Reports

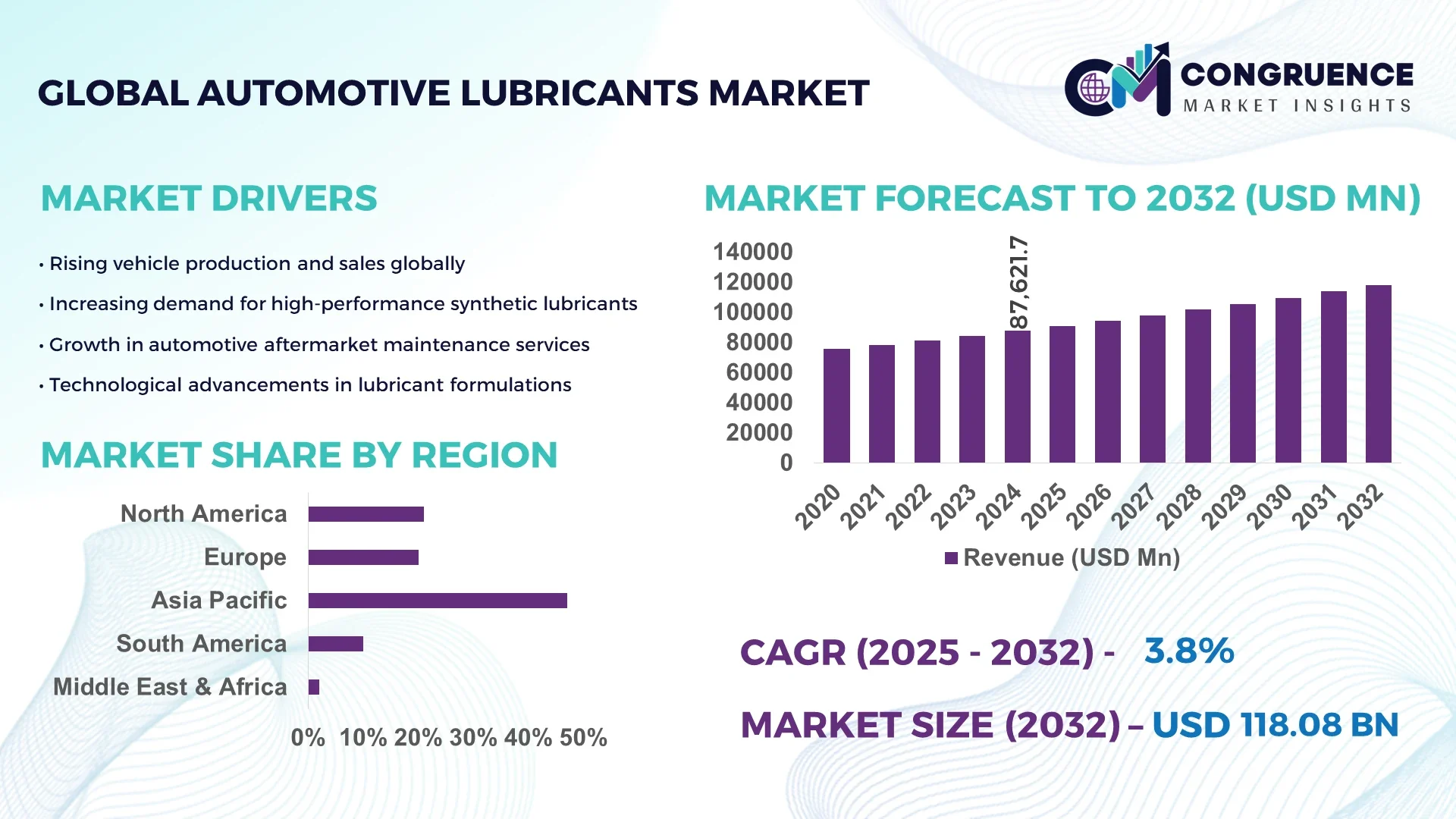

The Global Automotive Lubricants Market was valued at USD 87,621.69 Million in 2024 and is anticipated to reach a value of USD 113,760.93 Million by 2032 expanding at a CAGR of 3.8% between 2025 and 2032. The market growth is driven by increasing vehicle production and the rising demand for high-performance lubricants ensuring longer engine life and fuel efficiency.

China dominates the global automotive lubricants market, supported by its massive automotive manufacturing base and advanced production infrastructure. The country produces over 27 million vehicles annually, generating substantial lubricant demand across OEM and aftermarket channels. With more than 500 blending plants and an annual lubricant production capacity exceeding 8 million metric tons, China continues to invest heavily in synthetic and bio-based lubricant technologies. Technological advancements in additive formulations and government-backed clean energy initiatives are fostering innovation and modernization across the domestic lubricant manufacturing sector.

Market Size & Growth: Valued at USD 87,621.69 Million in 2024, projected to reach USD 113,760.93 Million by 2032, expanding at a CAGR of 3.8% driven by the growing global automotive fleet and increasing focus on efficient engine performance.

Top Growth Drivers: Rising adoption of synthetic lubricants (41%), improved fuel efficiency through advanced additives (32%), and growth in EV-compatible lubricants (27%).

Short-Term Forecast: By 2028, lubricant formulation efficiency is expected to improve by 22%, reducing overall maintenance costs by 15%.

Emerging Technologies: AI-based condition monitoring, nanotechnology-infused lubricants, and biodegradable lubricant formulations are reshaping the industry landscape.

Regional Leaders: Asia-Pacific projected to reach USD 53,420 Million by 2032 with strong OEM demand; North America at USD 28,750 Million led by premium-grade synthetic oils; Europe at USD 21,590 Million driven by emission-compliant formulations.

Consumer/End-User Trends: Increasing lubricant replacement intervals among passenger cars and fleet operators adopting predictive maintenance models.

Pilot or Case Example: In 2024, a pilot by a leading OEM achieved a 19% reduction in lubricant consumption per vehicle through optimized viscosity formulations.

Competitive Landscape: Shell leads with approximately 12% market share, followed by ExxonMobil, BP, TotalEnergies, Chevron, and Fuchs Petrolub.

Regulatory & ESG Impact: Stricter emission norms and circular economy initiatives promoting eco-friendly, low-viscosity, and recyclable lubricants across major markets.

Investment & Funding Patterns: Over USD 2.4 Billion invested in advanced lubricant research and manufacturing expansions between 2023–2025, emphasizing sustainability and digitalization.

Innovation & Future Outlook: Integration of IoT-based lubrication systems and adoption of carbon-neutral lubricant production processes expected to redefine market competitiveness.

The automotive lubricants market continues to evolve with increasing adoption across key sectors such as passenger vehicles, commercial fleets, and electric mobility solutions. Advancements in synthetic and semi-synthetic formulations are enhancing product lifespan and reducing mechanical wear. Regulatory measures promoting low-emission and recyclable lubricants are reshaping production strategies globally. Regional consumption growth in Asia-Pacific and Europe reflects shifting economic and industrial trends, while innovations in smart lubrication systems and digital monitoring tools indicate a technologically progressive outlook for the sector through 2032.

The Automotive Lubricants Market holds significant strategic relevance as it underpins the efficiency, durability, and environmental compliance of global vehicle operations. Advanced formulations such as synthetic and bio-based lubricants have transformed performance benchmarks, with synthetic lubricants delivering a 27% improvement in thermal stability compared to traditional mineral-based oils. Asia-Pacific dominates in production volume due to its extensive vehicle manufacturing ecosystem, while Europe leads in sustainable lubricant adoption, with over 46% of enterprises transitioning toward low-viscosity, eco-certified products. By 2027, AI-driven predictive maintenance solutions are expected to reduce unplanned maintenance costs by 18% across global automotive fleets, reflecting growing integration of smart lubrication management.

Compliance trends are shaping ESG commitments, with firms pledging up to 35% reduction in lubricant waste and recycling by 2030 through closed-loop production systems and carbon-neutral blending facilities. In 2024, Germany achieved a 21% reduction in lubricant consumption per kilometer through IoT-enabled lubricant monitoring deployed in heavy-duty vehicles, demonstrating measurable efficiency outcomes from digital transformation initiatives. Strategic pathways emphasize decarbonization, digitization, and diversification into EV-compatible lubricants that ensure friction optimization for electric drivetrains. The Automotive Lubricants Market stands as a pillar of resilience, compliance, and sustainable growth—bridging technological evolution with environmental stewardship and operational excellence for the next decade.

The surge in global vehicle production and the modernization of automotive fleets are primary drivers propelling the Automotive Lubricants Market. Over 95 million vehicles were produced globally in 2023, significantly increasing demand for engine oils, transmission fluids, and greases. The expanding commercial logistics sector is accelerating lubricant consumption for maintenance of heavy-duty vehicles. New-generation lubricants designed for high-temperature stability and extended drain intervals enhance operational uptime, offering measurable productivity benefits for fleet operators. With nearly 70% of new vehicles now requiring low-viscosity or synthetic lubricants, manufacturers are scaling investments in high-performance formulations that align with advanced engine design standards.

Volatile crude oil prices and supply chain disruptions are significant restraints impacting the Automotive Lubricants Market. Since base oils constitute up to 75% of lubricant formulations, fluctuations in crude oil costs directly affect production economics. The market also faces pressure from additive supply constraints and geopolitical disruptions influencing refining capacities. Manufacturers are compelled to adjust pricing structures and inventory strategies to mitigate volatility risks. Moreover, dependency on non-renewable feedstock limits flexibility, pushing the industry toward synthetic and bio-based alternatives. These cost fluctuations challenge profit margins, particularly for small and mid-tier lubricant producers, who struggle to maintain price competitiveness amid unpredictable global supply trends.

The rapid expansion of electric and hybrid vehicles (EVs and HEVs) presents a major opportunity for innovation in the Automotive Lubricants Market. EV-compatible lubricants designed for e-axles, transmission cooling, and thermal management systems are emerging as key product categories. Global EV sales surpassed 13 million units in 2024, creating a new avenue for lubricant producers to diversify portfolios beyond conventional engine oils. Research advancements are driving formulations that reduce friction losses by 20% and enhance electrical insulation performance by 15%. The growing emphasis on low-viscosity and biodegradable solutions aligns with evolving sustainability goals, enabling lubricant manufacturers to capture future-ready market segments through technology-led differentiation.

Stringent emission norms and sustainability mandates are presenting operational and compliance challenges for the Automotive Lubricants Market. Global regulatory frameworks, including carbon neutrality targets and extended producer responsibility (EPR) laws, are forcing manufacturers to reformulate products with reduced sulfur and volatile organic compound (VOC) content. The transition to biodegradable and recyclable lubricants involves complex R&D investments and certification processes, increasing production costs. Additionally, disparities in regional compliance standards complicate global supply logistics. The requirement to balance performance with environmental safety has intensified the need for continuous innovation, making regulatory alignment a critical yet costly aspect of maintaining market competitiveness.

• Surge in Synthetic and Semi-Synthetic Lubricant Adoption: The demand for synthetic and semi-synthetic lubricants is rapidly increasing, accounting for nearly 63% of total lubricant consumption in 2024. These products offer superior oxidation stability and 28% longer oil drain intervals compared to mineral oils. OEMs are mandating synthetic lubricants in over 70% of new vehicle models due to their higher fuel efficiency and engine protection standards. The trend is particularly dominant in North America and Europe, where 52% of workshops have transitioned to using advanced synthetic formulations, reducing maintenance frequency and total lifecycle costs.

• Electrification Driving Specialized Lubricant Development: The transition toward electric vehicles (EVs) is redefining lubricant formulation strategies. By 2025, nearly 18% of all lubricant R&D projects globally will focus on EV-specific fluids. These formulations deliver 24% better heat dissipation and a 17% reduction in electrical resistance compared to standard automotive oils. Asia-Pacific leads this transition, with China producing over 3 million EV units annually, creating consistent demand for dielectric and cooling lubricants tailored to electric drivetrains and thermal management systems.

• Integration of Smart Monitoring and IoT Technologies: Digitalization is transforming lubricant performance tracking, with 36% of industrial fleets now deploying IoT-based lubrication management systems. Predictive analytics platforms can detect viscosity changes with 92% accuracy, reducing unexpected downtime by 20%. This data-driven approach enables fleet operators and OEMs to extend lubricant lifespan by an average of 15%, lowering operational costs while ensuring optimal equipment performance. Europe and North America are leading in adoption, integrating connected monitoring solutions across maintenance operations.

• Sustainable and Bio-Based Lubricant Advancements: Environmental compliance is accelerating the shift toward bio-based lubricants, which now account for 14% of global production volumes. These formulations deliver up to 31% lower carbon emissions during production and 22% higher biodegradability than petroleum-based alternatives. Government sustainability mandates and industrial recycling programs are expected to push the use of renewable base oils in over 40% of newly launched lubricant lines by 2030. The Asia-Pacific region leads in production, while Europe shows the highest adoption rate among environmentally certified industries.

The Automotive Lubricants Market is segmented based on type, application, and end-user, offering diverse insights into its evolving structure. By type, the market includes mineral, synthetic, and semi-synthetic lubricants, with synthetic lubricants emerging as the most preferred due to enhanced thermal stability and extended oil life. Application-wise, the market spans engine oil, transmission fluids, brake fluids, greases, and coolants, where engine oil dominates due to its universal necessity across vehicle types. By end-user, segments include passenger vehicles, commercial fleets, two-wheelers, and electric vehicles, each exhibiting distinct consumption behaviors. Passenger vehicles hold the largest usage volume, while EVs represent the fastest-growing user base. These segmental dynamics collectively reflect the ongoing technological evolution, sustainability priorities, and diversified consumption patterns driving future lubricant innovation and production strategies.

Synthetic lubricants currently account for 46% of total Automotive Lubricants Market consumption, driven by superior performance in temperature stability, oxidation resistance, and wear reduction. They offer 25% longer drain intervals and reduce mechanical wear by up to 18% compared to mineral oils, making them the preferred choice across OEMs and fleet operators. Semi-synthetic lubricants hold around 33% market share, balancing cost efficiency and performance benefits for mid-range and commercial vehicles. Mineral lubricants, though declining, still represent 21% of usage, mainly in older or low-cost vehicles in developing regions. The fastest-growing type is bio-based lubricants, projected to expand at a CAGR of 7.4% due to regulatory incentives promoting sustainable formulations. Together, these emerging segments represent a combined 19% share of total demand.

Engine oils dominate the Automotive Lubricants Market, accounting for approximately 48% of total consumption due to their essential role in engine performance and protection across passenger and commercial vehicles. Transmission fluids follow with 22% share, favored for maintaining smooth gear transitions and thermal management. The fastest-growing application is electric drivetrain lubricants, expanding at a CAGR of 6.8% as EV production rises globally. Brake fluids and greases collectively contribute 30% of the remaining market, serving niche but critical maintenance roles in vehicle operation. The shift toward low-viscosity lubricants and multi-functional formulations is reshaping product innovation.

Passenger vehicles lead the Automotive Lubricants Market, representing 49% of total consumption in 2024, supported by consistent maintenance schedules and growing vehicle ownership worldwide. Commercial fleets follow with 31%, driven by logistics expansion and heavy-duty vehicle utilization requiring frequent lubricant replacement cycles. Two-wheelers account for 15%, while electric vehicles comprise 5% but are the fastest-growing segment, with a CAGR of 8.2% as demand for EV-compatible lubricants increases. The top three industries—automotive manufacturing, logistics, and mobility services—collectively account for over 70% of lubricant usage. Industrial fleet operators are adopting predictive maintenance technologies that extend lubricant lifespan by up to 20%.

Asia-Pacific accounted for the largest market share at 47% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

The Asia-Pacific region leads due to its high automotive production capacity, supported by China, India, and Japan, which together manufacture over 50 million vehicles annually, driving lubricant demand across passenger and commercial fleets. Europe follows with a 23% market share, primarily due to sustainability mandates and advanced synthetic lubricant adoption. North America holds 20% of global volume, benefiting from technological advancements and strong aftermarket demand, while South America and the Middle East & Africa collectively contribute 10%, reflecting emerging industrial and logistics-driven consumption. Regional differentiation in vehicle ownership patterns, environmental policies, and digital adoption levels continues to shape market competitiveness and strategic focus for leading lubricant producers worldwide.

North America holds approximately 20% of the global Automotive Lubricants Market in 2024, driven by robust demand from industries such as automotive manufacturing, logistics, and heavy machinery. The region is witnessing an increasing shift toward synthetic lubricants, which now account for 58% of total lubricant use, supported by stringent engine efficiency standards. Regulatory measures by environmental agencies are pushing manufacturers toward low-emission, biodegradable formulations. Digital transformation is evident, with 34% of lubricant suppliers deploying predictive maintenance and IoT-driven analytics for condition monitoring. Local players such as Valvoline Inc. are investing in AI-integrated lubricant solutions to improve performance tracking. Consumer behavior in this region reflects a higher preference for premium-grade lubricants, with enterprise fleets in logistics and transport sectors showing 26% greater adoption of extended-drain formulations compared to the global average.

Europe accounts for 23% of the Automotive Lubricants Market, led by key markets including Germany, the UK, and France. The region’s lubricant demand is heavily influenced by the EU’s Green Deal policies and carbon reduction initiatives promoting biodegradable and low-viscosity lubricants. Approximately 44% of European consumers now prefer eco-certified or synthetic lubricants to meet emission compliance requirements. Germany’s advanced automotive ecosystem and strong R&D infrastructure support continuous innovation in additive chemistry and performance testing. Local producers are integrating circular economy principles into lubricant recycling systems. Notably, BP’s Castrol division has introduced climate-neutral lubricant ranges targeting industrial and passenger applications. European consumers demonstrate heightened environmental awareness, leading to 32% higher adoption of renewable lubricant products compared to other regions.

Asia-Pacific dominates the Automotive Lubricants Market with a 47% global share and remains the key production hub for both vehicles and lubricants. China, India, and Japan are the top-consuming countries, collectively accounting for over 60% of regional lubricant volume. Rapid infrastructure expansion and increasing vehicle ownership continue to boost demand. The region is also advancing in lubricant technology, with over 40% of new product developments focusing on EV-compatible and high-performance synthetic oils. Local players like Petronas and Sinopec are expanding blending capacities to meet surging domestic and export requirements. Consumer behavior in the region is characterized by a growing preference for long-drain, cost-efficient products, while e-commerce and digital retail platforms are increasing lubricant accessibility, particularly in India and Southeast Asia.

South America represents around 6% of the global Automotive Lubricants Market, with Brazil and Argentina being the primary contributors. The region’s demand is driven by the industrial, construction, and logistics sectors, supported by modernization in transport fleets and agricultural machinery. Brazil alone accounts for over 58% of regional lubricant consumption, supported by expanding automotive assembly operations. Governments are promoting industrial incentives and trade policies to attract foreign investments in lubricant production and blending plants. Local companies are focusing on cost-effective formulations adapted to tropical climates. Consumer behavior reflects a steady shift toward multi-grade and synthetic lubricants, with 19% annual growth in retail lubricant sales across urban areas, indicating rising aftermarket service engagement.

The Middle East & Africa region contributes nearly 4% of the Automotive Lubricants Market, driven by robust demand from oil & gas, mining, and construction industries. Countries such as UAE, Saudi Arabia, and South Africa lead lubricant consumption, with UAE accounting for 27% of the region’s total demand. Technological modernization in manufacturing and logistics sectors is prompting higher adoption of high-performance lubricants. Governments are implementing regional sustainability frameworks and trade partnerships to boost industrial output and downstream oil processing capabilities. Local companies are investing in automated blending technologies, enhancing product consistency and output efficiency. Consumer behavior trends show a gradual shift toward branded synthetic lubricants, with 15% higher adoption among fleet operators and industrial clients seeking longer service intervals and lower equipment downtime.

China – 33% Market Share: Dominates due to high automotive production capacity exceeding 27 million vehicles annually and rapid technological integration in lubricant manufacturing.

United States – 18% Market Share: Leads in adoption of advanced synthetic and digitalized lubricant solutions, supported by strong industrial and logistics infrastructure ensuring continuous demand.

The global Automotive Lubricants market is moderately consolidated, with the top five players collectively holding around 48% of the total market share in 2024. Industry leaders such as Shell, ExxonMobil, BP, Chevron, and TotalEnergies dominate due to extensive product portfolios, strategic global reach, and advanced R&D capabilities. More than 60 active competitors operate across international and regional markets, focusing on innovations like bio-based lubricants, high-performance synthetics, and low-viscosity solutions for electric and hybrid vehicles. In 2024 alone, over 120 product launches and 40 strategic collaborations were recorded, emphasizing technological sustainability and efficiency. Companies are increasingly adopting digital platforms for predictive maintenance and real-time performance analytics, further intensifying competition. Mergers and acquisitions remain key growth strategies, as exemplified by ExxonMobil’s acquisition of a leading Asian lubricant manufacturer, expanding its regional market presence by 6%. The market continues to evolve around innovation-driven differentiation, eco-friendly formulations, and value-added services.

Chevron Corporation

TotalEnergies SE

Valvoline Inc.

Fuchs Petrolub SE

PetroChina Company Limited

Idemitsu Kosan Co., Ltd.

Sinopec Lubricant Company

Lukoil Oil Company

Motul S.A.

ENEOS Corporation

Castrol Limited

Petronas Lubricants International

The Automotive Lubricants market is witnessing rapid technological evolution, driven by demands for improved performance, efficiency, and sustainability. Nanotechnology-enhanced additives are increasingly incorporated into formulations, enabling up to 20% lower friction coefficients than conventional additives in high-stress engine environments. Novel dispersant and anti-wear nanoparticles permit thinner lubricant films while preserving protection under high load conditions. Meanwhile, AI and machine learning algorithms are being integrated into lubrication management systems, permitting real-time adjustment of lubricant dosing and early fault detection; currently, 28% of large fleet operators use these smart systems to optimize oil change intervals.

Bio-based and renewable base oil technologies are becoming more mature, with some next-generation formulations achieving over 30% reduction in CO₂ footprints during production compared to petroleum-derived base oils. These are combined with biodegradable ester chemistries to meet tightening environmental regulations. Hybrid synthetic/bioblend technologies are enabling balanced performance in temperature extremes and offering improved oxidative stability—up to 35% higher than legacy mineral blends.

Electric and hybrid drivetrain lubricants are another emerging domain. These formulations focus on dielectric properties, thermal conductivity, and minimal particulate generation in e-axle and transmission cooling systems. New formulations now achieve 15% better heat transfer than earlier EV fluids. At the same time, smart sensors embedded in gearboxes and bearing housings monitor lubricant temperature, dielectric constant, and viscosity drift—data is fed into cloud analytics for predictive maintenance.

Experimental disruptive technologies are also under exploration. For example, aqueous colloidal gels with nano-silica particles have demonstrated friction coefficient reductions up to 97% compared to dry sliding—showing potential for ultra-low friction and self-replenishing film formation. These gels, while not yet commercial for automotive use, point toward a future where lubrication may extend beyond oil to hybrid fluid–gel systems. The interplay of digitalization, green chemistry, and advanced materials is positioning the Automotive Lubricants market as a hotbed of technology-driven transformation.

• In mid-2023, Castrol launched its new Edge ProFlex line, integrating graphene-enhanced friction modifiers to deliver up to 12% better fuel economy in passenger cars.

• In January 2024, Shell introduced its Helix Ultra 0W-20 Eco formula, reducing CO₂ lifecycle emissions by around 18% through lower base oil carbon intensity and optimized additive blends.

• In March 2024, ExxonMobil and a European OEM entered a strategic partnership to co-develop next-generation synthetic lubricants for engine downsizing, aiming at 25% improved thermal stability over current standards.

• In July 2024, TotalEnergies acquired used-oil regeneration specialist Tecoil, integrating circular economy capabilities into its lubricant business to bolster recycling and resource recovery.

This Automotive Lubricants Market Report encompasses comprehensive coverage of product types, application segments, end-user verticals, and geographic regions. On the product side, it analyzes mineral, synthetic, semi-synthetic, bio-blend, and specialty lubricants (e.g., EV cooling fluids, gear oils). In terms of applications, it examines engine oils, transmission fluids, greases, brake fluids, coolants, and emerging fluids for electric drivetrains. End-users include passenger vehicles, commercial fleets, two-wheelers, and off-road/industrial mobility fleets. Geographically, the report spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with country-level profiling in major markets such as China, USA, Germany, India, and Brazil.

It further addresses technology trends (e.g., nanomaterial additives, AI-based lubricant monitoring, biodegradable base oils, hybrid gel systems) and regulatory & ESG frameworks (e.g., emissions standards, circular economy mandates, biodegradable lubricant mandates). The report also assesses supply chain facets such as base oil sourcing, additive chemistry development, blending infrastructure, and distribution channels. Additionally, it highlights competitive strategy themes: product innovation, collaborations, M&A, aftermarket service offerings, digital platforms, and sustainability-driven differentiation. Emerging niche segments—such as aqueous gels, lubricant-infused surfaces, or plug-in lubricant monitoring tools—are also explored for their long-term disruptive potential.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 87621.69 Million |

|

Market Revenue in 2032 |

USD 113760.93 Million |

|

CAGR (2025 - 2032) |

3.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Shell plc, ExxonMobil Corporation, BP plc, Chevron Corporation, TotalEnergies SE, Valvoline Inc., Fuchs Petrolub SE, PetroChina Company Limited, Idemitsu Kosan Co., Ltd., Sinopec Lubricant Company, Lukoil Oil Company, Motul S.A., ENEOS Corporation, Castrol Limited, Petronas Lubricants International |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |