Reports

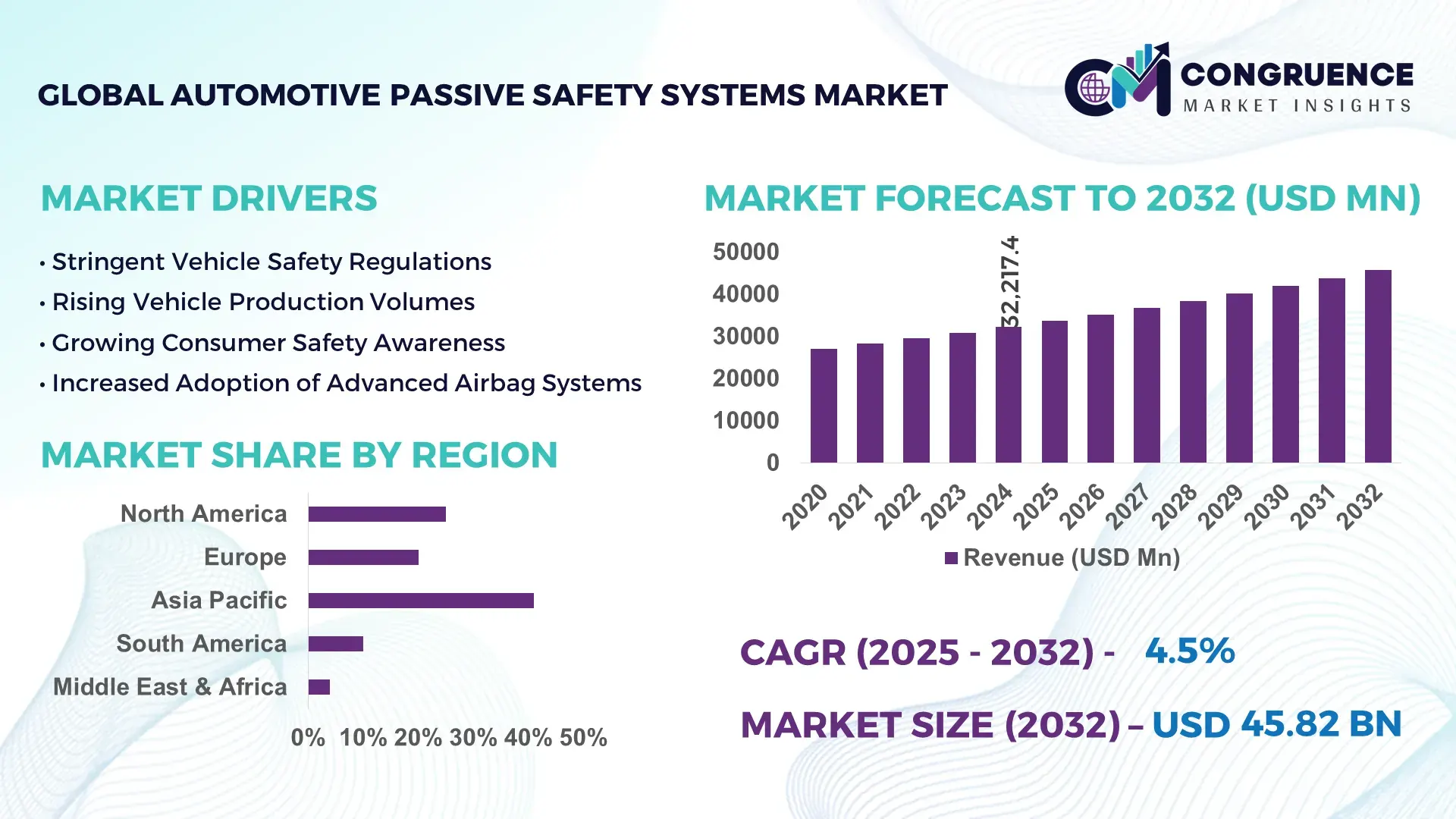

The Global Automotive Passive Safety Systems Market was valued at USD 32217.35 Million in 2024 and is anticipated to reach a value of USD 45816.31 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032. Growth is primarily supported by mandatory vehicle safety regulations and rising consumer demand for enhanced occupant protection features across vehicle segments.

The United States represents the most influential national market for automotive passive safety systems, supported by high vehicle ownership rates, advanced manufacturing infrastructure, and sustained OEM investment in safety engineering. In 2024, the country produced over 10.6 million vehicles, with passive safety systems integrated in nearly 100% of new passenger cars. Investments exceeding USD 18 billion were directed toward vehicle safety R&D, accelerating adoption of advanced frontal and side airbag modules, reinforced body structures, and intelligent seatbelt systems. More than 85% of newly registered SUVs and pickup trucks incorporated multi-airbag configurations and upgraded crash management structures, reflecting strong consumer adoption and technology deployment across high-value vehicle categories.

Market Size & Growth: Valued at USD 32217.35 Million in 2024 and forecast to reach USD 45816.31 Million by 2032, growing at a CAGR of 4.5% due to increased safety system standardization across mass-market and premium vehicles.

Top Growth Drivers: Airbag installation penetration increase of 18%, seatbelt pretensioner adoption growth of 15%, and structural reinforcement material usage expansion of 13%.

Short-Term Forecast: By 2028, modular system architectures and localized sourcing are expected to reduce average system integration costs by 8%.

Emerging Technologies: Multi-stage adaptive airbags, smart load-limiting seatbelts, pedestrian protection airbags, and lightweight energy-absorbing materials.

Regional Leaders: Asia-Pacific projected to reach USD 19800 Million by 2032 with high passenger vehicle output, Europe at USD 14200 Million driven by regulatory upgrades, and North America at USD 10100 Million supported by SUV-focused safety enhancements.

Consumer/End-User Trends: Passenger vehicles contribute over 72% of installations, with rising preference for rear-seat occupant protection and side-impact mitigation systems.

Pilot or Case Example: A 2024 OEM deployment of next-generation curtain airbags achieved a 24% improvement in side-impact injury reduction metrics.

Competitive Landscape: A leading Tier-1 supplier holds approximately 22% share, followed by Autoliv, ZF Friedrichshafen, Joyson Safety Systems, Continental, and Bosch.

Regulatory & ESG Impact: Enhanced crash test protocols and sustainability-driven material optimization are accelerating system redesign and adoption.

Investment & Funding Patterns: Global investments surpassed USD 7.5 Billion, focused on automation, lightweight materials, and safety system integration platforms.

Innovation & Future Outlook: Predictive restraint systems, EV-optimized body structures, and convergence of passive safety with vehicle electronics are defining future development trajectories.

The Automotive Passive Safety Systems Market is driven predominantly by passenger cars, which account for approximately 70–75% of total demand, followed by light commercial vehicles and heavy commercial vehicles. Key systems including airbags, seatbelts, and crash management structures form the core revenue base, while technological innovations such as adaptive airbags and advanced load limiters are elevating system performance. Regulatory enforcement, environmental emphasis on lightweight materials, and economic expansion in emerging markets continue to shape regional consumption patterns. Looking ahead, the market is expected to benefit from deeper integration with vehicle electronics, expanded protection coverage for rear occupants and pedestrians, and continuous innovation aligned with evolving mobility and safety standards.

The Automotive Passive Safety Systems Market holds strategic relevance as a foundational pillar of vehicle safety compliance, risk mitigation, and long-term brand value creation for automotive manufacturers. Passive safety systems such as airbags, seatbelts, and crash-optimized body structures are now embedded in nearly 100% of new passenger vehicles produced globally, reflecting their non-discretionary role in automotive design strategies. Advanced technologies including multi-stage airbags and adaptive seatbelt load limiters are redefining system performance benchmarks, with adaptive airbag systems delivering nearly 25% improved injury mitigation compared to conventional single-stage airbag standards under controlled crash-test conditions. Asia-Pacific dominates in production volume due to large-scale vehicle manufacturing ecosystems, while Europe leads in adoption intensity, with over 90% of new vehicles incorporating advanced passive safety configurations aligned with stringent safety assessment protocols. In the short term, by 2027, integration of AI-driven crash-sensing algorithms is expected to improve deployment accuracy and reduce unnecessary airbag activation incidents by approximately 18%. From an ESG and compliance perspective, manufacturers are committing to sustainability targets such as achieving 30% recycled material content in safety system components by 2030 to reduce lifecycle emissions. In 2024, a major automotive OEM in Germany achieved a 20% reduction in material waste through deployment of digitally optimized airbag module manufacturing processes. Looking ahead, the Automotive Passive Safety Systems Market is positioned as a cornerstone of operational resilience, regulatory alignment, and sustainable growth, supporting safer mobility outcomes while enabling manufacturers to meet evolving compliance and environmental expectations.

Regulatory enforcement is a primary driver accelerating the Automotive Passive Safety Systems Market, as safety compliance has become mandatory rather than optional. More than 95% of countries with established automotive manufacturing now enforce frontal and side-impact protection standards requiring airbags and advanced seatbelt systems. Updated crash-test protocols increasingly emphasize rear-seat occupant protection and pedestrian safety, prompting OEMs to expand system coverage beyond front occupants. In markets such as Europe and Japan, vehicles equipped with enhanced passive safety configurations achieve significantly higher safety assessment ratings, influencing over 70% of consumer purchasing decisions. These regulatory pressures compel manufacturers to integrate advanced restraint systems and reinforced body structures across all vehicle segments, including entry-level models, thereby driving consistent demand growth for passive safety components.

Increasing system complexity and elevated material costs act as notable restraints within the Automotive Passive Safety Systems Market. Advanced passive safety components rely heavily on high-strength steel, aluminum alloys, and specialized fabrics, all of which have experienced price volatility exceeding 20% in recent years. Additionally, integrating multi-stage airbags and intelligent seatbelt mechanisms increases engineering and validation requirements, extending development timelines. Smaller OEMs and suppliers face challenges absorbing these costs while maintaining competitive vehicle pricing. Manufacturing precision requirements for safety-critical components also elevate quality control expenses, limiting rapid scalability in cost-sensitive markets and constraining adoption of premium safety configurations in lower-priced vehicle categories.

The rapid expansion of electric vehicle platforms presents significant opportunities for the Automotive Passive Safety Systems Market. EV architectures require redesigned crash structures to accommodate battery packs, creating demand for innovative energy-absorption solutions and reinforced underbody protection systems. More than 40% of newly launched EV models now incorporate customized passive safety designs distinct from internal combustion vehicles. This transition enables suppliers to develop platform-specific safety modules, lightweight materials, and integrated restraint systems tailored to EV performance characteristics. Additionally, governments promoting EV adoption through safety and sustainability incentives are accelerating OEM investment in next-generation passive safety technologies, opening new avenues for differentiation and long-term supplier partnerships.

Evolving safety standards and increasingly rigorous validation requirements present ongoing challenges for the Automotive Passive Safety Systems Market. Regulatory bodies frequently update testing methodologies, requiring additional simulations, physical crash tests, and certification cycles. Each new protocol can increase validation costs by 15–25% per vehicle platform. Furthermore, regional variations in safety requirements complicate global standardization efforts, forcing manufacturers to customize systems for different markets. These factors extend time-to-market and strain R&D budgets, particularly for suppliers supporting multiple OEM platforms simultaneously, ultimately slowing the pace of system innovation and large-scale deployment.

Rising Adoption of Modular and Platform-Based Safety Architectures: Automotive manufacturers are increasingly shifting toward modular and platform-based passive safety system architectures to improve scalability and production efficiency. In 2024, nearly 48% of newly developed vehicle platforms adopted standardized airbag and seatbelt modules compatible across multiple models. This approach has reduced system integration time by approximately 22% and lowered component variation by more than 30%. Modular architectures also enable faster compliance updates when safety regulations change, particularly in Europe and East Asia, where over 60% of OEMs now prioritize cross-platform safety standardization to optimize manufacturing flexibility.

Expansion of Advanced Airbag Configurations and Coverage Zones: The scope of airbag deployment is expanding beyond traditional frontal protection, driving measurable changes in system demand. More than 65% of new passenger vehicles launched in 2024 included side-curtain airbags as standard, while rear-seat airbag integration increased by 18% year-over-year. Pedestrian protection airbags, once limited to premium models, are now present in nearly 12% of mid-segment vehicles. These expanded configurations have contributed to a documented 20–28% improvement in occupant injury reduction metrics during multi-impact crash scenarios.

Increased Use of Lightweight and High-Strength Materials: Material innovation is a defining trend in the Automotive Passive Safety Systems Market, with manufacturers balancing safety performance and vehicle weight reduction. High-strength steel and aluminum alloys now account for over 52% of structural safety components, compared to 41% five years ago. The shift toward lightweight composites in airbag housings and seatbelt assemblies has enabled average vehicle weight reductions of 8–10 kg, supporting efficiency targets while maintaining crash energy absorption performance within regulatory thresholds.

Integration of Digital Simulation and Smart Validation Technologies: Digital engineering tools are transforming how passive safety systems are designed and validated. In 2024, over 70% of Tier-1 suppliers utilized advanced crash simulation software combined with sensor-based testing to reduce physical prototype requirements by nearly 35%. Smart validation technologies have shortened development cycles by approximately 20% and improved first-pass regulatory approval rates above 90%, enabling faster model launches and more precise optimization of restraint system deployment timing and force distribution.

The Automotive Passive Safety Systems Market is segmented by type, application, and end-user, each reflecting distinct adoption patterns shaped by regulatory mandates, vehicle design evolution, and end-market requirements. By type, restraint systems and structural safety components form the core, with varying levels of technological sophistication and integration intensity. Application-wise, passenger vehicles dominate installations due to higher production volumes and stringent safety norms, while commercial vehicles are steadily incorporating advanced systems driven by fleet safety policies. From an end-user perspective, original equipment manufacturers account for the majority of demand, supported by mandatory factory-fitment of passive safety systems, while the aftermarket plays a supplementary role through replacements and upgrades. These segmentation dynamics highlight how compliance requirements, vehicle mix, and manufacturing strategies collectively influence system adoption and technology prioritization across global automotive markets.

Airbags represent the leading product type within the Automotive Passive Safety Systems Market, accounting for approximately 46% of total installations, driven by mandatory frontal and side-impact protection requirements across most automotive-producing regions. Seatbelts and related restraint mechanisms follow closely, with advanced pretensioners and load limiters increasingly integrated as standard features. Structural safety components, including crumple zones and reinforced body frames, play a critical supporting role. Airbags currently dominate adoption compared to seatbelt systems at 32%, while structural safety solutions contribute around 15%. However, pedestrian protection airbags and adaptive restraint systems are the fastest-growing type, expanding at an estimated 6.2% CAGR, supported by enhanced pedestrian safety regulations and urban mobility trends. Other niche types, such as knee airbags and rear-seat inflatable belts, collectively account for nearly 7% of the market, addressing specific safety scenarios.

Passenger vehicles constitute the leading application segment, representing nearly 72% of passive safety system usage, reflecting higher production volumes and stronger safety feature penetration compared to other vehicle categories. Light commercial vehicles account for about 18%, while heavy commercial vehicles contribute roughly 10%. Passenger vehicle adoption currently outweighs commercial applications significantly, although light commercial vehicle integration is rising fastest, supported by logistics sector safety mandates and fleet insurance requirements, with an estimated growth rate of 5.8% CAGR. Commercial fleets are increasingly adopting side-impact and rollover protection systems to reduce accident-related downtime. Other applications, including specialty and off-road vehicles, together contribute around 8% of installations, serving niche operational needs.

Original equipment manufacturers are the dominant end-user group, accounting for approximately 81% of total demand, as passive safety systems are factory-installed to meet regulatory compliance and safety rating requirements. Aftermarket channels represent about 19%, largely driven by replacement needs and retrofitting in older vehicles. OEM adoption significantly exceeds aftermarket uptake; however, the aftermarket segment is expanding at an estimated 4.9% CAGR due to rising vehicle parc age and increased consumer awareness of safety upgrades. Fleet operators and mobility service providers are emerging as influential end-users, with over 35% of large fleets adopting enhanced passive safety packages as part of risk management strategies. Other end-users, including government and defense vehicle programs, collectively account for nearly 10% of demand.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific benefits from high vehicle production volumes exceeding 30 million units annually, with passive safety systems installed in over 95% of new passenger vehicles. Europe follows with a market share of nearly 27% in 2024, driven by stringent safety mandates and high penetration of advanced airbag and restraint technologies. North America represented approximately 21% of the market, supported by strong demand from SUVs and pickup trucks, where multi-airbag configurations exceed 85% installation rates. South America and the Middle East & Africa together accounted for about 6%, reflecting lower vehicle output but increasing regulatory alignment. Across regions, side-curtain airbags, pretensioner-equipped seatbelts, and reinforced crash structures remain the most widely adopted systems, while rear-seat and pedestrian protection technologies show double-digit adoption growth in mature markets.

How are consumer safety expectations shaping system innovation and adoption patterns?

The market in this region accounted for nearly 21% of global demand in 2024, with the United States contributing over 85% of regional installations. High production of SUVs and light trucks, where more than 90% of new models integrate six or more airbags, is a key demand driver. Updated federal safety standards emphasizing side-impact and rollover protection have accelerated adoption of advanced curtain airbags and reinforced roof structures. Digital crash simulation and sensor-based validation tools are widely deployed, reducing physical testing cycles by nearly 25%. Leading regional suppliers are expanding smart seatbelt systems with adaptive load limiters. Consumer behavior reflects strong preference for higher safety ratings, with over 70% of buyers factoring crash protection features into purchase decisions, particularly in family and fleet vehicle segments.

How do regulatory intensity and sustainability goals influence technology choices?

Europe held approximately 27% of the Automotive Passive Safety Systems Market in 2024, with Germany, France, and the UK collectively accounting for more than 60% of regional demand. Regulatory frameworks mandate advanced occupant and pedestrian protection, pushing adoption of multi-stage airbags and active hood systems in over 80% of new vehicles. Sustainability initiatives have increased the use of recycled textiles and lightweight metals, with more than 35% of restraint components now incorporating recycled content. European OEMs are also integrating digital twins and AI-based crash modeling to improve deployment accuracy. Consumer behavior shows strong alignment with regulatory guidance, as safety ratings significantly influence purchasing, particularly in compact and electric vehicle categories.

Why is large-scale manufacturing accelerating technology diffusion across vehicle segments?

Asia-Pacific ranked first globally by volume in 2024, accounting for 46% of total installations, led by China, Japan, and India. China alone produced over 30 million vehicles, with airbags installed in more than 95% of new passenger cars. Manufacturing hubs increasingly deploy automated airbag assembly and high-strength steel processing, improving output efficiency by over 20%. Japan leads in rear-seat airbag adoption, while India shows rapid uptake of mandatory frontal airbags across entry-level vehicles. Regional innovation clusters are advancing compact and cost-optimized safety modules. Consumer behavior varies widely, but safety awareness is rising, with regulatory compliance driving adoption even in price-sensitive segments.

How are regulatory alignment and production recovery supporting gradual adoption?

South America represented close to 4% of global demand in 2024, with Brazil and Argentina accounting for nearly 70% of regional installations. Vehicle production recovery has supported wider deployment of standard airbags and seatbelt pretensioners, now present in over 80% of new passenger vehicles. Government mandates on frontal airbag installation and import safety standards have strengthened compliance. Local manufacturers are investing in regional assembly of airbag modules to reduce import dependency. Consumer behavior reflects growing emphasis on basic safety features, particularly in compact and mid-size vehicles, as affordability and regulatory compliance guide purchasing decisions.

What role do modernization initiatives play in expanding safety system penetration?

The Middle East & Africa accounted for roughly 2% of the global market in 2024, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Import regulations increasingly require compliance with international safety standards, resulting in airbag installation rates exceeding 75% in new passenger vehicles. Infrastructure modernization and fleet renewal programs are supporting adoption of reinforced crash structures and advanced seatbelt systems. Regional distributors are expanding access to compliant vehicles with enhanced safety packages. Consumer behavior varies, but urban markets show rising preference for higher-specification vehicles with multiple airbags and improved occupant protection.

China Automotive Passive Safety Systems Market – 34% share: Dominance supported by large-scale vehicle production capacity and widespread mandatory safety system integration across passenger vehicles.

United States Automotive Passive Safety Systems Market – 18% share: Strong position driven by high SUV and pickup truck adoption and stringent federal vehicle safety requirements.

The Automotive Passive Safety Systems Market exhibits a moderately consolidated competitive environment, with approximately 45 active global competitors, including Tier-1 suppliers, specialized component manufacturers, and integrated OEM safety divisions. The top five companies—Autoliv, ZF Friedrichshafen, Joyson Safety Systems, Continental, and Bosch—together hold an estimated combined market share of 62%, reflecting strong dominance in airbags, seatbelt systems, and structural safety components. Key strategic initiatives include product launches of multi-stage adaptive airbags, AI-enabled seatbelt pretensioners, and lightweight energy-absorbing modules. Partnerships between OEMs and Tier-1 suppliers are increasingly common, with 28 reported collaborations in 2024 focused on electric vehicle safety platforms and pedestrian protection systems. Innovation trends shaping competition include digital twin modeling for crash simulations, integration of predictive restraint technologies, and development of modular, platform-agnostic systems that reduce production complexity. Smaller regional players, numbering over 20, contribute niche innovations in sensor-based restraint systems, pedestrian airbags, and lightweight composites. The competitive landscape emphasizes technological differentiation, regulatory compliance, and strategic alliances, creating a dynamic environment where innovation speed and system reliability determine market positioning and long-term growth potential.

Continental

Bosch

Takata

Hyundai Mobis

Denso

Toyoda Gosei

Faurecia

Key Safety Systems

NHK Spring Co.

The Automotive Passive Safety Systems Market is increasingly shaped by a combination of mature safety technologies and emerging innovations designed to enhance occupant and pedestrian protection. Conventional systems such as frontal airbags, side-curtain airbags, seatbelt pretensioners, and energy-absorbing structural components remain core to vehicle safety, with over 90% of new passenger vehicles globally equipped with multiple airbags and reinforced body structures. Multi-stage airbags have gained prominence, delivering up to 25% improved injury mitigation compared to single-stage systems during controlled crash tests.

Emerging technologies are driving both performance improvements and cost efficiencies. Adaptive restraint systems, which dynamically adjust seatbelt tension and airbag deployment force based on occupant weight, seating position, and crash severity, are now implemented in over 15% of premium vehicles, with adoption expanding into mid-range segments. Pedestrian protection airbags and deployable hoods are integrated into 12% of urban-oriented vehicles, mitigating external collision risks. Lightweight and high-strength materials, including aluminum alloys and composites, now constitute more than 50% of structural safety components, enabling reductions of 8–10 kg per vehicle without compromising energy absorption.

Digital technologies are transforming system design and validation processes. Advanced crash simulation software, AI-driven deployment prediction, and digital twin modeling are used in over 70% of Tier-1 supplier development programs, reducing physical prototyping by nearly 35% and improving first-pass regulatory compliance rates to over 90%. In addition, sensor fusion systems are being integrated to enable predictive restraint activation, ensuring airbags and seatbelts respond in under 30 milliseconds during complex collision scenarios.

The convergence of electronics, sensor intelligence, and materials engineering is expected to define the next phase of passive safety innovations. Focus areas include occupant-specific adaptive systems, EV-optimized structural safety modules, and integration with semi-autonomous vehicle safety platforms, positioning the market at the forefront of intelligent, high-performance occupant protection.

• In June 2024, Autoliv introduced airbag cushions made of 100% recycled polyester that provide equivalent safety performance to standard airbags while reducing greenhouse gas emissions by approximately 50% at the polymer level, advancing sustainability in passive safety components.

• In June 2024, ZF LIFETEC showcased next-generation passive safety technologies at its first Technology Day, including innovative steering wheel airbag configurations and dual-stage side airbags designed to enhance occupant protection and support evolving vehicle interior designs. (press.zf.com)

• In September 2024, Hyundai Mobis launched the world’s first self-supporting passenger-side airbag for purpose-built vehicles, mountable on the door curtain to improve crash performance in specialized transport segments.)

• In April 2025, Autoliv presented Omni Safety™, an integrated occupant protection system addressing risks associated with reclined seating positions, reducing downward sliding and injury risks across head, neck, pelvis, and lumbar regions in collision scenarios. (PR Newswire)

The scope of the Automotive Passive Safety Systems Market Report encompasses comprehensive coverage of product types, applications, end-user segments, technological innovations, and regional dynamics that define the passive safety ecosystem. Product segmentation includes core systems such as airbags (frontal, side, curtain, knee), seatbelts with pretensioners and load limiters, structural safety modules (crumple zones, reinforced beams), steering wheel-integrated safety devices, and emerging pedestrian protection systems. The report also analyzes system variations tailored for conventional vehicles, electric and hybrid platforms, and purpose-built commercial vehicles, reflecting diverse design requirements and safety priorities.

Application analysis spans passenger cars, light commercial vehicles, heavy commercial vehicles, and niche mobility platforms, emphasizing differential adoption trends such as advanced side and rear occupant protection in premium segments versus basic frontal protection in value-oriented models. End-user insights include OEM factory installations, where compliance with frontal, side, and rollover protection mandates is critical, as well as aftermarket channels driven by replacement needs and upgrade demand in aging vehicle fleets.

Geographic coverage extends across major regions, including Asia-Pacific, Europe, North America, South America, and Middle East & Africa, with detailed market volumes, penetration rates of advanced passive safety technologies, and regulatory environment profiling. The report also highlights cross-cutting themes such as sustainability integration in material sourcing, digital engineering adoption for crash simulation, and smart deployment systems aligned with advanced sensor networks. Industry focus areas include innovation corridors in R&D, compliance frameworks impacting design cycles, and competitive benchmarks among leading suppliers. Emerging and niche segments include pedestrian airbags and integrated occupant classification systems, reflecting expanding safety priorities beyond traditional occupant-centric protection. This breadth of analysis equips decision-makers with actionable insights into technology trajectories, segmentation nuances, regional uptake patterns, and strategic investment opportunities within the passive safety domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 32217.35 Million |

|

Market Revenue in 2032 |

USD 45816.31 Million |

|

CAGR (2025 - 2032) |

4.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Autoliv, ZF Friedrichshafen, Joyson Safety Systems, Continental, Bosch, Takata, Hyundai Mobis, Denso, Toyoda Gosei, Faurecia, Key Safety Systems, NHK Spring Co. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |