Reports

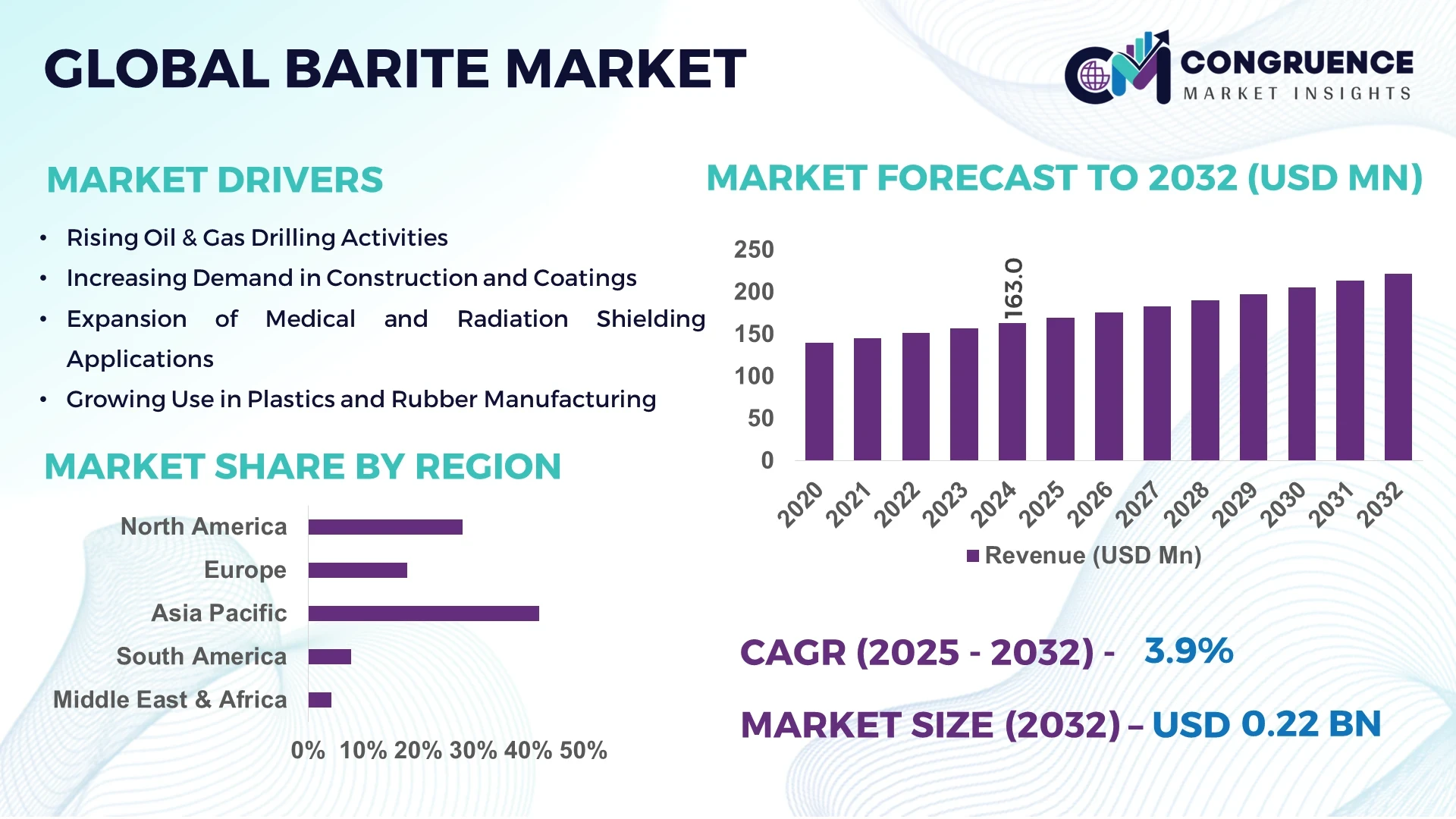

The Global Barite Market was valued at USD 163.0 Million in 2024 and is anticipated to reach a value of USD 221.4 Million by 2032 expanding at a CAGR of 3.9% between 2025 and 2032.

China leads the Barite Market with annual production capacity exceeding 3.6 million tonnes and investments exceeding USD 50 million in modern beneficiation and grinding facilities. The country’s industry supports extensive downstream uses in drilling fluids, fillers, and heavyweight aggregate applications, utilizing high-density purification technologies and automated quality-control systems to meet industrial demand.

Across the Barite Market, the oil and gas sector dominates demand through heavy reliance on barite-laden drilling muds, while the plastics, rubber, and coatings industries drive secondary consumption via filler applications. Technological progression includes micronized barite grades offering improved dispersion and reduced wear in equipment, along with enhanced radiopaque formulations tailored for radiation shielding in medical and construction settings. Environmental and regulatory pressures are encouraging adoption of cleaner mining techniques, lower-emission transport, and reclamation-led extraction methods. Regional consumption is highest in Asia-Pacific due to rapid infrastructure development and hydrocarbon exploration, while North America sustains demand through shale drilling operations and high-purity industrial uses. Emerging trends include development of nano-grade barite for advanced composites, regional partnerships for localized production, and integration of digital traceability in logistics. The market outlook points toward continued diversification through applications beyond oilfield use and investments in sustainable supply chain resilience.

AI is increasingly reshaping decision-making, production optimization, and supply chain efficiency within the Barite Market. In mining operations and processing plants, AI-driven process control is enabling real-time adjustments to grinding mill speed and classifier settings—reducing energy usage by approximately 12% and increasing particle-size consistency. AI-enabled computer vision systems supervise barite crushing and sizing, detecting sub-optimal particle distributions and triggering automated corrections that enhance throughput quality and reduce manual interventions.

Supply chain logistics within the Barite Market are also being transformed: advanced AI-powered forecasting tools now dynamically predict demand for drilling-grade barite based on live drilling activity, leading to optimized inventory levels and reducing lead times by up to 20%. Autonomous drones and AI-driven route optimization support faster and more reliable delivery of barite to well sites and industrial users, particularly in remote regions.

On the quality assurance front, machine learning models trained on spectral data can identify contamination or moisture content anomalies in ground barite, enabling rejection or reprocessing before shipping—a step that previously required manual sampling and lab testing. AI also assists in predictive maintenance of crushing and milling lines by analyzing vibration and temperature patterns, allowing preemptive servicing and avoiding unplanned downtime.

These AI innovations are helping Barite Market stakeholders—from miners and processors to logistics teams and industrial users—boost operational precision, reduce waste, and elevate reliability, positioning strategic decision-makers to optimize both cost and performance in a resource-sensitive market.

"In early 2024, a barite processing plant implemented an AI model that reduced grinding energy consumption by 10%, while increasing uniformity of particle size distribution by 15%."

Market dynamics in the Barite Market reflect evolving demand patterns across energy, construction, and materials sectors. The critical role of barite in drilling fluids for oil and gas exploration anchors its steady demand, while expanding industrial manufacturing—especially in plastics, coatings, and composites—is widening its consumption base. Supply dynamics are shaped by expansions in mining throughput and beneficiation capabilities, especially in production hubs, amid environmental regulations pushing for lower-impact extraction. Innovations in micronized and nano-grade barite enhance formulation performance, and diversification into radiation protection and additive manufacturing domains supports long-term growth. Regional disparities in infrastructure, energy projects, and industrial development—particularly in Asia-Pacific and North America—create segmentation opportunities. In response, industry players are investing in vertical integration, digital quality monitoring, and sustainable logistics to strengthen competitiveness in the Barite Market.

The driver underpinning market growth in the Barite Market is the sustained need for high-density barite in drilling mud formulations, particularly in deepwater and shale operations. Meanwhile, increased consumption by the plastics, rubber, and coatings sectors—where barite enhances product performance as a filler—continues to broaden use cases. Industrial players are responding by deploying high-output mining processing lines capable of delivering ultra-fine and heavy-density grades, supporting both energy-sector requirements and downstream manufacturing demands. This dual demand from oilfield and industrial filler applications drives infrastructure investments and supply chain optimization.

One key restraint in the Barite Market stems from tighter environmental and mining regulations. Strict permitting processes, mined-land reclamation requirements, and tighter emissions monitoring can delay expansion of existing mines or restrict new mine development. Additionally, inefficient logistics infrastructure in remote mining areas can raise freight costs and diminish supply reliability. These factors introduce operational complexity and increase time to market for barite producers, particularly in high-demand regions.

Opportunities in the Barite Market lie in development of high-purity micronized barite grades suitable for advanced composites, radiation shielding construction materials, and medical imaging use. Producers investing in classification technologies and washing systems can tap into premium margins in non-oilfield applications. Additionally, growing interest in green construction—leveraging barite’s radiation-blocking properties—opens demand in healthcare and nuclear facilities. Regional plants adopting modular beneficiation units can quickly adapt to shift demand, enabling entry into niche markets.

The Barite Market faces the challenge of volatility tied to fluctuations in oil and gas exploration activity and commodity pricing. Periods of reduced drilling activity can result in substantial declines in drilling mud demand, leading to inventory buildup and margin pressure. Commodity price instability affects cost visibility and contract planning, challenging producers and buyers alike. Hedging logistics and maintaining production flexibility are thus critical to managing exposure in this cyclical market environment.

Advanced Micronized Grades Gain Traction: The Barite Market is seeing increased adoption of ultra-fine barite with particle sizes under 10 μm, which now account for over 30% of total processed tonnage in select production facilities, driven by demand from high-performance fillers and composite applications.

Radiation Shielding Uses Expand: Barite-enhanced concrete and composite panels are being specified in 15% more new healthcare and nuclear facility projects compared to the previous two years, reflecting growing demand for radiation protection materials.

Automated Quality Control Systems Roll Out: Production plants equipped with AI-based vision systems are inspecting mill output in real-time, enabling a 25% reduction in out-of-spec shipments and assuring consistency in bulk density and impurity levels.

Regional Localization of Supply Chains: In regions like Southeast Asia and West Africa, localized beneficiation and packaging facilities are being established within 300 km of mining sites—shortening lead times by up to two weeks and reducing logistics-related carbon footprint.

The Global Barite Market is segmented by type, application, and end-user, each of which plays a pivotal role in shaping the industry landscape. Type segmentation highlights the differences between drilling grade, chemical grade, and filler grade barite, with drilling grade maintaining dominance due to its critical use in oilfield operations, while micronized and specialty grades are gaining importance in advanced manufacturing. Application-wise, oil and gas drilling continues to drive the majority of demand, supported by ongoing exploration and production activities, whereas emerging sectors such as medical, coatings, and radiation shielding are steadily strengthening their share. End-user insights indicate that the energy sector holds the largest portion of demand, while industries such as construction, healthcare, and manufacturing are expanding their reliance on high-purity barite for value-added applications. Together, these segments reveal a dynamic market where traditional drivers remain strong but diversification is creating new growth opportunities.

Drilling grade barite represents the leading type in the market, primarily due to its indispensable role as a weighting agent in drilling fluids used in oil and gas exploration. Its ability to control well pressure and prevent blowouts makes it the most demanded category across both onshore and offshore projects. Micronized barite, often categorized under filler grade, is emerging as the fastest-growing type. Its finely ground particles provide enhanced dispersion and improved performance when used in paints, plastics, and rubber products, particularly in high-performance coatings where density and durability are essential. Chemical grade barite, while smaller in overall consumption, plays a specialized role in producing barium-based chemicals such as barium carbonate, which are used in glassmaking and ceramics. High-purity and specialty grades also serve niche applications in radiation shielding and medical imaging. The diversity of these types ensures that barite maintains relevance across traditional and emerging industries, while innovation in micronized products is driving its wider adoption.

The oil and gas drilling segment remains the leading application of barite, accounting for the majority of consumption due to its effectiveness in controlling hydrostatic pressure in wells. Its high density and insolubility make it a critical component in drilling muds, especially in deepwater and unconventional drilling projects. The fastest-growing application, however, is radiation shielding, where barite is incorporated into concrete and panels for hospitals, laboratories, and nuclear facilities. Growing safety standards and infrastructure projects in healthcare are fueling demand in this area. In addition, barite’s role in paints and coatings continues to be significant, providing gloss control, chemical resistance, and stability. Plastics and rubber industries also utilize barite as a filler to enhance strength and durability. Smaller but valuable applications include barite’s use in medical diagnostics as a radiopaque contrast agent. This broad application base underscores the mineral’s importance across critical industries, with oilfield use providing stability and non-oilfield applications driving diversification.

The energy sector dominates the end-user landscape, led by oil and gas companies that rely heavily on drilling grade barite for exploration and production activities. The continued demand for hydrocarbons, particularly in developing economies, ensures the sector’s leading position. The fastest-growing end-user segment is healthcare, where barite is increasingly used in radiation shielding construction and medical imaging applications, reflecting rising healthcare infrastructure investments and stricter safety regulations. The construction industry also represents a significant end-user, employing barite in specialized concrete and aggregates for radiation protection in large-scale projects. Additionally, manufacturing industries such as plastics, rubber, and coatings continue to expand their utilization of barite as a filler material, benefiting from its density and chemical inertness. Collectively, these end-users illustrate a transition in the market where traditional dominance by the energy sector is complemented by rapid expansion in healthcare and construction, broadening the strategic importance of barite across global industries.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.9% between 2025 and 2032.

Asia-Pacific leads due to its extensive oil and gas exploration activities, coupled with high consumption in industrial filler applications such as plastics, rubber, and coatings. China, India, and Japan dominate production and usage, supported by significant infrastructure projects and investments in modern beneficiation facilities. North America’s rapid growth is driven by shale oilfield development and adoption of high-density barite for drilling fluids. Europe, South America, and the Middle East & Africa are also contributing to regional diversity in demand, with rising industrial applications and construction projects further shaping the Barite Market landscape globally.

North America accounted for approximately 28% of the Barite Market volume in 2024, reflecting strong demand from the shale oil and gas sector. Key industries driving this demand include exploration and production companies, industrial manufacturing sectors, and specialized construction firms. Regulatory support such as streamlined mining permits and environmental compliance incentives has encouraged domestic production, while digital transformation in mining—such as AI-based process optimization and automated quality monitoring—has enhanced operational efficiency. Technological advancements including micronized barite production and improved grinding equipment have further strengthened North America’s market position, enabling manufacturers to meet stringent industrial and energy sector requirements.

Europe contributed nearly 18% to the Barite Market in 2024, with Germany, the UK, and France serving as the primary consumers. The region’s demand is largely fueled by industrial fillers, paints and coatings, and specialized chemical applications. Regulatory bodies across Europe emphasize sustainability in mining operations, mandating emission reductions and land reclamation practices. Adoption of emerging technologies such as precision milling, micronization, and digital quality control systems has enhanced product performance and compliance with environmental standards. Europe continues to balance demand with environmental responsibility, positioning itself as a key market for high-purity and specialty barite applications.

Asia-Pacific held the largest market volume at 42% in 2024, driven by major consuming countries including China, India, and Japan. This region’s growth is supported by expansive infrastructure development, increased oil and gas exploration, and significant manufacturing activities in plastics, rubber, and coatings. Local production capacities are continually expanding with investments in modern beneficiation plants and automated quality monitoring systems. Technological innovation hubs in China and Japan focus on high-density and micronized barite grades, facilitating broader industrial and medical applications. Regional infrastructure modernization and government initiatives further strengthen the Barite Market’s position in Asia-Pacific.

South America contributed roughly 7% of the global Barite Market in 2024, with Brazil and Argentina being the leading countries. Industrial growth, mining infrastructure development, and expanding energy projects are driving barite consumption in this region. Government incentives for mineral exploration and trade agreements supporting export of raw and processed barite have enhanced supply chain efficiency. South American manufacturers are adopting modern processing techniques and micronization equipment to cater to both domestic and international demand. The region’s market is gradually diversifying beyond oilfield applications into construction, medical, and industrial filler uses.

The Middle East & Africa accounted for about 5% of the global Barite Market in 2024, with UAE and South Africa being the major contributors. Regional demand is primarily driven by oil and gas drilling operations, alongside growing construction and infrastructure projects. Technological modernization includes adoption of advanced crushing, milling, and automated quality inspection systems. Local regulations and trade partnerships facilitate raw material imports and exports, ensuring steady supply. The Barite Market in this region is characterized by strategic investments in energy sector applications while exploring opportunities in industrial fillers and specialty construction materials.

China – 30% Market Share

High production capacity and advanced beneficiation facilities support extensive oilfield and industrial applications.

United States – 20% Market Share

Strong end-user demand from shale oil exploration and technological adoption in processing and quality control.

The Barite Market is characterized by a highly competitive environment, with over 50 active global and regional competitors engaging in production, processing, and distribution activities. Market leaders focus on strategic initiatives such as partnerships with drilling and industrial firms, new product launches targeting high-purity and micronized barite, and mergers to strengthen supply chains. Innovation is a key differentiator, with companies investing in automated grinding, quality monitoring, and beneficiation technologies to improve consistency and product performance. Regional players are increasingly adopting digital solutions, including AI-driven process optimization and predictive maintenance, enhancing operational efficiency. Strategic collaborations with oilfield service providers and industrial end-users are shaping competitive positioning, while investments in environmentally sustainable mining and processing practices are gaining prominence. This competitive landscape drives continuous improvements in product quality, processing efficiency, and delivery timelines, creating a dynamic market where technological and operational advancements are critical to maintaining leadership.

Halliburton

Schlumberger Limited

Shaanxi Coal and Chemical Industry Group

Mineral Technologies Inc.

OM Holdings Limited

FGS Minerals Ltd.

Baroid Industrial Drilling Products

King Chemical Corp.

Severn Drilling & Supply Ltd.

Technological advancements are shaping the Barite Market by enhancing extraction, processing, and application capabilities. Automated beneficiation and grinding systems have significantly improved particle size consistency and purity levels, particularly for drilling and industrial applications. Micronization technology enables finer particle production, which is essential for high-performance fillers in plastics, coatings, and rubber industries. Digital quality control systems, including laser-based particle analysis and real-time monitoring, ensure compliance with industrial specifications and reduce waste. In oilfield applications, AI-driven process optimization supports accurate mixing of drilling mud formulations, improving wellbore stability and reducing operational risks. Sustainable processing technologies, such as water recycling and energy-efficient milling, are being implemented to minimize environmental impact. Additionally, research into barite-based composite materials for radiation shielding and medical applications is gaining traction, reflecting the material’s evolving technological significance across diverse sectors. These innovations collectively enhance product performance, expand application potential, and strengthen market competitiveness.

In March 2023, Halliburton launched a high-density barite variant designed for ultra-deepwater drilling applications, featuring enhanced particle uniformity and improved rheological performance.

In July 2023, Shaanxi Coal and Chemical Industry Group expanded its micronized barite production capacity by 15,000 tons per year to support growing demand in plastics and coatings applications.

In February 2024, OM Holdings Limited implemented an automated quality monitoring system across its beneficiation plants, reducing production inconsistencies and improving compliance with industrial specifications.

In November 2024, FGS Minerals Ltd. introduced a low-dust barite grade for construction and industrial applications, enhancing workplace safety and handling efficiency.

The Barite Market Report provides a comprehensive analysis of global and regional market trends, production capacities, consumption patterns, and technological innovations. It covers all key segments, including type—drilling grade, chemical grade, and filler grade—applications in oilfield, industrial fillers, coatings, plastics, rubber, and radiation shielding, and end-user industries such as energy, construction, healthcare, and manufacturing. The report examines market distribution across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting production hubs, demand centers, and infrastructure development. It also addresses technological advancements, such as automated beneficiation, micronization, and AI-enabled process optimization, as well as sustainable practices in mining and processing. Emerging niche applications, including medical imaging and radiation shielding, are explored, alongside competitive strategies and supply chain dynamics. This report offers a holistic view for decision-makers, emphasizing strategic insights, operational efficiency, and innovation opportunities across the Barite Market landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 163.0 Million |

| Market Revenue (2032) | USD 221.4 Million |

| CAGR (2025–2032) | 3.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Halliburton, Schlumberger Limited, Shaanxi Coal and Chemical Industry Group, Mineral Technologies Inc., OM Holdings Limited, FGS Minerals Ltd., Baroid Industrial Drilling Products, King Chemical Corp., Severn Drilling & Supply Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |