Reports

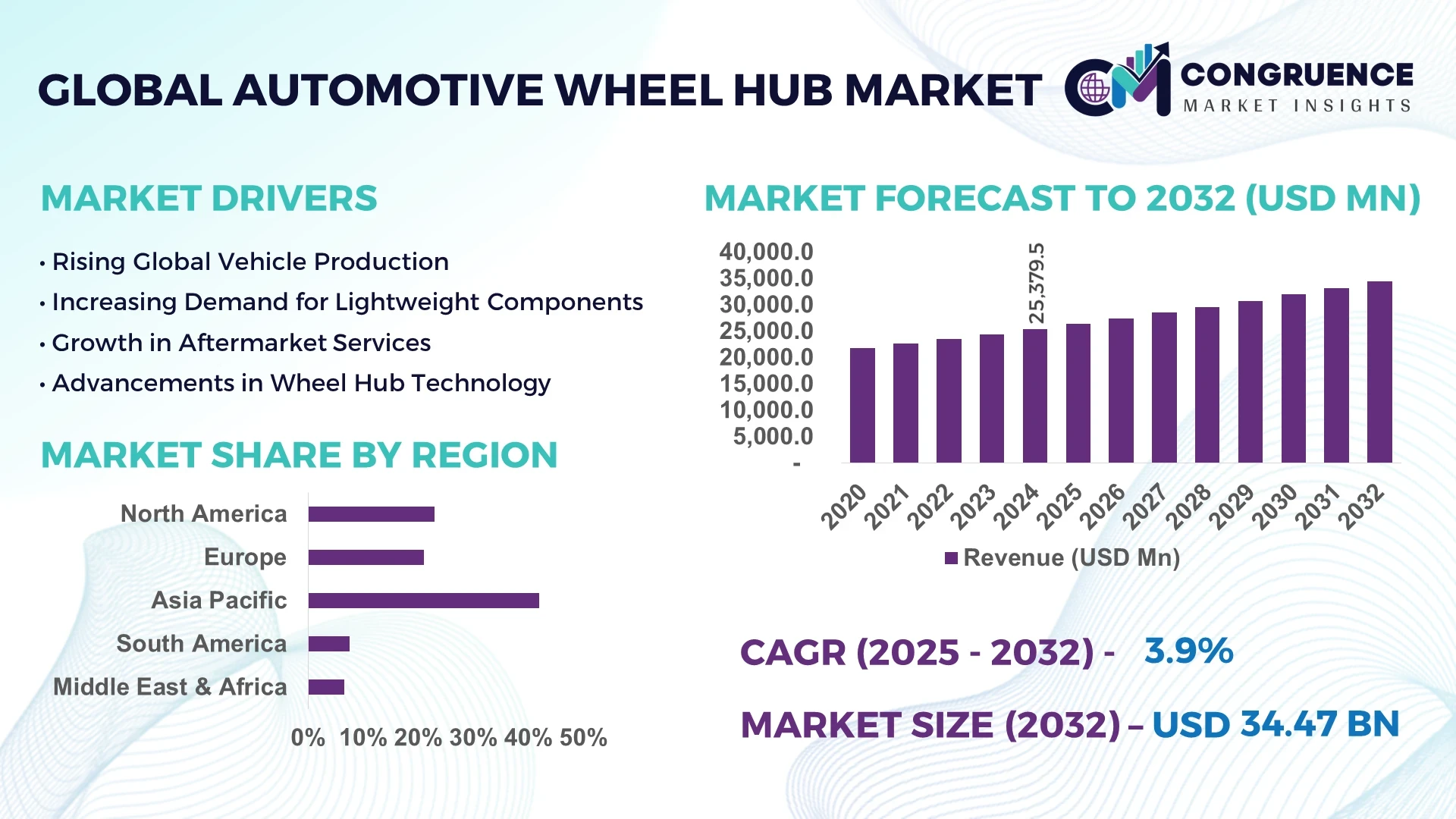

The Global Automotive Wheel Hub Market was valued at USD 25,379.53 Million in 2024 and is anticipated to reach a value of USD 34,467.36 Million by 2032, expanding at a CAGR of 3.9% between 2025 and 2032.

China leads the global automotive wheel hub market, driven by its extensive automotive manufacturing infrastructure and significant domestic production capacity.

The automotive wheel hub market is projected to witness substantial growth over the coming years, primarily driven by increasing global vehicle production and evolving consumer preferences for advanced automotive technologies. In 2022, global vehicle production reached 85.4 million units, indicating a notable 5.7% year-over-year increase. This growth directly correlates with the increased demand for high-performance wheel hub systems, which play a critical role in maintaining vehicle stability and supporting braking systems. Furthermore, the shift towards electric vehicles (EVs) has spurred the need for advanced wheel hubs capable of handling higher torque and ensuring enhanced braking efficiency. The market is also witnessing the adoption of lightweight materials, such as aluminum alloys and carbon composites, which contribute to improving fuel efficiency and reducing overall emissions. Technological advancements, including the integration of smart sensors and predictive monitoring systems, are further transforming the automotive wheel hub market, driving both innovation and demand.

AI is having a significant impact on the automotive wheel hub market, ushering in a new era of intelligent manufacturing, real-time diagnostics, and predictive maintenance. The integration of AI technologies into the design and production of wheel hubs is optimizing both performance and durability. AI algorithms are now used to simulate various conditions, enabling manufacturers to create more efficient and durable wheel hubs, tailored to the specific needs of different vehicle types, including electric and autonomous vehicles. Machine learning models are increasingly being applied to vehicle data collected from onboard sensors, helping to predict potential failures in wheel hubs before they occur, thereby reducing maintenance costs and improving safety.

AI-driven robotics and automation in manufacturing have led to faster production times and consistent quality control, ensuring that wheel hubs meet strict standards. In addition, AI is enhancing the design process by providing manufacturers with insights on optimizing material usage, minimizing weight, and improving strength. As the global automotive industry shifts towards sustainability and energy efficiency, AI is poised to play a crucial role in advancing the development of lightweight, high-performance wheel hubs for electric vehicles. The continued evolution of AI technology is expected to further streamline operations, reduce costs, and improve the overall quality and reliability of wheel hub components in the market.

“In 2024, a major automotive manufacturer successfully implemented an AI-based monitoring system for wheel hubs, which utilized data from onboard sensors to detect real-time performance issues. This proactive maintenance approach allowed for early interventions, significantly reducing unplanned maintenance costs and improving vehicle uptime.”

The growing demand for automotive vehicles, particularly in emerging economies, is a key driver for the automotive wheel hub market. In 2022, global vehicle production exceeded 85 million units, indicating a steady increase in demand. As vehicle production ramps up, the demand for high-quality wheel hubs that ensure safety, performance, and durability has risen sharply. Manufacturers are also focusing on reducing the weight of wheel hubs, which directly impacts fuel efficiency and overall vehicle performance. Additionally, the growing popularity of electric vehicles (EVs), which require wheel hubs designed for higher torque and enhanced braking systems, is further fueling the demand for advanced wheel hub solutions in the market.

While the market for automotive wheel hubs is expanding, high production costs remain a significant restraint. The rising cost of raw materials, particularly advanced alloys and composites used in wheel hub manufacturing, has made it more challenging for manufacturers to maintain cost-effectiveness. Additionally, complex designs and precision engineering required for modern vehicles, including electric vehicles, add to the cost burden. These increased costs could potentially limit the growth of the wheel hub market, especially in regions where cost-sensitive consumers dominate. Manufacturers must balance the demand for high-performance components with the need to manage production costs effectively, which poses a challenge for the broader market.

The rapid growth of the electric vehicle (EV) market presents significant opportunities for the automotive wheel hub sector. As governments worldwide focus on reducing carbon emissions, the shift toward electric vehicles continues to accelerate. According to data, global electric vehicle sales exceeded 10 million units in 2023, with the trend expected to intensify. This shift has created a new demand for wheel hubs designed to accommodate the specific requirements of electric vehicles, such as high torque and efficient braking systems. The increasing adoption of electric vehicles, combined with advancements in battery technologies and charging infrastructure, will drive demand for specialized wheel hubs in the coming years, presenting a substantial opportunity for manufacturers to innovate and expand their product offerings.

One of the primary challenges facing the automotive wheel hub market is the increasing competition and market saturation. As more players enter the market, particularly from emerging economies, manufacturers are facing pressure to differentiate their products while maintaining competitive pricing. In addition, the global automotive supply chain has experienced disruptions in recent years, which have affected the availability of critical components and raw materials, further complicating the competitive landscape. To stay ahead, companies need to continuously invest in research and development to innovate and improve the performance of their wheel hub solutions, while managing costs and maintaining product quality. This challenge is particularly relevant in mature markets where competition is fierce and product differentiation becomes increasingly difficult.

• Growth in Electric Vehicle (EV) Adoption: The shift toward electric vehicles (EVs) is transforming the automotive wheel hub market. With global EV sales surpassing 10 million units in 2023, demand for specialized wheel hubs designed to handle higher torque and improve braking efficiency is rising. Manufacturers are focusing on creating lighter, stronger, and more efficient wheel hubs to meet the specific demands of EVs, which require more advanced and durable components compared to conventional internal combustion engine vehicles.

• Integration of Advanced Materials: The automotive industry is increasingly using advanced materials in the production of wheel hubs. Aluminum alloys and composites are becoming more prevalent, as they provide benefits such as reduced weight and improved fuel efficiency. These materials also contribute to enhanced vehicle performance and safety. As automakers aim to reduce carbon emissions and improve energy efficiency, the demand for lightweight, high-performance wheel hubs is expected to continue growing, especially in regions like Europe and North America.

• Technological Advancements in Manufacturing: The automotive wheel hub market is benefiting from advanced manufacturing technologies, such as additive manufacturing and 3D printing. These technologies enable manufacturers to produce more complex, customized, and lightweight designs for wheel hubs. Automation in production lines is also helping to increase efficiency, reduce labor costs, and ensure higher-quality output. As these technologies continue to advance, they are expected to drive innovations in wheel hub design and manufacturing processes.

• Focus on Sustainability: As sustainability becomes a priority across industries, the automotive sector is also placing greater emphasis on eco-friendly practices. Manufacturers of wheel hubs are increasingly focusing on reducing their carbon footprints through the adoption of greener production processes and materials. This trend is supported by stricter environmental regulations, especially in Europe and North America, which are pushing for reduced emissions and increased energy efficiency in the automotive sector.

The automotive wheel hub market is segmented based on type, application, and end-user insights, providing a clear understanding of the key drivers and trends within the market. In terms of types, the market is divided into various categories, such as steel, aluminum, and composite wheel hubs, each offering unique advantages in terms of weight, strength, and durability. By application, the demand for wheel hubs is growing in passenger vehicles, commercial vehicles, and electric vehicles, with each segment requiring tailored solutions. The end-user insights focus on individual consumers, automotive manufacturers, and aftermarket suppliers, all of whom influence market trends and product development. Understanding these segments helps manufacturers to cater to the specific needs of each group, driving innovation and growth in the automotive wheel hub industry.

The automotive wheel hub market is primarily segmented into steel, aluminum, and composite wheel hubs. The steel wheel hub segment currently leads the market, as steel is a cost-effective and widely used material for wheel hub production. Steel wheel hubs offer strength and durability, making them suitable for a wide range of vehicle types, particularly for commercial vehicles. However, the aluminum wheel hub segment is experiencing the fastest growth, driven by the increasing demand for lightweight materials to enhance fuel efficiency and vehicle performance. Aluminum wheel hubs are commonly used in passenger cars and electric vehicles, offering a significant weight reduction compared to steel. Composite wheel hubs, while less common, are gaining traction due to their potential for even greater weight reduction and improved performance characteristics, making them a promising option for the future.

In terms of application, the automotive wheel hub market can be divided into passenger vehicles, commercial vehicles, and electric vehicles (EVs). The passenger vehicle segment holds the largest share, as it accounts for a significant portion of global vehicle production. Consumer preferences for higher performance, safety, and efficiency continue to drive demand for advanced wheel hub solutions. The electric vehicle segment is the fastest growing due to the rising adoption of EVs, with an increasing need for specialized wheel hubs capable of handling the unique demands of EVs, such as higher torque and enhanced braking systems. The commercial vehicle segment, while growing, is expected to see steady demand as these vehicles require wheel hubs that are durable and able to withstand heavy usage.

The automotive wheel hub market is segmented into individual consumers, automotive manufacturers, and aftermarket suppliers. Automotive manufacturers are the largest end-users of wheel hubs, as they require a wide variety of wheel hubs for different vehicle types. Manufacturers are increasingly focusing on high-performance, lightweight, and cost-effective wheel hubs to meet the growing demand for energy-efficient and sustainable vehicles. The aftermarket segment is also experiencing growth, as consumers seek replacement parts for their vehicles. The individual consumer segment, which includes vehicle owners, plays a significant role in driving demand for replacement and upgraded wheel hubs. As vehicle ownership rises and consumers place more value on vehicle performance, the aftermarket for wheel hubs is expected to continue expanding.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific dominates the automotive wheel hub market due to the massive production of vehicles, especially in countries like China, Japan, and India. The region has a substantial automotive industry, driven by both domestic consumption and export. In addition, rising demand for lightweight and high-performance wheel hubs in electric vehicles (EVs) is further boosting market growth. North America is witnessing significant technological advancements and an increase in electric vehicle adoption, leading to the fast expansion of the market.

North America remains a major hub for the automotive wheel hub market due to the strong presence of automotive manufacturers in the United States and Canada. The region is also home to a growing number of electric vehicle (EV) manufacturers, driving demand for specialized wheel hubs. With the automotive sector focusing on performance, safety, and sustainability, the demand for lightweight, durable wheel hubs has surged. Additionally, the rise in consumer preference for advanced automotive technologies and an increasing emphasis on vehicle efficiency are expected to further contribute to the growth of the market in this region.

In Europe, the automotive wheel hub market is poised for steady growth, primarily driven by the region's focus on high-performance vehicles and electric vehicle adoption. The European automotive industry is at the forefront of sustainability, with manufacturers focusing on reducing the weight of vehicles and improving energy efficiency. The demand for aluminum and composite wheel hubs is particularly high, as these materials help meet stricter environmental regulations. The growing number of EVs in countries like Germany, France, and the UK is also a key driver for the growth of the automotive wheel hub market in Europe.

The Asia-Pacific region leads the automotive wheel hub market, accounting for the largest share due to the high production and consumption of vehicles. Countries like China, Japan, and India are major contributors to the market, with China's vast manufacturing capacity and increasing demand for electric vehicles driving growth. The region has become the manufacturing base for several global automotive brands, and advancements in technology are enabling the production of high-performance wheel hubs. With the rising middle class and growing urbanization in the region, the demand for passenger cars is expected to continue driving the market expansion.

In South America, the automotive wheel hub market is growing, albeit at a slower pace compared to other regions. Brazil and Argentina are the primary markets in this region, with Brazil leading the automotive production. Although the automotive industry in South America faces challenges such as economic fluctuations, demand for lightweight and durable wheel hubs is steadily increasing. As vehicle manufacturing in Brazil increases, especially in the commercial vehicle segment, the need for high-performance and cost-effective wheel hubs is becoming more pronounced. The shift toward electric vehicles and improvements in road infrastructure are expected to boost the market in the coming years.

The Middle East & Africa automotive wheel hub market is witnessing moderate growth, with a significant portion of demand coming from countries like Saudi Arabia, the UAE, and South Africa. In the Middle East, the luxury vehicle segment is particularly strong, driving demand for high-quality and high-performance wheel hubs. In Africa, vehicle demand is growing slowly, but the focus on durability and cost-effectiveness in wheel hub design is driving steady demand in the commercial vehicle sector. As automotive manufacturing and infrastructure improve, the demand for advanced wheel hub solutions is expected to increase in both the Middle East and Africa.

China: 27% – China’s dominance is attributed to its high vehicle production rates and strong presence in the EV market.

United States: 19% – The U.S. holds a significant market share due to its advanced automotive manufacturing capabilities and the rise in electric vehicle adoption.

The automotive wheel hub market is highly competitive, with several global and regional players vying for market share. The market is characterized by technological advancements, with manufacturers focusing on the development of lightweight, durable, and high-performance wheel hubs to meet the demands of both traditional and electric vehicles. Some of the key players in the market are investing in research and development to improve the strength-to-weight ratio of their products, enhance the wheel hub's performance, and reduce vehicle fuel consumption. Partnerships and collaborations between automotive manufacturers and wheel hub suppliers are common, as automakers strive for innovations in their product offerings. The increasing demand for electric vehicles and advancements in materials such as aluminum and composites are expected to further intensify the competition. Additionally, the presence of regional players in key markets like China and India adds a layer of competition, as they strive to expand their share in the rapidly growing automotive sector.

Schaeffler Group

HUBER+SUHNER AG

SKF Group

Zhejiang Asia-Pacific Mechanical & Electronic Co. Ltd.

JTEKT Corporation

Magna International Inc.

NSK Ltd.

GKN Automotive

Mitsubishi Steel Mfg. Co., Ltd.

Aisin Seiki Co., Ltd.

The automotive wheel hub market is experiencing significant technological advancements aimed at enhancing vehicle performance, safety, and sustainability. One of the most notable trends is the integration of sensor technologies into wheel hubs. These sensors monitor parameters such as wheel speed, temperature, and vibrations, providing real-time data to vehicle control systems. This integration is crucial for the functioning of advanced driver assistance systems (ADAS) and autonomous vehicles, contributing to improved safety and performance.

Another significant development is the shift towards lightweight materials in wheel hub manufacturing. Materials like aluminum alloys and composites are increasingly being used to reduce the overall weight of vehicles. This reduction in weight leads to improved fuel efficiency and handling, which are particularly important for electric vehicles (EVs) that require efficient energy consumption. The adoption of these materials also contributes to the overall performance enhancement of vehicles.

Additive manufacturing, commonly known as 3D printing, is revolutionizing the production of wheel hubs. This technology allows for the creation of complex and customized designs that were previously challenging to achieve with traditional manufacturing methods. 3D printing enables rapid prototyping and production, reducing lead times and costs. It also allows for the use of advanced materials that can enhance the performance and durability of wheel hubs.

Moreover, automation and robotics are being increasingly utilized in the manufacturing processes of wheel hubs. These technologies improve precision, reduce human error, and increase production efficiency. Automated systems can perform repetitive tasks with high accuracy, leading to consistent product quality and reduced manufacturing costs. The implementation of these technologies is essential for meeting the growing demand for high-quality wheel hubs in the automotive industry.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In May 2024, Schaeffler presented its TriFinity™ wheel bearing unit, designed for electric vehicles. This innovative unit offers enhanced load capacity and durability, addressing the specific requirements of EVs and contributing to improved vehicle performance.

In April 2024, NSK Ltd. launched a new line of wheel hub bearings featuring advanced sealing technology. These bearings are designed to offer longer service life and improved performance under various driving conditions, catering to the growing demand for high-quality components in the automotive industry.

In March 2024, SKF announced the development of a new wheel hub bearing with integrated sensor technology. This advancement allows for real-time monitoring of wheel hub conditions, enabling predictive maintenance and enhancing vehicle safety and reliability.

The automotive wheel hub market report provides comprehensive insights into the key factors driving growth, challenges, trends, and the competitive landscape within the sector. The market is primarily influenced by the increasing demand for lightweight, durable, and high-performance wheel hubs across various automotive segments. As consumers and manufacturers prioritize safety, efficiency, and sustainability, the demand for advanced materials, including aluminum alloys and composites, continues to rise.

This report covers the full spectrum of the market, including various wheel hub types such as integral, multi-piece, and modular hubs. These are analyzed based on application in passenger vehicles, commercial vehicles, and electric vehicles (EVs). The report also delves into technological innovations, such as sensor integration, which enhances the performance and monitoring capabilities of wheel hubs in modern vehicles.

Additionally, the report highlights regional trends and dynamics, focusing on North America, Europe, Asia-Pacific, and other emerging markets. It provides an in-depth examination of regional preferences, technological adoption, and regulatory factors influencing the automotive wheel hub market. This scope allows stakeholders, including manufacturers, suppliers, and investors, to make informed decisions based on current market conditions and future growth projections.

By identifying key players and their strategic moves, the report aims to provide valuable insights into the competitive landscape, helping businesses understand market positioning and opportunities for expansion. It also covers the key challenges in the market, such as rising production costs and material supply chain issues, and outlines potential strategies to address them.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 25379.53 Million |

|

Market Revenue in 2032 |

USD 34467.36 Million |

|

CAGR (2025 - 2032) |

3.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schaeffler Group, HUBER+SUHNER AG, SKF Group, Zhejiang Asia-Pacific Mechanical & Electronic Co. Ltd., JTEKT Corporation, Magna International Inc., NSK Ltd., GKN Automotive, Mitsubishi Steel Mfg. Co., Ltd., Aisin Seiki Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |