Reports

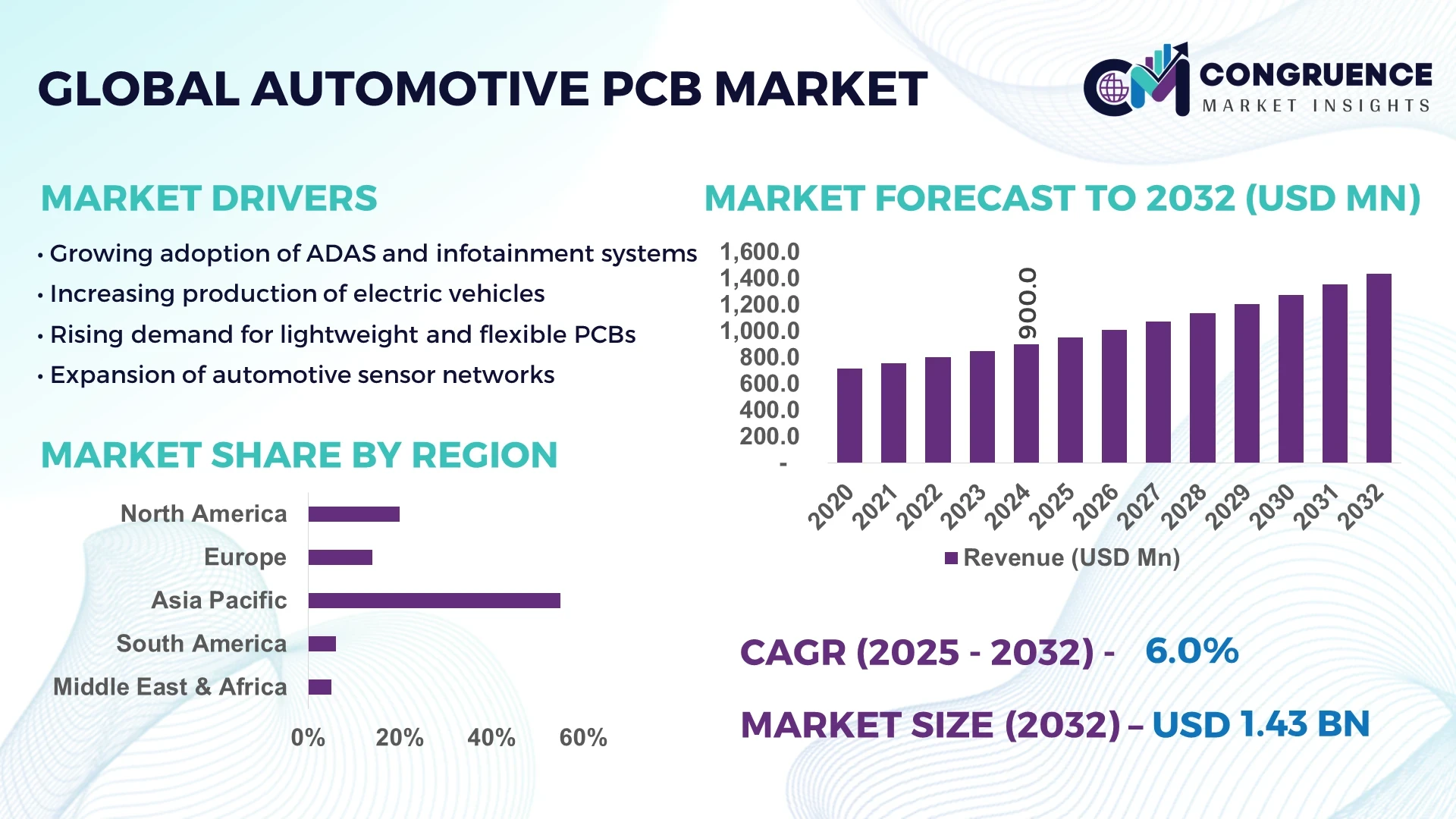

The Global Automotive PCB Market was valued at USD 900.0 Million in 2024 and is anticipated to reach a value of USD 1,434.5 Million by 2032, expanding at a CAGR of 6% between 2025 and 2032. This growth is driven by the increasing integration of electronic components in vehicles, including advanced driver assistance systems (ADAS), infotainment systems, and electric vehicle (EV) architectures.

China stands as a dominant force in the automotive PCB market, with substantial investments in manufacturing capacity and technological advancements. The country has been actively promoting the localization of semiconductor production, aiming for a 20–25% local sourcing target for automotive chips by 2025. This initiative is expected to bolster China's position in the global automotive PCB market.

Market Size & Growth: USD 900.0 Million in 2024; projected to reach USD 1,434.5 Million by 2032; CAGR of 6%.

Top Growth Drivers: EV adoption (25%), ADAS integration (20%), infotainment demand (15%).

Short-Term Forecast: By 2026, ADAS-related PCB applications are expected to improve system reliability by 30%.

Emerging Technologies: HDI PCBs, flexible PCBs, and 5G-enabled modules.

Regional Leaders: Asia Pacific: USD 1,050 Million by 2032; North America: USD 220 Million; Europe: USD 160 Million.

Consumer/End-User Trends: Increased adoption of EVs and premium vehicles driving demand.

Pilot or Case Example: In 2024, a major automaker reduced PCB-related defects by 25% through AI-driven quality control.

Competitive Landscape: Leading players include TTM Technologies (20%), Unimicron (15%), and Zhen Ding Technology (12%).

Regulatory & ESG Impact: Stricter safety standards and sustainability initiatives influencing PCB design and manufacturing.

Investment & Funding Patterns: Over USD 1 billion invested in PCB R&D and production facilities in 2024.

Innovation & Future Outlook: Advancements in 5G and AI technologies expected to drive next-generation PCB designs.

The automotive PCB market is characterized by rapid technological advancements and a shift towards more complex and reliable electronic systems. Key industry sectors such as ADAS, infotainment, and EV powertrains are witnessing significant growth, leading to increased demand for high-performance PCBs. Technological innovations, coupled with favorable regulatory frameworks, are expected to further propel market expansion.

The automotive PCB market is strategically significant as it underpins the electronic infrastructure of modern vehicles. With the shift towards electric and autonomous vehicles, the demand for advanced PCBs is escalating. For instance, HDI PCBs offer up to 40% more compact designs compared to traditional PCBs, facilitating the integration of more features in limited spaces.

Regionally, Asia Pacific dominates in volume, while North America leads in adoption, with over 60% of enterprises integrating advanced PCBs into their vehicle models. By 2027, the adoption of AI-driven PCB testing is expected to reduce defect rates by 35%, enhancing overall vehicle reliability.

In compliance with ESG metrics, firms are committing to a 20% reduction in PCB manufacturing waste by 2030, aligning with global sustainability goals. For example, in 2024, a European automaker achieved a 15% reduction in PCB-related waste through process optimization and material innovation.

Positioning the automotive PCB market as a pillar of resilience, compliance, and sustainable growth is imperative for stakeholders aiming to capitalize on the evolving automotive landscape.

The automotive PCB market is influenced by several dynamics, including technological advancements, regulatory changes, and shifting consumer preferences. The increasing complexity of vehicle electronics necessitates the development of more sophisticated PCBs. Additionally, regulatory pressures for enhanced safety and environmental sustainability are driving innovation in PCB design and manufacturing processes.

The surge in electric vehicle (EV) adoption is significantly impacting the automotive PCB market. EVs require advanced PCBs to manage high-voltage systems, battery management units, and electric drivetrains. This demand is prompting manufacturers to develop specialized PCBs that can withstand the unique challenges posed by EV architectures.

The high cost of advanced PCB materials, such as high-density interconnects (HDI) and flexible substrates, poses a challenge to the automotive PCB market. These materials are essential for the miniaturization and enhanced performance of vehicle electronics but can increase production costs, potentially impacting the affordability of vehicles.

The development of autonomous driving technologies presents significant opportunities for the automotive PCB market. Autonomous vehicles require a multitude of sensors, processors, and communication modules, all of which rely on advanced PCBs. This demand is driving innovation and growth in the PCB sector, with companies investing in research and development to meet these needs.

Supply chain disruptions, such as those caused by geopolitical tensions or natural disasters, can significantly affect the automotive PCB market. These disruptions can lead to delays in the procurement of raw materials and components, affecting production timelines and increasing costs for manufacturers.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the automotive PCB market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI in PCB Testing: The integration of artificial intelligence in PCB testing is enhancing the efficiency and accuracy of quality control processes. AI algorithms can detect defects and anomalies in PCBs with higher precision, reducing the likelihood of failures in automotive applications.

Shift Towards Sustainable Materials: There is a growing trend towards the use of sustainable materials in PCB manufacturing. Companies are exploring eco-friendly substrates and lead-free soldering techniques to align with environmental regulations and consumer preferences for green technologies.

Advancements in 5G-Enabled PCBs: The rollout of 5G networks is driving the development of PCBs that can support higher data transmission speeds and lower latency. These advancements are crucial for the implementation of connected vehicle technologies and smart transportation systems.

The Global Automotive PCB Market is strategically segmented by type, application, and end-user, providing a granular view of industry dynamics and adoption patterns. By type, the market is divided into single-sided, double-sided, and multi-layer PCBs, each designed for specific performance requirements and complexity levels. Application segmentation encompasses ADAS systems, infotainment units, electric powertrains, lighting modules, and sensor networks, reflecting the expanding role of electronics in modern vehicles. End-user insights cover passenger cars, commercial vehicles, and electric vehicles, highlighting differences in technology adoption and integration intensity. Regional consumption patterns, technological sophistication, and regulatory compliance are crucial factors influencing segmentation, with Asia Pacific demonstrating robust adoption across all categories. These segments together allow manufacturers and stakeholders to strategically allocate resources, optimize production, and address growing demand in high-value applications while identifying emerging niche opportunities within the automotive electronics ecosystem.

Among PCB types, multi-layer PCBs currently lead the market, accounting for 48% of adoption, due to their ability to support complex circuits required in ADAS and infotainment systems. Double-sided PCBs hold 30% of adoption, offering a balance between functionality and cost-effectiveness, while single-sided PCBs contribute the remaining 22%, primarily serving simpler electronic modules. The fastest-growing type is flexible PCBs, driven by the increasing integration of compact electronic components and dynamic automotive designs, expected to gain significant traction due to their lightweight and space-saving characteristics.

ADAS systems are the leading application segment, representing 40% of the market, as modern vehicles increasingly rely on advanced safety features including adaptive cruise control, lane-keeping assist, and automated parking modules. Infotainment systems hold 25% of adoption, driven by consumer demand for connectivity and multimedia integration, while electric powertrain modules account for 20%. The fastest-growing application is sensor networks, fueled by the proliferation of LiDAR, radar, and camera systems, enabling higher accuracy in autonomous driving systems. Consumer adoption trends reveal that over 35% of premium vehicle manufacturers globally implemented advanced sensor-based PCB modules in 2024, while 60% of Gen Z consumers prefer vehicles with integrated smart technologies.

The passenger car segment dominates the automotive PCB market with 55% adoption, driven by the widespread integration of advanced electronic systems in mid-to-high-end vehicles. The fastest-growing end-user is electric vehicles, with accelerated growth due to expanding battery and powertrain requirements. Commercial vehicles contribute 20% of the market, focusing on fleet management and telematics, while the remaining 25% consists of specialty and niche vehicles. Consumer adoption statistics indicate that over 38% of OEMs globally piloted EV-specific PCB modules in 2024, and 42% of North American fleets are testing connected vehicle technologies.

Asia-Pacific accounted for the largest market share at 55% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6% between 2025 and 2032.

In 2024, Asia-Pacific recorded a market volume of approximately USD 495 million, with China, Japan, and India contributing over 70% collectively. The region has over 150 major automotive PCB manufacturers, supporting high adoption in electric vehicles and infotainment systems. Regional consumer trends indicate increased preference for smart mobility solutions, with more than 60% of consumers in China and Japan seeking EVs equipped with advanced driver assistance systems (ADAS). Growing investments in R&D, local manufacturing expansions, and technology integration hubs have positioned Asia-Pacific as the core production and innovation center for automotive PCBs, influencing global supply and adoption patterns significantly.

North America holds a market share of approximately 25% in 2024, driven by strong adoption in passenger vehicles, EVs, and commercial fleets. Key industries, including automotive manufacturing, electronics, and defense, are driving demand for multi-layer and flexible PCBs. Regulatory support from bodies such as NHTSA and incentives for EV adoption encourage rapid deployment of advanced automotive electronics. Technological advancements include AI-enabled quality control, connected car modules, and smart sensor integration. Local players, such as TTM Technologies, are expanding capacity to support EV battery management and ADAS applications. Regional consumer behavior favors vehicles with high connectivity and digital integration, with over 55% of North American buyers prioritizing smart infotainment and safety technologies.

Europe accounted for 18% of the global automotive PCB market in 2024, with Germany, the UK, and France being key contributors. Regulatory pressures from the EU and sustainability initiatives are driving the adoption of environmentally friendly materials and lead-free PCB designs. The integration of advanced technologies such as HDI, flexible PCBs, and 5G-enabled modules is increasing across passenger and commercial vehicles. Local players like Unimicron Europe are investing in AI-assisted PCB testing to improve reliability and reduce waste. European consumer behavior reflects high demand for explainable and eco-compliant automotive electronics, with over 50% of consumers in Germany and France preferring vehicles with verified sustainability standards.

Asia-Pacific represents the largest regional market with 55% of the global volume in 2024, led by China, Japan, and India. Manufacturing trends include expansion of high-precision PCB production facilities and advanced automation. Top consuming countries like China account for 35% of production capacity, while India and Japan contribute 15% and 10%, respectively. Regional tech trends include AI-enabled PCB testing, flexible circuit adoption, and EV-specific designs. Local players such as Zhen Ding Technology are investing in multi-layer and HDI PCBs for electric powertrains. Consumer behavior shows strong adoption of EVs and connected vehicle technologies, with over 65% of new vehicles in Japan incorporating advanced infotainment modules.

South America accounted for approximately 6% of the global automotive PCB market in 2024, with Brazil and Argentina as the key contributors. Growth is supported by expanding vehicle manufacturing hubs, energy sector modernization, and government incentives for local production. Companies are exploring partnerships and trade agreements to streamline PCB imports and technology transfers. Local players, such as Eltek Brazil, focus on producing PCBs for commercial vehicle electrification and telematics systems. Consumer behavior trends include demand for localized infotainment and language-specific navigation systems, with over 40% of vehicle buyers in Brazil preferring smart automotive technologies tailored to regional needs.

Middle East & Africa contributed 5% of the global automotive PCB market in 2024, with UAE and South Africa leading regional demand. Growth is fueled by modernization in automotive infrastructure, oil & gas sector integration, and investment in EV infrastructure. Technological modernization includes smart sensors and digital dashboards for fleet management. Local players, such as Advanced Electronics UAE, are producing multi-layer PCBs for commercial and electric vehicles. Consumer behavior shows higher adoption in luxury and commercial vehicles, with over 30% of UAE buyers favoring connected vehicle technologies and smart fleet solutions.

China - 35% Market Share: Strong production capacity and high adoption of EVs and ADAS systems.

United States - 25% Market Share: Advanced technological integration and government incentives for EV and smart automotive electronics.

The Automotive PCB Market is characterized by a moderately fragmented competitive environment, with over 200 active global competitors, ranging from large-scale manufacturers to specialized niche players. The top 5 companies collectively account for approximately 75% of the market, reflecting a concentrated presence of key innovators. Leading companies, including TTM Technologies, Unimicron, NEOTech, Ibiden, and AT&S, are actively pursuing strategic initiatives such as partnerships, capacity expansions, and product innovations to strengthen their market positioning. In 2024 alone, over 50 new multi-layer and flexible PCB production lines were commissioned globally, reflecting ongoing investment in advanced manufacturing. Innovation trends focus on HDI PCBs, flexible and rigid-flex designs, AI-assisted quality testing, and 5G-enabled modules, driving differentiation among competitors. Market positioning strategies also include collaborations with OEMs, supply chain localization, and integration of environmentally sustainable manufacturing practices. With the increasing demand for EVs, ADAS, and connected infotainment systems, companies are competing to enhance product reliability, minimize failure rates, and capture growth opportunities in emerging regions such as Asia-Pacific and North America, reinforcing the strategic importance of technological leadership and operational efficiency.

AT&S

Ibiden

Tripod Technology

Meiko Electronics

Shenzhen Fastprint Circuit Tech

Daeduck Electronics

The Automotive PCB Market is increasingly shaped by high-density interconnect (HDI) PCBs, flexible PCBs, and rigid-flex technologies. HDI PCBs are critical for supporting advanced electronic architectures in EVs and ADAS systems, enabling up to 40% more compact layouts compared to conventional boards. Flexible PCBs facilitate weight reduction, space optimization, and improved thermal management, crucial for battery management systems and infotainment modules. Emerging technologies such as AI-assisted PCB testing enhance defect detection by over 30%, reducing production downtime and ensuring higher reliability. 5G-enabled PCBs are becoming essential to meet the data transmission and latency requirements of connected vehicles and autonomous systems. In addition, sustainable PCB materials, including lead-free solder and bio-based substrates, are being increasingly adopted, supporting environmental compliance and regulatory standards.

Companies like NEOTech are developing advanced multi-layer and flexible PCBs for electric powertrains and sensor fusion modules, improving thermal management and signal accuracy. Integration of automated assembly lines, high-precision laser drilling, and advanced inspection systems strengthens manufacturing efficiency, product reliability, and competitive differentiation across the global market.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths. Source: www.lapp.com

In March 2024, TTM Technologies launched a new series of multi-layer PCBs for EV battery management systems, enabling more compact designs and enhancing thermal performance by 15%, supporting next-generation electric vehicles. Source: www.ttm.com

In November 2023, Unimicron announced the expansion of its advanced PCB production facility in Taiwan, adding 12,000 square meters of manufacturing space to support high-demand ADAS and infotainment applications. Source: www.unimicron.com

In August 2024, NEOTech introduced flexible PCBs optimized for electric vehicle sensor networks, improving signal transmission accuracy by 18% and reducing assembly space by 12%, enhancing performance in high-density automotive electronics. Source: www.neotech.com

The scope of the Automotive PCB Market Report provides a comprehensive analysis of product types, applications, and end-user segments, including single-sided, double-sided, multi-layer, and flexible PCBs. The report examines applications across ADAS systems, infotainment modules, electric powertrains, lighting systems, and sensor networks, emphasizing technological relevance and adoption trends. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional manufacturing capabilities, consumption patterns, and innovation hubs. Emerging technologies covered include HDI, rigid-flex, and flexible PCBs, AI-assisted testing, 5G-enabled modules, and sustainable PCB materials, alongside niche segments like battery management and autonomous vehicle electronics.

The report also highlights industry focus areas, covering passenger cars, commercial vehicles, and electric vehicles, providing insights into adoption, regulatory compliance, and infrastructure developments. Key company strategies, competitive landscape, innovation initiatives, and investment trends are included, enabling decision-makers to identify growth opportunities, assess technology readiness, and plan strategic expansions in the highly competitive and evolving Automotive PCB ecosystem, including contributions from NEOTech, TTM Technologies, Unimicron, and other leading players.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 900.0 Million |

| Market Revenue (2032) | USD 1,434.5 Million |

| CAGR (2025–2032) | 6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | TTM Technologies, Unimicron Technology Corporation, NEOTech, AT&S, Ibiden, Tripod Technology, Meiko Electronics, Shenzhen Fastprint Circuit Tech, Daeduck Electronics |

| Customization & Pricing | Available on Request (10% Customization is Free) |