Reports

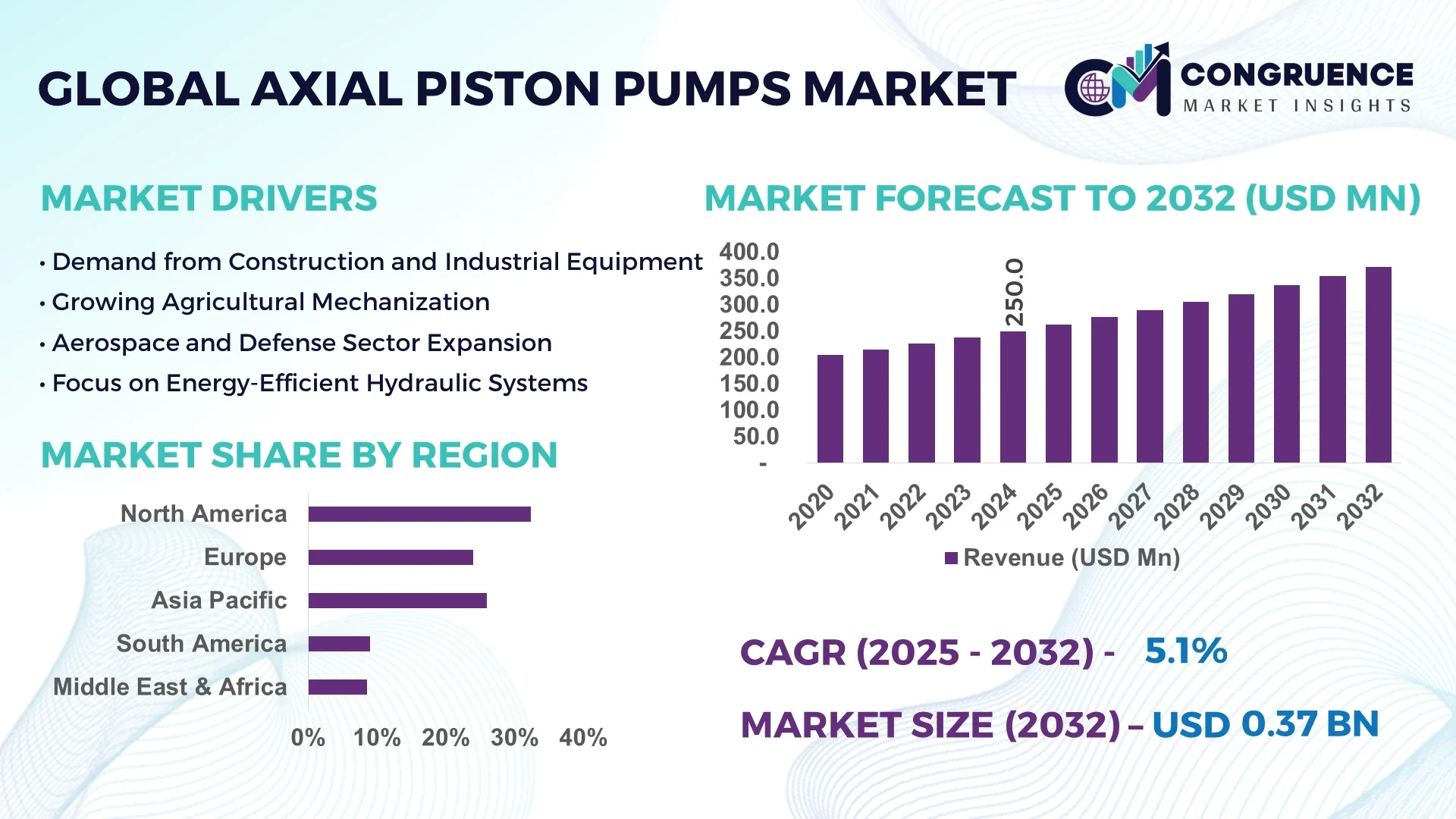

The Global Axial Piston Pumps Market was valued at USD 250 Million in 2024 and is anticipated to reach a value of USD 372.2 Million by 2032 expanding at a CAGR of 5.1% between 2025 and 2032.

The United States leads the Axial Piston Pumps Market with extensive manufacturing capabilities across aerospace, automotive, and industrial automation sectors. The country houses several advanced production facilities with high-precision CNC machining centers and automated quality control systems. Federal investments in hydraulic system innovation and R&D grants have further strengthened its leadership in advanced piston pump technologies for heavy-duty and high-pressure applications.

The Axial Piston Pumps Market plays a vital role across multiple sectors, including construction equipment, aerospace, marine propulsion, agricultural machinery, and industrial manufacturing. Construction and mining applications contribute a significant portion of market demand due to their reliance on high-pressure hydraulic systems for operational efficiency. Recent innovations include the use of lightweight materials, energy-efficient designs, and electronically controlled displacement adjustments. Regulatory pressure to reduce hydraulic fluid leakage and increase equipment sustainability has accelerated the adoption of eco-friendly designs. Regional consumption trends reveal increasing demand in Asia-Pacific driven by infrastructure growth and industrial expansion, while North America and Europe lead in innovation and OEM integration. Emerging trends such as the integration of smart sensors for real-time performance diagnostics, and the shift toward electrification in off-highway machinery, are expected to further transform the competitive landscape.

Artificial intelligence is driving substantial transformation in the Axial Piston Pumps Market by improving operational efficiency, predictive maintenance, and real-time system optimization. AI algorithms are increasingly being embedded within hydraulic control systems to analyze pressure differentials, fluid dynamics, and temperature fluctuations. These systems enable dynamic load adjustments, reduce energy consumption, and prevent unplanned downtime by forecasting component fatigue and wear in advance.

In high-performance environments like aviation hydraulics and offshore drilling, AI-enhanced axial piston pumps offer precision fluid control with adaptive responses to workload variations. This enhances equipment longevity and minimizes the need for manual calibration. AI also supports closed-loop control systems, enabling integration with IoT platforms and SCADA interfaces that track pump health remotely. As a result, end-users benefit from reduced maintenance costs and increased uptime.

Manufacturers are integrating AI to model flow simulations and improve pump design using generative engineering, shortening R&D cycles. These advances are especially valuable in custom engineering scenarios where every operational detail matters. Additionally, AI-driven supply chain analytics are helping companies optimize production and inventory levels, addressing volatility in global demand.

“In January 2024, a major hydraulic systems provider introduced an AI-powered axial piston pump controller that achieved a 17% increase in energy efficiency and extended maintenance intervals by 22% in industrial test environments.”

The Axial Piston Pumps Market is experiencing steady growth fueled by demand across diverse sectors requiring high-pressure hydraulic systems. Industries such as construction, mining, marine, and aerospace rely heavily on axial piston pumps due to their precision, durability, and compact design. Advancements in hydraulic fluid formulations and pump architecture are enhancing performance under extreme conditions. Increasing automation in industrial operations and the shift toward electrified heavy machinery are also influencing pump specifications and integration. Furthermore, digital monitoring and real-time diagnostics are elevating operational transparency and reducing maintenance interventions. These trends are reshaping the competitive dynamics and innovation priorities in the market.

Global infrastructure development, particularly in emerging economies, is significantly boosting demand for axial piston pumps. These pumps are essential components in heavy-duty equipment such as excavators, concrete pumps, and cranes. With governments investing in transportation networks, energy projects, and urban development, there is a consistent demand for hydraulics capable of handling high pressure and variable loads. Axial piston pumps offer compactness, higher flow rates, and flexibility—making them ideal for these applications. In India alone, recent infrastructure budgets have allocated billions toward highway and smart city development, leading to a rise in hydraulic equipment deployment, thereby strengthening the axial piston pumps market.

Despite long-term cost advantages, the high upfront costs and complexity of axial piston pumps present a barrier to wider adoption, particularly in cost-sensitive markets. These pumps require precision manufacturing and advanced control systems, which add to their price compared to simpler alternatives. Additionally, they demand skilled technicians for installation, calibration, and servicing. Smaller enterprises and emerging market users often opt for less sophisticated hydraulic solutions due to affordability and ease of use. This limits penetration, especially in regions lacking access to modern manufacturing infrastructure or trained personnel.

The integration of smart sensors into axial piston pump systems offers a major growth opportunity by transforming traditional maintenance practices. These sensors monitor key parameters such as pressure, temperature, fluid quality, and vibration. When linked with AI-powered platforms, they enable predictive maintenance, reducing unplanned downtime and improving system longevity. For fleet operators and OEMs, this leads to better equipment utilization and lifecycle cost management. Demand is growing for “smart pumps” in manufacturing and mobile equipment sectors, especially in Europe and North America, where remote diagnostics and IIoT compatibility are becoming standard requirements.

Tightening environmental regulations and fluid leakage standards are posing challenges to manufacturers and users of axial piston pumps. Hydraulic systems face scrutiny over oil leakage, emissions from fluid degradation, and disposal requirements. Meeting compliance mandates—such as those related to EU REACH or RoHS directives—requires redesigning components, adopting sustainable materials, and investing in fluid management systems. These changes raise production costs and require significant R&D investment. Moreover, traditional hydraulic systems are increasingly being compared against electric actuation solutions, adding competitive pressure on maintaining environmental viability.

Electrification of Hydraulic Equipment: Electrification of mobile hydraulic systems is accelerating, especially in construction and agriculture. OEMs are integrating electro-hydraulic axial piston pumps in hybrid and fully electric machinery to balance performance and sustainability. This transition is enabling higher energy efficiency, noise reduction, and better compatibility with onboard electronic controls.

Customized Compact Designs for Mobile Applications: The demand for compact, lightweight axial piston pumps is rising for use in aerial work platforms, forklifts, and portable hydraulic tools. These customized designs optimize power-to-weight ratios and allow integration into limited spaces. Manufacturers are developing modular configurations to meet specific load and space requirements in OEM applications.

Adoption of Biodegradable Hydraulic Fluids: Environmental regulations are driving the shift toward compatible pump systems for use with biodegradable and low-toxicity hydraulic fluids. Axial piston pumps are being redesigned with enhanced seals and corrosion-resistant materials to ensure compatibility with new eco-friendly formulations used in forestry, marine, and municipal sectors.

AI-Based Control Algorithms for Real-Time Optimization: AI-enabled control systems are now embedded into high-end axial piston pumps to manage variable displacement automatically. These systems continuously adjust pump parameters based on workload, improving performance and reducing power consumption. As these algorithms mature, their use is expanding from aerospace to industrial automation.

The Global Axial Piston Pumps Market is segmented based on type, application, and end-user, each playing a crucial role in shaping product demand and innovation. The type segment includes various pump configurations that meet specific operational needs in mobile and stationary hydraulic systems. In terms of applications, the market covers critical industrial sectors such as construction, mining, aerospace, marine, and power generation—each with unique fluid control requirements. End-user segments highlight OEMs, aftermarket players, and service providers with different purchase motivations and value expectations. As industrial automation advances and demand for energy-efficient systems grows, segmentation insights reveal the rising importance of tailored solutions, compact integration, and real-time system diagnostics. The diversity across segments reflects strong competition and a constant need for innovation to meet stringent performance, environmental, and cost-efficiency benchmarks.

The axial piston pumps market encompasses multiple product types, each suited for distinct performance demands. Variable displacement axial piston pumps dominate the market due to their flexibility in adapting flow rates to system pressure, making them ideal for energy-saving applications and advanced load-sensing systems. Their broad adoption in construction equipment, mobile hydraulics, and industrial automation highlights their versatility.

Fixed displacement pumps are the fastest-growing segment, particularly in applications where consistent output is essential. Their simplicity and cost-efficiency make them highly preferred in manufacturing equipment and smaller mobile systems, especially in emerging economies where system complexity needs to be minimized.

Other niche types include swashplate and bent-axis configurations, each with specialized roles. Swashplate designs are known for compactness and are widely used in medium-duty systems, while bent-axis pumps are favored in heavy-duty, high-pressure environments like marine propulsion and large industrial presses. This product diversity allows manufacturers to target multiple industries with application-specific offerings.

Axial piston pumps are widely used across a range of applications, each contributing uniquely to market growth. The construction and mining sector leads in terms of demand, driven by the need for powerful hydraulic systems in excavators, loaders, and heavy-duty earth-moving equipment. These applications require high flow rates and pressure stability, which axial piston pumps are well-equipped to deliver.

The industrial machinery segment is witnessing the fastest growth, driven by rising automation, factory modernization, and smart manufacturing initiatives. These pumps play a vital role in fluid power transmission in presses, injection molding machines, and robotic equipment.

Other significant application areas include aerospace, where compact, lightweight, and high-precision pumps are critical for flight control and actuation systems, and marine, where axial piston pumps are used in steering, winching, and propulsion systems. The increasing emphasis on energy-efficient and electronically controlled hydraulic systems is further broadening the application scope, particularly in advanced and regulated industries.

In terms of end-user segmentation, original equipment manufacturers (OEMs) represent the largest share of the axial piston pumps market. These players integrate pumps into new machinery and vehicles across construction, agricultural, and industrial platforms, driving consistent bulk demand. OEMs focus on performance, compactness, and energy efficiency to meet customer expectations and regulatory standards.

The aftermarket and maintenance, repair, and overhaul (MRO) segment is expanding rapidly, supported by the need for replacement pumps in aging equipment fleets. Increasing industrial uptime demands and the availability of custom-fit replacements are supporting this segment’s momentum, especially in heavy industry and transportation.

Fleet operators and service contractors also represent a notable end-user group, particularly in logistics, marine, and mining sectors, where hydraulic system reliability is mission-critical. These users prioritize smart pumps with diagnostic features and easy serviceability. Collectively, the end-user landscape reflects a transition toward smarter, connected, and performance-optimized fluid power systems.

North America accounted for the largest market share at 32.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America’s dominance is largely driven by high adoption across industrial, aerospace, and construction sectors, along with strong OEM presence and advanced technological infrastructure. Meanwhile, Asia-Pacific is witnessing robust growth, primarily due to accelerating industrialization, increasing investment in manufacturing and infrastructure, and expanding construction activities in major economies like China and India. Europe remains a critical contributor, particularly in precision engineering and sustainability innovation, while other regions are seeing incremental demand due to modernization initiatives in key industries like oil & gas, energy, and transport.

North America held a 32.4% share of the global Axial Piston Pumps Market in 2024, anchored by its advanced manufacturing ecosystem and widespread usage across automotive, aerospace, and energy sectors. The United States remains the largest contributor due to its high demand for precision fluid power systems in defense and construction. The region benefits from strong government initiatives promoting digital transformation and energy-efficient equipment. Additionally, regulatory bodies have encouraged modernization in hydraulic systems to reduce energy waste. Advanced sensor integration, predictive analytics, and AI-enabled control in axial piston pumps are now commonly adopted by OEMs and industrial operators across the U.S. and Canada.

Europe continues to be a leading region in the Axial Piston Pumps Market, holding approximately 27.8% market share in 2024. Countries such as Germany, France, and the United Kingdom dominate due to their strong base in industrial machinery and automotive manufacturing. The EU’s emphasis on environmental sustainability and machinery efficiency has driven widespread adoption of energy-efficient hydraulic components. Regulatory frameworks such as REACH and eco-design directives are shaping product innovation. European manufacturers are actively integrating axial piston pumps with digital control systems and are investing in sustainable materials and compact design innovations to meet future regulatory thresholds and green industry goals.

Asia-Pacific is emerging as the fastest-growing regional market for axial piston pumps, supported by rapid industrialization and increasing infrastructure investment. In 2024, China, India, and Japan were among the top consumers of axial piston pumps. China leads in manufacturing volume, while India’s construction boom and Japan’s automation advancements further expand regional demand. The surge in smart factories and large-scale industrial machinery installations across the region has elevated the need for compact, durable, and high-pressure fluid power systems. Innovation hubs in countries like South Korea and Singapore are also contributing to regional advancements in pump design and smart integration.

South America's Axial Piston Pumps Market is gaining traction, led by Brazil and Argentina, which together account for the majority of regional demand. The region contributed 6.5% to global market volume in 2024. Government-backed infrastructure projects, energy extraction, and agricultural modernization are increasing the use of high-capacity hydraulic systems. Brazil’s expanding mining and hydroelectric industries, combined with Argentina’s focus on mechanized farming, have created pockets of high demand for axial piston pumps. Several countries are offering tax incentives to modernize industrial equipment, attracting OEM and aftermarket interest in upgrading to more reliable and efficient pump systems.

The Middle East & Africa region accounted for 5.1% of the global axial piston pumps market in 2024, with growing demand from oil & gas, infrastructure, and defense industries. The UAE, Saudi Arabia, and South Africa are leading countries driving regional demand. Investment in smart infrastructure and renewable energy projects is increasing the use of advanced hydraulic systems. In oil-rich nations, axial piston pumps are critical for high-pressure fluid systems in drilling and extraction. Meanwhile, modernization programs across utilities and construction sectors, particularly in North Africa and the Gulf Cooperation Council countries, are driving adoption of new-generation axial piston pumps that offer greater efficiency and lower maintenance.

United States – 24.6% Market Share

High production capacity and extensive use in aerospace, defense, and industrial machinery drive the U.S. dominance in the Axial Piston Pumps Market.

China – 21.3% Market Share

Strong end-user demand in manufacturing and infrastructure sectors, supported by large-scale production and machinery exports, secures China’s leading market position.

The Axial Piston Pumps Market is characterized by intense competition with over 35 globally active manufacturers, including both established multinational brands and regional specialists. Market players are strategically positioning themselves through innovation, digital transformation, and customized product offerings to cater to application-specific requirements across sectors like construction, industrial automation, marine, and aerospace.

Leading companies are actively investing in R&D to develop compact, energy-efficient, and smart axial piston pumps integrated with IoT and predictive diagnostics. Several firms have introduced models compatible with Industry 4.0 systems, enabling real-time monitoring and remote fault detection. Key strategic moves include product portfolio expansion, joint ventures, and localization of production facilities to meet regional demand more efficiently. The competitive environment is further shaped by merger and acquisition activities targeting technological enhancement and geographical footprint expansion. As environmental compliance becomes more stringent, manufacturers focusing on low-emission, high-efficiency pump systems are gaining a significant edge in the global marketplace.

Bosch Rexroth AG

Danfoss Power Solutions

Kawasaki Heavy Industries, Ltd.

Parker Hannifin Corporation

Eaton Corporation

HAWE Hydraulik SE

Bucher Hydraulics GmbH

Yuken Kogyo Co., Ltd.

Linde Hydraulics GmbH & Co. KG

HYDAC International GmbH

Technological advancement in the Axial Piston Pumps Market is centered around efficiency optimization, digital integration, and application-specific adaptability. One of the most notable innovations is the integration of electronic pressure control and on-board diagnostics that enable real-time feedback, facilitating condition-based maintenance and reducing unplanned downtime. These features are particularly valuable in mission-critical sectors such as aerospace, mining, and marine.

Manufacturers are increasingly adopting electro-hydrostatic actuators (EHAs), which combine axial piston pumps with compact motor controllers, eliminating the need for centralized hydraulic systems. This advancement is improving system energy efficiency by up to 30%, especially in mobile machinery and aerospace applications.

Additionally, noise-reduction technologies such as helical gear design, hybrid swashplates, and fluid vibration dampening systems are being integrated into newer models. These innovations not only improve performance but also comply with stringent industrial noise regulations.

Smart axial piston pumps with built-in sensors and wireless data transmission capabilities are now being used to optimize load cycles, monitor temperature and pressure, and ensure precise fluid control. With the growing adoption of Industry 4.0 standards, manufacturers are embedding pumps into digital ecosystems, enabling centralized analytics, remote fault detection, and automated calibration. These advancements are reshaping operational benchmarks and redefining customer expectations in industrial fluid power systems.

In March 2024, Bosch Rexroth unveiled a new range of axial piston pumps with integrated sensor modules that support wireless data transmission, enabling predictive maintenance and reducing hydraulic system failures by over 20% in field trials.

In November 2023, Danfoss Power Solutions expanded its digital displacement pump production facility in Nordborg, Denmark, to meet rising demand for energy-efficient axial piston pumps in mobile hydraulics and construction equipment.

In January 2024, Kawasaki Heavy Industries launched a high-pressure bent-axis axial piston pump for marine propulsion systems, offering a 15% improvement in fuel efficiency and significantly lower fluid leakage.

In May 2024, Parker Hannifin introduced its SmartPUMP™ series featuring real-time AI-based control algorithms that automatically adjust displacement according to workload, optimizing performance and reducing energy consumption by 18%.

The Axial Piston Pumps Market Report delivers a comprehensive analysis of the global market landscape by covering a diverse range of segments, including pump types (variable and fixed displacement), applications (construction, industrial, marine, aerospace), and end-user categories (OEMs, MRO, service contractors). The report provides in-depth regional assessments for North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, reflecting distinct growth patterns and industry priorities across different geographies.

The report also evaluates technological shifts impacting the market, including the rise of electro-hydrostatic systems, AI-integrated pumps, and sensor-enabled performance monitoring. It examines the structural evolution of demand across energy-intensive industries and highlights the importance of sustainability, modularity, and automation in shaping product design.

Moreover, the report identifies strategic trends such as digitization, nearshoring of production, and aftermarket expansion. It also includes detailed competitor profiling, recent development tracking, and opportunity analysis for emerging sectors like renewable energy, defense systems, and offshore infrastructure. This comprehensive scope is designed to support industry professionals, strategic planners, and investment analysts in understanding market behavior and forecasting future direction with clarity and confidence.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 250.0 Million |

| Market Revenue (2032) | USD 372.2 Million |

| CAGR (2025–2032) | 5.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bosch Rexroth AG, Danfoss Power Solutions, Kawasaki Heavy Industries, Ltd., Parker Hannifin Corporation, Eaton Corporation, HAWE Hydraulik SE, Bucher Hydraulics GmbH, Yuken Kogyo Co., Ltd., Linde Hydraulics GmbH & Co. KG, HYDAC International GmbH |

| Customization & Pricing | Available on Request (10% Customization is Free) |