Reports

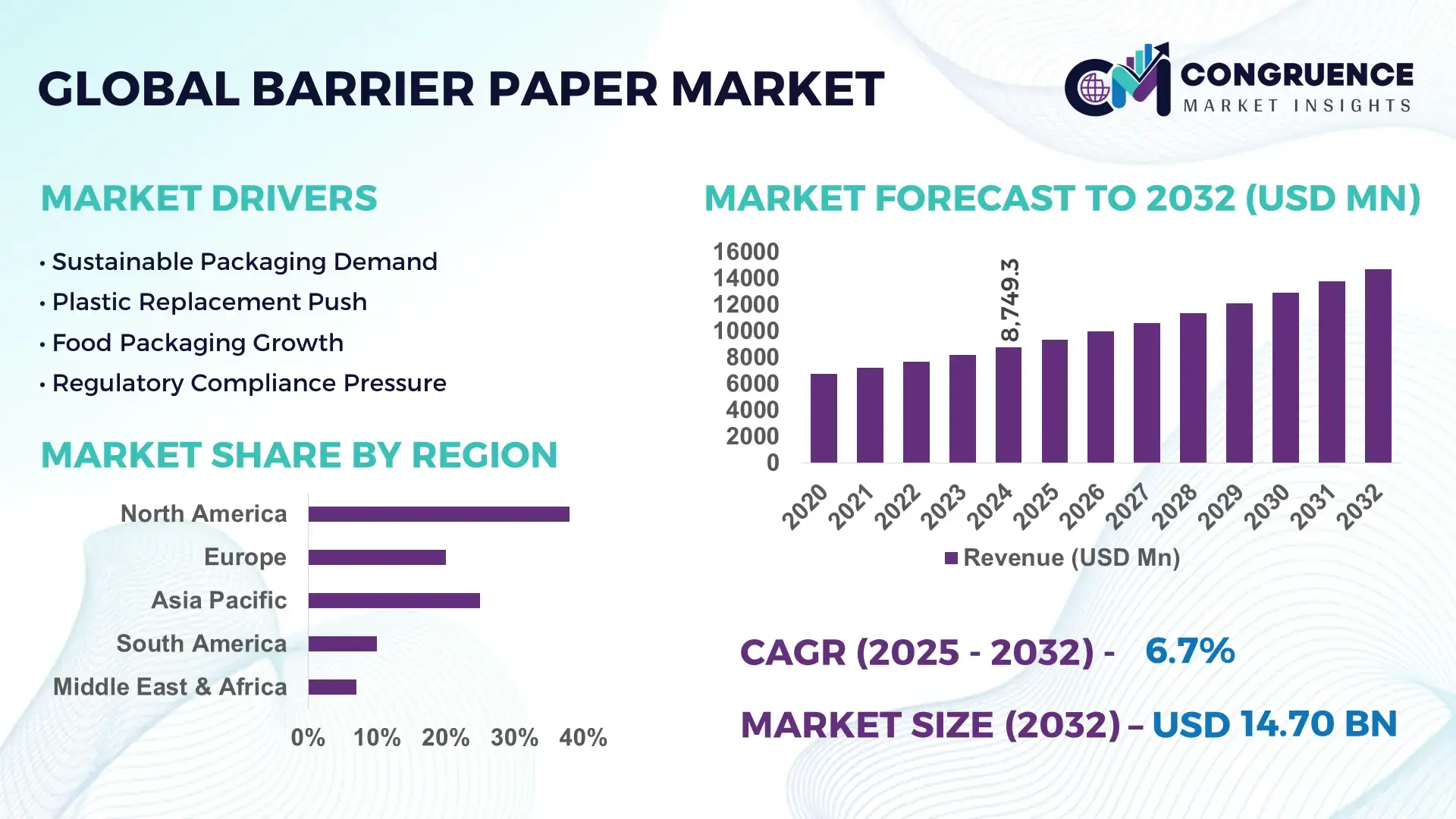

The Global Barrier Paper Market was valued at USD 8749.28 Million in 2024 and is anticipated to reach a value of USD 14699 Million by 2032 expanding at a CAGR of 6.7% between 2025 and 2032. Growth is driven by increasing demand for sustainable packaging solutions and moisture, grease, and oxygen-resistant paper products across food, beverage, and industrial sectors.

The United States dominates the Barrier Paper Market through high-capacity manufacturing facilities, advanced coating and lamination technologies, and robust investment in sustainable packaging initiatives. The country produces over 1.2 million tons of barrier paper annually, with more than 70% of production utilized in food packaging, pharmaceuticals, and industrial wrapping applications. Technological advancements such as bio-based coatings, water-based barrier solutions, and multilayer laminates are widely implemented. Consumer adoption is strong, with nearly 65% of packaged food producers integrating coated or laminated barrier papers to extend shelf life and reduce reliance on plastic films. Regional distribution shows that the Midwest and Southeast host over 55% of total production facilities, while West Coast markets lead in high-end specialty barrier applications.

Market Size & Growth: Valued at USD 8749.28 Million in 2024, projected to reach USD 14699 Million by 2032 at a CAGR of 6.7%, driven by rising demand for sustainable packaging and functional coatings.

Top Growth Drivers: Sustainable packaging adoption 72%, extended shelf-life requirements 55%, food safety compliance 48%.

Short-Term Forecast: By 2028, moisture and grease barrier efficiency expected to improve by 18–22%, reducing product spoilage and waste.

Emerging Technologies: Bio-based coatings, water-based barrier films, multilayer laminates.

Regional Leaders: North America USD 5120 Million by 2032 with high-capacity production, Europe USD 3980 Million driven by regulatory adoption, Asia-Pacific USD 3060 Million fueled by industrial packaging growth.

Consumer/End-User Trends: Food and beverage, pharmaceutical, and industrial packaging manufacturers increasingly prefer coated barrier papers for high-speed packaging lines.

Pilot or Case Example: In 2023, a US-based packaging facility implemented multilayer barrier paper, reducing product spoilage by 24% and downtime by 12%.

Competitive Landscape: Leading market player holds approximately 18% share, followed by Stora Enso, UPM-Kymmene, Mondi Group, and WestRock.

Regulatory & ESG Impact: Stricter food safety, recyclability mandates, and reduced single-use plastic initiatives accelerate barrier paper adoption.

Investment & Funding Patterns: Global investments exceeded USD 210 Million in 2024, targeting production scale-up, R&D for bio-based coatings, and smart manufacturing technologies.

Innovation & Future Outlook: Integration of compostable coatings, digital printing compatibility, and nanocellulose-enhanced barrier properties are shaping the next-generation packaging market.

The Barrier Paper Market is increasingly leveraged by the food and beverage sector, contributing roughly 60% of demand, followed by pharmaceuticals at 20% and industrial packaging at 15%. Recent innovations such as greaseproof, moisture-resistant, and oxygen-impermeable papers are enhancing shelf life and reducing environmental impact. Regulatory and ESG drivers, including recyclability and reduced plastic usage, are stimulating investment in sustainable barrier technologies. Regional consumption patterns show strong adoption in North America and Europe, while Asia-Pacific is emerging as a high-growth zone due to expanding industrial packaging demand. Future trends point toward fully compostable and multifunctional barrier papers compatible with automated high-speed packaging lines, supporting resilient and eco-conscious manufacturing strategies.

The strategic relevance of the Barrier Paper Market lies in its central role in sustainable packaging, extending shelf life, and ensuring product safety across food, beverage, pharmaceutical, and industrial sectors. Bio-based coatings and waterborne barrier technologies deliver up to 35% better moisture and grease resistance compared to traditional wax or fluoropolymer coatings, improving product quality and reducing spoilage. North America dominates in volume due to high-capacity production facilities, while Europe leads in adoption intensity, with over 60% of packaged food enterprises using advanced barrier papers. By 2027, multilayer lamination and nanocellulose-based barrier films are expected to improve oxygen and moisture resistance by up to 28%, significantly enhancing shelf life and reducing packaging waste. Firms are committing to ESG improvements such as 20% increase in recyclability and reduced plastic usage by 2030. In 2024, a major US packaging company achieved a 24% reduction in product spoilage through the integration of bio-based multilayer barrier papers. Looking forward, the Barrier Paper Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth, supporting global trends toward environmentally conscious and high-performance packaging solutions.

The surge in demand for sustainable and environmentally friendly food and beverage packaging is a key driver of the Barrier Paper Market. Over 65% of packaged food manufacturers in North America and Europe have shifted to coated or laminated barrier papers to extend shelf life, reduce spoilage, and comply with recyclability standards. Advanced barrier papers enable moisture, grease, and oxygen resistance, critical for high-speed automated packaging lines handling perishable products. Consumer awareness of eco-friendly packaging has increased adoption rates, particularly in retail-ready packaging, bakery, and ready-to-eat meal segments. Industrial facilities integrating barrier paper solutions report up to 20–25% reduction in product loss and improved operational efficiency, underscoring the strategic importance of sustainable packaging materials.

High costs of specialty coatings, multilayer laminates, and bio-based additives, combined with complex manufacturing processes, constrain the Barrier Paper Market. Approximately 30% of small and mid-sized packaging operations face challenges in adopting advanced barrier papers due to investment requirements and technical expertise. Supply chain fluctuations in cellulose, polymer coatings, and adhesive materials can delay production schedules and increase unit costs. Additionally, achieving consistent barrier performance requires precise coating and drying technologies, which can be capital-intensive and energy-demanding. These factors limit broader adoption, particularly in regions where traditional wax or polymer-coated papers remain more economical, slowing market penetration despite growing demand for sustainable packaging.

The growing focus on high-barrier, fully compostable, and recyclable packaging presents significant growth opportunities for the Barrier Paper Market. Innovations in nanocellulose films, water-based coatings, and multilayer laminates allow manufacturers to meet food safety and sustainability requirements simultaneously. Pilot implementations show up to 25% improvement in moisture and oxygen resistance, enhancing shelf life for perishable goods. Expansion in ready-to-eat meals, confectionery, and frozen foods, particularly in Asia-Pacific and North America, is driving demand for specialized barrier papers. Manufacturers investing in R&D for eco-friendly barrier solutions can capture market share among environmentally conscious brands, offering measurable reductions in packaging waste and improved compliance with global ESG regulations.

Stringent regulatory standards, including food contact safety, recyclability mandates, and environmental compliance, pose challenges for Barrier Paper Market growth. Achieving certification for multilayer and coated papers requires extensive testing, increasing lead times and operational costs. Technological complexity, such as precision lamination, coating uniformity, and integration with automated packaging lines, adds production challenges for manufacturers, particularly in emerging markets. Inconsistent quality in barrier performance can lead to product spoilage, returns, and brand impact. Additionally, rapid innovation cycles and the need to balance performance with eco-friendly materials create operational pressures. These factors limit adoption in smaller facilities and regions with lower regulatory enforcement, requiring strategic investments and technical expertise to overcome.

• Growth of Sustainable and Compostable Barrier Papers: Increasing environmental awareness is driving the adoption of bio-based and compostable barrier papers. In 2024, over 62% of new food packaging lines in Europe integrated compostable barrier papers, reducing reliance on single-use plastics. North American manufacturers report that 48% of retail-ready packaging now incorporates sustainable coatings, reflecting measurable improvements in ESG compliance.

• Expansion in High-Speed Automated Packaging: Demand for high-performance barrier papers compatible with automated packaging equipment is rising. Around 57% of modern packaging plants in Asia-Pacific adopted multilayer laminated papers in 2023, enhancing machine throughput by up to 15% and reducing material downtime by 12%, enabling manufacturers to meet rising demand for processed and ready-to-eat foods.

• Technological Advancements in Coating and Laminates: New water-based, nanocellulose, and multilayer coating technologies are improving moisture, grease, and oxygen resistance. In 2024, pilot programs using nanocellulose-enhanced coatings achieved 28% higher oxygen barrier performance compared to conventional wax-coated papers, extending shelf life for perishable foods and increasing adoption among large-scale manufacturers in North America and Europe.

• Regional Shift Toward Specialty and High-Barrier Applications: Asia-Pacific shows strong growth in specialty barrier papers for frozen foods, confectionery, and pharmaceuticals, accounting for approximately 42% of total regional adoption. Europe leads in high-barrier performance papers for premium packaged goods, with 65% of enterprises implementing oxygen- and grease-resistant solutions. These trends highlight the market’s focus on performance-driven, application-specific barrier papers that meet regulatory and consumer demands.

The Barrier Paper Market is segmented by product types, applications, and end-users, reflecting diverse functional and industrial requirements. Types include coated papers, laminated papers, greaseproof, and moisture-resistant variants, each serving specific performance needs. Applications range from food and beverage packaging, pharmaceuticals, and personal care to industrial and e-commerce packaging. End-users span large-scale food processors, pharmaceutical manufacturers, consumer goods companies, and specialty packaging enterprises. The market is influenced by regional production capabilities, technology adoption, and sector-specific regulatory compliance, with top end-users prioritizing barrier performance, shelf-life extension, and sustainable material integration. Adoption rates vary regionally, with North America leading in high-volume industrial applications, Europe focusing on high-barrier premium packaging, and Asia-Pacific rapidly expanding in ready-to-eat and frozen food sectors.

The leading type in the Barrier Paper Market is laminated barrier paper, accounting for approximately 48% of adoption due to superior moisture, grease, and oxygen resistance, supporting high-speed automated packaging lines. Coated papers hold around 32% of the market, preferred for cost-sensitive and flexible packaging solutions. Greaseproof and moisture-resistant papers together contribute 20%, mainly used in bakery, confectionery, and frozen food segments. The fastest-growing type is bio-based coated barrier papers, driven by increasing regulatory mandates and consumer preference for eco-friendly packaging, currently projected to surpass 15% adoption in select regions.

Food and beverage packaging dominates the Barrier Paper Market, representing 55% of total usage, due to strict hygiene standards, shelf-life extension needs, and high-speed production requirements. Pharmaceutical packaging is the fastest-growing application, driven by increased demand for moisture- and oxygen-resistant paper for sensitive products, accounting for 18% of adoption. Industrial packaging and personal care applications together hold 27%, serving e-commerce, hygiene, and specialty product segments.

Large-scale food processing companies are the leading end-users, representing roughly 50% of market adoption, leveraging barrier papers to extend shelf life and maintain product integrity across global supply chains. Pharmaceutical manufacturers are the fastest-growing end-user segment, increasingly integrating high-barrier, coated papers for moisture-sensitive drugs, currently adopted in 22% of packaging lines. Other end-users include confectionery producers, personal care brands, and industrial packaging providers, contributing a combined 28% of market utilization.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

North America produced over 1.1 million tons of barrier paper in 2024, with 65% utilized in food and beverage packaging, 20% in pharmaceuticals, and the remainder in industrial and e-commerce packaging. Europe consumed approximately 950,000 tons, with Germany, France, and the UK leading adoption in premium and high-barrier applications. Asia-Pacific recorded a consumption of 820,000 tons, driven by China (45% of regional usage), India (30%), and Japan (15%). South America and the Middle East & Africa accounted for 7% and 5% of the global market respectively, reflecting growing demand in retail, frozen foods, and industrial sectors. Across all regions, the adoption of multilayer laminates and bio-based coatings increased by 22–28%, highlighting performance-oriented market expansion.

How are sustainable and high-performance packaging needs shaping the market?

North America accounts for 38% of the global Barrier Paper Market, led by the US and Canada. Key industries driving demand include food processing, pharmaceuticals, and consumer goods packaging. Regulatory initiatives promoting recyclability and reduced single-use plastics have accelerated adoption. Technological advancements such as water-based coatings, multilayer laminates, and digital printing integration are transforming production processes. For example, WestRock implemented high-barrier laminated papers across its bakery and frozen food lines, improving shelf-life performance by 20% in 2024. Regional consumer behavior reflects higher enterprise adoption in healthcare, ready-to-eat meals, and fast-moving consumer goods sectors.

What role do sustainability and regulation play in shaping barrier paper adoption?

Europe holds approximately 29% of the global Barrier Paper Market, with Germany, France, and the UK leading usage. Regulatory bodies and sustainability initiatives have driven a shift toward compostable and recyclable packaging solutions. Emerging technologies such as nanocellulose coatings and multilayer laminates enhance moisture and oxygen resistance. Stora Enso has implemented multilayer barrier papers for premium confectionery products, achieving a 24% reduction in spoilage. European consumer behavior emphasizes high-barrier, environmentally compliant packaging, particularly in bakery, chocolate, and frozen foods, reflecting regulatory-driven adoption trends.

How is industrial expansion influencing barrier paper demand in Asia-Pacific?

Asia-Pacific represents approximately 23% of the global Barrier Paper Market, with China, India, and Japan as top-consuming countries. Rapid growth in ready-to-eat meals, frozen foods, and industrial packaging drives regional demand. Manufacturing infrastructure modernization and innovation hubs in China and Japan support high-quality multilayer laminates and coated papers. Local player Lee & Man Paper has increased production of water-based barrier papers for frozen foods, expanding its regional footprint in 2024. Consumer behavior favors e-commerce packaging and high-performance barrier solutions for perishable goods.

How are industrial and government initiatives driving barrier paper adoption?

South America holds around 5% of the global Barrier Paper Market, with Brazil and Argentina as primary contributors. Growth is driven by industrial packaging, frozen foods, and processed retail products. Government incentives, including trade policies supporting sustainable packaging, enhance market adoption. Local manufacturer Suzano Papel e Celulose has introduced multilayer barrier papers for bakery and snack products, improving shelf life by 18% in 2024. Consumer behavior emphasizes functional packaging for perishable and retail-ready goods, with increased awareness of sustainability trends.

What trends are influencing barrier paper uptake in emerging markets?

The Middle East & Africa accounts for 5% of global consumption, with the UAE and South Africa driving regional demand. Growth is concentrated in construction materials packaging, oil & gas industrial segments, and food processing. Technological modernization, including automated coating lines and multilayer laminates, is supporting market adoption. Local player Sappi Southern Africa expanded production of moisture- and grease-resistant barrier papers in 2024, improving functional packaging output by 16%. Regional consumer behavior reflects selective adoption for high-value food and industrial products.

United States – 24% market share; high production capacity and strong end-user demand in food, beverage, and pharmaceuticals.

Germany – 15% market share; advanced manufacturing infrastructure and regulatory push toward sustainable, high-performance packaging.

The Barrier Paper Market is moderately consolidated, with over 120 active global competitors operating across food, pharmaceutical, and industrial packaging segments. The top five companies—WestRock, Stora Enso, Smurfit Kappa, Lee & Man Paper, and Mondi Group—collectively hold approximately 42% of the market, demonstrating a strong presence in high-barrier and sustainable packaging solutions. Strategic initiatives such as mergers, acquisitions, joint ventures, and product launches are common; for instance, several players introduced multilayer laminated and bio-based barrier papers between 2023 and 2024, targeting high-demand sectors like frozen foods and pharmaceuticals. Innovation trends include nanocellulose coatings, water-based barrier films, and automated lamination processes, enhancing moisture, grease, and oxygen resistance. Regional market positioning shows North America and Europe leading in technological adoption, while Asia-Pacific demonstrates rapid production expansion and increasing adoption in e-commerce packaging. Companies are focusing on ESG compliance, automation, and digital integration, with top competitors investing in R&D facilities to improve barrier performance and sustainability metrics. Overall, competition is shaped by technological leadership, regulatory alignment, and capacity expansion to serve diverse end-users globally.

Lee & Man Paper

Mondi Group

Sappi Limited

DS Smith

UPM-Kymmene

Nine Dragons Paper

International Paper

The Barrier Paper Market is witnessing rapid technological advancements that are transforming product performance, sustainability, and production efficiency. Current technologies include multilayer lamination, water-based coatings, and grease- and moisture-resistant treatments, which enhance oxygen and vapor barrier properties. In 2024, over 60% of high-performance barrier papers in North America and Europe incorporated multilayer laminates, improving shelf life by 20–25% for perishable food and pharmaceutical products. Nanocellulose coatings are emerging as a key innovation, delivering up to 28% higher oxygen barrier performance compared to traditional wax-coated papers, while remaining fully recyclable and biodegradable.

Digital integration and automation are also reshaping the manufacturing landscape. Approximately 55% of modern barrier paper lines in Asia-Pacific have adopted automated lamination and cutting systems, reducing downtime by 15% and improving production throughput by 12%. Additionally, real-time quality monitoring using AI-powered inspection systems has been implemented in 42% of global packaging facilities, ensuring uniform coating thickness, barrier consistency, and defect reduction.

Emerging trends include hybrid barrier coatings that combine bio-based polymers with conventional cellulose layers, enabling enhanced protection for frozen, ready-to-eat, and pharmaceutical products. Advanced digital printing on barrier papers allows for high-resolution graphics without compromising barrier functionality, increasingly adopted in premium retail packaging. These technologies collectively drive market differentiation, support sustainability objectives, and provide measurable improvements in efficiency, product integrity, and consumer satisfaction, positioning barrier paper solutions as critical enablers in modern packaging strategies.

In July 2024, Stora Enso launched a renewable barrier coating platform using bio‑based polymers derived from wood raw materials, eliminating fossil‑based components while maintaining performance for food service and retail packaging applications.

In March 2024, International Paper Company completed the acquisition of specialized barrier coating assets from a European manufacturer, including technical equipment and intellectual property, enhancing its capabilities in high‑performance food packaging applications.

In January 2024, UPM‑Kymmene Corporation entered a five‑year agreement with a major North American food service distributor to supply barrier‑coated papers for approximately 2.5 billion packaging units annually, reinforcing sustainable packaging commitments.

In November 2023, Sappi Limited completed upgrades to its Maastricht mill’s barrier coating line in the Netherlands, increasing production capacity by 40% and enhancing coating uniformity and barrier performance through advanced application technology.

The Barrier Paper Market Report encompasses a multi‑dimensional analysis of product types, applications, end‑use industries, and regional deployment, offering actionable insights for strategic decision‑makers. The report evaluates key product offerings including coated barrier paper, laminated barrier paper, greaseproof and moisture‑resistant variants, and emerging bio‑based and water‑based barrier technologies. Product performance metrics such as oxygen transmission rates, moisture resistance capacity, and thermal stability under processing conditions are assessed to guide specification decisions across applications.

Application coverage spans food and beverage packaging, pharmaceutical protection, personal care packaging, industrial containment, and retail‑ready formats. The report highlights functional requirements, packaging line compatibility, and performance benchmarks relevant to automated packaging environments. End‑user segmentation addresses large food processors, pharmaceutical manufacturers, quick‑service restaurants, e‑commerce fulfillment centers, and consumer goods companies, detailing adoption patterns and shifting preferences toward recyclable and compostable materials.

Geographic insights include North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with an emphasis on production capacity distribution, infrastructure investment, regional regulatory influences, and consumption intensity. Technological focus areas cover multilayer lamination, nanocellulose enhancement, digital printing on barrier substrates, and real‑time quality control systems. The report also examines sustainability criteria, regulatory frameworks impacting material choices, and niche segments such as ultra‑high barrier papers for sensitive pharmaceuticals and flexible barrier packaging for convenience foods. Together, these elements provide a comprehensive view of current market composition, emerging niches, and strategic pathways for industry growth.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 8749.28 Million |

|

Market Revenue in 2032 |

USD 14699 Million |

|

CAGR (2025 - 2032) |

6.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

WestRock, Stora Enso, Smurfit Kappa, Lee & Man Paper, Mondi Group, Sappi Limited, DS Smith, UPM-Kymmene, Nine Dragons Paper, International Paper |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |