Reports

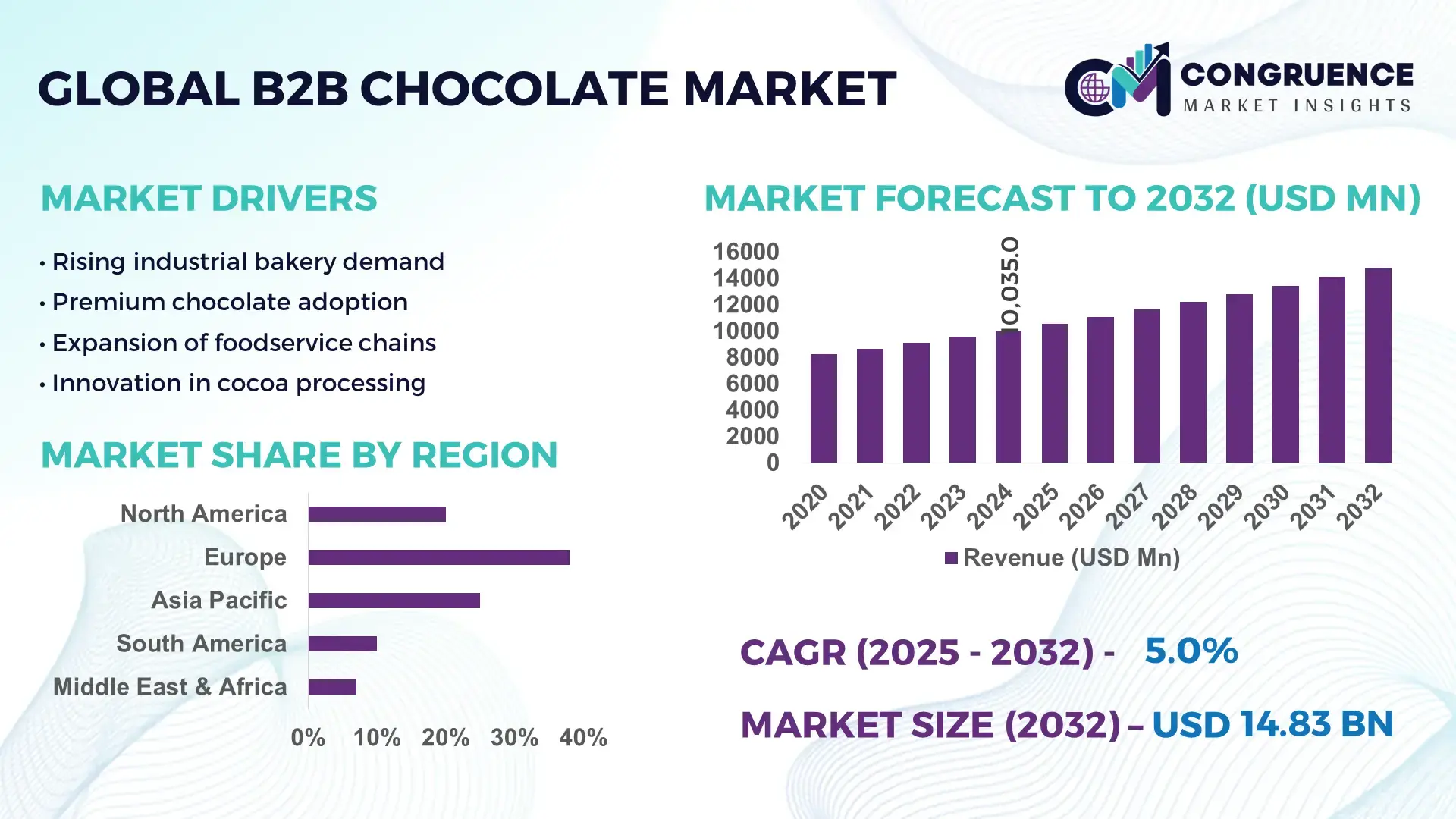

The Global B2B Chocolate Market was valued at USD 10034.95 Million in 2024 and is anticipated to reach a value of USD 14826.19 Million by 2032 expanding at a CAGR of 5.0% between 2025 and 2032. This growth is primarily driven by rising industrial demand from confectionery, bakery, dairy, and foodservice manufacturers seeking consistent quality, scalable supply, and customized chocolate formulations.

Germany represents the dominant country in the global B2B chocolate marketplace, supported by advanced industrial-scale production and strong downstream demand. The country processes over 700,000 metric tons of cocoa annually and hosts more than 1,600 confectionery manufacturing facilities. Capital investment in automated chocolate processing and tempering lines exceeds USD 1.2 billion cumulatively across major producers. Industrial chocolate in Germany is extensively applied across confectionery, baked goods, ice cream, and functional foods, with over 65% of output supplied through B2B contracts. Technological adoption includes AI-driven quality inspection, energy-efficient roasting systems, and precision fat-content control, enabling high-volume, specification-driven supply for multinational food manufacturers.

Market Size & Growth: Valued at USD 10034.95 Million in 2024 and projected to reach USD 14826.19 Million by 2032 at a CAGR of 5.0%, driven by expanding industrial confectionery and bakery production.

Top Growth Drivers: Clean-label chocolate adoption at 38%, private-label manufacturing growth at 29%, automation-led processing efficiency improvement at 24%.

Short-Term Forecast: By 2028, manufacturers are expected to achieve 18% reduction in batch variability and 15% improvement in production throughput.

Emerging Technologies: AI-enabled flavor profiling, low-energy continuous tempering systems, and precision cocoa butter replacement technologies.

Regional Leaders: Europe projected at USD 5,900 Million by 2032 with premium industrial chocolate demand, North America at USD 4,100 Million driven by foodservice chains, Asia Pacific at USD 3,400 Million led by bakery expansion.

Consumer/End-User Trends: Large-scale confectionery brands and QSR chains increasingly prefer long-term B2B sourcing contracts with customized formulations.

Pilot or Case Example: In 2024, an automated molding pilot reduced production downtime by 22% in an industrial chocolate facility.

Competitive Landscape: Barry Callebaut holds approximately 28% share, followed by Cargill, Olam Food Ingredients, Fuji Oil, and Blommer Chocolate.

Regulatory & ESG Impact: Cocoa traceability mandates and carbon-reduction targets are accelerating certified and deforestation-free sourcing.

Investment & Funding Patterns: Over USD 2.4 billion invested recently in capacity expansion, sustainable sourcing, and digital manufacturing.

Innovation & Future Outlook: Growth in functional chocolate, sugar-reduction technologies, and integration with smart factory systems is shaping future demand.

The B2B chocolate market serves key industry sectors including confectionery manufacturing contributing approximately 45% of industrial demand, bakery and patisserie at around 25%, dairy and frozen desserts near 15%, and foodservice and beverages accounting for the remainder. Recent innovations include plant-based industrial chocolate, reduced-sugar formulations using alternative sweeteners, and enhanced emulsification techniques improving shelf stability. Regulatory pressure around sustainable cocoa sourcing, coupled with environmental targets to cut processing emissions, is influencing procurement strategies. Regionally, Europe leads in premium and specialty chocolate usage, while Asia Pacific shows strong volume growth driven by urban bakery expansion. Emerging trends point toward customized formulations, digital quality control, and long-term B2B supply partnerships shaping the market’s future trajectory.

The B2B Chocolate Market holds strong strategic relevance within the global food manufacturing ecosystem due to its direct linkage with industrial-scale confectionery, bakery, dairy, and foodservice operations. Enterprise buyers increasingly prioritize reliability, formulation precision, and compliance-ready sourcing, positioning B2B chocolate as a core input for value-added food production. Advanced continuous tempering technology delivers nearly 20% higher throughput efficiency compared to traditional batch tempering standards, enabling manufacturers to meet rising order volumes with lower variability. Europe dominates in production volume due to its dense network of industrial processors, while Asia Pacific leads in adoption, with over 42% of large-scale bakery and confectionery enterprises integrating contract-based B2B chocolate sourcing.

Strategic pathways are increasingly shaped by digitalization and automation. By 2027, AI-enabled quality analytics and predictive maintenance systems are expected to reduce process-related waste by approximately 18% across industrial chocolate facilities. ESG compliance is becoming equally decisive, with firms committing to sustainability metrics such as a 30% reduction in carbon emissions per ton of chocolate processed by 2030 through energy-efficient roasting and renewable power integration. In 2024, Switzerland-based manufacturers achieved a 16% reduction in defect rates through AI-driven viscosity and crystallization control systems. Looking ahead, the B2B Chocolate Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting long-term supply stability while aligning industrial food production with regulatory and environmental expectations.

Industrial food manufacturers require chocolate with precise viscosity, cocoa content, and melting profiles to maintain standardized end products across multiple production sites. More than 60% of multinational confectionery brands now specify customized B2B chocolate formulations for applications such as molded chocolates, coatings, and inclusions. This demand has accelerated investment in automated refining and conching systems capable of maintaining particle size variation below 5 microns. Additionally, foodservice chains and private-label brands are expanding rapidly, increasing bulk procurement volumes. The need for predictable sensory outcomes and regulatory compliance continues to push manufacturers toward specialized B2B suppliers rather than in-house chocolate processing.

Cocoa supply instability remains a significant restraint for the B2B Chocolate Market. Climate variability has contributed to yield fluctuations of up to 20% in key cocoa-producing regions, directly impacting raw material availability. Industrial buyers face challenges in cost planning and formulation stability when cocoa butter and liquor specifications vary across shipments. Compliance with deforestation-free sourcing regulations further limits supplier pools, particularly for high-volume buyers. These constraints increase procurement complexity and require higher inventory buffers, affecting operational efficiency for B2B chocolate processors and their downstream customers.

The growing demand for sustainable, reduced-sugar, and functional food products presents strong opportunities for the B2B Chocolate Market. Industrial customers are increasingly requesting chocolate formulations with alternative sweeteners, higher cocoa solids, and added functional ingredients such as fibers or plant proteins. Over 35% of new product launches in the confectionery sector now involve reformulated chocolate bases. Additionally, certified sustainable cocoa and traceable supply chains enable B2B suppliers to secure long-term contracts with global brands seeking ESG-aligned inputs. These trends support product differentiation and premium positioning within industrial supply frameworks.

The B2B Chocolate Market faces challenges related to escalating compliance and operational costs. Investments in traceability systems, allergen segregation infrastructure, and emissions monitoring increase capital and operating expenditures. Energy-intensive processes such as roasting and grinding are also exposed to electricity and fuel price volatility. For mid-sized B2B suppliers, aligning with evolving food safety and environmental standards while maintaining competitive pricing is increasingly complex. These pressures require continuous efficiency improvements and scale optimization to sustain profitability and long-term competitiveness.

Expansion of Customized Industrial Chocolate Formulations: B2B buyers are increasingly demanding application-specific chocolate tailored for coatings, fillings, inclusions, and enrobing. More than 62% of large confectionery and bakery manufacturers now procure customized fat profiles, cocoa percentages, and viscosity ranges. Customized formulations have reduced line-level defect rates by nearly 14% and improved batch-to-batch consistency by 18%, supporting large-scale, multi-site food production strategies.

Acceleration of Automation and Smart Processing Technologies: Automation adoption across grinding, refining, and tempering stages has increased significantly, with over 48% of industrial chocolate processors deploying AI-enabled monitoring systems. Smart sensors now track crystallization curves in real time, cutting process deviations by approximately 21%. Automated material handling has also lowered manual intervention by 30%, improving throughput reliability and reducing contamination risks in high-volume B2B environments.

Growing Emphasis on Sustainable and Traceable Cocoa Inputs: Sustainability-driven procurement is reshaping supplier selection, with nearly 58% of B2B chocolate contracts now including traceability and ESG-linked performance clauses. Manufacturers using fully traceable cocoa have achieved up to 25% improvement in supply transparency metrics. Energy-efficient roasting technologies are also reducing energy consumption per ton processed by around 17%, aligning production with corporate carbon-reduction commitments.

Rising Demand from Foodservice and Private-Label Channels: Foodservice operators and private-label brands are emerging as high-growth B2B customers, accounting for roughly 34% of bulk chocolate demand. Standardized chocolate bases optimized for scalability have improved production cycle times by 12% for private-label manufacturers. In parallel, portion-controlled and heat-stable chocolate variants are seeing adoption rates exceeding 40% among quick-service restaurant chains, supporting menu consistency across regions.

The B2B Chocolate Market is segmented based on type, application, and end-user, reflecting the diverse functional requirements of industrial buyers. By type, segmentation is driven by cocoa content, fat composition, and functional performance in large-scale processing. Application-based segmentation highlights how industrial chocolate is optimized differently for confectionery, bakery, dairy, and foodservice uses, each requiring distinct melting, viscosity, and stability characteristics. End-user segmentation underscores demand concentration among multinational confectionery manufacturers, private-label producers, and foodservice operators, with procurement decisions shaped by scale, compliance requirements, and formulation consistency. Together, these segments illustrate how the market is structured around performance-driven differentiation rather than consumer branding, enabling suppliers to align production technologies, sustainability practices, and customization capabilities with specific industrial needs.

Industrial couverture chocolate currently accounts for approximately 46% of overall adoption, driven by its high cocoa butter content and superior flow properties, making it the preferred choice for enrobing, molding, and premium confectionery applications. Compound chocolate holds around 28%, favored for cost efficiency and thermal stability in high-volume bakery and foodservice environments. However, single-origin and specialty chocolate types are emerging as the fastest-growing segment, expanding at an estimated CAGR of 7.2%, supported by demand for differentiated flavor profiles and traceable sourcing among premium and private-label manufacturers. Other types, including reduced-sugar, functional, and plant-based industrial chocolates, collectively contribute nearly 26%, serving niche applications such as health-oriented products and alternative dairy formulations.

Confectionery manufacturing represents the leading application segment with nearly 48% share, as molded chocolates, bars, and inclusions require precise crystallization and sensory consistency at scale. Bakery applications account for around 27%, utilizing chocolate for fillings, coatings, and chips that must withstand baking temperatures. Dairy and frozen desserts hold close to 15%, while beverages and other uses collectively represent about 10%. Foodservice and quick-service restaurant applications are the fastest-growing, expanding at an estimated CAGR of 6.8%, driven by standardized dessert menus and centralized sourcing models. Heat-stable and portion-controlled chocolate formats are gaining traction in this segment.

Large confectionery manufacturers dominate end-user adoption with approximately 44% share, supported by their reliance on long-term B2B supply contracts and high-volume procurement. Private-label producers account for about 26%, benefiting from scalable formulations and faster product launch cycles. Foodservice operators represent nearly 18%, while specialty food manufacturers and others contribute the remaining 12%. Among these, private-label manufacturers are the fastest-growing end-user group, expanding at an estimated CAGR of 7.5%, driven by retailer expansion and demand for differentiated yet cost-efficient products. Adoption rates of customized B2B chocolate among private-label producers exceed 60% in developed markets.

Europe accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

Europe’s leadership is supported by over 1,600 industrial chocolate and confectionery processing facilities and annual cocoa processing volumes exceeding 1.2 million metric tons. North America followed with nearly 27% share, driven by large-scale confectionery, bakery, and foodservice operators with centralized procurement models. Asia-Pacific currently represents around 22% of global demand, but rapid urbanization, rising bakery penetration, and industrial food manufacturing expansion are increasing B2B chocolate volumes by double-digit percentages in key economies. South America and the Middle East & Africa together account for approximately 13%, supported by proximity to cocoa production zones, improving processing infrastructure, and growing regional food manufacturing bases.

How is industrial-scale food manufacturing reshaping enterprise chocolate procurement patterns?

The region accounts for approximately 27% of global B2B Chocolate Market demand, supported by high-volume confectionery, bakery, and dairy manufacturing. Key demand originates from packaged food brands, private-label producers, and quick-service restaurant chains, with over 70% of industrial buyers relying on long-term B2B supply contracts. Regulatory frameworks emphasizing food safety, allergen control, and labeling consistency are influencing supplier qualification processes. Digital transformation is evident, with nearly 45% of processors using automated tempering and AI-based quality monitoring systems. Local players such as Barry Callebaut’s North American operations are expanding customized formulation capabilities and sustainable cocoa programs. Consumer behavior shows preference for standardized taste profiles and heat-stable chocolate, supporting large-batch, efficiency-driven procurement models.

Why are compliance-driven procurement strategies shaping industrial chocolate demand?

Europe holds the largest share at about 38%, anchored by Germany, the UK, and France, which together process over 60% of the region’s industrial chocolate volume. Sustainability regulations and traceability requirements are central, with more than 55% of B2B contracts now incorporating certified cocoa and emissions-reduction targets. Emerging technologies such as energy-efficient roasting, digital batch tracking, and predictive maintenance are widely adopted, with automation penetration exceeding 50% in large facilities. Companies like Lindt & Sprüngli and regional processors are investing in low-sugar and specialty industrial chocolate lines. Consumer behavior reflects strong demand for premium, responsibly sourced chocolate, driving specification-focused B2B sourcing.

How is manufacturing scale-up accelerating industrial chocolate consumption?

Asia-Pacific ranks third by current volume at around 22% share but leads in growth momentum. China, India, and Japan together account for over 65% of regional industrial chocolate usage. Manufacturing expansion is notable, with more than 400 new industrial bakery and confectionery plants commissioned over the past five years. Automation adoption is rising, with approximately 35% of processors integrating smart mixing and refining systems. Regional players such as Fuji Oil are expanding specialty fats and compound chocolate production. Consumer behavior shows strong growth in western-style bakery products and ready-to-eat desserts, supporting higher-volume B2B chocolate procurement.

How does proximity to cocoa supply influence industrial chocolate production strategies?

South America contributes roughly 8% of global B2B Chocolate Market demand, led by Brazil and Argentina. Brazil alone processes over 250,000 metric tons of cocoa annually, supporting regional industrial chocolate manufacturing. Infrastructure investments in food processing zones and improved energy access are enhancing production efficiency. Government trade incentives supporting agricultural processing have encouraged domestic value addition. Local processors are increasingly supplying regional bakery and confectionery brands. Consumer behavior is influenced by localized flavor preferences and cost-sensitive formulations, driving demand for compound and blended industrial chocolates.

What role does industrial diversification play in shaping chocolate demand?

The region accounts for approximately 5% of global demand, with the UAE and South Africa as key growth countries. Demand is linked to expanding food processing hubs, tourism-driven foodservice, and retail bakery growth. Technological modernization includes adoption of imported automated tempering and molding systems, improving consistency and output. Trade partnerships and food security initiatives support ingredient imports and processing investments. Regional players are focusing on halal-compliant and heat-resistant chocolate formulations. Consumer behavior emphasizes shelf stability and affordability, shaping B2B chocolate specifications.

Germany – 18% market share; dominance driven by high industrial processing capacity, advanced automation, and strong confectionery manufacturing base.

United States – 15% market share; leadership supported by large-scale foodservice chains, private-label production, and centralized B2B procurement models.

The B2B Chocolate market is moderately consolidated, characterized by the presence of approximately 40–50 active global and regional manufacturers supplying industrial-scale chocolate to confectionery, bakery, dairy, and foodservice clients. The top five companies collectively account for nearly 62% of total market participation, reflecting strong concentration at the upper tier alongside a long tail of regional specialists. Market leaders maintain differentiated positioning through large-scale processing capacity exceeding 1 million metric tons annually, vertically integrated cocoa sourcing, and advanced formulation capabilities. Competitive strategies increasingly focus on long-term supply agreements, customized industrial chocolate solutions, and sustainability-linked contracts, with over 55% of large buyers preferring multi-year procurement partnerships. Innovation intensity is high, as nearly 48% of leading players have introduced reduced-sugar, plant-based, or specialty fat formulations within the last three years. Strategic initiatives include capacity expansions of 10–20% at key processing hubs, partnerships with foodservice chains, and digital investments such as AI-driven quality control systems that reduce defect rates by over 15%. Mergers and acquisitions activity remains selective, primarily aimed at geographic expansion and access to specialty chocolate technologies, reinforcing competitive barriers for smaller entrants.

Barry Callebaut

Cargill

Olam Food Ingredients

Fuji Oil Holdings

Lindt & Sprüngli

Blommer Chocolate Company

Puratos Group

JB Cocoa

Meiji Holdings

Guan Chong Berhad

Technology adoption in the B2B Chocolate Market is transitioning from labor-intensive batch processing toward integrated, data-driven manufacturing systems designed to improve consistency, traceability, and operational efficiency. Continuous tempering systems with inline viscosity and temperature controls are increasingly deployed, enabling up to 20% higher throughput stability and reducing batch-level deviations. These systems support uniform crystallization profiles across large production volumes, which is critical for industrial confectionery and bakery applications. Artificial intelligence and machine learning are gaining traction across quality assurance and maintenance operations. Industrial chocolate manufacturers are implementing AI-enabled vision systems and sensor analytics to monitor particle size distribution, flow behavior, and surface defects in real time. These technologies have demonstrated reductions in defect rates ranging between 15% and 25%, while predictive maintenance platforms are helping reduce unplanned equipment downtime by nearly 18% through early fault detection and optimized servicing schedules.

Energy efficiency technologies are also reshaping cocoa roasting and processing stages. Modern low-temperature roasting profiles, combined with heat recovery systems, are lowering energy consumption per kilogram of cocoa processed. Optimized thermal management has achieved energy-use reductions of approximately 12% to 17% in high-capacity facilities, while also preserving volatile flavor compounds important for premium industrial chocolate formulations.

Material and formulation technologies represent another key area of innovation. Cocoa butter equivalents, alternative fat blends, and advanced emulsification systems are increasingly used to improve thermal stability, shelf life, and cost predictability. These formulations are particularly valuable for foodservice and bakery applications operating in warm climates. Additionally, modular production lines, robotics-assisted depositing systems, and limited pilot use of 3D food printing are enabling faster customization, reduced labor dependency, and scalable plant expansions. Collectively, these technologies are strengthening production resilience, compliance readiness, and long-term competitiveness in the B2B Chocolate Market.

The B2B Chocolate Market Report encompasses a comprehensive examination of industrial chocolate supply chains, product types, application areas, end‑user segments, and regional dynamics. It delineates product segmentation based on chocolate formulations, including industrial couverture, compound chocolate, specialty functional types, and niche variations such as heat‑stable or plant‑based industrial grades tailored for large‑scale confectionery, bakery, dairy, and foodservice manufacturing. The report analyzes application usage patterns, detailing how manufacturers specify chocolate properties such as viscosity, cocoa content, and melting profiles to meet the functional requirements of enrobing, molding, inclusions, coatings, and baking applications.

Geographically, the scope covers major regions including Europe, North America, Asia‑Pacific, South America, and Middle East & Africa, with insight into regional consumption volumes, infrastructure trends, regulatory environments, and adoption behaviors. It further explores technology influences such as automation, AI‑driven quality systems, and advanced formulation engineering that shape production efficiency and quality consistency at industrial scale.

Industry focus areas include supply chain traceability, sustainability compliance frameworks such as traceable cocoa sourcing, and ESG‑linked procurement models critical for industrial buyers navigating regulatory pressures. The report also highlights emerging or niche segments such as reduced‑sugar industrial chocolate, functional ingredient‑enhanced chocolate, and programmable formulation platforms for customized industrial requirements. End‑user insights report on procurement patterns of multinational confectionery brands, private‑label producers, and foodservice operators, while benchmarking competitive strategies, innovation trends, and partnership activities that define the evolving B2B chocolate landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 10034.95 Million |

|

Market Revenue in 2032 |

USD 14826.19 Million |

|

CAGR (2025 - 2032) |

5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Barry Callebaut, Cargill, Olam Food Ingredients, Fuji Oil Holdings, Lindt & Sprüngli, Blommer Chocolate Company, Puratos Group, JB Cocoa, Meiji Holdings, Guan Chong Berhad |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |