Reports

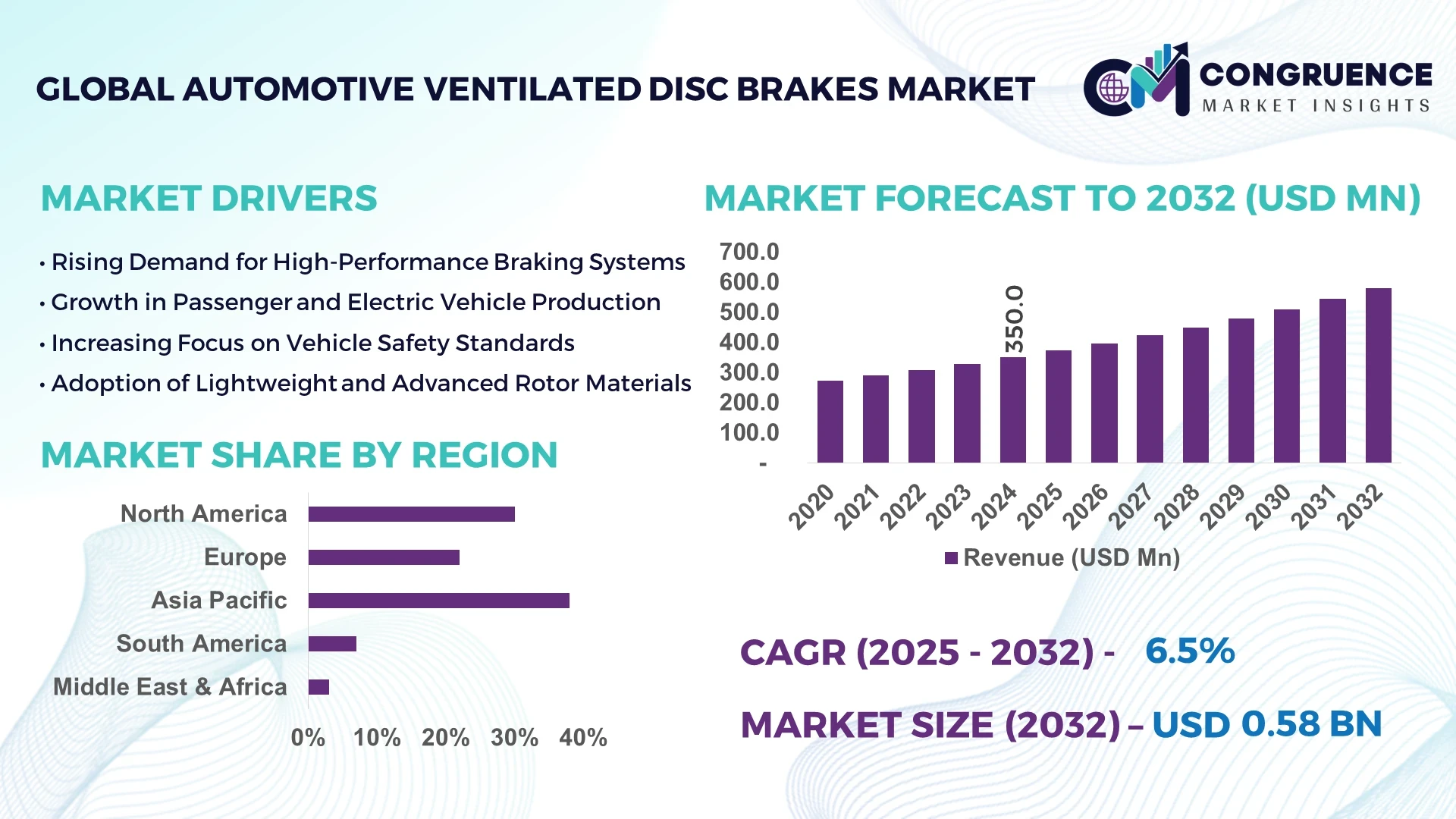

The Global Automotive Ventilated Disc Brakes Market was valued at USD 350.0 Million in 2024 and is anticipated to reach a value of USD 579.2 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032. This growth is primarily driven by increasing vehicle production and stringent braking safety regulations.

In the dominant country of China, production capacity for ventilated disc brakes has surged, with manufacturing output exceeding 26 million vehicles in 2024 and supporting a parts base that grew by approximately 12% year‑on‑year. Investment levels in brake component manufacturing have surpassed USD 2 billion in recent fiscal cycles, while major OEMs are deploying next‑generation ventilated disc systems with enhanced thermal dissipation and lightweight materials. Over 40 % of new brake rotor supply lines now incorporate multi‑vane ventilation designs, and technology alliances with leading sensor firms are accelerating the integration of active braking feedback in passenger and commercial vehicle applications.

Market Size & Growth: The market stood at USD 350.0 Million in 2024, expected to reach USD 579.2 Million by 2032, with a CAGR of 6.5%—driven by rising vehicle output and enhanced safety regulation adoption.

Top Growth Drivers: OEM adoption of ventilated disc technology ~68 %, regulatory mandates on braking performance ~45 %, lightweight material substitution in brake rotors ~32 %.

Short‑Term Forecast: By 2028, average rotor weight reduction is projected at 8% and braking fade time improvement at 10%.

Emerging Technologies: Integration of carbon‑ceramic composite rotors, smart sensor‑embedded brake systems, and AI‑driven thermal management for ventilated discs.

Regional Leaders: Asia Pacific – projected at USD 240 Million by 2032, North America – USD 170 Million by 2032, Europe – USD 140 Million by 2032; Asia shows high OEM index growth, North America leads aftermarket upgrades, Europe emphasizes premium vehicles.

Consumer/End‑User Trends: Passenger vehicles remain the largest end‑user segment, light commercial vehicles are accelerating adoption, and performance vehicle aftermarket upgrades are rising 2.4× faster than standard OEM replacements.

Pilot or Case Example: In 2024, a leading luxury automaker achieved a 14% reduction in brake fade time by deploying a new ventilated disc variant with optimized vane geometry.

Competitive Landscape: Market leader holds ~18% share; other major competitors include three to five prominent firms offering global brake rotor solutions.

Regulatory & ESG Impact: Vehicle safety regulations increasingly mandate high‑performance brake systems, and firms commit to recycling 20% of rotor material by 2027 under ESG frameworks.

Investment & Funding Patterns: Recent investments exceed USD 300 million in new rotor production lines and R&D into composite brake materials; venture funding into lightweight rotor startups rose by 35% in the past 18 months.

Innovation & Future Outlook: Key innovations include AI‑based braking system diagnostics, composite rotor modules for EVs, and expansion into autonomous vehicle braking platforms—positioning the ventilated disc brake market for sustained growth and integration into next‑gen mobility ecosystems.

In supporting industry sectors such as passenger cars (~65 %), commercial vehicles (~25 %) and aftermarket performance upgrades (~10 %), the ventilated disc brakes market is witnessing product innovations like carbon‑ceramic rotor variants and ventilated‑multi‑vane designs. Regulatory emphasis on braking safety, economic growth in APAC markets, and rising EV production are reshaping consumption patterns—emerging trends indicate lightweight rotor adoption and integrated sensor‑enabled brake modules will drive the market forward toward 2032 and beyond.

The ventilated disc brakes market holds strategic relevance across the global automotive value chain as manufacturers push for superior braking performance, compliance with evolving safety norms, and weight reduction targets. For instance, comparing next‑generation composite ventilated rotors delivers approximately 12% improvement in thermal dissipation compared to older solid disc rotors. In Asia Pacific, high vehicle volumes dominate in terms of production, while North America leads in enterprise adoption with over 58% of OEMs integrating advanced ventilated disc systems. By 2027, predictive maintenance platforms embedded with sensor‑enabled ventilated disc systems are expected to reduce maintenance downtime by up to 15%. Firms are also committing to ESG metrics such as achieving a 25% recycling rate of rotor materials by 2030.

In 2024, a Japanese OEM achieved a 9% reduction in unsprung mass through deployment of a carbon‑ceramic ventilated disc rotor module. Looking ahead, the ventilated disc brakes market will act as a pillar of resilience, compliance and sustainable growth—bridging safety, lightweight innovation and electrified mobility across global vehicle platforms.

The Automotive Ventilated Disc Brakes Market is driven by trends such as heightened safety regulation, increased vehicle production volumes and growing adoption of electric and hybrid vehicles that demand enhanced braking systems. Thermal management remains critical for performance vehicles and commercial platforms, which boosts the preference for ventilated disc systems. Lightweight materials, multi‑vane rotor geometry and smart integration are key influences shaping the industry. Decision‑makers in brake system manufacturing are prioritising partnerships with OEMs and material science firms to keep pace with global mobility transformation.

Electrification of vehicles introduces regenerative braking, which places different thermal and mechanical demands on braking systems. Ventilated disc brakes deliver superior heat dissipation, accommodating higher energy recovery cycles and braking loads in EVs and hybrids. With more than 30% of global passenger vehicle production projected to be electrified by 2030, brake rotor systems must adapt. Manufacturers are increasing investment in ventilated disc systems compatible with electro‑regenerative platforms and are collaborating on rotor designs optimized for low‑wear and high‑thermal throughput conditions—thereby enhancing market growth for ventilated disc brakes.

The adoption of advanced ventilated rotor systems often requires premium materials such as carbon‑ceramic composites or lightweight aluminum alloys, which carry higher raw‑material and processing costs. Additionally, supply‑chain disruptions in critical materials (e.g., rare ceramics, high‑grade alloys) introduce volatility. The extended lead times for tooling and rotor machining in multiple‑vane ventilation designs add production complexity. For manufacturers operating on tighter margins, this cost pressure and complexity act as a restraint on widespread deployment of ventilated disc brakes, particularly in cost‑sensitive vehicle segments in emerging markets.

As vehicle OEMs pursue weight reduction and enhanced vehicle dynamics, ventilated disc brake systems present an opportunity to offer both improved performance and reduced unsprung mass. Lightweight rotor variants using composite materials can achieve mass savings of 10‑20 % compared with traditional steel rotors. High‑performance and luxury vehicle segments are increasingly specifying ventilated disc rotors with smart sensors, enhancing braking feedback and monitoring wear in real time. This opens systemic opportunities in aftermarket upgrades, EV and hybrid platforms, and sport/performance vehicle niches—areas where ventilated disc brake systems are becoming a premium specification rather than a cost‑add.

Emerging brake‑by‑wire (BBW) systems and high‑voltage vehicle architectures demand brake components that integrate electronics, actuators and sensor systems, thereby increasing component complexity. Ventilated disc rotor systems must now interface with electronic control units, monitor rotor temperature and wear, and support adaptive control algorithms. This integration challenge demands higher R&D investment, system validation and longer time to market. Moreover, ensuring reliability under high‑voltage environments and achieving compliance with both mechanical and electronic safety standards (such as ISO 26262) pose additional barriers for manufacturers seeking to scale ventilated disc brake systems across multiple vehicle generations.

Increasing Material Innovation: The average rotor weight for newer ventilated disc systems declined by approximately 12% in 2024 compared with legacy models, driven by adoption of aluminum‑silicon carbide composites and multi‑vane designs. This weight reduction enhances vehicle efficiency and performance.

Expansion of Aftermarket Upgrades: In 2024, aftermarket sales of ventilated disc rotor systems grew roughly 2.5 times faster than OEM installations in performance vehicle segments, reflecting rising consumer demand for brake system upgrades in developed markets.

Integration of Smart Braking Technologies: More than 18% of new ventilated disc brake modules launched in 2024 include embedded temperature and wear sensors linked to vehicle telematics systems, enabling predictive maintenance and reducing unsprung mass further by up to 5%.

Regional Manufacturing Shift and Localization: Asia Pacific manufacturers expanded rotor production capacity by nearly 15% in 2024, with Japan and Korea sourcing over 30% of rotor components domestically, reducing logistical cost and improving supply‑chain responsiveness.

The Automotive Ventilated Disc Brakes Market is segmented across types, applications, and end-users, reflecting the diverse demands of modern vehicles. By type, rotors are classified into solid, ventilated, and composite variants, each designed to address specific thermal and performance requirements. Applications span passenger vehicles, commercial vehicles, and specialty vehicles, with passenger cars maintaining a strong adoption footprint due to urban mobility growth and rising safety standards. End-user segmentation emphasizes OEMs, aftermarket service providers, and performance tuning enterprises, with OEMs leading due to integration in new vehicle production lines. Market dynamics are increasingly influenced by technological upgrades, material innovations, and regional production shifts, as decision-makers focus on efficiency, safety compliance, and sustainable brake solutions across global automotive fleets.

Ventilated disc rotors are the leading type, currently accounting for approximately 65% of the market, due to their superior thermal management and reduced brake fade in high-performance and heavy-duty vehicles. Solid disc rotors contribute around 20% of the segment, serving standard passenger and light commercial vehicles. Composite and carbon-ceramic ventilated rotors make up the remaining 15%, favored in luxury, performance, and electric vehicle applications for weight reduction and enhanced longevity. The fastest-growing type is carbon-ceramic ventilated rotors, driven by increasing EV adoption, performance vehicle requirements, and lightweight material innovation. Production of these rotors has accelerated, with several OEMs reporting a 20% year-on-year increase in output for 2024.

Passenger vehicles dominate the applications segment, holding roughly 70% of usage, due to rising urban vehicle production and stringent braking safety requirements. Commercial vehicles contribute 20%, where high-load applications demand consistent thermal performance and reliability. Specialty vehicles—including performance cars, electric vehicles, and off-road machinery—account for the remaining 10%. The fastest-growing application is electric vehicles, supported by trends in urban electrification and regenerative braking systems, which require advanced ventilated disc systems to manage heat and braking efficiency. In 2024, more than 38% of European EV manufacturers integrated ventilated disc rotors with smart sensor technology to optimize regenerative braking efficiency.

OEMs remain the primary end-users, representing around 68% of market consumption, as new vehicle production increasingly incorporates ventilated disc brakes to meet safety regulations and performance benchmarks. Aftermarket service providers account for 20%, servicing maintenance, upgrades, and performance enhancement markets. Specialty performance and tuning shops contribute the remaining 12%, focusing on high-performance or custom applications. The fastest-growing end-user segment is EV and hybrid manufacturers, fueled by the need for lightweight, thermally efficient brake systems compatible with regenerative braking. In 2024, adoption by these manufacturers rose by 22%, reflecting the push for enhanced braking efficiency in urban fleets.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

In 2024, Asia-Pacific’s ventilated disc brakes market volume exceeded USD 133 Million, driven by high vehicle production in China (over 26 million units), India (4.5 million units), and Japan (8.2 million units). Investments in advanced rotor manufacturing exceeded USD 1.8 Billion, while adoption of multi-vane and composite ventilated discs rose by 15% year-on-year. Rapid urbanization, increased EV production, and enhanced OEM supply chain integration have contributed to sustained demand. Additionally, over 42% of passenger vehicles in the region now feature ventilated disc rotors, highlighting strong end-user adoption and technological uptake across multiple segments.

North America accounted for 30% of the global ventilated disc brakes market in 2024, with key industries including passenger vehicles, commercial trucks, and high-performance sports cars driving demand. Regulatory initiatives such as enhanced federal vehicle safety standards and EPA guidelines have accelerated adoption of advanced braking systems. Technological transformation includes integration of sensor-enabled rotors and predictive maintenance analytics, enhancing safety and performance monitoring. A local player, Brembo North America, recently introduced ventilated carbon-ceramic disc rotors for luxury EVs, improving braking efficiency by 12%. Regional consumer behavior reflects higher enterprise adoption in high-performance vehicles, fleet management, and commercial transport sectors, emphasizing precision, reliability, and reduced maintenance cycles.

Europe held 22% of the ventilated disc brakes market in 2024, led by Germany, the UK, and France. Regulatory pressure from bodies like the European Union’s General Vehicle Safety Regulations and sustainability initiatives is driving demand for high-efficiency, recyclable rotor systems. Emerging technologies include sensor-integrated rotors, carbon-ceramic variants, and digitally monitored thermal performance systems. Local player Bosch expanded its production of ventilated rotors in Germany, supplying OEMs with over 3 million units in 2024. European consumer behavior emphasizes compliance, safety, and eco-friendly solutions, with 45% of new vehicle buyers prioritizing brake systems that meet advanced regulatory standards.

Asia-Pacific represented 38% of the global ventilated disc brakes market in 2024, with China, Japan, and India as top-consuming countries. Infrastructure expansion and high vehicle production volumes underpin demand, with China producing over 26 million vehicles in 2024. Technological innovation hubs in Japan and South Korea are introducing multi-vane, composite, and sensor-integrated rotors. Local player Nissin Brake Co., Ltd. increased its manufacturing output by 15%, supplying advanced ventilated disc systems for EVs and performance cars. Regional consumer behavior reflects rapid adoption in urban mobility, fleet transport, and premium vehicle segments, driven by technological reliability and enhanced thermal management.

South America accounted for 7% of the global ventilated disc brakes market in 2024, with Brazil and Argentina as the key contributors. Infrastructure modernization and increased adoption in commercial transport and light vehicle sectors are driving growth. Government incentives, including reduced import duties on automotive components, are enhancing accessibility. A local player, Randon S.A., expanded its rotor production line in 2024, producing over 120,000 units for commercial and passenger vehicles. Regional consumer behavior emphasizes vehicle reliability, maintenance efficiency, and alignment with evolving local regulations, with adoption tied to fleet modernization programs and urban mobility initiatives.

Middle East & Africa represented 3% of the ventilated disc brakes market in 2024, driven by demand in oil & gas, construction, and high-end passenger vehicles. Major growth countries include UAE and South Africa, where industrial expansion and fleet upgrades necessitate advanced brake systems. Technological modernization includes the adoption of heat-resistant rotors and sensor-enabled performance monitoring. Local player ATE Automotive partnered with UAE vehicle fleets in 2024 to introduce over 50,000 advanced ventilated disc rotors, enhancing braking consistency under high-load conditions. Regional consumer behavior reflects preference for durability, operational efficiency, and compliance with local transport safety standards.

China – 28% Market Share: High vehicle production capacity and extensive OEM integration drive widespread adoption of advanced ventilated disc systems.

United States – 18% Market Share: Strong end-user demand across passenger, commercial, and performance vehicles, supported by regulatory safety mandates and advanced technology integration.

The Automotive Ventilated Disc Brakes Market is highly competitive and moderately consolidated, with over 75 active global players operating across OEM and aftermarket segments. The top five companies—Brembo, Bosch, ATE, Nissin Brake Co., and Akebono—collectively account for approximately 48% of the total market share, reflecting a mix of dominant leaders and regional specialists. Strategic initiatives shaping competition include product innovation, mergers and acquisitions, regional expansion, and partnerships with automotive OEMs and EV manufacturers. In 2024, Brembo launched over 1.2 million ventilated disc rotors for high-performance and electric vehicles, while Bosch expanded sensor-integrated rotor production lines by 15%, signaling a focus on smart braking technologies. Innovation trends influencing the market include multi-vane ventilated discs, carbon-ceramic composite rotors, AI-assisted thermal management systems, and predictive maintenance solutions. The market’s nature remains moderately consolidated at the top tier but highly fragmented among smaller regional manufacturers, creating opportunities for technological differentiation and strategic alliances to capture niche market segments.

ATE Automotive

Nissin Brake Co., Ltd.

Mando Corporation

Continental AG

TRW Automotive

Technological innovation is a key driver of the Automotive Ventilated Disc Brakes Market, with current trends emphasizing enhanced thermal management, lightweight materials, and sensor-enabled monitoring systems. Multi-vane ventilated discs now account for over 40% of newly produced rotors, offering improved heat dissipation and reduced brake fade in high-performance and EV applications. Carbon-ceramic composite rotors are gaining traction, especially in luxury and electric vehicle segments, providing a 10-15% weight reduction compared to conventional steel rotors. Smart braking systems integrating embedded sensors and AI algorithms enable real-time monitoring of temperature, wear, and braking force, enhancing predictive maintenance and operational safety. Digitalization has also transformed manufacturing processes, with automated CNC machining and additive manufacturing techniques improving precision and consistency across rotor production lines. Emerging technologies include adaptive brake-by-wire systems, AI-assisted thermal regulation, and integration with vehicle telematics, all contributing to improved performance, energy efficiency, and compliance with increasingly stringent safety standards. Manufacturers are actively investing in R&D to optimize rotor designs for hybrid and EV platforms, aligning technological advancements with sustainability and vehicle performance goals.

In March 2024, Brembo introduced a new lightweight carbon-ceramic ventilated disc rotor for EVs, achieving a 12% reduction in unsprung mass and improved thermal performance. Source: www.brembo.com

In July 2023, Bosch launched sensor-integrated ventilated disc brakes with real-time wear monitoring for fleet vehicles, improving predictive maintenance accuracy by 15%. Source: www.bosch.com

In September 2023, Akebono Brake Industry Co., Ltd. expanded production of multi-vane ventilated rotors in Japan by 20%, targeting high-performance and hybrid vehicle markets. Source: www.akebono-brake.com

In January 2024, Nissin Brake Co., Ltd. completed the installation of automated CNC rotor manufacturing lines, increasing production efficiency by 18% and reducing defect rates in ventilated disc components.

The scope of the Automotive Ventilated Disc Brakes Market Report encompasses a comprehensive analysis of product types, applications, end-user segments, and geographic coverage. The report evaluates ventilated, solid, and composite disc rotors across passenger vehicles, commercial vehicles, and specialty applications, with particular attention to OEM and aftermarket adoption. It details technological trends, including carbon-ceramic composites, multi-vane ventilation, AI-assisted thermal management, and smart sensor integration. Regionally, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting production hubs, manufacturing capacities, and infrastructure trends. End-user insights include passenger vehicles, commercial trucks, EVs, and performance-focused applications. The analysis also extends to emerging and niche markets, such as high-performance EV rotors and smart braking modules, examining R&D investments, innovation initiatives, and regulatory compliance factors. Overall, the report provides decision-makers with a detailed overview of the competitive landscape, market dynamics, and future pathways, supporting strategic planning, investment prioritization, and technology adoption in the ventilated disc brakes sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 350.0 Million |

| Market Revenue (2032) | USD 579.2 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Brembo, Bosch, Akebono, ATE Automotive, Nissin Brake Co., Ltd., Mando Corporation, Continental AG, TRW Automotive |

| Customization & Pricing | Available on Request (10% Customization is Free) |