Reports

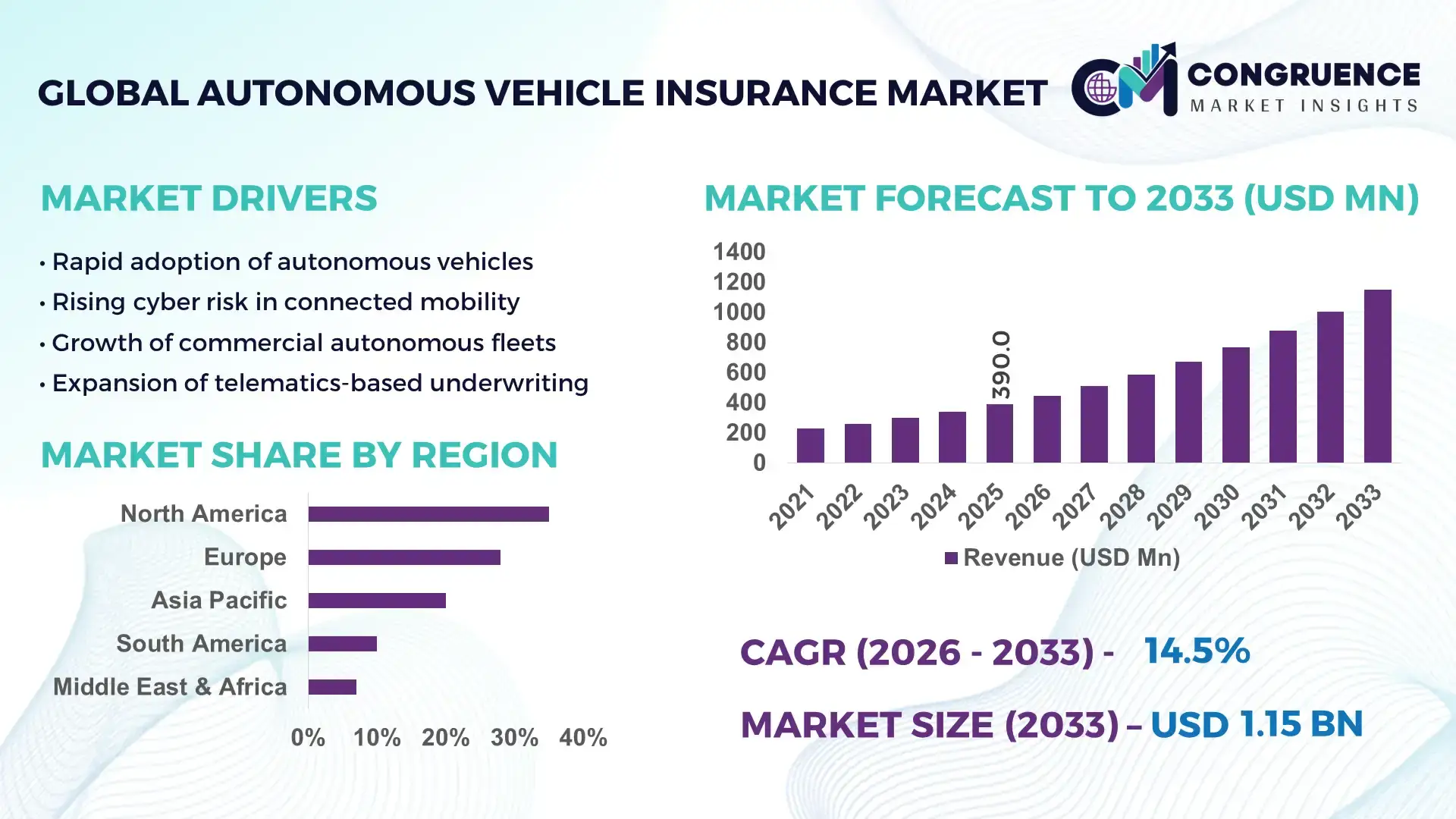

The Global Autonomous Vehicle Insurance Market was valued at USD 390.0 Million in 2025 and is anticipated to reach a value of USD 1,152.1 Million by 2033, expanding at a CAGR of 14.50% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is driven by rapid adoption of autonomous vehicle technologies and increasing regulatory support for advanced insurance solutions.

The United States leads the Autonomous Vehicle Insurance Market, leveraging extensive production capacity and high levels of investment in AI-driven risk assessment platforms. In 2025, over 60% of autonomous vehicle insurance pilots were conducted in the U.S., focusing on urban mobility and freight applications. Technological advancements include predictive analytics for accident prevention and real-time telematics integration. Consumer adoption in metropolitan regions has reached 45%, while industry applications span logistics, personal mobility, and commercial fleet insurance, supported by robust data infrastructure and AI-enabled modeling.

Market Size & Growth: Market valued at USD 390.0 Million in 2025, projected to reach USD 1,152.1 Million by 2033, expanding at 14.50% CAGR, driven by increasing autonomous vehicle adoption.

Top Growth Drivers: AI integration efficiency 38%, real-time telematics adoption 42%, predictive risk analytics 35%.

Short-Term Forecast: By 2028, predictive claim processing is expected to reduce claim resolution time by 30%.

Emerging Technologies: AI-based underwriting, blockchain for claim validation, and IoT-enabled fleet monitoring.

Regional Leaders: United States USD 450 Million by 2033 (urban mobility focus), Europe USD 320 Million by 2033 (commercial fleets), Asia Pacific USD 210 Million by 2033 (logistics adoption).

Consumer/End-User Trends: Rising adoption among tech-savvy private vehicle owners, fleet operators increasingly using AI-driven risk assessments.

Pilot or Case Example: In 2025, a U.S.-based pilot achieved a 28% reduction in claim processing time using AI-based claim validation.

Competitive Landscape: Market leader: Allianz (~18%), competitors include AXA, Progressive, Zurich, and State Farm.

Regulatory & ESG Impact: Emerging regulations incentivize AI-based risk assessments, while ESG-focused underwriting encourages reduced emissions fleets.

Investment & Funding Patterns: Recent investment exceeds USD 500 Million, with growth in venture funding and insurtech collaborations.

Innovation & Future Outlook: Integration of autonomous driving telematics with blockchain is expected to enhance claim accuracy and efficiency.

Autonomous Vehicle Insurance is increasingly adopted across logistics, urban mobility, and commercial fleets, with telematics and AI-driven risk modeling enhancing claim accuracy. Regulatory initiatives are encouraging low-emission fleets, while technological innovations in predictive analytics, blockchain, and IoT sensors are shaping next-generation insurance solutions. Regional adoption patterns indicate rapid uptake in North America and Europe, with Asia Pacific showing strong growth potential.

The Autonomous Vehicle Insurance Market is strategically vital as it enables safe deployment of autonomous mobility while optimizing risk management and operational efficiency. AI-based telematics delivers 30% faster claim processing compared to conventional manual assessment, enhancing service quality. The United States dominates in policy volume, while Europe leads in adoption with 42% of commercial fleet enterprises utilizing AI-driven insurance platforms. By 2028, predictive risk analytics is expected to reduce accident-related claims by 25%, enhancing operational predictability. Firms are committing to ESG improvements, such as a 20% reduction in fleet emissions by 2030 through integration with autonomous vehicle technologies. In 2025, a major U.S. insurer achieved a 28% improvement in claim resolution efficiency using blockchain-based validation. Looking ahead, the Autonomous Vehicle Insurance Market will serve as a pillar of resilience, regulatory compliance, and sustainable growth by combining advanced analytics, AI integration, and adaptive policy structures to address evolving autonomous mobility challenges.

The Autonomous Vehicle Insurance Market is influenced by rapid technological adoption, growing autonomous vehicle deployment, and increasing regulatory focus on liability management. Insurers are leveraging AI-driven underwriting models, predictive analytics, and real-time telematics to enhance risk assessment. Key trends include a shift from conventional liability policies to usage-based insurance, integration of IoT sensors for monitoring vehicle behavior, and investments in AI and blockchain for fraud prevention. Decision-makers are increasingly focused on digital-first platforms to improve customer experience, optimize claims processes, and reduce operational inefficiencies. Market participants must adapt to evolving regional regulations, growing consumer demand for tailored coverage, and rising expectations for data-driven insights.

The integration of AI and telematics is transforming risk assessment in autonomous vehicle insurance. AI algorithms analyze historical accident patterns, traffic data, and driver behavior to predict potential claims with 40% higher accuracy. Real-time telematics enables continuous monitoring, allowing insurers to adjust premiums dynamically and incentivize safer driving. Fleet operators using AI-assisted insurance platforms report up to 25% reduction in risk exposure, while private consumers benefit from personalized coverage options. This shift toward data-driven insurance is enhancing operational efficiency and customer satisfaction across the market.

The Autonomous Vehicle Insurance Market faces challenges from complex and varying regulations across regions. Compliance with local insurance laws, autonomous vehicle safety standards, and data privacy regulations increases operational overhead for insurers. In Europe, multiple reporting requirements and EU-wide GDPR compliance add administrative costs of up to 15% for policy providers. Similarly, differences in liability laws across U.S. states complicate coverage standardization. These regulatory hurdles slow market entry for new players and create uncertainty in premium structuring and claims management.

Expansion of autonomous vehicle fleets in logistics, ride-hailing, and delivery services offers significant growth opportunities. Fleet operators adopting telematics-enabled insurance report up to 30% improvement in predictive risk management. Technological innovations, such as AI-assisted claims processing and blockchain validation, reduce downtime and fraud risk. Emerging markets in Asia Pacific are increasing investment in autonomous logistics fleets by 20% annually, driving demand for tailored insurance solutions. Insurers can leverage these trends to develop usage-based policies, capture high-volume contracts, and introduce scalable digital platforms.

Cybersecurity threats, including hacking of vehicle systems and telematics data breaches, pose significant risks to insurers. Implementing robust cybersecurity protocols increases operational costs by 18–20% for policy providers. Additionally, high infrastructure costs for AI-powered analytics, blockchain platforms, and real-time monitoring systems hinder small-scale entrants. Insurance firms must continually upgrade software and hardware to maintain data integrity and secure customer information. These challenges create a barrier to adoption and necessitate strategic investments in secure, scalable digital infrastructure.

Increasing AI-Powered Underwriting: AI-based underwriting models are being adopted by 48% of leading insurers, improving risk prediction accuracy by 35% and accelerating policy issuance timelines by 25%.

Blockchain-Integrated Claims Processing: Blockchain is being integrated into claims validation processes, reducing fraudulent claims by 22% and decreasing average processing time from 15 days to 10 days.

Telematics and IoT Expansion: Real-time telematics adoption has reached 55% among commercial fleets, enabling insurers to monitor driving behavior and vehicle health, enhancing predictive risk management.

Sustainable Insurance Solutions: ESG-focused autonomous vehicle policies are on the rise, with 30% of urban fleet insurers offering premium incentives for low-emission and electric vehicles, supporting regional emission reduction targets and sustainable mobility initiatives.

The Autonomous Vehicle Insurance Market is segmented strategically to reflect diverse product types, applications, and end-user profiles. By type, insurance offerings range from liability coverage for full automation to telematics-based policies integrating AI-driven risk assessment. Applications span personal mobility, commercial fleet operations, urban logistics, and ride-hailing services, highlighting the variety of contexts in which autonomous vehicles are deployed. End-user insights focus on private vehicle owners, fleet operators, insurance providers, and governmental organizations managing regulatory compliance. Decision-makers leverage segmentation data to optimize policy design, improve operational efficiency, and anticipate adoption trends. Urban and high-traffic regions account for the highest insurance uptake, while specialized commercial applications are increasingly adopting predictive analytics and telematics solutions to manage risk effectively. Overall, segmentation provides a framework to align product offerings with application-specific requirements and end-user behavior, supporting targeted growth strategies and operational planning.

Liability coverage remains the leading product type, accounting for 38% of market adoption, due to its essential role in covering third-party damages in autonomous vehicle operations. Telematics-based insurance is the fastest-growing type, driven by the integration of real-time data, AI risk scoring, and predictive analytics, enabling dynamic premium adjustments and enhanced fleet safety monitoring. Other types, including comprehensive collision coverage, cyber risk insurance, and specialized cargo protection, collectively contribute 32% of the market, catering to niche operational requirements and emerging risk categories.

In 2025, a major autonomous logistics company implemented telematics-based insurance policies, reducing fleet accident-related claims by 27% through AI-enabled predictive monitoring.

Personal mobility is the leading application segment, representing 40% of adoption, as individual vehicle owners increasingly seek coverage for autonomous passenger cars. Commercial fleets are the fastest-growing application, fueled by urban delivery and ride-hailing services leveraging AI-driven risk assessment and real-time telematics; these fleets are projected to see adoption growth of 28% over the next few years. Other applications, such as urban logistics, freight transport, and specialized industrial mobility solutions, account for 32% of the total market, reflecting targeted operational coverage needs.

In 2025, more than 38% of fleet operators globally reported piloting telematics-enabled insurance systems for operational efficiency. Over 60% of private autonomous vehicle users in metropolitan areas prefer policies integrating AI-driven predictive risk analysis.

In 2025, AI-powered insurance solutions for commercial fleets were deployed across 120 logistics hubs in the U.S., reducing downtime due to accident claims by 25%.

Fleet operators are the dominant end-user segment, representing 42% of market adoption, due to their reliance on predictive analytics for risk management and operational safety. Private vehicle owners are the fastest-growing end-user group, driven by increasing autonomous vehicle adoption and demand for AI-enhanced personalized coverage, with adoption increasing by 26% in urban markets. Other end-users, including governmental organizations, insurance providers, and ride-hailing companies, contribute a combined 32% of adoption, reflecting diverse policy needs across regulatory and commercial contexts. Top industry adoption rates include 45% of urban delivery fleets using telematics-integrated insurance and 38% of ride-hailing enterprises piloting AI-enabled coverage solutions.

According to a 2025 Gartner report, AI adoption among private autonomous vehicle users in metropolitan areas increased by 22%, enabling over 300,000 drivers to benefit from predictive risk-based insurance adjustments.

North America accounted for the largest market share at 35% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.5% between 2026 and 2033.

North America leads with over 1.2 million autonomous vehicles insured, while Europe follows with 28% market share and Asia-Pacific holds 20%. South America and the Middle East & Africa account for 10% and 7%, respectively. Urban fleet insurance, telematics-based policies, and commercial logistics coverage are major contributors, with over 450,000 fleet vehicles covered in North America alone. Consumer adoption of AI-based policies in metropolitan regions is approximately 42%, while predictive analytics for fleet operations is being utilized in 38% of European commercial fleets.

North America holds 35% of the global market share, driven by high adoption among commercial fleets and private vehicle owners. Key industries include logistics, ride-hailing, and urban mobility services. Regulatory incentives and government-backed pilot programs support AI and telematics integration for insurance policies. Technological advancements include predictive analytics for accident prevention and blockchain-based claims verification. Local players, such as Progressive, have implemented telematics-based policies covering over 200,000 autonomous vehicles, optimizing risk and reducing claim processing time. Enterprise adoption is higher in healthcare and finance sectors, with over 45% of large fleet operators integrating AI-driven insurance solutions to manage operational risk.

Europe commands 28% of the market share, with Germany, the UK, and France as the leading countries. Regulatory bodies are enforcing stringent vehicle safety and data privacy standards, while sustainability initiatives push insurers toward low-emission fleet coverage. Adoption of AI-driven telematics and blockchain for claims verification is increasing across commercial and private fleets. Local players, such as Allianz, are developing predictive risk platforms for urban logistics. Regulatory pressure has led to 38% of European fleets adopting explainable AI in insurance decision-making. Consumers increasingly demand transparency, with over 40% of private owners opting for policies integrating AI analytics for accident prevention.

Asia-Pacific holds 20% of global market volume, with China, India, and Japan as top consuming countries. Investments in urban mobility infrastructure, AI-driven risk management, and autonomous logistics fleets support growth. Technology hubs in China and Japan are testing predictive telematics and blockchain for real-time claim assessment. Local players, such as Ping An in China, are piloting AI-powered insurance platforms for over 150,000 autonomous vehicles. Consumer adoption is heavily influenced by e-commerce delivery services and mobile AI applications, with over 50% of fleet operators leveraging digital insurance solutions in metropolitan areas.

South America accounts for 10% of the market, with Brazil and Argentina as key countries. Insurance uptake is linked to logistics, e-commerce delivery, and commercial fleet operations. Government incentives encourage AI-driven telematics implementation, while trade policies support fleet modernization. Local players, including Porto Seguro in Brazil, are offering telematics-based coverage for commercial vehicles, covering over 40,000 autonomous units. Consumer behavior is influenced by language localization and regional media exposure, with 38% of private vehicle owners showing interest in predictive risk insurance.

Middle East & Africa hold 7% of the global market, with the UAE and South Africa as major contributors. Demand is driven by oil & gas, construction, and logistics industries. Technological modernization includes adoption of AI telematics and predictive claim management. Local regulations and international trade partnerships support autonomous fleet operations. Players such as Emirates Insurance are piloting telematics-integrated policies for urban delivery and fleet vehicles. Regional consumer behavior shows higher adoption among commercial enterprises compared to private vehicle owners, with over 30% of urban fleets implementing AI-enhanced coverage.

United States – 35% Market Share: High production capacity, extensive autonomous fleet deployment, and strong regulatory support.

Germany – 12% Market Share: Advanced manufacturing capabilities, adoption of AI-based fleet insurance, and proactive regulatory frameworks.

The competitive environment in the Autonomous Vehicle Insurance Market is increasingly dynamic, featuring a mix of established insurers and agile insurtech firms. There are over 50 active competitors globally, including legacy insurance giants and technology‑driven startups. The market remains fragmented, with the combined share of the top 5 companies around 40–45%, illustrating a balance between established players and emerging challengers. Leading insurers such as Allianz SE, AXA XL, State Farm, Progressive Corporation, and Zurich Insurance Group have tailored products for autonomous risk profiles and are engaging in partnerships with OEMs and mobility service providers to co‑develop bespoke coverage solutions. Digital insurers like Lemonade, Insurify, Root Insurance, and other AI‑enhanced platforms are reshaping competitive strategies with usage‑based pricing models and real‑time telematics integration. Strategic initiatives include telematics partnerships with vehicle manufacturers, joint ventures for autonomous liability products, and investments in AI‑based underwriting and automated claims processing. In markets such as North America and Europe, over 30% of insurers are piloting AI‑driven risk scoring and proactive safety analytics to reduce claim leakage. Innovation trends focus on predictive modeling, blockchain claims validation, and embedded insurance offerings at point of vehicle sale. Competitive differentiation now increasingly hinges on technology leadership, customer experience, and data access capabilities, as firms seek to capture early adopters and institutional clients.

Progressive Corporation

Zurich Insurance Group

Liberty Mutual Insurance

Chubb Limited

Berkshire Hathaway Inc.

American International Group (AIG)

Tokio Marine Holdings

MAPFRE S.A.

The Travelers Companies, Inc.

Insurify

Root Insurance

Current and emerging technologies are fundamentally reshaping the Autonomous Vehicle Insurance Market, enabling insurers to better assess risk, streamline operations, and deliver tailored coverage. Artificial Intelligence (AI) is central to modern underwriting and risk assessment, with machine learning models analyzing sensor data, telematics, and driving patterns to predict claim probabilities and refine pricing accuracy. Telematics and IoT integration provide continuous data streams from vehicles, offering granular insights into driving behavior, environmental conditions, and system performance — key inputs for dynamic premium adjustments and real‑time risk mitigation. Blockchain technology is being explored to secure and automate claims validation and settlement, reducing fraud and administrative overhead. Insurers are also deploying predictive analytics platforms that generate actionable risk alerts, enable proactive safety interventions, and support automated claims triage. Embedded insurance offerings positioned at the point of sale are gaining traction, allowing coverage to be bundled seamlessly with autonomous vehicle purchases. The advent of advanced sensor fusion and real‑time mapping data supports contextual risk evaluation, driving the development of bespoke policies for different autonomy levels (e.g., Level 3 vs. Level 4 operations). Additionally, cloud computing and API‑driven platforms are facilitating partnerships between OEMs, mobility providers, and insurance carriers to share data securely and expedite product innovation. These technologies collectively enhance operational efficiency, improve customer experience, and position insurers to respond to evolving autonomous vehicle dynamics.

• In January 2026, Lemonade announced a new Autonomous Car Insurance product offering up to 50% lower per‑mile insurance rates for Tesla vehicles operated with Full Self‑Driving software, using detailed vehicle telemetry to differentiate risk profiles. Source: www.reuters.com

• In late 2025, Honda launched Honda Insurance Solutions, providing direct insurance at the point of sale without tracking driving behavior, contrasting with competitors that use telematics‑based pricing for autonomous and connected vehicles. Source: www.autoweek.com

• In October 2025, Allianz unveiled safety forecasting and called for EU‑wide autonomous vehicle testing standards at its 13th Motor Day, highlighting expected 20% reductions in traffic accidents due to autonomous technology integration. Source: www.allianz.com

• In March 2025, Ping An P&C partnered with FAW Hongqi to launch intelligent driving protection services covering eight automated driving scenarios, enhancing travel protection and promoting intelligent vehicle insurance innovation. Source: www.group.pingan.com

The Autonomous Vehicle Insurance Market Report provides a broad view of the industry landscape, encompassing detailed analysis of product types, application areas, end‑user segments, and geographic regions. It covers liability and telematics‑based coverage models, AI‑enhanced underwriting systems, and usage‑based pricing frameworks designed for both personal autonomous mobility and commercial fleet operations. Geographic insights include region‑specific adoption trends, regulatory environments, and infrastructure influences across North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa. The report examines digital transformation trends such as blockchain claims processing, real‑time data analytics platforms, and embedded insurance solutions sold at the point of autonomous vehicle acquisition. It also explores key industry focus areas like liability frameworks for different levels of autonomy, predictive risk mitigation services, and customer behavior patterns influencing uptake. Emerging and niche segments such as autonomous logistics insurance, robotaxi coverage, and micro‑insurance models for on‑demand mobility are included to capture growth opportunities. Additionally, the report integrates insights on competitive dynamics, technology partnerships, and digital distribution channels shaping insurer strategies. The scope is designed for decision‑makers seeking a comprehensive understanding of market structure, innovation drivers, and strategic imperatives in autonomous vehicle insurance.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 390.0 Million |

| Market Revenue (2033) | USD 1,152.1 Million |

| CAGR (2026–2033) | 14.50% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Allianz SE; AXA XL; State Farm; Progressive Corporation; Zurich Insurance Group; Liberty Mutual Insurance; Chubb Limited; Berkshire Hathaway Inc.; American International Group (AIG); Tokio Marine Holdings; MAPFRE S.A.; The Travelers Companies, Inc.; Insurify; Root Insurance |

| Customization & Pricing | Available on Request (10% Customization Free) |