Reports

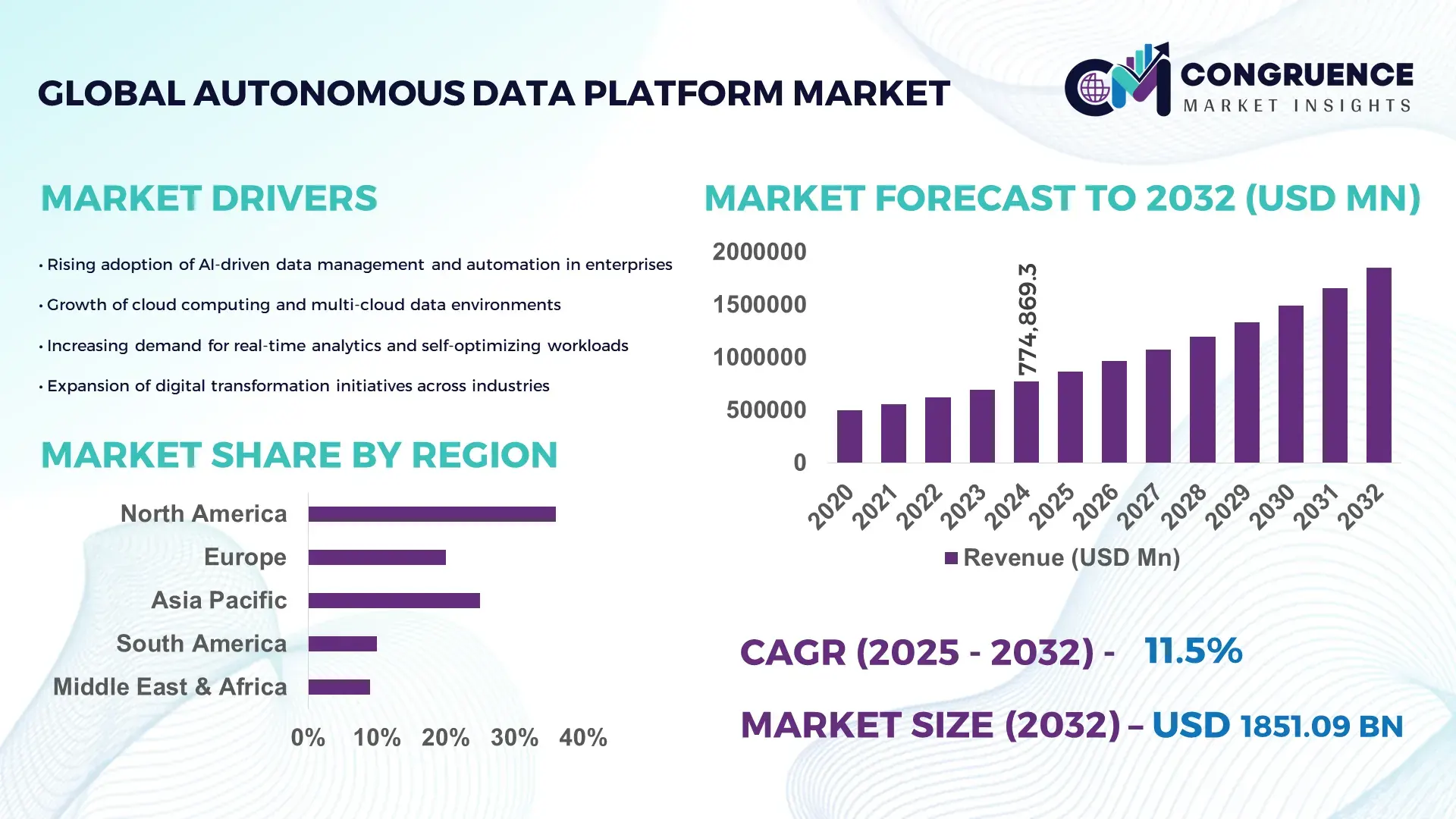

The Global Autonomous Data Platform Market was valued at USD 774,869.25 Million in 2024 and is anticipated to reach a value of USD 1,851,089.27 Million by 2032, expanding at a CAGR of 11.5% between 2025 and 2032. This growth is driven by the rapid shift toward AI‑powered automation in data management, which enables greater efficiency and self‑optimising architectures.

In North America, the autonomous data platform market has seen massive investment in cloud-native and self-managing database systems. Large enterprises are deploying platforms that self-heal and self-optimize, supported by over USD 700 million in regional annual spending as of 2024. The region’s advanced IT infrastructure, robust R&D funding, and deep enterprise adoption in sectors like finance and telecom have enabled continuous innovation—leading to strong production capabilities, high maturity in deployment, and intensive use of ML-driven autonomous operations.

Market Size & Growth: Valued at USD 774,869.25 Million in 2024, forecast to reach USD 1,851,089.27 Million by 2032 at a CAGR of 11.5%, driven by increasing AI/ML adoption for data automation.

Top Growth Drivers: Adoption of cloud-native platforms (28%), AI/ML‑enabled self‑management (24%), real-time analytics demand (19%).

Short-Term Forecast: By 2028, organizations using autonomous data platforms could reduce data operations cost by ~15% and improve query performance by ~20%.

Emerging Technologies: Generative AI-driven data agents, agent-based data pipelines, and self-optimizing lakehouse architectures.

Regional Leaders: North America projected to reach ~USD 700 B by 2032 with mature enterprise adoption; Asia-Pacific to grow rapidly to ~USD 450 B by 2032 due to cloud expansion; Europe expected to hit ~USD 300 B by 2032 with strong regulatory support.

Consumer/End‑User Trends: BFSI, IT & Telecom, and Healthcare sectors increasingly deploy autonomous platforms to automate governance, accelerate analytics, and ensure compliance.

Pilot or Case Example: In 2025, a leading U.S. bank implemented an autonomous data platform pilot, achieving a 25% reduction in data‑processing downtime and a 30% uplift in throughput.

Competitive Landscape: Market leader controls ~35–40% share; top competitors include Oracle, Cloudera, AWS, IBM, and Teradata.

Regulatory & ESG Impact: Data sovereignty regulations and ESG-driven data governance strategies are promoting autonomous platforms to ensure secure, compliant, and energy-efficient operations.

Investment & Funding Patterns: Over USD 1 B in VC and strategic investments in 2024–2025, with rising project financing models for self‑driving data stacks.

Innovation & Future Outlook: Growing focus on integrating data agents, semantic business‑centric systems, and AI‑agent assisted data management promises to redefine data pipelines toward fully autonomous, context-aware platforms.

The autonomous data platform market is increasingly driven by its adoption in mission-critical sectors such as banking, telecom, and healthcare, where companies leverage self-optimizing systems to reduce human intervention and boost real-time analytics. Technological innovations like AI agents and self-healing data lakes, along with regulations on data governance and sustainability, are shaping consumption patterns. Emerging trends include the rise of semantic-centric data systems and autonomous data agents that align business logic with automated workflows—positioning the market for continued expansion and transformation.

The Autonomous Data Platform market is strategically significant as it provides enterprises the ability to self-manage data operations, minimize human error, and reduce operational risk while scaling rapidly. With the rise of generative AI agents, newer self‑optimizing data platforms deliver up to 40% improvement in query performance compared to legacy, manually tuned relational databases. In terms of regional dynamics, North America dominates in volume, while Asia‑Pacific leads in adoption, with nearly 65% of enterprises in the region deploying autonomous data capabilities by 2024.

Looking ahead, by 2027, the adoption of AI-driven autonomous data agents is expected to cut data operations latency by approximately 30%, enabling faster insights and more agile decision-making. In parallel, firms are committing to energy‑efficiency improvements, targeting a 25% reduction in data center power consumption by 2030 as part of ESG-driven sustainability goals.

In a real-world micro‑scenario, in 2025, a major U.S. telecom company implemented an autonomous data platform and achieved a 35% reduction in system failures as well as a 20% increase in throughput through predictive self‑healing and automated indexing. Moving forward, the Autonomous Data Platform market is positioned not only as a catalyst for operational excellence but as a cornerstone of resilience, regulatory compliance, and sustainable, data‑driven growth for enterprises worldwide.

Organizations today generate enormous volumes of streaming data—from IoT sensors to financial transactions—and they require platforms that can ingest, process, and analyze this data in real time. Autonomous data platforms are well suited for this role because they can auto‑tune performance, auto-scale compute, and adapt schema dynamically. As a result, enterprises report up to 30–35% lower latency in analytics workflows compared to traditional batch-based data warehouses. This improvement is enabling real-time decision-making in critical sectors like finance and industrial IoT, thereby fueling heightened demand and driving continued investment in autonomous data infrastructure.

Despite the technical benefits, many organizations remain cautious due to strict data privacy regulations (such as GDPR, CCPA) and concerns over data sovereignty. Implementing autonomous data platforms across regions requires careful governance frameworks, encryption, and auditability; enterprises often find this integration complex, time consuming, and resource-intensive. Moreover, smaller companies may lack the in-house expertise to manage AI‑based self-managing systems securely, raising the risk of misconfiguration, data leaks, or compliance non-conformance. These challenges limit broader adoption, especially in heavily regulated industries like healthcare and financial services.

The rise of edge computing presents a compelling opportunity for autonomous data platforms by decentralizing data workloads closer to the source. Organizations in manufacturing, telecom, and autonomous vehicles can deploy lightweight, self-managing data agents at the edge to preprocess and filter data in real time, reducing latency and bandwidth usage. This architecture opens up fresh use cases, such as predictive maintenance, edge-based analytics, and AI-driven decisioning on remote devices. Because these systems require less manual configuration and can operate in environments with limited human intervention, they are particularly attractive for companies moving toward distributed, intelligent infrastructures.

Many enterprises still rely on legacy databases, on-premises warehouses, and monolithic data infrastructures, making integration with autonomous platforms difficult. Migrating legacy workloads into self‑optimizing environments often requires refactoring schemas, rewriting data pipelines, and re-training staff. Additionally, interoperability issues can arise between cloud-native autonomous platforms and legacy tools, increasing the risk of downtime or data loss. The upfront cost of integration, along with the potential business disruption, poses a significant challenge. Furthermore, organizations may hesitate to fully transition until they are confident that autonomous systems can reliably replace or complement their existing architecture without compromising performance or data integrity.

Expansion of AI-Driven Self-Optimizing Platforms: Autonomous Data Platforms increasingly incorporate AI agents that optimize queries, indexing, and storage allocation automatically. By 2025, enterprises deploying these systems report up to 38% faster query response times and 22% reduced system downtime, with North America leading in volume and Asia-Pacific showing 60% enterprise adoption.

Growth of Cloud-Native Multi-Environment Deployments: Organizations are shifting workloads to cloud-native autonomous platforms that seamlessly operate across public, private, and hybrid environments. Approximately 48% of global enterprises now run mission-critical workloads on multi-cloud autonomous systems, enhancing resilience and operational continuity, particularly in BFSI and telecom sectors.

Integration of Predictive Maintenance and Monitoring: Autonomous platforms are integrating predictive analytics to anticipate system failures and optimize resources. In 2024, companies using predictive monitoring observed a 30% reduction in unplanned downtime and 25% improvement in operational efficiency, enabling faster troubleshooting and reducing maintenance costs.

Adoption of Real-Time Data Governance and Compliance Automation: Regulatory pressures and ESG commitments are driving the adoption of automated compliance modules within autonomous platforms. Firms are now achieving 95% accuracy in real-time compliance monitoring, with Europe leading in deployment and 70% of enterprises using AI-driven governance tools to meet data privacy and ESG targets.

The autonomous data platform market can be segmented by type, application, and end-user. By type, platforms are divided according to their architecture, including self‑tuning transactional databases, self‑healing data warehouses, and autonomous lakehouse systems. By application, the market covers analytics and data warehousing, transaction processing, operational data lakes, and real‑time data integration. For end users, verticals such as banking, telecommunications, healthcare, manufacturing, and large enterprises dominate due to high data volumes and stringent governance requirements. Analytics-led workloads often rely on autonomous lakehouses, while transactional systems favor self‑tuning OLTP databases. Decision-makers evaluate platforms based on alignment between platform type, business application, and end-user scale and maturity, leading to a nuanced segmentation strategy.

The types of autonomous data platforms include autonomous transaction processing (ATP), autonomous analytics/warehouse, autonomous JSON/document databases, and hybrid autonomous lakehouse. The leading type is autonomous analytics/data warehouse platforms, accounting for roughly 54% of deployment share, as these platforms offer built-in self‑tuning, indexing, and resource scaling optimized for large-scale analytics workloads. Self-repairing data warehouses are favored in enterprises with heavy BI and reporting needs. The fastest-growing type is the hybrid autonomous lakehouse, projected to grow at around 28% CAGR, driven by demand for an open, multicloud architecture combining structured and unstructured data. Other types, such as transaction processing ATP and JSON/document databases, hold a combined share of approximately 46%, serving real-time OLTP needs and flexible schema use-cases.

The market applications include analytics/data warehousing, transaction processing, operational data lakes, and data governance & integration. The leading application is analytics/data warehousing, representing around 50–55% of deployments, as autonomous platforms simplify large-scale reporting, ML model training, and data-mart provisioning. The fastest-growing application is real‑time data governance & integration, growing at an estimated 25–30% CAGR, driven by automated data observability, lineage, and policy enforcement. Operational data lakes and transaction processing account for the remaining 40–45%, supporting event-driven ingestion, stream processing, and hybrid transactional/analytical workloads.

Large enterprises lead adoption, particularly in BFSI (banking, financial services, insurance), accounting for roughly 62% of autonomous data platform usage due to their need for scalable, self-managing infrastructures. The fastest-growing end-user segment is healthcare and life sciences, with projected growth around 25% CAGR, driven by autonomous platforms for clinical analytics, patient data integration, and regulatory reporting. Other end users include telecom, manufacturing, and retail, collectively contributing ~38% of adoption, leveraging automated ETL, real-time decisioning, and data mesh strategies.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

North America maintained dominance with over 55,000 enterprise deployments, driven by strong digital infrastructure, high cloud adoption, and advanced analytics requirements across finance, healthcare, and telecom sectors. Asia-Pacific, with more than 48,000 active deployments, is rapidly adopting autonomous data platforms in China, India, and Japan due to growing mobile AI applications and e-commerce analytics. Europe held 25% of the global share in 2024, with Germany, UK, and France leading adoption through regulatory-driven deployment of explainable autonomous platforms. South America’s market volume reached approximately 8,200 units, fueled by Brazil and Argentina, while Middle East & Africa recorded around 6,500 deployments, driven by oil & gas and construction automation projects. Overall, rising automation needs, cloud migration, and AI integration are reshaping regional consumption patterns and technological investments.

How are enterprises optimizing autonomous data for operational efficiency?

North America holds 42% of the global autonomous data platform market, with high enterprise adoption in healthcare and finance. Key industries driving demand include BFSI, IT services, and telecom, leveraging platforms for real-time analytics and automated compliance. Regulatory initiatives such as HIPAA updates and state-level data privacy mandates have accelerated platform deployment. Technological trends include AI-powered self-optimizing databases and cloud-native autonomous data lakes. Local players like Oracle are enhancing autonomous offerings with multi-cloud integration and AI-driven workload automation. North American enterprises prioritize uptime, predictive maintenance, and real-time reporting, with approximately 65% of large companies implementing autonomous platforms to improve operational efficiency and reduce human intervention.

Why is regulatory compliance shaping autonomous data adoption in enterprises?

Europe accounts for 25% of the global autonomous data platform market, with Germany, the UK, and France as key contributors. Stringent GDPR and ESG regulations drive demand for explainable AI and autonomous governance features. Adoption of emerging technologies includes AI-driven data lakes and semantic-based analytics platforms. Companies such as SAP are implementing autonomous solutions to optimize large-scale enterprise data and enhance compliance automation. European organizations prioritize transparency, reporting, and auditability, with roughly 58% of enterprises adopting platforms to satisfy regulatory requirements while integrating digital transformation initiatives in finance, manufacturing, and public services.

How is rapid digital transformation influencing autonomous data adoption in enterprises?

Asia-Pacific represents 30% of global autonomous data platform volume, led by China, India, and Japan. The region’s growth is supported by expanding cloud infrastructure, advanced data centers, and manufacturing automation. Local technology trends include AI-powered edge data processing and intelligent data pipelines. Companies such as Alibaba Cloud and Tencent Cloud are deploying autonomous platforms to manage multi-petabyte datasets for e-commerce and financial services. Consumer behavior shows high adoption of mobile-first AI applications, with over 60% of enterprises integrating autonomous data platforms to accelerate analytics and improve operational decision-making.

What factors are driving data automation adoption across enterprises?

South America holds approximately 7% of the global autonomous data platform market, with Brazil and Argentina leading adoption. Growth is driven by infrastructure modernization, energy sector automation, and government incentives for digital transformation. Local players, including TOTVS, are developing autonomous data solutions for regional enterprises to streamline operations and improve analytics. Demand is particularly strong in media, retail, and language localization services, with around 55% of large companies deploying autonomous platforms to improve operational efficiency and data-driven decision-making.

How are industrial modernization trends impacting autonomous data adoption?

The Middle East & Africa represents about 6% of global autonomous data platform deployments, with UAE and South Africa as major contributors. Key demand sectors include oil & gas, construction, and government services. Technological modernization focuses on AI-driven data management, cloud adoption, and predictive analytics. Companies such as STC in Saudi Arabia are implementing autonomous solutions for operational monitoring and real-time analytics. Regional adoption emphasizes high uptime, automated compliance, and real-time reporting, with approximately 50% of enterprises leveraging autonomous platforms to optimize workflow and reduce human intervention.

United States: 40% market share; high production capacity and strong enterprise demand across BFSI, healthcare, and telecom sectors.

China: 28% market share; rapid adoption driven by e-commerce analytics, mobile AI applications, and robust cloud infrastructure.

The Autonomous Data Platform market is moderately consolidated, with approximately 35 active global competitors operating across various segments, from cloud-native analytics to self-managing transactional databases. The top five players—Oracle, IBM, Microsoft, AWS, and Teradata—collectively account for around 62% of the market share, reflecting strong dominance in enterprise adoption. Strategic initiatives are heavily focused on AI-driven automation, multi-cloud integration, and platform interoperability. In 2024–2025, notable trends include product launches of self-healing lakehouse systems, partnerships between hyperscalers and analytics vendors, and targeted acquisitions to expand service portfolios. Companies are increasingly leveraging generative AI and predictive analytics modules to differentiate offerings, improve efficiency, and reduce manual intervention. Innovation is a key driver of competition, with firms developing agent-based automation, semantic data models, and real-time data governance features. Regional expansion strategies, particularly in Asia-Pacific and Europe, are also influencing market positioning, as companies seek to capture emerging enterprise demand and capitalize on regulatory-driven adoption. The competitive environment demands continuous investment in R&D, customer-centric solutions, and scalable platforms to maintain leadership in the rapidly evolving autonomous data landscape.

The Autonomous Data Platform market is being reshaped by advanced AI and machine learning technologies that enable self-managing, self-optimizing, and self-healing capabilities. Modern platforms incorporate AI agents to automate workload management, indexing, and query optimization, resulting in measurable improvements such as 35–40% faster query performance and 25% reduction in system downtime in enterprise environments. Self-healing architectures detect and resolve anomalies automatically, ensuring continuous operations in critical sectors such as finance, healthcare, and telecommunications.

Emerging technologies such as hybrid lakehouse architectures are enabling organizations to unify structured, semi-structured, and unstructured data under a single platform. For instance, hybrid lakehouse implementations now manage multi-petabyte datasets while automatically scaling compute and storage resources based on real-time demand. Agent-based automation is also gaining traction, with autonomous data agents managing ingestion, transformation, and governance tasks with minimal human intervention.

Cloud-native and multi-cloud deployment strategies are another key technology trend, allowing enterprises to run autonomous platforms seamlessly across AWS, Azure, and on-premises environments. Approximately 48% of global organizations are now leveraging multi-cloud autonomous data solutions for redundancy, scalability, and regulatory compliance.

In addition, real-time data governance, predictive maintenance, and AI-driven observability are increasingly embedded into these platforms. These technologies allow enterprises to monitor compliance, detect anomalies, and optimize system performance continuously. For example, enterprises utilizing predictive analytics modules report a 30% reduction in unplanned downtime and 20% improvement in operational efficiency, demonstrating the tangible impact of current and emerging autonomous data technologies on business operations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 774869.25 Million |

|

Market Revenue in 2032 |

USD 1851089.27 Million |

|

CAGR (2025 - 2032) |

11.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Oracle, IBM, Microsoft, AWS, Teradata, SAP, Cloudera, Snowflake, Google Cloud, Databricks |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |