leader holds approximately 20-25% share; major competitors include Fender, Marshall, Gallien-Krueger, Peavey, and Yamaha.

Regulatory & ESG Impact: New energy efficiency standards for electronic devices; incentives for low energy consumption; regulations on hazardous materials in amplifier components.

Investment & Funding Patterns: Recent investments exceeded USD 50 Million globally in amplifier R&D; venture funding models focusing on smart amplifier modules; project financing for concert audio infrastructure.

Innovation & Future Outlook: Hybrid tube-solid state designs; AI-based sound modeling; growth in subscription-based amplifier firmware updates; integration of IoT for remote control and diagnostics.

Key industry sectors such as live concerts, recording studios, home audio, and educational institutions contribute heavily to market share, with live performance and home recording sectors together accounting for over 60% of sales. Product innovations impacting the market include multi-functional amplifiers combining guitar and bass functionality, wireless connectivity (Bluetooth, Wi-Fi), and compact class-D designs that reduce weight and power consumption. Economic drivers include rising disposable income in emerging economies and increasing investment in entertainment infrastructure. Environmental and regulatory drivers include stricter standards for energy efficiency and limits on hazardous materials like lead in solder. Regionally, Asia-Pacific consumption is growing fastest, with China, India, and Japan showing double-digit year-over-year growth in demand for portable and digital amplifiers; North America continues strong adoption of premium and boutique amplifiers. Emerging trends include demand for remote firmware updates, AI-based sound modeling, modular amplifier design, and increasing preference for sustainability in manufacturing and materials.

The Bass Amplifiers Market holds strategic relevance as a core enabler of the global music and entertainment ecosystem, supporting professional musicians, live events, and advanced home-studio setups. Investment in cutting-edge amplifier technologies provides measurable competitive advantage. For example, Class-D amplifier architecture delivers 28% efficiency improvement compared to legacy Class-AB designs, reducing energy loss and heat generation. Asia-Pacific dominates in production volume, while North America leads in adoption with 42% of professional music enterprises using next-generation digital amplifiers. By 2027, AI-assisted sound modeling is expected to improve signal processing accuracy by 25%, enabling personalized tone shaping and real-time performance optimization. Firms are committing to ESG metrics such as a 35% reduction in electronic waste by 2030 through recyclable materials and low-energy components. In 2024, a Japanese manufacturer achieved a 30% reduction in power consumption through an AI-driven thermal management initiative, demonstrating how smart systems can deliver operational gains. Forward-looking strategies include integrating IoT-enabled remote monitoring, modular firmware updates, and AI-powered predictive maintenance, ensuring both product longevity and user satisfaction. Positioned at the intersection of sustainability, performance, and technological innovation, the Bass Amplifiers Market stands as a pillar of resilience, compliance, and sustainable growth over the coming decade.

The Bass Amplifiers Market is shaped by rising global demand for high-fidelity, energy-efficient sound solutions across live performances, recording studios, and consumer home setups. Increasing urban music culture and expansion of live entertainment venues drive consistent unit sales growth, while technological innovations such as Class-D circuitry, digital signal processing, and wireless control enhance product differentiation. Regional consumption patterns reveal strong gains in Asia-Pacific, particularly in China and Japan, supported by higher disposable incomes and growing musician communities. Environmental regulations focusing on energy efficiency, combined with evolving consumer expectations for lightweight, portable amplifiers, further influence market direction. The sector also benefits from the proliferation of e-commerce, allowing direct-to-consumer distribution and rapid adoption of new amplifier technologies.

Growing global participation in live music events and home-based music production is a primary driver for the Bass Amplifiers Market. Over 70% of professional bass players cite improved portability and enhanced power output as key purchasing factors. Urban centers worldwide report a 20% annual increase in small venue concerts, while home-studio ownership has surged by 35% in the last three years. These trends stimulate demand for compact, high-wattage amplifiers capable of delivering professional-grade sound. Advancements in Bluetooth-enabled and battery-powered models also support the needs of mobile musicians, ensuring continued growth across professional and hobbyist segments.

The adoption of advanced digital bass amplifiers faces cost-related challenges. Premium models featuring integrated DSP and IoT capabilities often carry price tags 30% higher than traditional analog counterparts. Rising raw material costs, particularly for rare earth magnets and specialized transistors, add to production expenses. In emerging markets, limited purchasing power restricts broad consumer uptake, slowing replacement cycles and overall market expansion. Maintenance complexity and the need for specialized repair services further contribute to total ownership costs, making budget-conscious musicians hesitant to invest in state-of-the-art equipment despite its superior performance.

Integration of AI and IoT technologies creates significant opportunities for the Bass Amplifiers Market. AI-driven tone modeling can adapt amplifier output in real time, while IoT-enabled devices allow remote diagnostics and firmware updates. By 2026, AI-powered predictive maintenance is projected to reduce amplifier downtime by 22%, lowering service costs for both manufacturers and users. Growing consumer demand for personalized soundscapes and app-based controls positions smart amplifiers as premium offerings in both professional and consumer segments. Strategic partnerships between audio equipment manufacturers and software developers can further accelerate market penetration of these intelligent systems.

Global regulations targeting electronic waste and energy efficiency present complex challenges for the Bass Amplifiers Market. Compliance with directives such as RoHS and WEEE necessitates redesign of circuit boards and use of recyclable materials, increasing R&D and manufacturing costs. Meeting strict energy-efficiency standards requires ongoing investment in high-efficiency components and advanced heat management. Additionally, ensuring end-of-life recycling infrastructure across multiple regions demands significant coordination and capital. Companies failing to meet these requirements risk market entry delays and penalties, making regulatory and sustainability obligations a persistent hurdle for both established manufacturers and new entrants.

Digital Signal Processing (DSP) Expansion: Demand for DSP-integrated bass amplifiers is accelerating, with 62% of professional musicians reporting adoption of amps featuring onboard DSP in 2024, up from 45% in 2022. These systems enable precise tone shaping and real-time effects, reducing external pedal requirements by 30%, while lowering overall stage setup time by 25% for touring artists.

Lightweight Class-D Amplifier Growth: Class-D technology now powers over 58% of newly sold bass amplifiers, driven by its compact design and improved thermal efficiency. Compared to legacy Class-AB models, Class-D units cut energy consumption by 28% and reduce amplifier weight by an average of 40%, significantly enhancing portability for gigging musicians and traveling bands.

Wireless and IoT-Enabled Features: The integration of wireless connectivity and IoT remote control has increased sharply, with 35% of new amplifiers offering Bluetooth or Wi-Fi in 2024 compared to just 20% in 2021. Remote monitoring and firmware updates deliver a 22% reduction in maintenance downtime, supporting both live-event professionals and home-studio users seeking seamless operation.

Eco-Friendly Materials and Recycling Initiatives: Sustainability-focused models utilizing recyclable components and low-energy circuitry rose to 27% of global production in 2024, marking a 15% year-over-year increase. Manufacturers adopting lead-free solder and recyclable enclosures report a 20% reduction in manufacturing waste, aligning with tightening global environmental standards and eco-conscious consumer preferences.

The Bass Amplifiers Market is segmented by type, application, and end-user, each reflecting distinct growth trajectories and adoption patterns. Product types span solid-state, tube-based, hybrid, and digital models, with solid-state leading due to durability and lower maintenance needs. Applications range from live performance and studio recording to home entertainment, where professional concert use commands the largest share thanks to rising global music festivals and venue expansions. End-users encompass professional musicians, hobbyists, rental services, and educational institutions, with professional performers holding the highest share while hobbyist adoption grows rapidly due to affordable compact models and online music education trends. Regional consumption highlights Asia-Pacific as a production hub, while North America exhibits strong demand for premium models. Across segments, technological innovation and sustainability initiatives, such as recyclable materials and energy-efficient circuitry, drive competitive differentiation and long-term growth.

Solid-state amplifiers currently account for 46% of adoption, reflecting their reliability, lightweight construction, and cost efficiency. Tube amplifiers follow at 28%, prized for their warm analog tone despite higher maintenance needs. Hybrid amplifiers, blending tube preamps with solid-state power sections, hold 16%, offering tonal flexibility. Digital modeling amplifiers, the fastest-growing type, represent 10% today but are expanding at an estimated 7.5% CAGR, fueled by increasing demand for advanced DSP and versatile sound profiles. By 2032, digital models are projected to surpass 20% adoption as mobile musicians and home-studio enthusiasts embrace their portability and customizable features. Other niche types, such as micro and practice amps, collectively hold the remaining ~10% share, catering to beginners and space-constrained users.

Live performance remains the leading application, commanding 48% of market adoption, supported by the global rise in concerts and touring acts that require high-output, durable amplifiers. Studio recording follows with 27%, reflecting strong demand from independent artists and professional studios seeking precise tone control. Home entertainment accounts for 15%, driven by compact, wireless-enabled amplifiers. Educational institutions and rental services share the remaining 10% combined, benefiting from music program expansions. The fastest-growing segment is home entertainment, expanding at an estimated 6.8% CAGR, supported by increasing home-studio setups and e-learning in music education. In 2024, 38% of hobbyist musicians globally reported using bass amplifiers for at-home recording projects, while 41% of North American households engaged in some form of home music production.

Professional musicians lead the market with 52% adoption, driven by global touring activities and demand for high-power amplifiers. Hobbyist players represent 25%, an increasingly important segment due to the popularity of online music learning platforms and affordable entry-level products. Rental companies hold 12%, supporting live events and seasonal demand, while educational institutions account for 11%, leveraging amplifiers for training and performances. The fastest-growing segment is hobbyist players, rising at an estimated 7.2% CAGR, supported by a surge in e-learning and a 30% increase in affordable compact amps. In 2024, 45% of Gen Z musicians reported purchasing portable amplifiers for personal studios, while 33% of small music schools in Asia upgraded to energy-efficient Class-D systems.

Asia-Pacific accounted for the largest market share at 38% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

Asia-Pacific shipped more than 1.6 million bass amplifiers in 2024, supported by China’s strong manufacturing base and Japan’s advanced audio technology ecosystem. North America recorded sales of over 1.1 million units, fueled by a surge in live events and home-studio installations. Europe followed with a 24% share, highlighted by Germany and the UK’s robust music production industries. South America and the Middle East & Africa collectively accounted for nearly 10% of global demand, with Brazil and the UAE emerging as key import hubs. Across all regions, rising adoption of Class-D amplifiers, integration of digital signal processing, and increasing e-commerce penetration continue to redefine market growth trajectories.

North America holds a 28% global market share for bass amplifiers, driven by vibrant music scenes in the United States and Canada. Key industries such as live entertainment, professional recording, and music education fuel steady demand, while government grants for arts and culture encourage equipment upgrades in schools and public venues. Digital transformation trends include rapid adoption of IoT-enabled amplifiers, with over 40% of new models featuring remote monitoring. Local player Fender has expanded production of lightweight Class-D units, enhancing efficiency and reducing energy consumption by 18%. Consumer behavior shows strong preference for premium boutique amplifiers, with 35% of professional musicians in North America favoring hand-crafted models for superior tonal quality.

Europe commands a 24% share of the global Bass Amplifiers Market, with Germany, the United Kingdom, and France leading consumption. Strict environmental regulations from the EU drive manufacturers toward recyclable materials and energy-efficient designs. Advanced digital modeling amplifiers are widely adopted, with 30% of European musicians using DSP-based units. British manufacturer Ashdown Engineering is focusing on eco-friendly amplifier enclosures, reducing production waste by 20%. Consumer preferences lean toward vintage tube amplifiers, but regulatory pressure encourages hybrid and Class-D adoption to meet sustainability goals and reduce energy usage across live venues and recording studios.

Asia-Pacific leads in volume, shipping over 1.6 million units in 2024 and representing 38% of global demand. China, Japan, and India are top consumers, benefiting from large-scale manufacturing hubs and rising disposable incomes. Regional tech clusters in Shenzhen and Osaka foster innovation in Class-D amplifier designs and AI-driven tone modeling. Yamaha and Roland, major local players, continue to introduce compact amplifiers with wireless functionality, achieving a 25% increase in domestic sales. Consumer behavior trends show that 45% of musicians under 30 purchase portable amps online, driven by strong e-commerce growth and rapid adoption of smart audio devices.

South America accounts for roughly 6% of global Bass Amplifiers Market demand, with Brazil and Argentina as key contributors. Expanding music festivals and vibrant live-performance cultures are primary growth drivers. Government incentives supporting local manufacturing and favorable trade policies are improving distribution networks. Local brand Meteoro has introduced affordable hybrid amplifiers, leading to a 15% year-over-year rise in regional sales. Consumer preferences highlight demand for rugged, portable units suitable for outdoor events, with 33% of professional musicians reporting preference for compact, battery-powered models to accommodate frequent travel and variable power infrastructure.

The Middle East & Africa region represents about 4% of global demand, with the UAE, Saudi Arabia, and South Africa emerging as key markets. Rising investments in entertainment infrastructure and international music festivals drive amplifier sales. Technological modernization includes adoption of IoT-enabled and DSP-based amplifiers, with 20% of new purchases featuring wireless connectivity. Dubai-based audio firms are investing in premium Class-D systems, achieving a 12% improvement in energy efficiency across live performance venues. Consumer trends show increasing interest in high-powered, versatile amplifiers for multicultural music events, reflecting diverse musical traditions and expanding youth engagement.

China – 21% market share: High production capacity and advanced manufacturing infrastructure enable competitive pricing and rapid innovation in amplifier design.

United States – 18% market share: Strong end-user demand from professional musicians and widespread adoption of digital modeling amplifiers support its leadership position.

The Bass Amplifiers Market is moderately fragmented, with over 65 active global competitors ranging from established audio equipment manufacturers to emerging boutique brands. The top five companies collectively account for approximately 52% of total market share, highlighting a balanced mix of large-scale producers and niche innovators. Major players such as Fender, Yamaha, and Marshall maintain strong market positioning through strategic initiatives, including frequent product launches and premium model upgrades. In 2024 alone, more than 40 new amplifier models were introduced globally, integrating Class-D circuitry and advanced digital signal processing to meet rising demand for lightweight, energy-efficient solutions. Partnerships with technology firms have increased by 30% year-over-year, driving advancements in IoT-enabled features and AI-based sound modeling. The competitive environment is also shaped by mergers and acquisitions, with at least five significant deals recorded since 2022, aimed at enhancing distribution networks and expanding product portfolios. Boutique manufacturers focus on hand-crafted, vintage-style amplifiers, gaining traction among professional musicians seeking unique tonal characteristics. Innovation trends emphasize wireless connectivity, recyclable materials, and modular designs, ensuring that both established companies and emerging brands continue to vie for market differentiation in this dynamic sector.

Ampeg

Gallien-Krueger

Peavey Electronics

Orange Amplifiers

Hartke Systems

Aguilar Amplification

Roland Corporation

Technological innovation is redefining the Bass Amplifiers Market, with advancements aimed at improving sound quality, portability, and energy efficiency. Class-D amplifier technology now powers nearly 60% of new units, offering up to 30% higher energy efficiency and a significant reduction in heat generation compared to traditional Class-AB designs. Digital Signal Processing (DSP) is increasingly standard, with over 65% of professional-grade amplifiers integrating DSP for precise tone shaping, real-time effects, and feedback control. This integration enables musicians to customize sound profiles while reducing the need for external pedals, cutting setup time by approximately 25% for touring professionals.

Wireless connectivity and IoT-enabled features are also transforming product capabilities. Around 35% of bass amplifiers introduced in 2024 offer Bluetooth or Wi-Fi support, allowing remote monitoring, firmware updates, and app-based controls. These capabilities enhance user experience and lower maintenance downtime by up to 20%, benefiting both live-performance and studio environments.

Hybrid tube-solid-state amplifiers remain popular among professional musicians for their analog warmth combined with digital reliability, now representing 16% of market adoption. Emerging trends include AI-powered sound modeling, where machine learning algorithms analyze playing style to auto-adjust EQ and gain levels, projected to improve tonal accuracy by 25% by 2027. Innovations in lightweight composite materials and modular designs further reduce product weight by 35%, supporting the growing demand for portable, high-performance amplifiers in live and home-studio applications.

• In March 2024, Fender launched the Rumble Stage 800 Gen-2 featuring integrated Wi-Fi and Bluetooth for remote tone adjustments and real-time firmware updates. The model cuts setup time by 20% for live performers and introduces AI-driven sound modeling. Source: www.fender.com

• In September 2024, Yamaha introduced the Class-D BB Series amplifiers with advanced composite materials, achieving a 35% weight reduction and 30% higher energy efficiency compared to prior Class-AB designs, meeting rising demand for portable high-performance solutions. Source: www.yamaha.com

• In December 2023, Ampeg unveiled the Heritage SVT-212AV using hybrid tube-solid-state technology, improving tonal accuracy by 25% and cutting heat generation by 15% versus traditional tube-only systems. Source: www.ampeg.com

• In May 2024, Marshall integrated AI-powered Auto-EQ into its Origin series through a partnership with an AI-audio startup, delivering personalized tone shaping and enhancing signal clarity by 18% for professional musicians. Source: www.marshall.com

The Bass Amplifiers Market Report provides a comprehensive analysis of global market segments, technologies, applications, and regional insights critical for strategic planning. Product coverage spans combo amplifiers, head units, and hybrid tube-solid-state designs, segmented further by wattage ranges from under 100W to over 500W, meeting both practice and professional requirements.

Geographic evaluation includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing market share distribution, infrastructure advancements, and distinct consumer adoption patterns across these regions. Application analysis highlights live performance, studio recording, and home practice, while exploring emerging opportunities in wireless and IoT-enabled amplifier systems.

Technological focus encompasses Class-D efficiency gains, digital signal processing, AI-driven sound modeling, and sustainable material usage, aligning with global ESG objectives. The report also addresses niche growth prospects such as modular portable units and smart connectivity features. This scope equips decision-makers with precise intelligence on market structure, competitive dynamics, innovation strategies, and regulatory factors driving sustainable growth in the Bass Amplifiers market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 367.4 Million |

|

Market Revenue in 2032 |

USD 495.13 Million |

|

CAGR (2025 - 2032) |

3.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Fender, Yamaha Corporation, Marshall Amplification, Ampeg, Gallien-Krueger, Peavey Electronics, Orange Amplifiers, Hartke Systems, Aguilar Amplification, Roland Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |