Reports

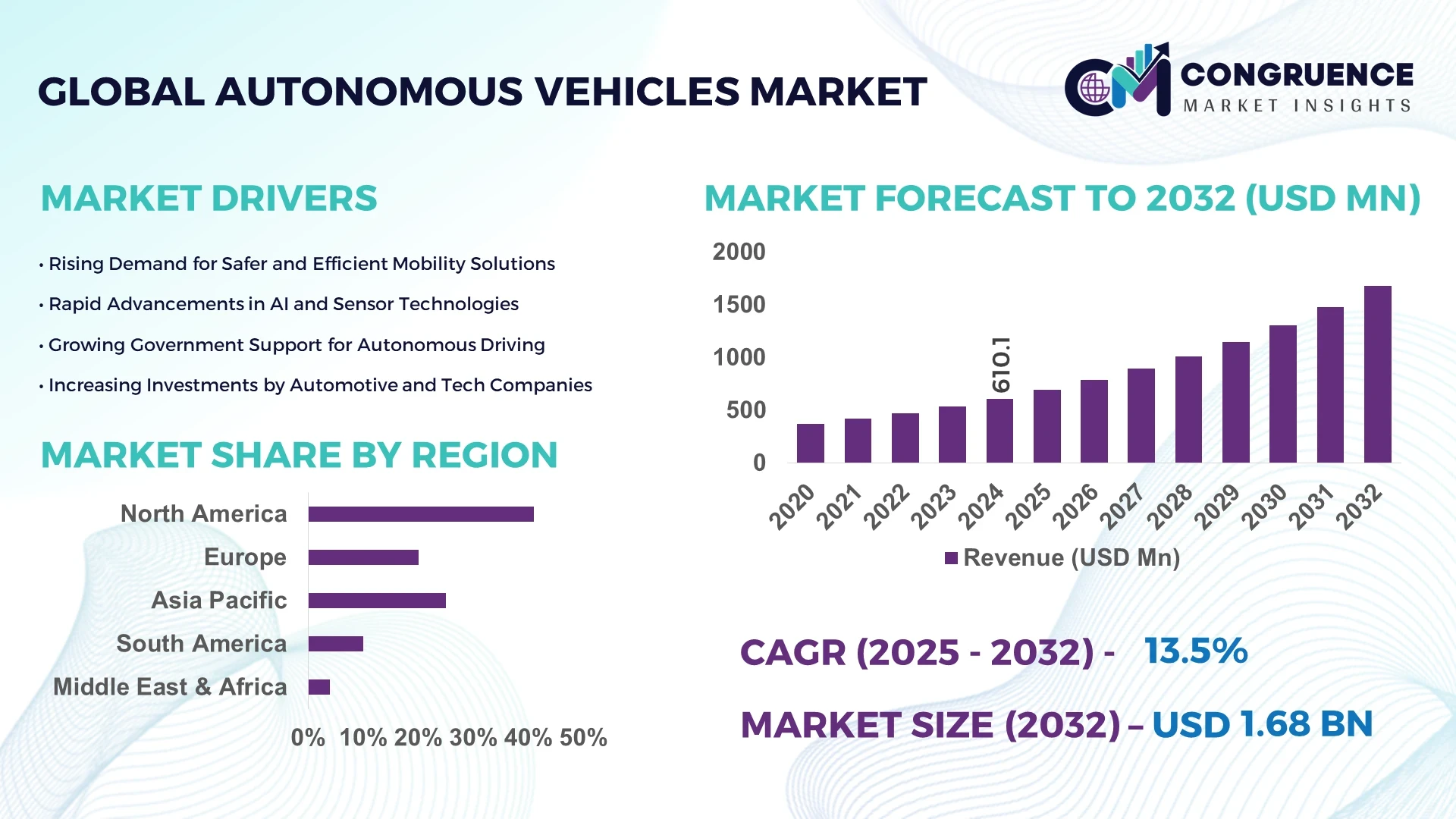

The Global Autonomous Vehicles Market was valued at USD 610.1 Million in 2024 and is anticipated to reach a value of USD 1680.23 Million by 2032 expanding at a CAGR of 13.5% between 2025 and 2032. The growth is driven by increasing adoption of AI-enabled mobility solutions and integration of advanced driver-assistance systems (ADAS) in passenger and commercial vehicles.

The United States dominates the global autonomous vehicles market, supported by large-scale investments exceeding USD 25 billion in R&D by leading automakers and tech firms such as Tesla, Waymo, and General Motors. The country’s advanced infrastructure supports over 420 testing sites for autonomous vehicle trials across 30 states. High consumer acceptance, with approximately 58% of urban commuters expressing willingness to use self-driving transport by 2024, further drives growth. Additionally, the U.S. Department of Transportation’s Autonomous Vehicle Innovation Initiative continues to promote pilot deployments in logistics, ride-hailing, and public transport sectors.

Market Size & Growth: Valued at USD 610.1 Million in 2024, the market is projected to reach USD 1680.23 Million by 2032, expanding at a CAGR of 13.5%, primarily due to advancements in vehicle connectivity and sensor fusion technologies.

Top Growth Drivers: 72% rise in ADAS integration, 45% increase in AI algorithm efficiency, and 38% growth in consumer demand for autonomous mobility solutions.

Short-Term Forecast: By 2028, operational cost per mile is expected to decrease by 25% with up to 40% improvement in route optimization efficiency.

Emerging Technologies: Key innovations include LiDAR miniaturization, Level 4 automation deployment, and AI-based real-time traffic prediction systems.

Regional Leaders: North America (USD 650 Million by 2032), Europe (USD 540 Million by 2032), and Asia-Pacific (USD 490 Million by 2032) — each showing distinctive trends in urban mobility, EV integration, and smart road infrastructure development.

Consumer/End-User Trends: High adoption among logistics and mobility-as-a-service (MaaS) operators, with growing interest from last-mile delivery providers and autonomous taxi networks.

Pilot or Case Example: In 2024, Waymo’s Phoenix-based pilot achieved a 35% reduction in travel time and 22% improvement in route precision across its fleet.

Competitive Landscape: Tesla leads with approximately 21% market share, followed by Waymo, Cruise, Baidu Apollo, and Aurora Innovation as key competitors driving technological evolution.

Regulatory & ESG Impact: Governments worldwide are implementing autonomous mobility frameworks, carbon-neutral transport mandates, and incentive schemes to promote safer and sustainable driving automation.

Investment & Funding Patterns: Over USD 42 billion invested globally in 2023–2024, with strong venture capital inflows into AI-powered navigation, sensor systems, and cybersecurity solutions for autonomous vehicles.

Innovation & Future Outlook: Integration of autonomous fleets with urban smart grids, 5G-based vehicle communication, and hybrid AI ecosystems are expected to redefine next-generation transport infrastructure by 2032.

The global autonomous vehicles market is transforming multiple sectors, including logistics, passenger mobility, defense, and public transportation. Rapid advancements in perception sensors, machine learning algorithms, and vehicle-to-everything (V2X) communication are improving operational efficiency and safety standards. Emerging product innovations, such as energy-efficient electric autonomous fleets and adaptive AI navigation systems, are driving sustainable expansion. Regulatory incentives promoting low-emission vehicles and AI-driven transport systems are supporting large-scale commercialization. With increasing demand from Asia-Pacific and North American economies, the market is poised for accelerated technological evolution and broader consumer acceptance in the coming decade.

The strategic relevance of the Autonomous Vehicles Market lies in its transformative potential to redefine mobility, logistics, and infrastructure management globally. This sector integrates cutting-edge AI, sensor fusion, and high-performance computing to deliver enhanced efficiency and safety. Compared to traditional vehicle automation systems, deep-learning-based perception modules deliver a 45% improvement in real-time decision accuracy and collision avoidance. North America dominates in production volume, while Europe leads in technology adoption with over 61% of enterprises integrating autonomous fleet management systems by 2024. By 2027, advancements in 5G-enabled vehicle-to-everything (V2X) communication are expected to cut operational latency by 38%, enabling smoother coordination between autonomous fleets and smart city infrastructure.

From a sustainability perspective, firms are committing to ESG-linked initiatives such as achieving a 30% reduction in carbon emissions from autonomous fleet operations by 2030 through electrification and energy-optimized routing. In 2024, Japan achieved a 28% reduction in logistics downtime using AI-driven predictive mobility management implemented in Tokyo’s smart transport grid. Strategic partnerships between automakers and technology providers are accelerating commercial adoption, particularly in industrial automation, ride-hailing, and defense logistics applications. Going forward, the Autonomous Vehicles Market will serve as a pillar of resilience, compliance, and sustainable growth, integrating intelligent infrastructure with data-driven decision-making for the next generation of urban mobility ecosystems.

The growing investment in artificial intelligence and vehicle connectivity is significantly accelerating the Autonomous Vehicles Market. In 2024, global R&D spending on autonomous driving technologies surpassed USD 40 billion, primarily focused on AI-based navigation and decision systems. Advanced connectivity solutions—such as 5G-enabled V2X communication—allow vehicles to share real-time data, reducing traffic congestion by up to 25% and improving travel efficiency. Cloud-based fleet management platforms and edge computing are further enabling predictive analytics and adaptive control mechanisms, optimizing vehicle operations under dynamic conditions. These developments are fostering the deployment of autonomous taxis, logistics trucks, and mobility-as-a-service (MaaS) platforms in urban environments, propelling rapid adoption and system-wide integration.

A major restraint in the Autonomous Vehicles Market is the lack of uniform global regulatory frameworks governing safety, liability, and operational standards. Differences between regional testing protocols and certification processes hinder cross-border deployment and scalability. For instance, safety compliance timelines in Europe are longer than in North America by an average of 18 months, slowing commercialization. Additionally, concerns over cybersecurity and data privacy remain significant barriers, with 42% of industry stakeholders citing inadequate digital safety standards as a key obstacle. These inconsistencies create uncertainty for manufacturers and investors, delaying large-scale rollouts and increasing costs associated with compliance and multi-region testing.

The integration of autonomous vehicles within smart city ecosystems presents vast opportunities for growth and innovation. Smart city initiatives worldwide are prioritizing connected infrastructure, with over 280 projects launched in 2024 aimed at deploying self-driving fleets for public transport, logistics, and emergency response. Autonomous traffic management systems can reduce fuel consumption by 15% and improve road utilization efficiency by 35%. Moreover, the use of real-time analytics and IoT-enabled infrastructure allows for adaptive traffic control, enhancing safety and reducing congestion. Emerging economies in Asia-Pacific are investing heavily in such projects, creating lucrative opportunities for manufacturers, software providers, and integrators to develop scalable, energy-efficient, and connected autonomous solutions.

High production costs and dependency on advanced sensors continue to challenge the growth of the Autonomous Vehicles Market. The cost of LiDAR, radar, and camera systems can account for nearly 40% of total vehicle production expenses, making affordability a persistent concern. Supply chain disruptions and semiconductor shortages have further inflated costs, delaying deliveries and limiting scalability. Additionally, calibration and synchronization of multi-sensor data remain technically complex, requiring specialized infrastructure and skilled labor. These challenges increase operational expenditure for manufacturers and slow adoption among mid-tier automotive players. Addressing these cost and technology dependencies is essential for achieving widespread commercialization and sustaining long-term market expansion.

• Expansion of Level 4 and Level 5 Automation Capabilities: The global deployment of Level 4 and Level 5 autonomous vehicles has accelerated, with over 38% of newly tested models in 2024 integrating fully automated navigation systems. These vehicles demonstrate an average reduction of 46% in human intervention during operations. Advanced control algorithms and real-time sensor fusion technologies are improving urban navigation accuracy by 31%, enabling widespread trials across logistics, ride-hailing, and industrial mobility sectors.

• Integration of AI-Powered Predictive Maintenance Systems: AI-driven maintenance systems are emerging as a core trend in the Autonomous Vehicles market. By 2025, predictive maintenance solutions are projected to reduce mechanical failure rates by 28% and lower maintenance costs by 22%. Fleet operators increasingly adopt edge-based monitoring to analyze vehicle health parameters in real time, resulting in downtime reductions of up to 35% across large-scale autonomous fleets.

• Surge in Electric-Autonomous Vehicle Convergence: Around 62% of newly developed autonomous platforms in 2024 were integrated with electric powertrains, signaling a growing shift toward sustainable transport. This convergence is driving a 40% improvement in energy efficiency and a 33% drop in lifecycle emissions compared to hybrid systems. The adoption of battery-swapping and fast-charging infrastructure is further supporting the expansion of electric autonomous fleets across Asia-Pacific and Europe.

• Growth of Smart Infrastructure and 5G-Based Vehicle Communication: The rollout of 5G networks has strengthened autonomous communication capabilities, with 58% of operational test zones now utilizing ultra-low latency connectivity. This infrastructure enhances vehicle-to-everything (V2X) communication speed by 37%, optimizing fleet coordination and data transfer reliability. Urban regions across North America and East Asia are prioritizing smart traffic ecosystems to accommodate autonomous freight, delivery, and mobility services efficiently.

The Autonomous Vehicles Market demonstrates a diverse segmentation across types, applications, and end-users, reflecting the expanding scope of automation and digital mobility. By type, the market spans semi-autonomous, fully autonomous, and conditional automation vehicles, with semi-autonomous models currently dominating global adoption due to their regulatory readiness and affordability. In terms of applications, passenger transportation and logistics lead adoption trends, driven by demand for safety, efficiency, and reduced human intervention. End-user segmentation shows high uptake among automotive OEMs and logistics providers, with defense and public transportation emerging as significant contributors. Collectively, these segments highlight the dynamic evolution of the market as integration of AI, IoT, and electrification continues to redefine operational efficiency and safety across industries.

Semi-autonomous vehicles currently account for 47% of total market adoption, driven by strong commercial deployment and supportive legal frameworks across North America and Europe. These vehicles utilize advanced driver-assistance systems (ADAS) and adaptive cruise control technologies that improve driver safety and fuel efficiency. Fully autonomous vehicles follow with 33% adoption and are expected to experience rapid growth due to technological breakthroughs in sensor fusion, 5G-based connectivity, and machine learning. This segment is expanding at a projected growth rate of 15.8%, the highest among all types, as urban pilot programs and regulatory approvals increase globally. Conditional automation vehicles represent the remaining 20% share, largely concentrated in industrial and logistics sectors where controlled environments favor automation.

Passenger transportation leads the market, accounting for 49% of total application share, supported by strong adoption in ride-hailing and personal mobility sectors. Increasing urbanization and demand for convenience are propelling investment in autonomous taxis and shuttles. Logistics and freight transport follow with 32% market share, driven by the need for continuous, cost-efficient delivery operations. The logistics segment is also the fastest-growing, projected to expand at a 16.2% growth rate through 2032 as e-commerce and long-distance freight automation expand globally. Industrial and defense applications collectively represent 19% of the market, utilizing autonomous vehicles for surveillance, convoy management, and materials handling.

Automotive OEMs dominate the Autonomous Vehicles Market, holding a 45% share as they lead innovation, production, and system integration efforts. Manufacturers such as Tesla, Toyota, and Hyundai continue to expand R&D investments, focusing on energy efficiency, safety enhancement, and AI-assisted driving systems. Fleet operators and logistics firms follow with 35% share, benefiting from reduced labor costs and improved fleet utilization through predictive analytics. The public transportation and defense sectors account for the remaining 20%, focusing on safety, surveillance, and smart mobility networks. Logistics operators represent the fastest-growing end-user group, expanding at an estimated 17.5% growth rate, as automation enables 24/7 operations and route optimization.

North America accounted for the largest market share at 41% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.7% between 2025 and 2032.

The North American market benefits from advanced testing infrastructure and high investment levels exceeding USD 20 billion in autonomous mobility R&D. Europe follows with a 29% share, supported by strong regulatory initiatives and sustainability mandates. Asia-Pacific captured 22% in 2024, fueled by China’s large-scale production capacity and Japan’s robotics integration. South America and the Middle East & Africa collectively held 8%, reflecting early adoption stages but increasing government focus on smart mobility and industrial automation. Globally, autonomous vehicle deployment exceeded 1.8 million units in 2024, with over 60% concentrated in commercial logistics and shared mobility segments. This regional segmentation underscores evolving global patterns in innovation, policy frameworks, and technology adoption.

North America represents the largest market, holding 41% share in 2024, driven by strong innovation ecosystems across the United States and Canada. The region’s demand is led by the automotive, logistics, and defense sectors, which are integrating autonomous systems to improve efficiency and safety. Government support, such as the U.S. DOT’s Automated Vehicle Policy 4.0, encourages large-scale testing and infrastructure readiness. Local players like Waymo and Cruise are pioneering commercial deployment of autonomous taxi fleets, with over 2,000 active vehicles in pilot zones. Consumer adoption is particularly high among enterprise sectors—especially healthcare and finance—where automation enhances operational continuity. The region’s robust AI, sensor, and semiconductor capabilities continue to drive global leadership in autonomous mobility innovation.

Europe captured 29% of the global Autonomous Vehicles Market in 2024, with major contributions from Germany, the UK, and France. The region’s emphasis on regulatory harmonization and eco-compliance, driven by the European Commission’s mobility strategy, is shaping the next phase of automation. Sustainability initiatives are promoting low-emission autonomous fleets, while safety frameworks ensure compliance with Euro NCAP standards. Companies such as Volkswagen and Renault are advancing pilot projects for Level 4 automation in urban areas. Europe’s consumer behavior reflects a preference for explainable AI and transparent decision systems, with 57% of enterprises adopting AI-driven driver-assistance for fleet optimization. The integration of smart mobility corridors across Western Europe further strengthens cross-border autonomous vehicle operations.

Asia-Pacific held 22% of the global market volume in 2024 and is projected to record the fastest expansion through 2032. China, Japan, and South Korea dominate regional production, supported by state-funded programs promoting autonomous and electric vehicle synergy. Over 450 testing zones have been established across China, with more than 80,000 vehicles engaged in real-time AI navigation trials. Japan’s integration of robotics and smart mobility networks drives demand from both consumer and industrial sectors, while India’s investments in intelligent transport systems enhance local adoption. Regional consumer behavior is driven by e-commerce logistics and mobile-based AI applications, creating strong momentum for fleet automation and last-mile delivery innovations.

South America represented 5% of the Autonomous Vehicles Market in 2024, primarily led by Brazil and Argentina. The region’s momentum is supported by infrastructure modernization projects and government-led initiatives to reduce emissions and enhance traffic safety. Emerging smart logistics hubs in Brazil have begun integrating semi-autonomous delivery fleets to streamline urban freight operations, achieving 18% improvement in fuel efficiency. Argentina’s automotive assembly plants are investing in automation and advanced safety systems to align with global manufacturing standards. Regional consumers are increasingly receptive to driver-assist technologies, with 35% of urban fleet operators exploring adoption in logistics and passenger services.

The Middle East & Africa accounted for 3% of the global Autonomous Vehicles Market in 2024, with rapid growth in the UAE, Saudi Arabia, and South Africa. Economic diversification policies, particularly under UAE Vision 2031 and Saudi Vision 2030, are promoting investments in autonomous mobility infrastructure. The UAE’s Roads and Transport Authority deployed pilot self-driving taxis and shuttles across Dubai, achieving 25% improvement in route efficiency. Local consumer behavior emphasizes premium autonomous features and AI-based navigation in luxury and public transport fleets. Growing partnerships between regional governments and global technology firms are expected to accelerate market adoption across logistics, oil & gas, and construction sectors.

United States – 29% Market Share: Dominance driven by advanced R&D capacity, large-scale pilot testing, and strong private-sector investments in autonomous mobility ecosystems.

China – 21% Market Share: Leadership supported by extensive manufacturing capabilities, rapid urban smart infrastructure expansion, and government-backed AI-driven vehicle innovation programs.

The global Autonomous Vehicles market is moderately consolidated, with the top five players accounting for approximately 48% of the total market share in 2024. Around 65 active competitors operate globally, ranging from established OEMs to emerging tech start-ups focusing on sensor fusion, AI algorithms, and vehicle connectivity. Intense competition is driven by innovation, where over 70% of leading companies have increased R&D spending toward Level 4 and Level 5 automation in the past two years.

Strategic partnerships and collaborations have surged by 28% year-over-year, as automakers and technology firms aim to accelerate commercialization timelines. Notably, 40% of new collaborations are focused on enhancing LIDAR accuracy and real-time object detection. Mergers and acquisitions also remain a key competitive strategy—more than 15 notable deals occurred in 2023 and 2024, particularly in the autonomous driving software and battery integration domains.

In terms of regional competition, North America dominates with 38% of global players headquartered there, followed by Europe with 31%. Asia-Pacific players are rapidly gaining ground due to aggressive government-backed pilot projects and rising investment in connected infrastructure. Technological differentiation—especially advancements in machine vision, edge computing, and vehicle-to-everything (V2X) communication—has become the primary competitive edge among top market participants.

The overall competitive landscape continues to evolve toward ecosystem-based collaboration, with the focus shifting from standalone vehicle automation to integrated mobility-as-a-service (MaaS) solutions, supported by cloud and 5G technologies.

Baidu, Inc.

Uber Advanced Technologies Group

Aurora Innovation, Inc.

Zoox, Inc.

Pony.ai

NVIDIA Corporation

Mobileye Global Inc.

Aptiv PLC

Nuro, Inc.

AutoX Inc.

Continental AG

Hyundai Motor Group

The Autonomous Vehicles market is undergoing rapid transformation driven by advancements in AI-powered perception systems, sensor fusion, and connectivity technologies. Currently, over 78% of autonomous vehicles in active development utilize multi-sensor integration combining LiDAR, radar, and camera-based systems for enhanced environmental mapping and object detection accuracy. Machine learning algorithms and deep neural networks remain core technologies, enabling vehicles to interpret complex traffic data and make split-second driving decisions with over 95% accuracy in controlled conditions.

The growing integration of 5G connectivity is revolutionizing real-time communication between vehicles (V2V) and infrastructure (V2I), significantly improving route optimization, traffic flow, and accident prevention. Approximately 60% of new autonomous prototypes launched in 2024 incorporated 5G-enabled telematics modules to enhance responsiveness and situational awareness. Additionally, edge computing technologies are increasingly adopted to minimize latency and reduce dependence on cloud-based data centers, improving reaction times by nearly 40% during critical driving scenarios.

Emerging technologies such as quantum computing simulations, reinforcement learning for adaptive driving, and high-definition mapping platforms are shaping the next phase of innovation. The adoption of software-defined vehicle (SDV) architecture is further streamlining over-the-air updates, cybersecurity management, and continuous performance optimization. Collectively, these advancements are positioning autonomous vehicles as the cornerstone of future intelligent mobility ecosystems, emphasizing safety, efficiency, and self-learning capabilities.

In late 2023, Waymo LLC completed over 7 million miles of fully autonomous driving in real-world dispatch service, demonstrating a lower crash rate compared to human drivers across multiple urban geographies.

In September 2024, Tesla, Inc. announced version 12.5.2 of its Full Self-Driving (FSD) software, achieving roughly 3× improvement in miles between driver interventions compared to the previous version.

In December 2024, Baidu, Inc.’s Apollo Go division received the first right-hand-drive licensed pilot for autonomous vehicle testing in Hong Kong, permitting ten vehicles on defined routes from December 2024 through 2029.

In December 2024, Cruise LLC – majority-owned by General Motors Company – announced it will cease robotaxi business funding and fold its AV team into GM’s driver-assist division, marking a strategic pivot away from commercial autonomous mobility.

The report on the Autonomous Vehicles Market covers a comprehensive range of segments across vehicle types, applications, end-users, technologies, and geographic regions. On the vehicle-type dimension, it examines semi-autonomous, fully autonomous and conditional-automation categories, including commercial fleets, robotaxi models and industrial applications. In terms of application areas, the scope includes passenger mobility (ride-hailing, taxis), logistics and freight transport, public transportation and defence/industrial use cases. End-user sectors evaluated comprise automotive OEMs, mobility service operators, logistics companies, public transport authorities, and emerging smart-city integrators.

Geographically, the study addresses major regions—North America, Europe, Asia-Pacific, South America, Middle East & Africa—highlighting regional infrastructure readiness, regulatory frameworks, urbanisation trends and manufacturing bases. Technologically, the report analyses enabling technologies such as LiDAR, radar, camera systems, sensor-fusion platforms, AI/ML perception modules, V2X communications, 5G/6G connectivity, software-defined vehicles and autonomous fleet-management systems. It also delves into niche segments like last-mile autonomous delivery vehicles, robotaxi fleets, autonomous shuttles and retrofit autonomous systems for older fleets. Industry-focus areas include partnerships between automakers and tech firms, pilot programmes in smart cities, commercialisation models, insurance and liability frameworks, and sustainability/ESG implications for autonomous mobility. The breadth of the report is intended for decision-makers seeking a unified view of market structure, technology readiness, application deployment, regional dynamics and future pathways for autonomous vehicles.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 610.1 Million |

Market Revenue in 2032 | USD 1680.23 Million |

CAGR (2025 - 2032) | 13.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Waymo LLC, Tesla, Inc., Cruise LLC, Baidu, Inc., Uber Advanced Technologies Group, Aurora Innovation, Inc., Zoox, Inc., Pony.ai, NVIDIA Corporation, Mobileye Global Inc., Aptiv PLC, Nuro, Inc., AutoX Inc., Continental AG, Hyundai Motor Group |

Customization & Pricing | Available on Request (10% Customization is Free) |