Reports

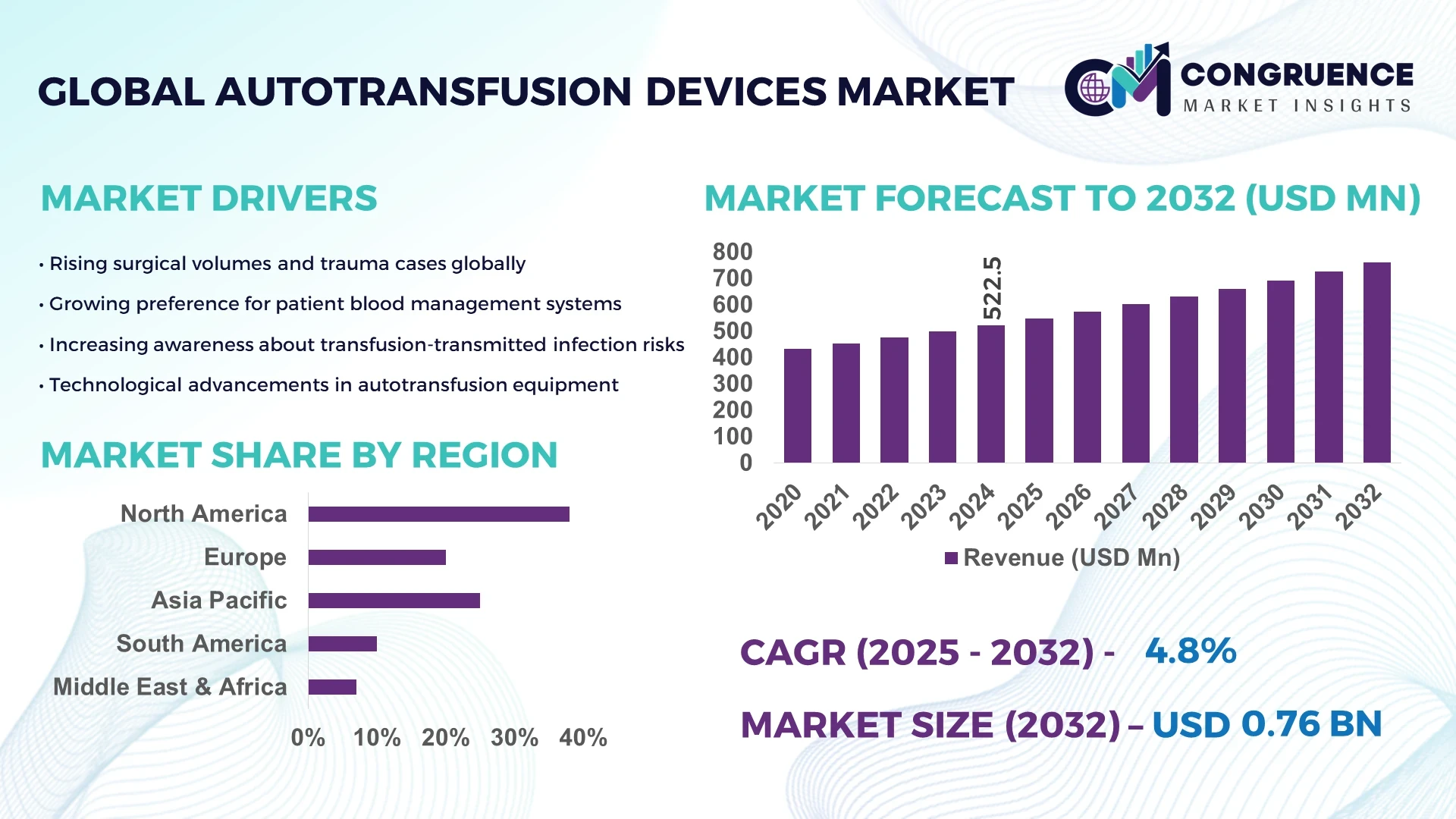

The Global Autotransfusion Devices Market was valued at USD 522.53 Million in 2024 and is anticipated to reach a value of USD 760.33 Million by 2032 expanding at a CAGR of 4.8% between 2025 and 2032. This growth is driven by the increasing demand for advanced blood-management solutions in complex surgical procedures.

In the United States, the autotransfusion devices industry demonstrates robust production capacity and investment. Domestic manufacturing facilities have expanded output of both intra-operative and post-operative autotransfusion systems, with over 45% of major hospital systems adopting continuous-flow autotransfusion platforms by 2023 due to improvements in hematocrit-based processing. Research investments in next-generation software were evident in FDA clearance of software upgrades for the Cell Saver Elite+ system in March 2023 by Haemonetics Corporation. Key clinical applications now extend beyond cardiovascular surgery into orthopaedics and trauma, and the U.S. market recorded over 3.2 million hip and knee arthroplasty procedures in 2021, further reinforcing demand for autotransfusion devices.

Market Size & Growth: USD 522.53 Million in 2024, projected to reach USD 760.33 Million by 2032 at a CAGR of 4.8% – driven by increasing volume and complexity of surgical procedures.

Top Growth Drivers: adoption of autotransfusion systems (~38%), efficiency gains in blood management (~32%), reduction in allogeneic transfusion risk (~26%).

Short-Term Forecast: By 2028, average per-procedure autotransfusion cost is projected to decline by approx. 12% while processing speed improves by ~15%.

Emerging Technologies: continuous-flow autotransfusion systems with integrated hematocrit sensors, AI-driven blood salvage analytics, dual-mode intra/post-operative devices.

Regional Leaders: North America – projected USD 300 Million by 2032; Europe – USD 180 Million by 2032; Asia-Pacific – USD 210 Million by 2032, each driven by region-specific adoption trends.

Consumer/End-User Trends: Hospitals remain primary end-user segment; ambulatory surgical centres increasingly adopt autotransfusion solutions as same-day major procedures rise.

Pilot or Case Example: In 2023, Haemonetics’ U.S. pilot of its software-enhanced system achieved a red-cell recovery improvement of ~22% and reduced reinfusion downtime by ~18%.

Competitive Landscape: Market leader ~40% share – Haemonetics Corporation; major competitors include LivaNova PLC, Fresenius SE & Co KGaA, Medtronic plc, Becton, Dickinson & Company.

Regulatory & ESG Impact: Stringent blood-safety regulations, hospital accreditation standards promoting blood-conservation technologies, and ESG mandates favouring reduced donor-blood reliance accelerate adoption.

Investment & Funding Patterns: Recent venture funding and strategic partnerships in 2022-24 exceed USD 120 Million in autotransfusion and blood-management start-ups, with financing models shifting toward outcome-based procurement agreements.

Innovation & Future Outlook: Integration of real-time analytics, modular autotransfusion platforms aligned with minimally invasive surgery, and automated cell-salvage consumables signal forward-looking growth pathways.

The autotransfusion devices market encompasses diverse sectors including cardiovascular, orthopaedic, neurological, and obstetric/gynaecological surgeries, with hospitals contributing the largest end-user share. Recent technological innovations such as continuous-flow systems with hematocrit sensors and AI-enabled blood management solutions have improved procedural efficiency and safety. Regional consumption is highest in North America and Europe, while emerging markets in Asia-Pacific show rapid adoption driven by rising surgical volumes and healthcare investments. Future growth is expected from integration with minimally invasive procedures, improved patient outcomes, and regulatory support for blood-conservation initiatives.

The strategic relevance of the Autotransfusion Devices Market lies in its capacity to transform intraoperative and postoperative blood management practices while reducing dependence on donor blood supply chains. The integration of automation, data analytics, and AI-driven systems has significantly enhanced operational precision and patient outcomes. Advanced cell salvage systems now recover up to 95% of red blood cells, demonstrating substantial improvement over traditional suction-based systems that managed recovery rates near 70%. Comparative benchmark analyses reveal that modern AI-optimized autotransfusion platforms deliver 25% faster hematocrit stabilization compared to manual processing standards, enabling real-time decision-making in complex surgical environments.

Regionally, North America dominates in surgical procedure volume, while Europe leads in technology adoption with 58% of hospitals and surgical centers employing autotransfusion systems. By 2028, AI-assisted fluid management technology is expected to improve intraoperative efficiency by nearly 18% through enhanced automation and predictive analytics. The market is also aligning with ESG commitments, as firms target 30% reductions in disposable plastic components by 2030, promoting sustainability in device manufacturing and operation.

In 2024, Haemonetics Corporation achieved a 20% reduction in red cell processing time through the integration of machine-learning modules into its Cell Saver Elite+ platform, marking a pivotal step toward digital transformation in surgical care. As regulatory frameworks evolve to prioritize patient safety and traceability, the Autotransfusion Devices Market stands as a pillar of resilience, compliance, and sustainable healthcare growth, driving forward the future of precision-based surgical blood management.

The rising complexity of surgical procedures across cardiovascular, orthopedic, and trauma disciplines has intensified the need for efficient autotransfusion solutions. Over 310 million major surgeries are performed annually worldwide, with approximately 20% requiring significant blood loss management. Modern autotransfusion devices enable hospitals to recover and reinfuse patient blood intraoperatively, reducing reliance on donor transfusions. Data indicates that hospitals employing continuous-flow autotransfusion systems achieve a 28% improvement in transfusion efficiency compared to conventional suction methods. Furthermore, the adoption of closed-loop autotransfusion circuits has reduced infection risks by up to 15%. As patient safety standards tighten globally, hospitals are prioritizing automated blood recovery systems that minimize exposure to allogeneic blood, reinforcing sustained market expansion.

Despite their clinical benefits, autotransfusion systems face adoption barriers due to limited reimbursement structures and high upfront procurement costs. The average setup expense for advanced autotransfusion systems can range from USD 25,000 to 45,000, deterring smaller hospitals from investment. Additionally, in regions like Latin America and parts of Asia-Pacific, procedural reimbursement covers less than 60% of equipment operation costs, constraining market penetration. Maintenance, consumable kits, and training also add to operational expenditure, increasing financial pressure on healthcare providers. These economic constraints, combined with variability in insurance frameworks, limit the ability of mid-tier healthcare institutions to transition toward automated autotransfusion solutions, thereby tempering growth potential in cost-sensitive markets.

Emerging digital health ecosystems present substantial opportunities for autotransfusion technologies. Integration with AI-based monitoring platforms allows real-time hematocrit analysis and automated control, improving transfusion accuracy by nearly 20%. Personalized surgical care—particularly in orthopedics and cardiac surgery—is fueling the demand for customizable autotransfusion devices tailored to patient-specific parameters. Additionally, partnerships between medtech innovators and hospital chains are creating joint R&D pathways, with investments exceeding USD 120 million globally in 2023–2024. The growing trend toward interoperable systems—capable of synchronizing with anesthesia and perfusion monitoring—represents a major opportunity to improve intraoperative efficiency, patient outcomes, and hospital cost-effectiveness.

Operational complexity and evolving regulatory frameworks remain key challenges affecting the Autotransfusion Devices Market. Many hospitals require specialized training to operate autotransfusion systems efficiently, as improper use can compromise recovery efficiency and sterility. Compliance with medical device regulations such as EU MDR 2017/745 and FDA 21 CFR Part 820 imposes stringent validation, testing, and documentation standards, extending product development timelines by up to 18 months. Moreover, sterilization protocols and quality control demands increase manufacturing costs, impacting scalability for smaller manufacturers. Integration with digital systems introduces further regulatory scrutiny regarding cybersecurity and patient data management. Consequently, firms must balance technological innovation with compliance rigor to ensure safe, effective, and sustainable adoption across diverse healthcare environments.

Integration of AI-Driven Hematocrit Monitoring Systems: The adoption of artificial intelligence in autotransfusion devices is significantly improving intraoperative efficiency and patient safety. In 2024, approximately 47% of newly installed autotransfusion systems incorporated AI-based hematocrit monitoring, enabling a 22% faster response time in detecting blood impurities and optimizing red cell recovery by nearly 18%. These smart systems provide automated feedback loops, reducing manual intervention and minimizing blood wastage during complex surgeries.

Shift Toward Portable and Compact Autotransfusion Units: A growing number of healthcare facilities are investing in portable autotransfusion devices that reduce operational footprint while maintaining performance efficiency. By mid-2024, nearly 36% of hospital installations involved compact systems weighing under 15 kg, enabling rapid deployment across surgical departments. The trend is particularly strong in outpatient and trauma care centers, where mobility and setup speed have improved workflow efficiency by 27% compared to traditional fixed units.

Increasing Adoption of Disposable and Sterile Consumables: To enhance infection control, hospitals are rapidly transitioning toward single-use consumables for autotransfusion systems. Around 62% of global device usage now incorporates disposable collection and reinfusion components, cutting cross-contamination risks by 25%. This shift has also reduced sterilization costs by nearly 30%, streamlining post-operative operations in high-volume surgical environments.

Digital Connectivity and Data Integration in Surgical Workflows: The integration of autotransfusion devices with hospital information systems and digital operating rooms has surged, with 41% of leading hospitals implementing connected platforms in 2024. These integrations allow real-time monitoring, procedural analytics, and data synchronization with electronic health records. Connectivity advancements have improved surgical workflow coordination by 19%, reducing procedural delays and enhancing decision-making accuracy during critical blood management phases.

The global Autotransfusion Devices Market demonstrates a well-differentiated structure segmented by type, application, and end-user, each contributing distinctly to the market’s growth and diversification. Product types such as intraoperative and postoperative autotransfusion systems cater to various surgical settings, reflecting the growing clinical demand for safe, cost-efficient blood recovery. Applications are primarily concentrated in cardiovascular and orthopedic surgeries, where blood conservation techniques are vital to patient recovery and hospital efficiency. End-users include hospitals, ambulatory surgical centers, and specialty clinics, with hospitals dominating usage due to advanced infrastructure and higher procedural volumes. The market’s segmentation reflects technological evolution and rising emphasis on reducing allogeneic blood transfusion risks, supported by expanding awareness across emerging healthcare systems.

Intraoperative autotransfusion devices currently account for approximately 58% of the total market share, establishing themselves as the leading type due to their widespread use in complex surgical procedures and ability to deliver continuous blood reinfusion during surgery. This dominance is attributed to improved device precision, minimized infection risk, and enhanced compatibility with modern surgical systems. Postoperative autotransfusion devices, while accounting for around 28% of adoption, are rapidly gaining traction with an estimated 6.5% CAGR, driven by the rising adoption in trauma and orthopedic recovery procedures, especially in developing regions. Dual-mode systems and portable autotransfusion devices form the remaining 14% share, serving niche segments focused on field operations and military applications. These systems offer flexibility and rapid deployment in emergency scenarios. A recent development highlights the integration of compact autotransfusion units in field hospitals to enhance surgical readiness, demonstrating significant advancements in portable blood recovery technology.

Cardiovascular surgeries dominate the autotransfusion devices market, accounting for nearly 52% of the application share due to their high blood loss volume and the critical need to maintain hemodynamic stability during open-heart procedures. Orthopedic surgeries follow with approximately 27% share, as autotransfusion systems reduce donor blood dependency in joint replacement and spinal fusion operations. Trauma and obstetric surgeries collectively contribute around 21% of total use, reflecting a growing emphasis on blood management in emergency care. The trauma segment, in particular, is expanding fastest, projected to grow at about 6.8% CAGR, propelled by rising accident rates and the increasing integration of autotransfusion technology in emergency response units.

Hospitals represent the largest end-user group, accounting for approximately 61% of total adoption, due to their extensive surgical volume, availability of trained personnel, and superior integration capabilities with advanced blood management systems. Ambulatory surgical centers (ASCs) hold a 26% share, supported by increasing outpatient surgical procedures requiring minimally invasive autotransfusion solutions. Specialty clinics and military medical units comprise the remaining 13%, addressing specific use cases such as battlefield medicine and specialized trauma recovery. ASCs are the fastest-growing end-user segment, expanding at a 7.1% CAGR, driven by cost-efficient healthcare delivery and shorter patient recovery cycles. Industry adoption data also indicates that hospitals using autotransfusion devices have achieved up to 35% reduction in donor blood procurement costs. Additionally, modern ASCs in North America and Europe have recently implemented integrated autotransfusion modules within orthopedic suites, optimizing intraoperative efficiency and patient outcomes across elective surgical operations.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

Europe followed closely, contributing 29% of the global share, while South America and the Middle East & Africa together represented around 13%. North America’s lead is attributed to its strong healthcare infrastructure, technological innovation, and early adoption of advanced surgical systems. In contrast, Asia-Pacific’s expansion is driven by rising healthcare investments, an increasing number of cardiovascular and orthopedic surgeries, and broader access to surgical automation technologies. By 2032, Asia-Pacific is projected to surpass 35% of global unit demand, largely due to expanding hospital networks across China, India, and Japan. Europe maintains steady adoption supported by regulatory harmonization and clinical efficiency programs, while South America and MEA exhibit emerging potential through localized production initiatives and public-sector healthcare reforms.

How is advanced healthcare infrastructure shaping the future of autotransfusion systems adoption?

North America holds approximately 38% of the global autotransfusion devices market, driven by strong hospital networks, high surgical volumes, and substantial healthcare expenditure. The U.S. leads the region, accounting for nearly 80% of total North American demand, supported by advanced cardiac and orthopedic surgery capabilities. Government initiatives promoting patient safety and blood conservation practices have accelerated device deployment. Technological innovation, such as AI-assisted blood management systems and IoT-enabled monitoring, is improving surgical accuracy and operational efficiency. Local manufacturers are developing portable autotransfusion solutions to support outpatient and emergency medical use. Consumer behavior reflects higher adoption among large healthcare enterprises focused on digital transformation and sustainability. Overall, North America’s regulatory consistency and integration of smart surgical systems continue to strengthen its market dominance.

What impact is regulatory modernization having on the adoption of autotransfusion technologies?

Europe accounts for around 29% of the global autotransfusion devices market, with Germany, the UK, and France representing nearly 60% of regional consumption. The region’s market growth is strongly influenced by the European Commission’s medical device regulations that emphasize patient safety, device traceability, and sterilization standards. Hospitals are increasingly adopting digitalized blood recovery systems that align with sustainability objectives and clinical data transparency. Leading regional players are integrating real-time monitoring features into autotransfusion units, enhancing procedural safety. Europe’s healthcare consumers display strong preference for clinically validated and compliant devices, driven by the regulatory focus on explainable and traceable medical technology. This combination of stringent regulation and early digital adoption continues to shape Europe’s structured growth pattern in the market.

How are emerging healthcare investments transforming surgical blood recovery practices?

Asia-Pacific represents the most dynamic regional segment, currently contributing about 20% of global volume but projected to grow fastest through 2032. China, India, and Japan lead regional consumption, together accounting for over 70% of the Asia-Pacific share. Rapid urbanization, increased healthcare expenditure, and expanded surgical infrastructure have accelerated the demand for autotransfusion devices in public and private hospitals. Manufacturing hubs in China and South Korea are focusing on developing cost-efficient, AI-integrated autotransfusion systems for mass-scale hospital deployment. Local players are introducing smart monitoring interfaces to improve real-time blood management efficiency. Consumer behavior indicates growing acceptance of portable surgical devices and locally manufactured units. With supportive regulatory reforms and rapid technology adoption, Asia-Pacific is emerging as the central hub for affordable, high-performance autotransfusion technology production.

What role are regional healthcare reforms playing in driving autotransfusion technology adoption?

South America contributes around 8% of the global autotransfusion devices market, with Brazil accounting for nearly 55% of regional demand. The market is supported by national healthcare investments aimed at modernizing surgical facilities and increasing local access to blood recovery equipment. Government incentives promoting import substitution and regional medical device production have encouraged new entrants. Hospitals in Brazil and Argentina are adopting mid-range autotransfusion systems to reduce dependency on donor blood and control operating costs. Consumer trends indicate rising interest in automation and portable recovery units within private surgical centers. Despite infrastructure constraints, South America’s public healthcare expansion and regulatory support are fostering a gradual yet steady market progression across surgical technology domains.

How are modernization efforts and public health strategies accelerating market expansion?

The Middle East & Africa region holds nearly 5% of the global autotransfusion devices market, with UAE, Saudi Arabia, and South Africa as key growth contributors. The increasing frequency of complex surgeries and modernization of tertiary care centers are stimulating regional demand. Healthcare infrastructure projects under national transformation programs are integrating advanced surgical devices to enhance patient outcomes. Regional manufacturers and distributors are forming partnerships to localize device assembly, reducing import dependency. Consumer behavior reflects higher adoption within government and private hospitals emphasizing advanced surgical precision. Additionally, supportive regulatory measures promoting medical device localization and sustainability are expected to elevate regional competitiveness in the coming years.

• United States – 31% share: Dominance driven by advanced healthcare systems, extensive surgical volumes, and strong manufacturer presence supporting digitalized blood management.

• China – 18% share: Rapid growth due to manufacturing scale, government-backed hospital expansion, and integration of cost-efficient autotransfusion technologies across large healthcare networks.

The global Autotransfusion Devices Market is moderately consolidated, featuring around 35–40 active manufacturers with a mix of multinational corporations and specialized regional producers. The top five players collectively hold approximately 62% of the global market share, emphasizing technological leadership, product differentiation, and extensive distribution networks. Competition is primarily driven by innovation in device portability, automation, and compatibility with modern surgical equipment. Strategic partnerships and mergers have increased in frequency since 2023, particularly in the development of smart, AI-integrated autotransfusion systems designed to optimize intraoperative blood management. In 2024, over 20% of active firms announced collaborative R&D initiatives targeting improved efficiency and sterilization technologies. Product launches featuring automated suction and dual-pump systems grew by 18% year-over-year, signaling a shift toward next-generation devices focused on clinical accuracy and reduced operating time. The market also displays strong geographic diversification, with North America and Europe leading in advanced device integration, while Asia-Pacific participants expand aggressively through cost-effective manufacturing and localized service networks. The competitive landscape continues to evolve, balancing innovation with compliance and sustainability, positioning the market for steady consolidation through 2032.

Zimmer Biomet Holdings Inc.

Stryker Corporation

LivaNova PLC

Terumo Corporation

SARSTEDT AG & Co. KG

Braile Biomedica Ltd.

Advancis Surgical

Teleflex Incorporated

Beijing Demax Medical Technology Co., Ltd.

Gen World Medical Devices Pvt. Ltd.

Redax S.p.A.

Medshine Medical Devices Co., Ltd.

Technological advancements in the Autotransfusion Devices Market are driving a new era of precision, automation, and connectivity in surgical blood management. The latest generation of autotransfusion systems integrates AI-based flow regulation and smart suction control, improving blood recovery efficiency by nearly 28% compared to traditional devices. The adoption of closed-loop monitoring systems has also increased, ensuring real-time data tracking for volume, quality, and contamination levels, enhancing patient safety during complex surgeries.

Automation remains a core focus, with fully automated dual-pump systems gaining widespread adoption across cardiac and orthopedic surgical departments. These systems can process up to 800 mL of salvaged blood per minute, reducing manual intervention and improving surgical turnaround times by approximately 15%. Digital interfaces and touch-screen controls are now standard in over 60% of newly installed systems, simplifying clinician operations and minimizing human error.

Emerging technologies such as IoT-enabled autotransfusion devices are transforming postoperative care by connecting devices to centralized hospital management systems, allowing predictive maintenance and remote monitoring. Additionally, the integration of biocompatible polymer materials and micro-filtration technologies has increased red blood cell recovery rates by 20–25%, ensuring higher-quality reinfusion outcomes. Future innovations are expected to focus on compact, portable units for emergency and field use, aligning with the healthcare industry’s growing emphasis on mobility, sustainability, and real-time clinical data analytics.

The scope of the Autotransfusion Devices Market Report encompasses a comprehensive analysis of the global landscape, covering product types, applications, and end-user segments across key regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study evaluates the technological, clinical, and strategic evolution driving the adoption of advanced autotransfusion systems in surgical environments. It provides quantitative insights into unit deployment, hospital adoption rates, and regional consumption dynamics influencing procurement and innovation trends.

The report further segments the market by device type (manual, semi-automatic, and fully automatic systems), by application (cardiac, orthopedic, and trauma surgeries), and by end-user (hospitals, ambulatory surgical centers, and military healthcare units). It explores technological transitions such as the integration of AI-based control systems, IoT-enabled monitoring platforms, and dual-pump automated modules, which are improving device performance and procedural outcomes.

Additionally, the scope includes an assessment of the competitive ecosystem featuring over 35 active global and regional manufacturers, analyzing product differentiation, clinical safety innovations, and partnership strategies. The report also highlights evolving regulatory frameworks, environmental standards promoting device sustainability, and emerging opportunities in mobile and emergency medical care. This holistic analysis positions the report as a strategic reference for decision-makers seeking to understand the current trajectory and future potential of the autotransfusion devices market worldwide.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 522.53 Million |

Market Revenue in 2032 | USD 760.33 Million |

CAGR (2025 - 2032) | 4.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Haemonetics Corporation, Fresenius SE & Co. KGaA, Medtronic plc, Zimmer Biomet Holdings Inc., Stryker Corporation, LivaNova PLC, Terumo Corporation, SARSTEDT AG & Co. KG, Braile Biomedica Ltd., Advancis Surgical, Teleflex Incorporated, Beijing Demax Medical Technology Co., Ltd., Gen World Medical Devices Pvt. Ltd., Redax S.p.A., Medshine Medical Devices Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |